Issue #28, Volume #1

How Small Investors Can Benefit From Bond “Smart Money” Constraints

This is Porter & Co.’s free daily e-letter. Paid-up members can access their subscriber materials, including our latest recommendations and our “3 Best Buys” for our different portfolios, by going here.

Three Things You Need To Know Now:

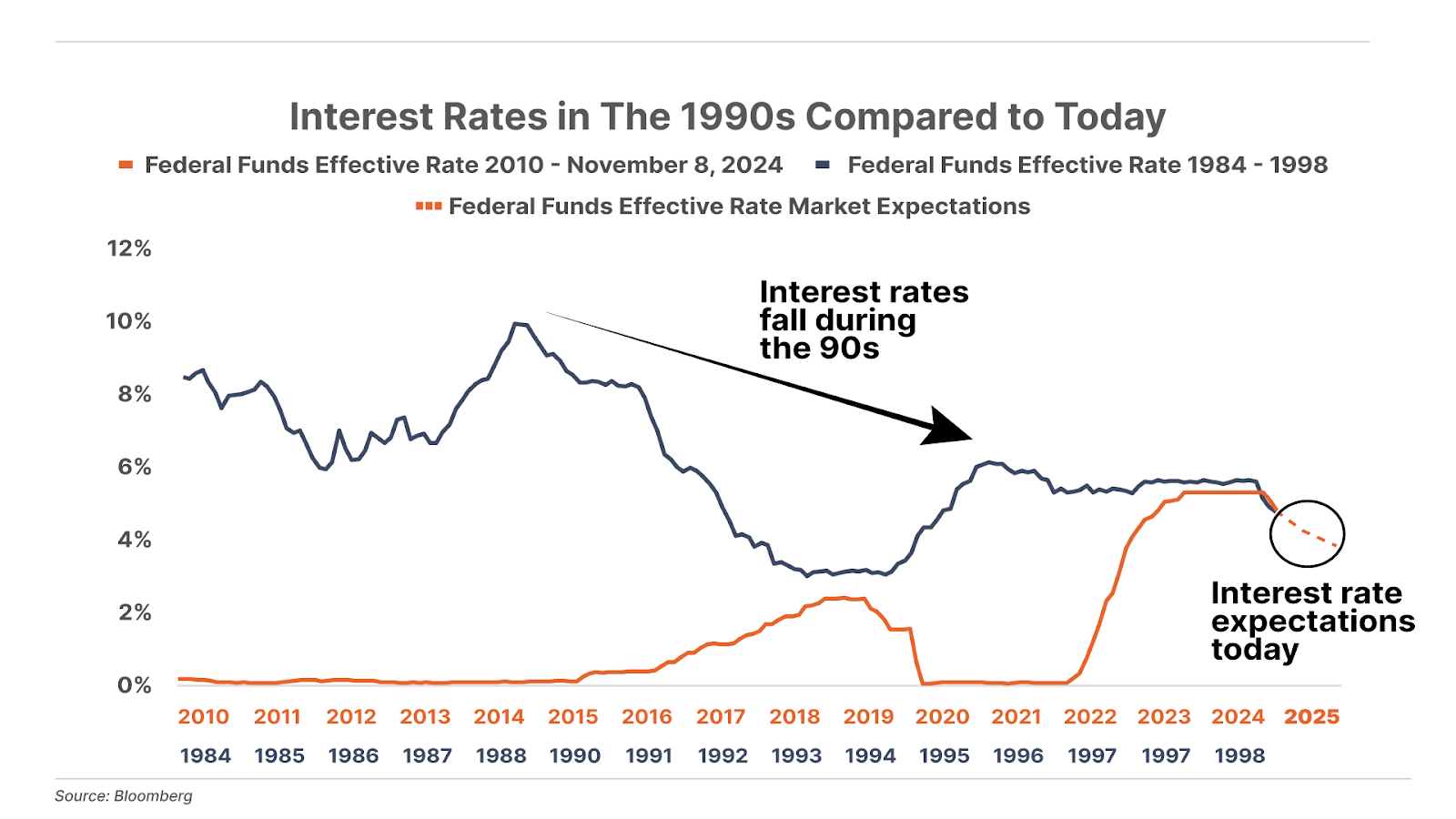

1. What’s coming up this week. After a quiet Monday on Veterans Day… oil cartel OPEC will on Tuesday be releasing their monthly update, which is likely to tell us that crude oil is still headed down. On Tuesday and Thursday, the U.S. Bureau of Labor Statistics will release monthly CPI (consumer spending) and PPI (producer prices) figures, while on Friday, the U.S. Census Bureau will come out with retail sales data. All of those numbers will likely point to higher inflation… which means little to Fed Chair Jerome Powell (scheduled to speak on Thursday). He slashed rates last week, and markets right now say there’s a 65% chance he’ll cut by another 25 basis points in December.

