“We’re All in it Together” – How Government Uses Fear to Manipulate Voters

- PREPARING FOR A “HURRICANE”

- A CURRENCY OF ENERGY: BITCOIN

- YOU CAN’T PRINT COPPER

In America, inflation began with violence.

In October 1690, the Puritans of the Massachusetts Bay Colony launched a raid on their prosperous (and French Catholic) neighbors to the north. Led by Sir William Phips, the colonists’ expeditionary force numbered 2,500 and traveled to Quebec aboard 32 ships.

Phips was a man of his time. As a sea captain and treasure hunter, he recovered a huge treasure from a sunken Spanish galleon, which made him rich and powerful. What made him popular was killing witches.

The previous spring, Phips had seized Port Royal, the Acadian capital (present-day Nova Scotia), on behalf of the British Crown, with 700 soldiers. Even though the town surrendered without a fight, Phips allowed his men to sack and plunder the town… which made a substantial economic impact on the Massachusetts economy.

In the fall, the colonists launched a larger expedition to raid Quebec. Confident in their ability to plunder the French, they hired thousands of additional soldiers, on credit.

Alas, Quebec’s leader, Count Frontenac, knew they were coming. He prepared the city’s defenses, building a stockade and mounting cannons. When Phips demanded the town’s surrender, Frontenac famously replied: “I have no reply to make other than from the mouths of my cannons and muskets.”

What followed was the typical fog of war. The colonists’ attack was stymied by, among other challenges, “a lack of rum.” Phips’ flagship Six Friends was heavily damaged when it ran out of ammunition, leading to the end of the assault. After two days of fighting, a prisoner exchange was negotiated, and the colonists’ fleet returned to Boston, empty-handed. While only 150 soldiers died of their wounds, more than 1,000 died of smallpox.

The survivors were hungry, cold, and armed. They were also owed a lot of money. The expedition racked up 5,000 pounds in debt (roughly 10,000 ounces of silver) – a fortune at the time.

Phips tried to borrow the money to pay his men from Boston’s merchants, but they doubted the Colony’s credit, and wouldn’t lend. Instead, in December 1690 the colonial government printed 7,000 pounds worth of paper money and paid off the soldiers. To gain acceptance of this new form of money (the first paper money ever issued in the New World), the Massachusetts Bay Colony made a two-fold pledge: first, that the notes would, in time, be redeemed for specie (silver or gold) at full face value, and, second, that absolutely no more notes would be printed.

What happened next is instructive. It has been repeated, in one way or another, by every subsequent government that has chosen to print money to pay its debts.

At first, the new notes gave the local economy a big boost. But… strangely… after a short boom of around two months, there was a terrible crash. All the gold and silver in the colony seemed to disappear. And, as the exchange value of the notes plummeted, there was an economic crisis.

To quell the panic, another issue of new notes had to be printed in February 1691. This issuance, because of the falling value of the notes, had to be much larger (40,000 pounds) to achieve the same economic impact as the first.

Covid Witches

Facing a growing crisis, Phips and the head of the church, Increase Mather, went to England to negotiate for more support with the new British monarchs, King William and Queen Mary. They needed a new charter, as the former King James II had been deposed. And they were hoping for a charter that would bolster their own authority. They returned to New England in the spring of 1692 with additional financial support. And Phips was named Governor. But the new charter greatly expanded the right to vote, granting the franchise to virtually every man in the colony.

How did Phips and Mather adjust to the new political reality? What’s the best way to manipulate voters? Fear.

Phips and Mather needed to focus the electorate on something they feared more than poverty. But the colonists dealt with real and terrifying threats every day – like smallpox, Indian raids, and pirates. What’s scarier than these things? What did the Puritans fear more than anything else? The devil. Puritans were consumed with a fear of going to hell. To them, the devil was a very real threat. They ascribed natural phenomena – like sickness – to witches and demons. Mather had come to power with a book about witchcraft that he published in 1684. Time to dust it off…

Phips and Mather got back to Boston on May 14, 1692.

Phips – an orphan, a treasure hunter, and a soldier of fortune – was not a religious man. But now, new royal charter in hand, Phips made ostentatious displays of piety: he halted his swearing-in ceremony to faithfully observe the Sabbath. And on May 27, less than two weeks after returning from England, Mather and Phips created a special new court, with jurists selected from the leaders of the new colonial government, to deal with the rising specter of… witchcraft.

In June the new court began hanging witches, mesmerizing the colony. Among the gruesome deaths that followed was that of Giles Corey, an 81-year-old man who was pressed to death by Captain John Gardner. It took him three days to die as heavy irons were laid on top of him, slowly crushing him. He was crushed, as opposed to hung, because he refused to cooperate with the court. That meant he couldn’t be convicted of a felony, which prevented the government from seizing his land. (Killing witches was good business for the government.)

Before the Phips raid on Quebec, there was approximately 200,000 pounds of silver money in the colony. By 1711, 740,000 pounds of paper money had been issued by various colonial governments, including an enormous 500,000-pound issue by Massachusetts to pay for, you guessed it, another failed expedition to sack Quebec!

Prices continued to rise. And, despite various efforts to control the money supply, by 1748, 2.5 million pounds worth of paper money had been printed in the colonies. Prices had increased 10-fold.

Sound familiar? Government takes on debt it cannot finance with legitimate means. Government prints money, which provides a short-term economic boom. And Gresham’s Law ensues: the bad money forces out the good, as people wisely hoard bullion and spend paper. Another crash follows. Still more money must be printed. The cycle continues. And each cycle causes more and more economic dislocation. The government is trapped: if they stop printing, the economy will collapse. If they keep printing, inflation will destroy civil society.

Why? One major problem is wages can’t keep pace with inflation. Various schemes and regulations must be instituted to try and limit the damage to the middle class. In Maryland, in 1733, when the colony decided to print 70,000 pounds worth of new paper money, 30,000 pounds were given away, in equal allotments, to each inhabitant of the colony. Of course, back then, nobody had college loans. Another appeasement technique is the granting of additional political rights, like universal suffrage for men in the colonies. We don’t think the colonists would have understood gay marriage, transgender rights, anti-racism or the ESG movement… but maybe if they printed enough money, for long enough.

But the most powerful technique for controlling the population and limiting the political blowback for inflation is simply fear. Bankrupt governments facing the collapse of their paper currencies almost always use fear to manipulate the population. What’s the first thing Phips and Mather did when confronting their crisis? Hang 20 witches and preach about the devil being in the colony. You can imagine Increase Mather saying from the pulpit: “we’re all in this together.” Or “20 witches to flatten the curve.”

And when did a new strain of flu become “Covid” – an imminent threat to the entire world? Only after the Federal Reserve tried to reduce the size of its balance sheet and return to normalized interest rates in 2018. When it realized it had to continue printing, Covid became an existential threat to the world that required massive new government powers, an abandonment of the First Amendment (the right to free assembly), health privacy, and virtually every financial norm. The Fed’s balance sheet then doubled.

The Beginning of the End of America

Our current spate of money printing began in 1998 with the bailout of hedge fund Long-Term Capital Management.

A modern-day Phips, the founder and leader of LTCM, John Meriwether, was powerful because he’d found treasure – not off the coast of Florida, but in the financial markets. Meriwether earned billions for Salomon Brothers trading bonds. Together with two Nobel Prize-winning economists, Myron Scholes and Robert Merton, the founders of LTCM were widely recognized as being the smartest men in finance.

And their hedge fund was wildly successful – at first.

They earned 40% a year, seemingly without any volatility. How? They capitalized on having access to very low-cost sources of funding. (Many of the investors in the fund were the leading executives of Wall Street’s top banks.)

By using enormous position sizes, enabled by extreme amounts of leverage (LTCM was responsible for roughly 5% of the global trading in fixed income), LTCM could make reliable profits through arbitrage. The firm would simultaneously sell and buy bonds with similar financial characteristics to capitalize on tiny differences in prices across the world’s markets.

No one else could make these trades because no one else had the capital (hundreds of billions), the computing power, the database of global bond inventory, or the algorithms to scan for relative value trades across virtually every market in the world, in real time.

Oh, and no one else would make these trades, because in virtually every position, the upside was infinitesimal… but the downside, in the event of a default, was cataclysmic.

One of the many repeating themes of paper money is the inevitable decline of liquidity as Gresham’s Law inevitably requires more and more money to be added to the system, and bad money forces out good.

A Short, Sad Primer on Bad Money

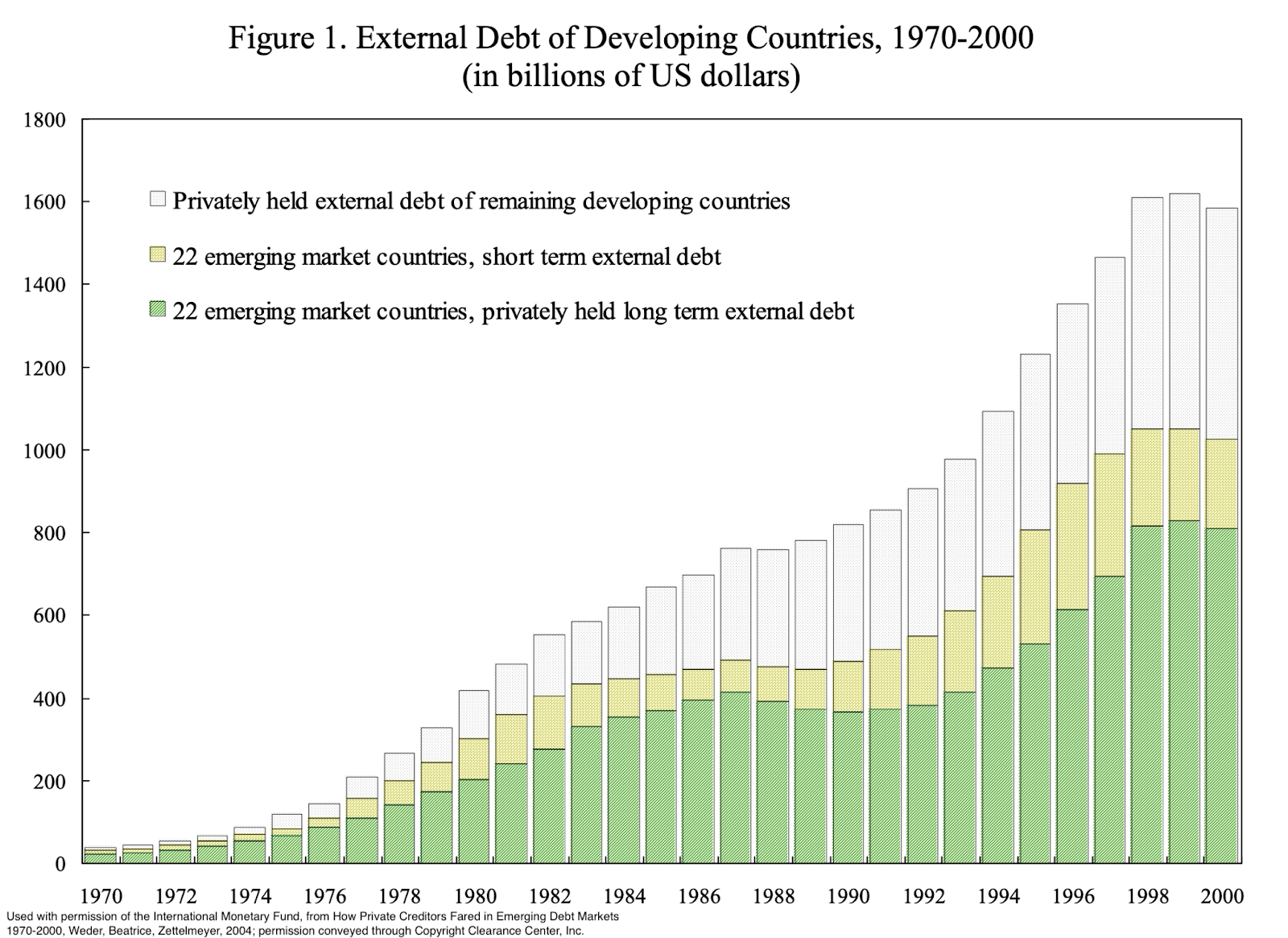

In the 1990s, the “bad money” was emerging market bonds.

In the 25 years prior to 1998, the 22 countries known as “emerging” economies had seen their external debt loads grow 10-fold, far outpacing economic activity. Beginning in 1995 with the Mexican peso crisis, virtually every emerging market in the world suffered a currency collapse, a debt default, or both. Long Term Capital Management held a highly leveraged position in Russian domestic government bonds when the Russian government defaulted in August 1998, leading to massive losses.

So… what happened? Much like when the colonial army got back to Boston, instead of suffering their losses, LTCM’s backers appealed to the government. And $3.6 billion in new money was created by a consortium of 14 banks, led by the Federal Reserve.

It was the first time the U.S. government had intervened directly to prevent credit losses by private investors since the creation of the world’s current monetary regime, the all-paper, U.S. dollar standard. It would not be the last.

About ten years later, in 2008, the “bad money” was subprime mortgage bonds, on which Wall Street banks had gorged themselves over the previous several years, creating an enormous economic boom led by real estate prices.

The resulting bailout was 10,000 times bigger than that of Long Term Capital Management. Looking at all of the direct bailouts, debt guarantees, mortgage purchases, and central bank swaps, the mortgage crisis saw $30 trillion in new money and credit.

Judging from history, we all should have known what would happen next.