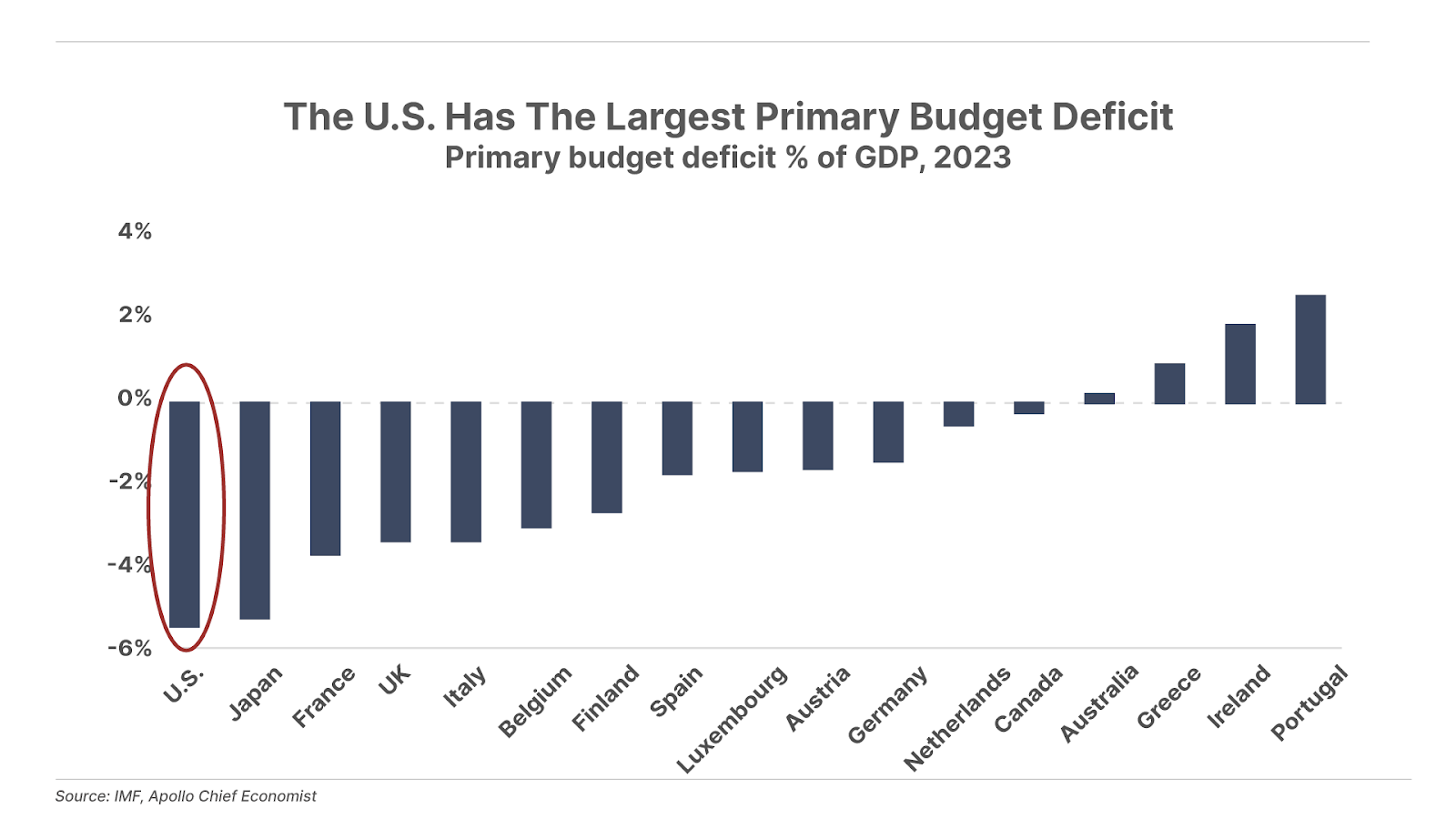

2. The U.S. is No. 1… in deficit spending. The United States government ran a primary deficit – that is, the budget deficit not including interest payments – of 5.8% of GDP last year. That’s the most of the 38 major market-based economies in the OECD (Organization for Economic Cooperation and Development), including Japan, France, the UK, Italy, Spain, Germany, and Canada, among others. This is crisis-level spending, exceeding all prior U.S. deficits outside of severe recessions (2008 and 2020) and World War II. The U.S. debt crisis is a catastrophe happening in slow motion.