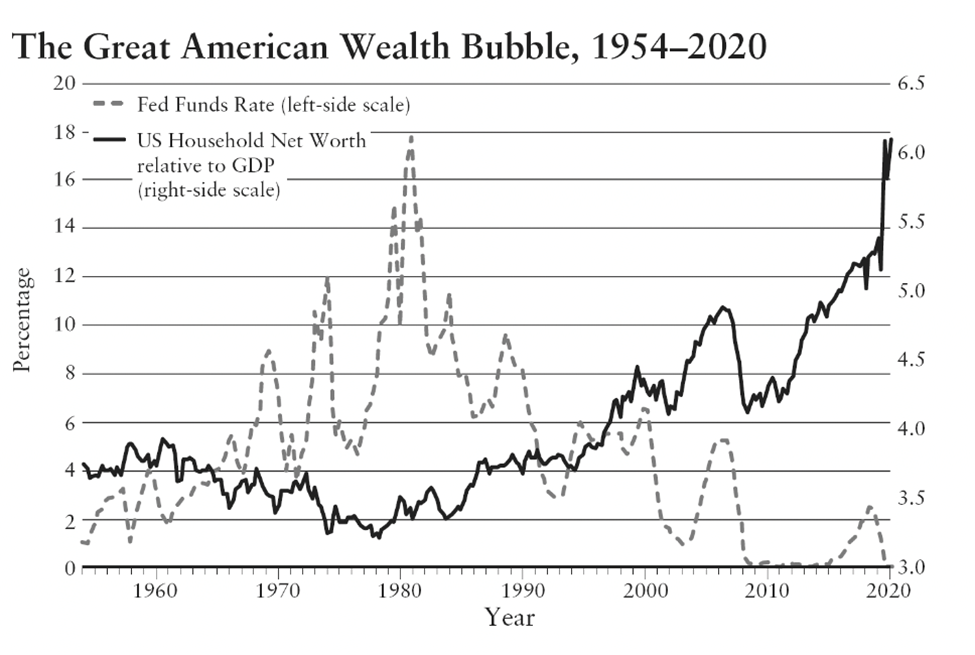

As the chart below (from The Price of Time by Edward Chancellor) shows, the late 1990s (and the bailout of LTCM) marks the beginning of America’s “super bubble,” where household net worth, as denominated in dollars, became completely untethered to any real, underlying economic activity. And with each new cycle of boom, bad money, and bust, the resulting printing of new money would grow ever larger.

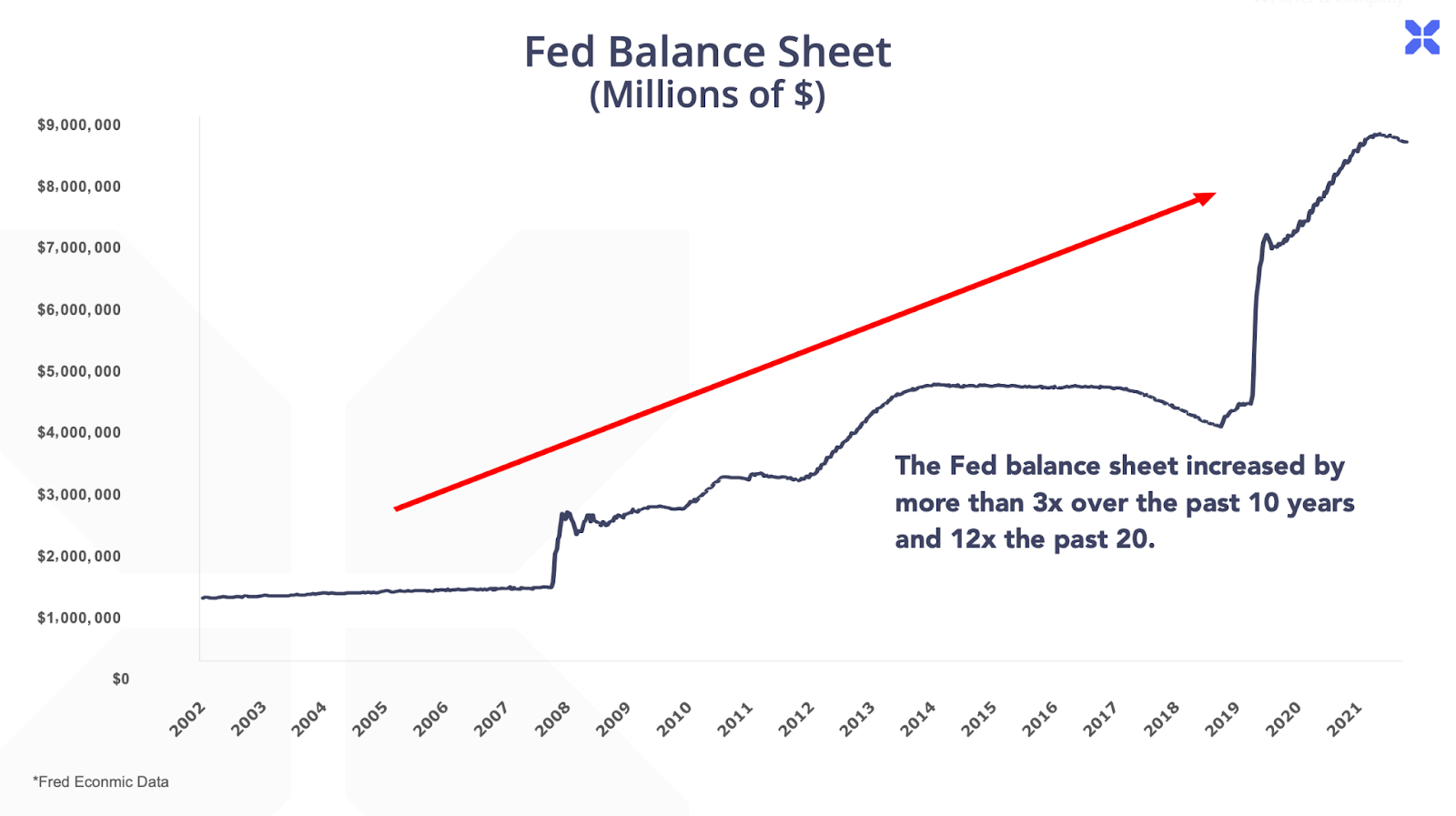

The scale of the printing is most apparent in the growth of the Federal Reserve’s balance sheet.

Our central bank printed trillions over the last 20 years to finance the bailout of Wall Street in 2009, and then again in 2011 to help solve the European debt crisis, and then, most recently, to finance the battle over Covid witches. Each successful wave of printing was bigger and bigger.

And following each expansion, the interest offered on government debt was lower and lower.

The result is a monetary system that bears little direct relationship to the allocation of real assets or services.

Deadly Paper

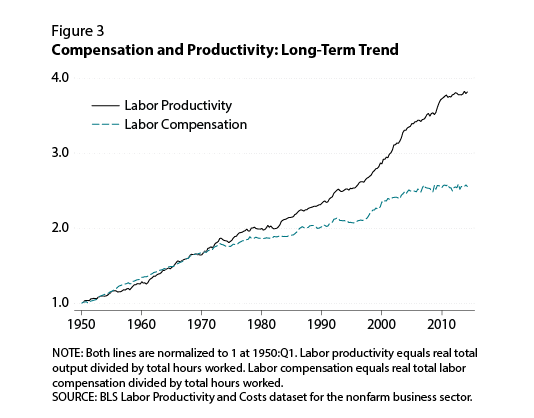

Consider the impact on wages. Since the beginning of the paper dollar standard in the 1970s, as money and credit began to expand well beyond physical limits, the value of wages became untethered to gains in productivity.

Paper money is devastating to the middle class, whose wages have declined massively relative to the soaring value of assets. That’s extremely dangerous for civil society. It creates the very real impression in the general population that the economy (and therefore the government that controls it) is illegitimate.

This is why paper money and major inflations always presage the most violent forms of populism and revolution – from the witch trials, to the rise of the Nazis, to the storming of the U.S. Capitol in 2021.

Perhaps the bigger problem, however, is that paper money is an enormous subsidy for the state. It sets the stage for virtually unlimited government budgets. That encourages people to use the government in all kinds of ways that are extremely destructive for civil society – like starting wars, whether that’s raiding Quebec or invading Iraq.

Paper money and the lack of any fundamental limit to credit and money, also leads to unrealistic projects to reorder our domestic society – because no social benefit is unaffordable. The “war on poverty” and the “war on drugs” were both launched as the U.S. switched to a pure paper currency in the 1970s.

Paper money leads to a bull market in government insanity: The U.S. is now spending more than $100 billion a year on food stamps, even though obesity is our country’s greatest health risk. And there’s no better example of paper-financed government hubris than the “war on drugs.” Surely after Prohibition’s utter failure (here and everywhere else around the world), wise leaders would question the notion of giving government control over the most private and complicated areas of our private lives. But did they? Not a chance.

Paper money also gives unprecedented power to “the money changers.” Before the 2008-2012 bailout of Wall Street, BlackRock, Wall Street’s largest firm, had $500 billion of assets under management. It grew 10x after the bailout, to $5 trillion in assets under management.

Today, following the COVID witch hunt, and the massive money printing that enabled it, BlackRock controls $10 trillion – roughly 50% of annual U.S. GDP.

Never in the history of the United States has one firm, led by one man (Larry Fink), controlled wealth equal to half our GDP. Or even 10% of it. What if the ideas that Larry Fink holds are wrong? He’s the leading and most powerful proponent of the ESG movement and wants to ban all fossil fuels by 2050. But, with so much capital under his control, who can stop him?

Paper money is also dangerous because it’s very hard to avoid the economic consequences of asset bubbles, even when it’s clear that general inflation is underway. For people who need a place to live, it hardly matters that housing prices are inflated – they have to live somewhere. For people who are retired, it hardly matters that corporate bonds have been in an enormous bubble, because they need income to survive.

But worst of all, as the monetary system becomes detached from economic reality, it can no longer perform its most important, core function – which is to guide production in the most efficient way possible. Prices convey information across our entire, enormously complex economy. Prices are what inform entrepreneurs and other value creators what to make, and what to stop making.

This, the growing inefficiency of our economic engine, is the greatest weakness of our “financialized” economy. Just as the availability of virtually unlimited credit leads governments to take on projects (like war and social experiments) that are inherently destructive, virtually unlimited funding for corporations leads to malinvestment.

These are investments that are made despite the invisible hand of supply and demand, such as renewable energy investments that make our power grid both vastly more expensive and less reliable. How many billions have been lost already on solar power? Would these investments have been made in an environment of free market interest rates and sound money? Absolutely not.

How can you track how far America has traveled on its descent into total financial collapse?

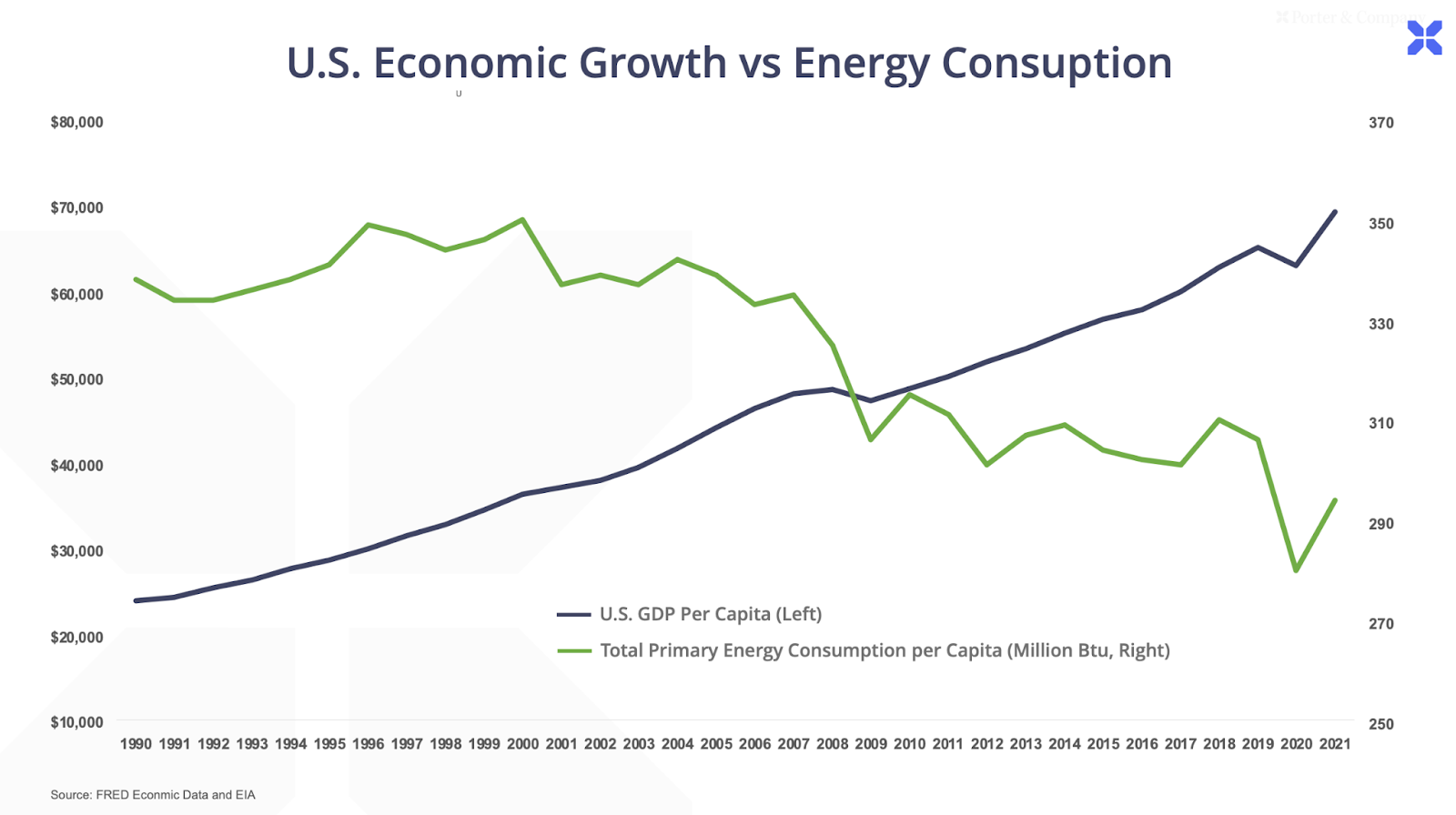

We think the best way to measure the growth of the real economy isn’t stock prices or even GDP figures, which have been impossibly warped by the ongoing inflation.

Instead, to track the real underlying economy we measure per capita energy consumption.

The Magic Energy Bullet

As societies become wealthier, more productive, and more efficient, more energy is consumed per person. Energy is almost a perfectly “elastic” commodity: the cheaper it can be produced, the more it will be consumed, with virtually no limit to potential demand. Thus, in wealthier societies, energy consumption is higher than in poorer countries.

There are, of course, some outliers, like Iceland. Thanks to its virtually unlimited, cheap geothermal power, the average person in Iceland consumes more energy, per year, than anyone else in the world, except the people of Qatar. But as the chart below shows, using energy consumption per capita offers a very good objective assessment of real wealth.

In America, energy per capita peaked in 2000, at 350 mmBtu, just before the collapse of the tech bubble. It’s since declined almost 20%.

Meanwhile, GDP, as measured in ever more rapidly printed dollars, has more than doubled.