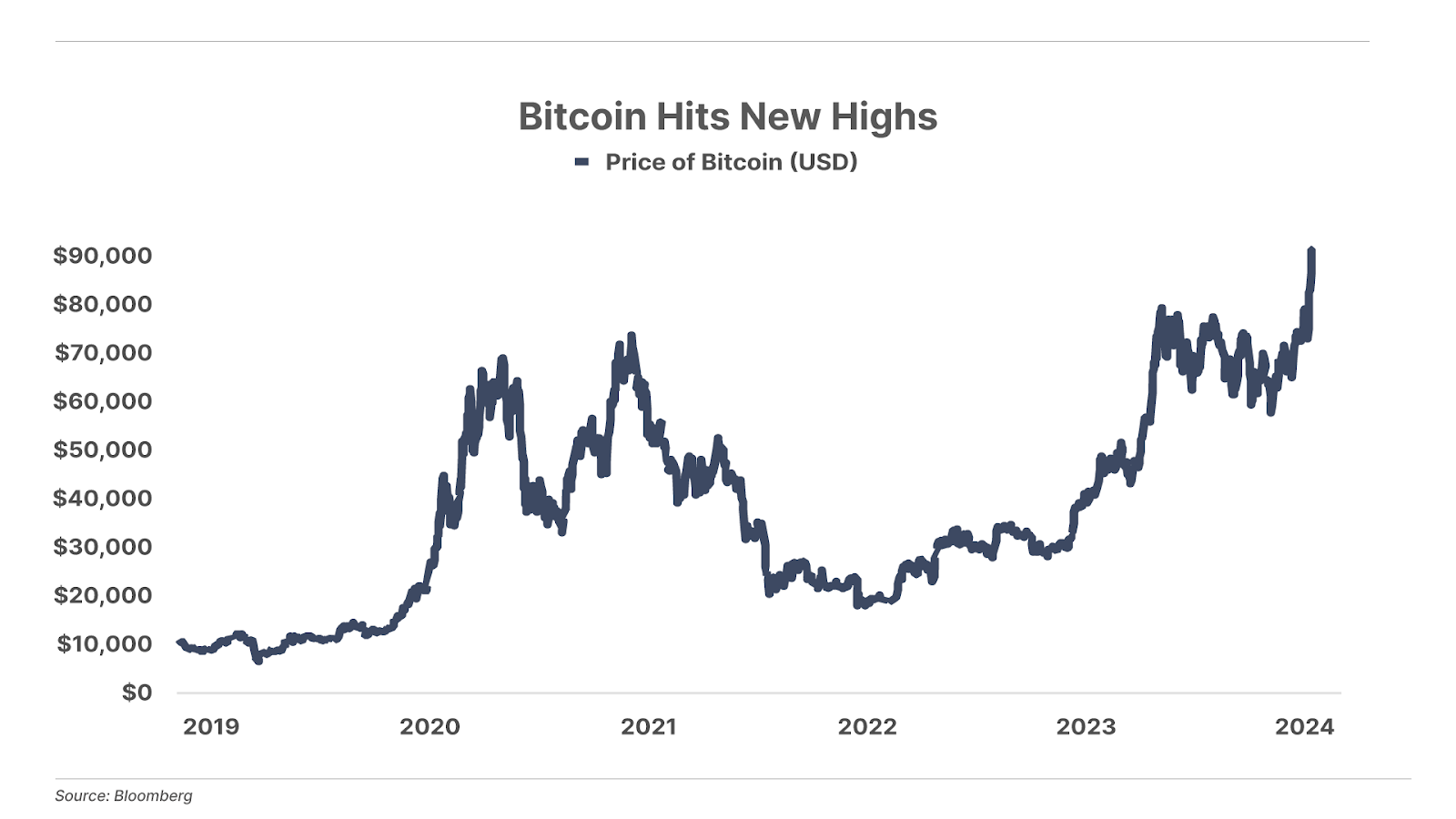

3. Trump victory pushes Bitcoin to all-time highs. With the prospect of a more favorable regulatory environment for Bitcoin under a Trump administration, the cryptocurrency has hit all-time highs. Trump has also proposed a strategic national Bitcoin stockpile – and it may be only a matter of time before some of the world’s central banks add Bitcoin to the menu of options to diversify away from the U.S. dollar. It’s up 98% in 2024 so far (compared to 26% for the S&P 500).