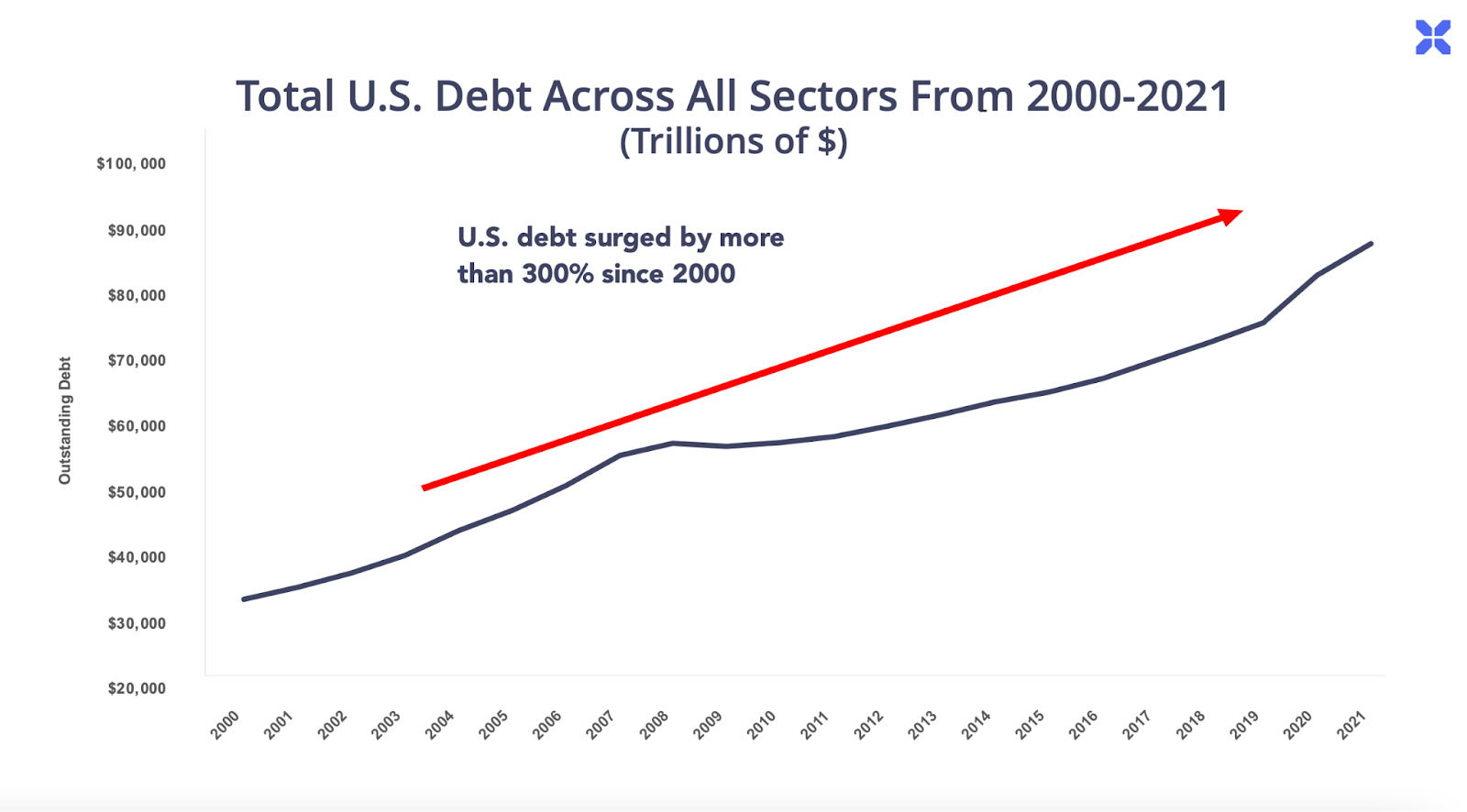

Has America’s standard of living doubled in the last 20 years? No way. But our debts sure have – they more than tripled, from less than $30 trillion to over $90 trillion.

The size of these debts, relative to the real size of our underlying economy (as measured by per capita energy consumption) have gone from a factor of 82 (highly indebted) to a factor of 310. You can think of these factors as being the “real” debt-to-GDP ratio. No country survives a debt load more than 100% of GDP without either a massive devaluation or a debt default, or both.

So, in the short term, the U.S. dollar might be the “winning” paper currency. Compared to Europe, our economy is in better shape, thanks to our energy independence. The overwhelming financialization of our economy means that our government will continue to overreach, that our society will continue to be plagued by massive income inequity and social unrest, and that our economy will grow progressively less efficient as malinvestment grows.

Sooner or later, this massive credit bubble will deflate and the paper money currency that enabled it will collapse. The only question is when. And how many people will die first. Our advice: Try not to end up like poor Giles Corey.

What happens after the eventual demise of paper money?

Bitcoin is a cryptocurrency that’s created at the nexus of computation and energy. Limited to only 21 million coins (but divisible into virtually limitless fractions), Bitcoin could become a much better, new global reserve currency. It is hard to imagine the world’s governments will ever willingly give up the incredible power of their printing presses. But it could happen if the dollar standard collapses, and the advantages of sound money become readily apparent to the average person.

We recommend holding both gold and Bitcoin, as the two most widely recognized and accepted forms of “real” money, instead of saving in dollars. We believe that Gresham’s Law will continue to drive the price of those forms of money higher relative to the dollar.

With regards to the current situation in the markets, it seems likely to us that sooner than most people expect, the Federal Reserve will not only have to lower interest rates once again, it will, almost surely, have to reinstate “quantitative easing” – printing money – to prevent a financial collapse.

Thus, we do not expect inflation to end. Quite the contrary. We can see that there are many parts of our economy that lack badly needed capital investments. When the Fed is forced to ease (like Britain’s central bank was this week), the parts of our real economy that have been starved for capital will see soaring prices.

For example, you can’t print copper.

The Coming Copper Boom

It might not feel like it now, but the fossil fuel-powered internal combustion engine (ICE), which accounts for more than 90% of global car sales, is going the way of the dinosaur – to be replaced by electric vehicles (EVs). In the first half of this year, a record 4.2 million EVs were sold worldwide – up 63% from the same period last year. By 2035, experts project that EV sales will surge to make up over half of global vehicle sales.

Replacing ICEs with EVs is part of the global push for Net Zero by 2050, the coordinated effort by governments around the world to eliminate carbon emissions by the year 2050 – a trend we’ve written about since the inaugural issue of publication, when we explained why gasoline is going extinct. Transport is increasingly electrified, as exemplified most recently last month, when California lawmakers announced plans to ban altogether the sale of new gasoline-powered vehicles by 2035.

Meanwhile, automakers are investing hundreds of billions to revamp their vehicle lineups towards EVs. GM, for example, announced in June of last year that it will invest $35 billion in order to boost EV sales to 2 million by 2025, up four-fold from last year. Ford plans to invest $30 billion to bring new EV models to market by 2025. And Honda will invest $40 billion with the aim of converting 40% of its vehicle sales to EV by 2030, and 80% by 2035.

Automakers will also invest additional billions in battery manufacturing to replace traditional fuel combustion with electrified power trains. In total, global vehicle manufacturers will spend more than $500 billion transforming their vehicle fleets from ICE to EVs and batteries by 2030. And meanwhile hundreds of billions more will flow into solar and wind power installations, with the aim of displacing fossil-fuel based electricity generation.

The true economic and environmental merits of the so-called “green revolution” are subject to debate. But what isn’t in dispute are the hundreds of billions of dollars that are moving the world towards electrification.

And these capital flows will re-shape global commodity markets. In particular, the demand for the critical minerals required to electrify the economy will explode, as a report by PriceWaterhouseCoopers explains:

“The rapid scaling of the low-emission energy systems of the future — solar and wind power, electric vehicles (EVs) and grid-scale batteries — will be highly material-intensive. The production of a solar farm requires three times more mineral resources than a similar-sized coal plant, and constructing a wind farm needs 13 times as much as a comparable gas-fired plant.”

Of all the minerals powering the green revolution, there’s one metal that will rule them all…

King Copper Is the Critical Metal For The Green Revolution

Copper is known as the “red metal” for its shiny red luster. It’s prized for its corrosion resistance and malleability, which means that it’s easily molded into various forms.

Humans first started using copper around 8,000 B.C. for amulets and jewelry. By 3,000 BC humans discovered that copper combined with tin made bronze, kicking off the Bronze Age, when copper was used extensively in armor and weapons. Millennia later, during the Industrial Age, copper was prized as a dependable material for plumbing pipes, thanks to its resistance to corrosion and durability. Copper also efficiently transmits temperature, making it useful for a variety of heat-exchange applications, like air conditioning and refrigeration.

In the green economy, the most important feature of copper is its superior electrical conductivity. No other element on the periodic table transmits electricity better than copper, except for silver – which costs around ten times as much as copper. Its relatively low cost makes copper the primary conduit for electricity transmission around the globe, used in countless applications ranging from computers and cell phones to the electrical wiring in structures throughout the electrical grid.

As the world moves from fossil-fuel based electricity generation and transportation, copper will come to be known as the “green metal,” displacing oil as the world’s most critical global commodity.

The New Oil

The biggest copper demand driver in the electrified economy will come from the rise of EVs, which require roughly 300% more copper than a comparable passenger ICE vehicle.

The EV drive train is built around copper, including the battery, inverter and motor. Unlike combustion engine blocks that create motion from firing pistons, EV motors contain a series of copper induction coils centered around an axle. When electricity flows through the copper coils, a magnetic field is generated that creates motion around the axle, as shown below:

All that copper adds up. A typical EV passenger vehicle requires a mile or more of copper wiring. And the bigger the EV vehicle, the more copper it requires compared with its ICE cousin. An electric bus, for example, can require up to 16 times more copper than a comparable ICE bus.

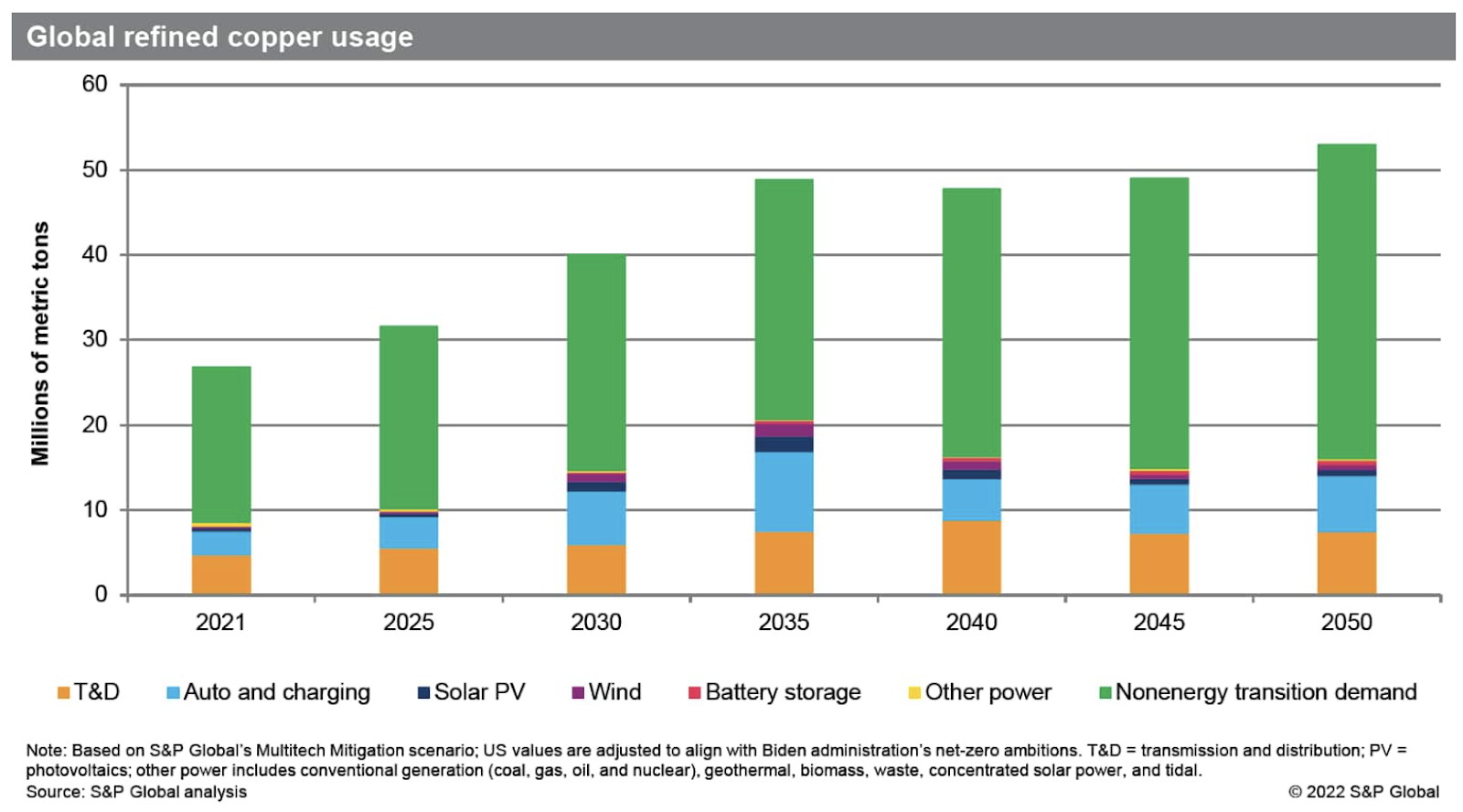

Today, EVs account for 2.2 of the total 25 million tons of global copper consumption each year. But given the rapid pace of EV adoption, this number is expected to more than triple to approximately 7 million tons per year by 2035.

Meanwhile, the world will need a lot more electricity to charge all these new EVs. And policymakers are pushing for solar panels and windmills to supply this electricity, both of which also require huge volumes of copper.

Take windmills, which operate on the same dynamics of an EV motor, only in reverse. That is, windmills convert ambient wind into a spinning rotor, surrounded by copper induction coils. The spinning motion creates a magnetic field, which generates electricity. A standard 3 megawatt (MW) windmill contains 4.7 tons of copper wiring.

As solar panels and windmills increase their share of total power generation, copper demand from these sources is expected to grow from 0.6 million tons per year (Mt/y) in 2021 to 3.7 Mt/y by 2035.

Finally, the electrical grid will require substantial new copper infrastructure to support growing demand from EV charging. The additional copper required to beef up global electrical grids will boost copper demand in this segment from 4.7 Mt/y in 2021 to 7.5 Mt/y by 2035.