And one more thing…

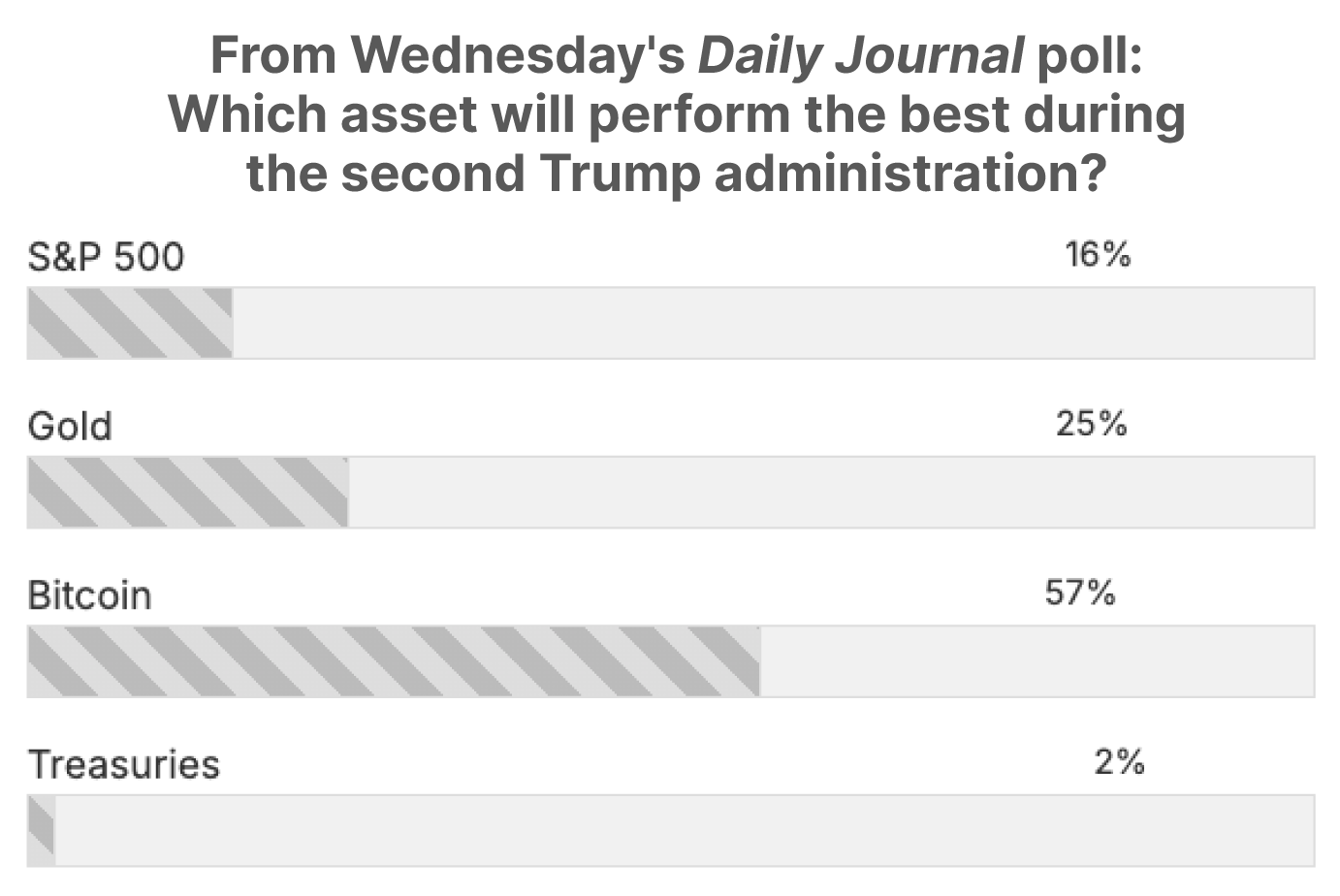

Respondents to our November 6 Daily Journal poll believe – by a significant majority – that Bitcoin is only getting started. As shown below, 57% of readers think that it will outperform stocks, gold, and Treasuries during the second Trump administration.

** 100% Gainer **

On June 14, Marty Fridson added shares of Peloton Interactive (PTON) to the Porter & Co.’s Distressed Investing portfolio. Today we sent out an alert to subscribers recommending that they sell half of their position – with the shares hitting $8.90/share at Friday’s close – to reap a profit of 124% on the total position. While most of the Distressed Investing portfolio is comprised of bonds, Marty and his team include distressed equities on occasion… and his four stock positions are up an average of 84% (!).

Marty is adding a new share position to the portfolio in the upcoming issue of Distressed Investing on Thursday. And what’s more, the economy is on the verge of tipping into an optimal environment for distressed bonds – in the post-presidential election window… Porter explains here.

“Zeroes”, Tight Spreads, and Why the CEO Rushed Back From Singapore

How Small Investors Can Benefit From Bond “Smart Money” Constraints

Marty Fridson, the lead analyst for Porter & Co.’s Distressed Investing, is a titan in his field. Called “the most well-known figure in the high-yield world” by Investor’s Digest, Marty joined Porter & Co. in March 2023. Since then he’s made about 20 recommendations – of the 13 current open positions, 11 are in the green, resulting in an average portfolio return of 29.6%.

Last month in the Daily Journal, Marty shared his experiences doing bond research at Salomon Brothers in the 1980s, around the time that Michael Lewis was at the Wall Street titan, slinging bonds and gathering material for his subsequent best-seller Liar’s Poker.

In this issue, Marty has more stories from his early days in high-yield bonds, sharing tricks – that are still in use today – about how companies looking to raise capital tend to issue new bonds into an environment that benefits them, and not investors. Marty uses his decades in the sector to provide insights into how you can get in on the right side of the bond market.

Here’s Marty…

I’ve spent most of my 47-year career on the lookout for attractive investment opportunities in low-quality (“junk”) and distressed bonds. It’s what I did at Morgan Stanley… at Merrill Lynch… at BNP Paribas… and what I do now at Porter & Co.

One day in the 1990s, when I was the director of high-yield research at Merrill Lynch, I went to a roadshow presentation in New York by the CEO of a high-flying telecom company that was looking to sell $100-million-plus of bonds (by today’s standards that’s not a large issue – but adjusted for inflation, and in the context of the bigger issuance sizes of today, it wasn’t small at all). In that pre-Zoom era, the way companies usually marketed their issuances was through lunch presentations in major financial centers. The CEO and CFO would make their case to high-yield analysts from institutional money managers.

(I attended many roadshows. Attendees knew not to ask tough questions following the presentation. It was an implicit part of the arrangement. Probe too deeply… and you probably wouldn’t be invited next time around. There were consequences to the silence, though. A lack of genuine give-and-take meant that serious flaws in a company’s finances and business plans were not addressed… often leading to painful losses for bondholders.)

During a lunch I sat next to the CEO, who mentioned that he’d just been in Singapore. “Why?” I asked, as at the time it wasn’t a regular stop on the high-yield roadshow circuit. “I was looking to raise some equity over there,” he said. “But then I heard the window for issuing zero-coupon, high-yield bonds was open. So I cut short the stock sale and caught the first plane back to New York to take advantage of the opportunity.” (More on what zero-coupon bonds are below.)