Add it all up, and global copper demand is expected to double from roughly 25 Mt/y in 2021 to 50 Mt/y by 2035. It will only continue growing from there for the foreseeable future to meet the global push to “net zero” by 2050.

The sheer magnitude of this growth trajectory is hard to fathom. Since humans first started pulling copper from the Earth’s crust around 4,000 B.C. a total of 700 million metric tons of copper has been mined. To meet the massive demands of the green revolution, the world must produce more copper in the next two decades than has been mined throughout human history.

The demand side of the copper market will be very bullish for decades to come… but that’s only half of the story. The jet fuel for the copper rally will come from the supply side of the equation. The reason is because higher prices are not being met with more investment – as Goldman Sachs metals analyst Nick Snowdon explained in a recent Bloomberg interview:

“It’s very different from what we saw in the 2000s. In 2002, when that bull market began, almost immediately you saw the supply side response. You saw projects being approved and investment flowing rapidly, and the supply side really almost moved in lockstep with the increase in price. This time around, that isn’t occurring at all. In the last two years, even though the price has doubled, you haven’t seen a single new copper mine approved… We’re in the first innings in terms of the supply response.”

The lack of new supply – more on that in a moment – is the driving force behind the coming copper boom. The price of copper will likely exceed the highs of the copper supercycle of the early 2000s, when copper soared from $0.60 per pound in late 2001 to a high of $4 by 2006 (today, copper trades at around $3.35 per pound):

The question is, then: Why isn’t more copper being produced to meet rising demand?

The ESG Paradox: Creating More Mineral Demand, While Killing New Supply

The world doesn’t have enough energy today partly because ESG policies have stymied investment in the fossil fuels that still account for over 80% of total global energy consumption. And those same policies are killing capital investment in extractive industries, including copper.

Of course, getting commodities – oil, gold, gas or copper – out of the earth requires massive amounts of capital. And extracting resources inevitably comes with the unavoidable cost and risk of environmental degradation. Even as mining companies learn to minimize these risks, their impact on the earth and the environment are still substantial.

But the environmental activists that are pushing the global economy towards wind power and EVs don’t seem to recognize this basic reality. And that’s the paradox of the ESG investing movement: Pushing hundreds of billions of dollars into infrastructure that will create record new demand for key minerals, like copper, while starving the supply side of the mineral extraction business because of its environmental impact.

ESG-focused investors in global money centers – and the politicians promoting the movement – are only part of the problem. Environmental activism in major copper producing regions around the world is also constraining copper supply.

For example, in Chile – known as the Saudi Arabia of copper for its massive copper reserves – the recently elected leftist government is imposing new environmental regulations that prevent new mining activity. This includes rejecting environmental permits for an extension of Anglo American’s Los Bronces copper mine, citing the mine’s proximity to a glacier.

Projects to develop reserves of gold – which often produce copper as a byproduct – are being similarly hamstrung. Environmental regulators in Columbia have delayed AngloGold Ashanti’s Quebradona gold and copper project in Colombia by up to two years. And earlier this month, gold miner Newmont canceled development of a $2 billion copper and gold mine in Peru.

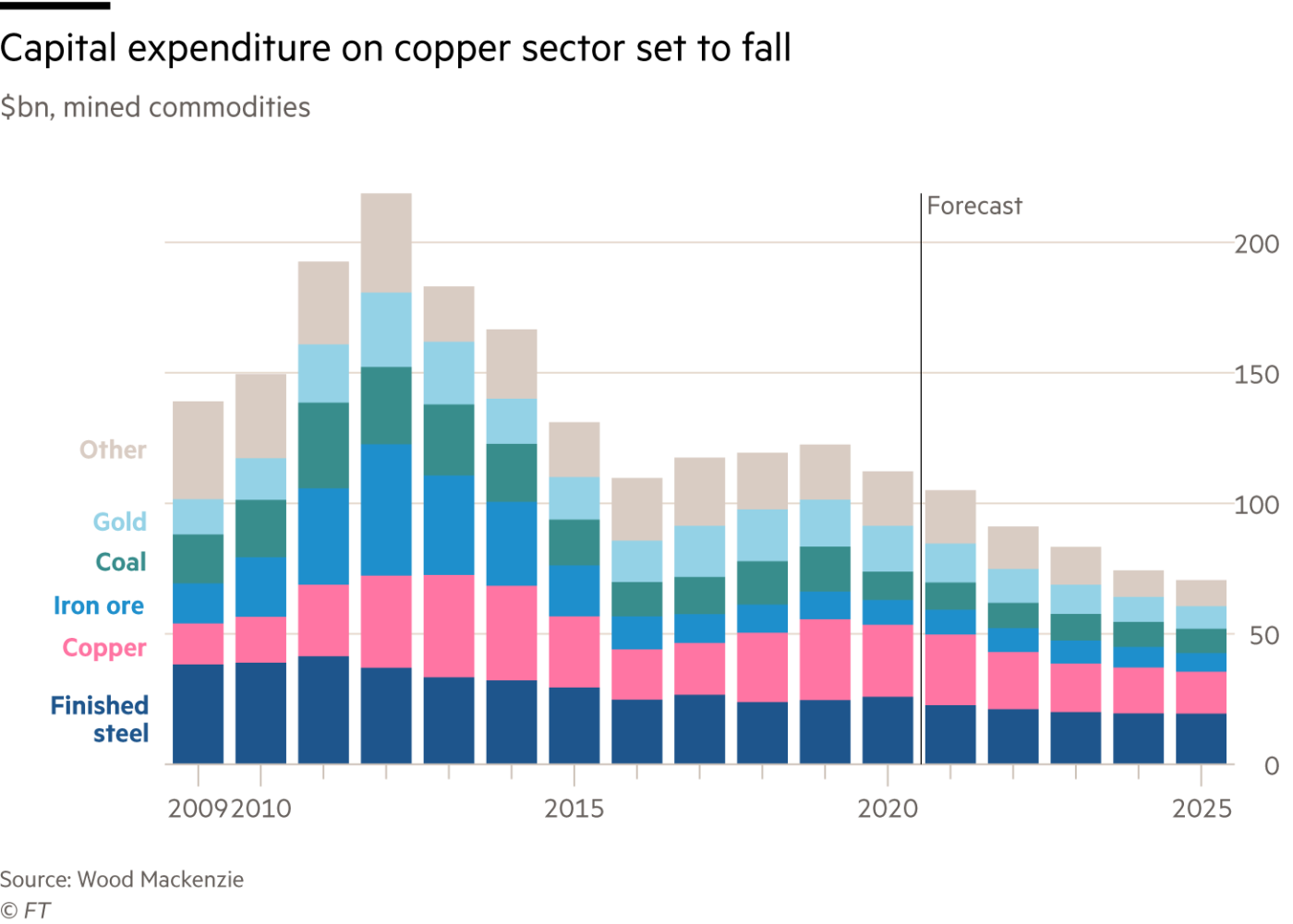

As a result, despite surging prices for copper, gold and other metals, investment into new sources of supply has plummeted:

In order to meet the record surge in copper demand coming from the green revolution, copper producers should be ramping up capital spending to new record highs today. Instead, capital expenditures are 41.6% below previous highs set in 2012.

That’s a big problem.