Radically changing plans so abruptly, from selling shares to selling bonds – a decision that’s critical to a company’s balance sheet, financial trajectory, and long-term planning – isn’t the way big public companies normally operate. Low-rated companies’ operating earnings cover their interest costs by relatively thin margins – and backing away from a chance to raise equity in order to ease the debt burden isn’t ordinarily something to make a snap decision about.

But this was no ordinary time. Much like in the current market, investor enthusiasm for high-yield bonds had been running super high. Then, like now, the Federal Reserve was injecting vast amounts of capital into the financial system by cutting short-term interest rates. When the Fed starts pumping up the money supply, that money eventually goes looking for somewhere to get invested. In such an environment, even companies that aren’t particularly creditworthy manage to raise capital in the new-issue high-yield market.

To cite a classic Wall Street phrase, there was too much money chasing too few deals – and the globe-trotting CEO wanted to take advantage of that dynamic. He wanted to sell bonds at a good price – rather than sell a part of the company via a share sale.

The “zeroes” the CEO was so eager to peddle are a form of financing that flourished when the bargaining power was skewed toward the issuing company and away from investors. These bonds are sold at a substantial discount to their $1,000 face value – and since they pay no interest, the only return comes from the appreciation from the discounted price to maturity. For the first several years, the company doesn’t have to shell out any cash for interest payments – hence the name “zero.” Only if the structure includes cash payments on the back end – the last few years before maturity – do bondholders receive any income.

And during the years when the company is not paying any interest, it receives tax deductions on imputed interest – interest the IRS acknowledges that you paid, even though you didn’t actually pay it. It’s done to be sure the bond holder pays tax for the entire duration of the bond, and not just on the back end – when interest is actually paid.

What a deal! A tax deduction on interest that the company doesn’t have to pay. No wonder that CEO had been so desperate to get back to New York before the window closed!

Since the 1990s, zero-coupon bonds have become a less-prominent feature of the high-yield market. But they’re a perfect example of an extreme imbalance of power between speculative-grade companies and bond buyers that still applies today.

Unless they’re in dire financing straits, companies usually have some flexibility about when they go to the market with a new issue. They have the luxury of being able to tap investors only when supply/demand conditions tilt the terms in their favor. That is to say, that’s when the balance of power for negotiating rates and terms puts investors at the maximum disadvantage.

Actually… there isn’t any negotiating to speak of. If orders for a new issue exceed the total amount being offered, the underwriters can simply dictate the price and provisions – take it or leave it, they say.

How to Take Advantage of This Power Imbalance

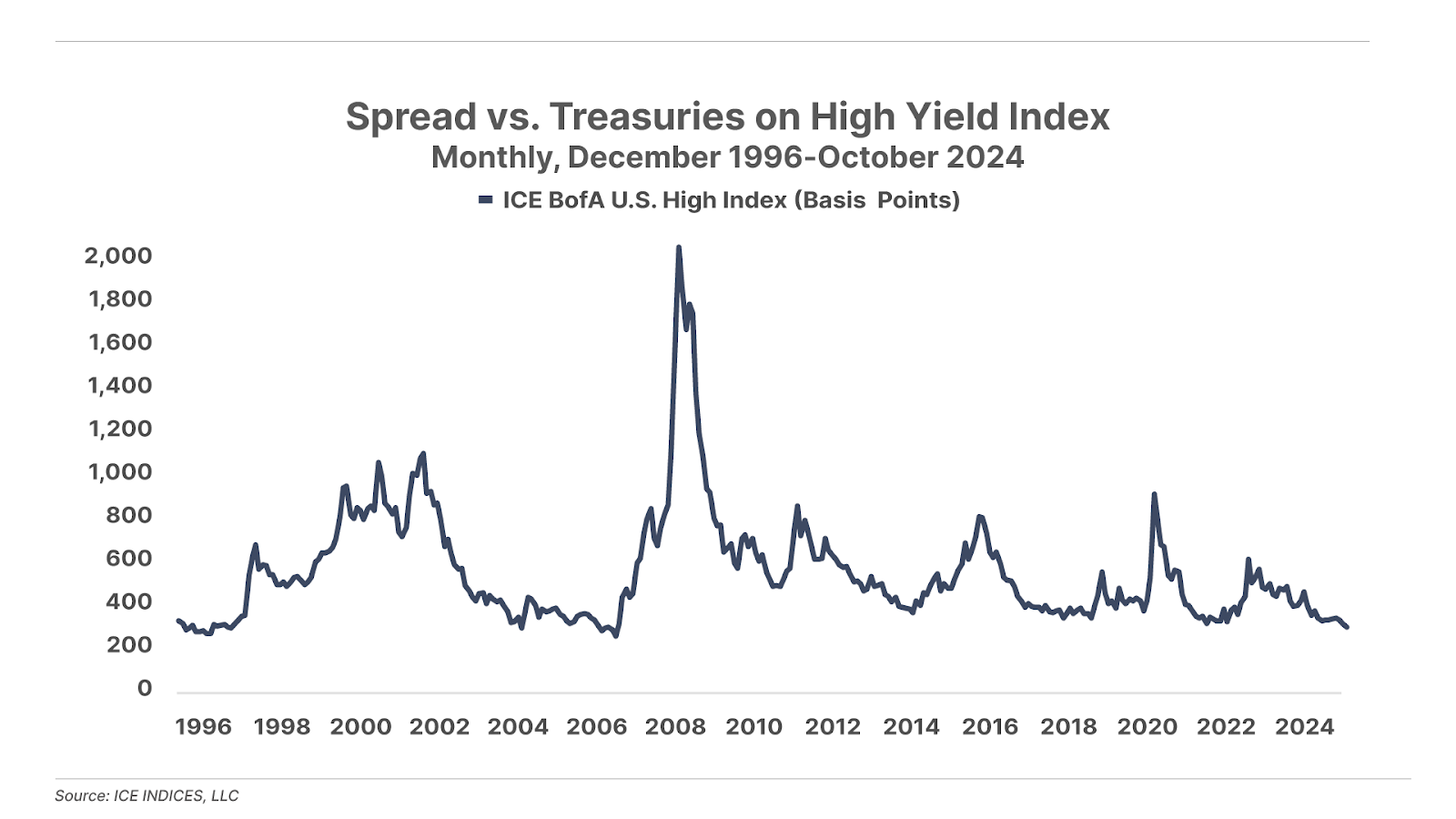

And in the current environment, with high-yield bond spreads at their tightest levels since 2007, the issuers have an unusually strong hand.

This raises a question: If new issues are offered to investors only when market conditions strongly disfavor them (that is, when they’re getting less return on their money), why do those big institutions purchase new issues? Can’t they find more attractive offerings in the secondary (resale) market when demand isn’t exceeding supply?

The practical impediment to that strategy is that the leading high-yield bond buyers, like BlackRock, Franklin Templeton, T. Rowe Price, and many other asset managers and major hedge funds, manage billions of dollars that need to be invested in the market. They don’t want to own a lot of different issues. It’s easier to keep track of fewer positions that are larger – rather than a lot of smaller positions.

As a result, the big players have little choice but to rely heavily on the new-issue market – because with these they can buy tens of millions of dollars’ worth of an issue in just one transaction. They’re buying bonds that have a less favorable risk-reward ratio than issues that are already in the market, because they have no choice – the liquidity of bonds in the secondary market is generally too low for them.

These dynamics, though, create a nice advantage for small investors. If, as a small investor, you’re looking to buy just a few thousand dollars’ or so worth of a high-yield bond issue, you can fill your needs in the secondary market. You’ll likely need patience until your order gets filled – but since you’re not looking to buy a large lot, you can find much better deals than new issues, where the bond issuer holds all the cards. (Finding these far more compelling bonds – which large investors mostly ignore because it’s not worth their while to buy small lot sizes – is what we do in Distressed Investor.)

Here’s some more good news: Distressed investors may not have to wait too long for market conditions to turn strongly in their favor. Shortly after high-yield spreads reached lows similar to today’s in 2007, the Global Financial Crisis of 2008-2009 unfolded. Currently, only 4% of outstanding high-yield bonds are trading at distressed levels. In 2008 that ratio got as high as 84%.

We won’t necessarily see that level of distress, but things can change quickly. When the big institutions are once again choking on distressed debt, investors who have kept some cash ready for just those circumstances will have a huge profit opportunity. In 2009, the ICE BofA U.S. High Yield Distressed Index as a whole delivered a 57.5% return, with many individual issues doing far better than the average.

Even in that kind of environment, you have to be choosy about which bonds you buy, but that’s when being in the driver’s seat feels really good.

We’ve been writing about how – contrary to what the head-in-the-sand Federal Reserve (and mainstream financial media) say – a recession in the U.S. economy may already be underway. That means that before long, it’s going to be the best possible environment for distressed investing – with distressed bonds the perfect counterweight as stocks suffer.

And getting in before the inauguration of the new president is critical… I explain it all here. (And… to become a subscriber, you can also call Lance James, our Director of Customer Care, at 888-610-8895, or internationally at +1 443-815-4447.)

Good investing,

Porter Stansberry,

Stevenson, MD

P.S. Bonds are not boring – at all.

But if just now you’re more excited about investing in tech… Jeff Brown is the best in the business.

Jeff is a bona fide prophet when it comes to understanding what’s next in tech.

He got his subscribers into Bitcoin in 2015… Nvidia in 2016… and AMD in 2017.

The results… Bitcoin is up 26,613%… Nvidia, 10,422%… AMD, 1,229%.

In addition to – and connected with – his uncanny ability to tell the future about the direction that technology is moving in, and who will be the winners, Jeff is one of the best stock pickers I’ve ever worked with.

And if you want to find out more about Jeff’s research (at a substantial discount to his normal prices) and get his future recommendations, go here now.

Mailbag

Paid-up Partner Pass member George writes:

Hi Porter and Aaron: Wow, I really enjoyed your latest Black Label Podcast with your special guest, Marko Papic – Chief Strategist of BCA Research. I thought it was your best podcast yet. It was entertaining, informative, passionate, and I learned a lot. Thank you.

Even though I am a proud Canadian, your negative comments about Toronto, and the economic policies of the current Canadian government are spot on. I further agree that President-elect Trump’s proposal to apply tariffs to all foreign goods entering the USA will hurt many countries but especially Canada.

I should add however, hopefully Americans will keep top of mind that in a dangerous and competitive world everyone needs a few true friends. Let’s not forget the quote by President John F. Kennedy when he said before the Canadian Parliament “Geography has made us neighbours, but history has made us friends”. Kennedy said that in 1961, but it still rings true today.

I am a Partner Pass member, and it is one of the best investments I have made. Congratulations on the quality of work produced by you and your team. I enjoy reading and viewing the content produced by Porter & Co. and appreciate the ability to render complex ideas in a simple and easy-to-read format. Your explanations on how unwarranted increases in the money supply causes inflation, and the damage it is doing to everyday citizens has made me a smarter investor. Also, Porter’s Daily Journal is a big hit with me as I am not in the habit of reading anything on Twitter (X).

I do have a couple of thoughts for you and your team to consider. With the uptick in the price of bitcoin and its increasing importance in preserving wealth, will you be updating sometime soon your thoughts regarding Bitcoin – and perhaps moving further into other cryptocurrencies such as Ethereum (and the blockchain in general)? Secondly, I wanted to mention I enjoyed listening to international financial analysts such as Pieter Slegers and Marko Papic. I hope to hear from them again.

Porter’s comment: George, thank you for your kind words (for those who haven’t listened to our latest Black Label podcast, you can find it here). We’ll be saying a lot more about Bitcoin in coming weeks and months. And yes… Pieter and Marko were fantastic podcast guests.

Paid-up Partner Pass subscriber Bob writes…

Porter, I remember meeting you for the first time at Hotel Del at Bonner’s Millennium get together in October 1999. To my great advantage, I picked up an issue of the Pirate Investor from the table in the hall. I liked your writing style (then and still) and subscribed. I added several of your letters to my reading list and finally became an Alliance Member. Apparently, I wasn’t paying attention when you started Porter & Co., but I joined as a Partner when I heard about it.

Can I tell you how much money your advice has allowed me to make? Nope. I’ve never tracked it, but I know it’s a large number. I don’t always follow your recommendations, (A friend several years ago once commented “Opportunities are infinite, my bank account isn’t.”) but I always try to “recall” your advice when considering any investment. Results? My lifestyle hasn’t really changed after my retirement 20 years ago. If anything, it’s improved.

If you keep writing, Porter, I’ll keep reading… and profiting.