Developing a copper mine takes many years of permitting, site prep, and mine construction before bringing production online. And higher environmental hurdles have substantially increased the timeline for this process. During the previous copper bull market in the early 2000s, the permitting stage typically lasted six to twelve months. Today, that same process takes two to three years, which means bringing a new mine online now takes at least a decade.

So, even if a flood of investment capital was deployed to develop new mines starting today, that wouldn’t resolve the coming supply crunch and price spike until at least 2032.

Given this time lag, the fate of the copper market has already been sealed – a severe supply deficit is baked into the cake. The only question is, how bad will it get?

All signs indicate things will get worse, not better. Incentivizing new supply will require higher prices and lower financing costs for miners to deploy capital sooner rather than later. But the recent tightening of financial conditions across the globe, and collapse in commodities prices, is doing the exact opposite. Copper prices have dropped 30% from recent highs of $5 per pound earlier this year to $3.35 per pound today, while interest rates are spiking at the fastest pace in a generation.

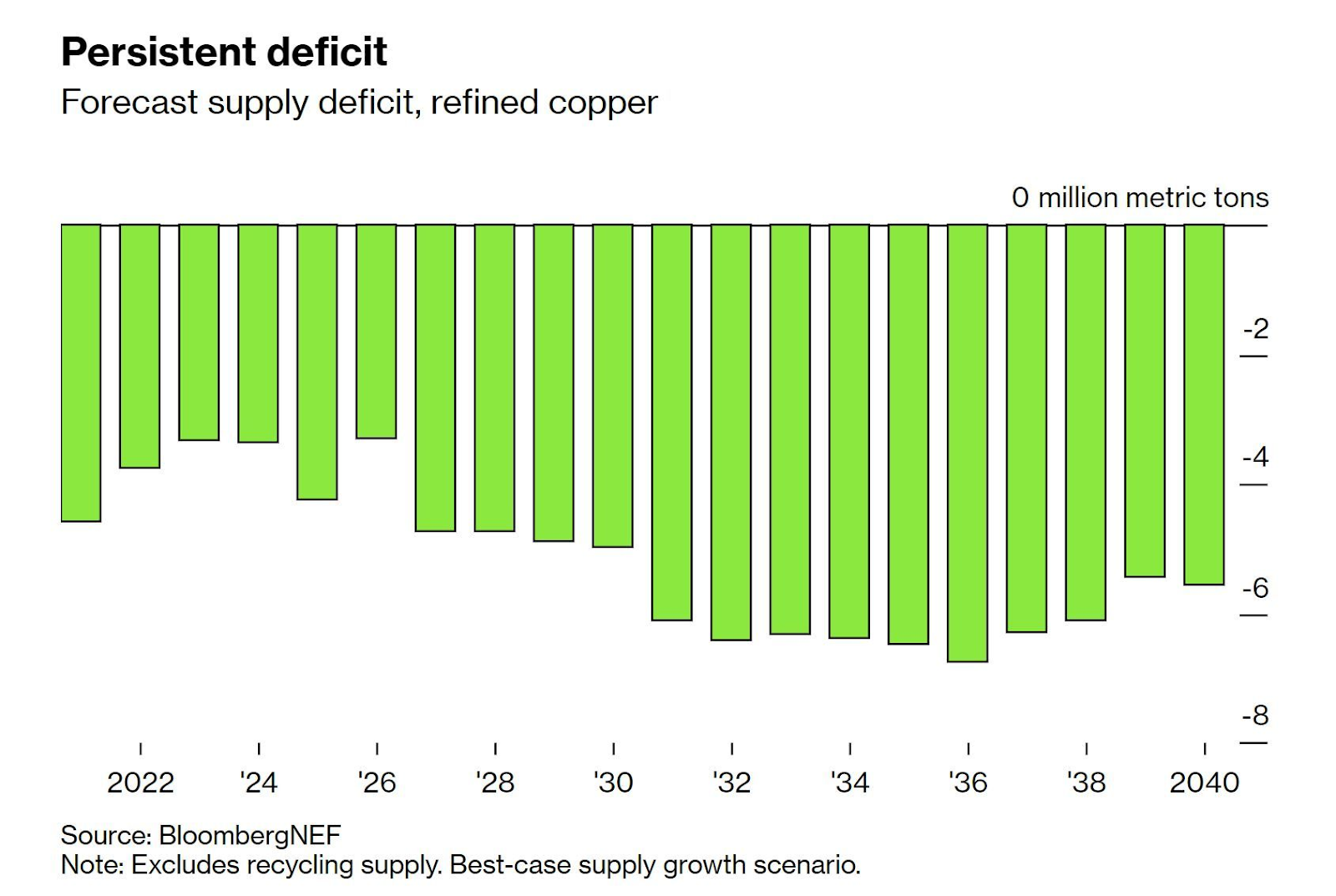

Recently, Freeport-McMoRan, the world’s largest public copper miner, warned that copper prices are “insufficient” to support new investments. Even before these latest headwinds, research compiled by Bloomberg indicated that copper deficits would hit record territory by the middle of this decade, and continue until 2040:

Similarly, a report by S&P Global explains:

“Copper demand from energy transition end markets is expected to reach a maximum of almost 21 MMt in 2035. This surge in demand to meet Net-Zero Emissions by 2050 requires a near doubling of today’s global copper supply by 2035, an expansion that current exploration trends or projects in the feasibility stage of development are incapable of meeting.”

Now, the only real question is – how high will prices go?

Remember that prices serve one basic function: to balance supply with demand. In a normal bull market, high prices create a profit incentive for miners to bring new supply online, eventually limiting the scope of price increases. That’s how the early-2000s bull market lost its steam – as supply eventually caught up with demand.

But given the unique dynamics in today’s market, the supply side of the equation will fall far short of demand for many years to come. That leaves only one lever to balance the market – a massive price rally that pushes copper prices high enough to destroy demand.

In that scenario, copper prices could soar into the stratosphere. That’s because of the unique demand elasticity of copper.

The Road to $50 Copper: a Demand-Destroying Price Rally

Demand elasticity refers to how sensitive demand is to changes in price. For some commodities like crude oil and gasoline, consumers can simply consume less during periods of high prices. They can carpool, use public transportation, or forego that summer road trip.

For other commodities, substitution comes into play. When corn prices spike, ranchers can shift their cattle feed from corn to wheat. When beef prices rise sharply, consumers can eat more cheap chicken.

But copper is unique. There are no viable low-cost substitutes for copper for many of its key applications. Silver, for example, is roughly 10 times more expensive.

Aluminum is the only cost-competitive replacement for copper, but it has several key drawbacks that limit its substitution. Aluminum has lower conductivity than copper – meaning it requires thicker cables to transmit the same amount of electricity. It also suffers from higher corrosion, and is less durable than copper.

A second factor that limits the demand-elasticity of copper is that it makes up a relatively minor part of the cost structure in the key demand sources that it goes into. Consider that a typical EV requires about 175 pounds of copper. At current prices of around $3.35 per pound, that’s around $600 per EV. So if copper prices double, a company like Tesla would only need to raise the price of its Model 3 from $50,000 to $50,600. Over the course of 6 years of car ownership, that’s about $100 per year.

The same is true for the traditional sources of copper demand, like construction. The average American home requires about 440 pounds of copper, or about $1,540 worth of copper at $3.50 per pound. If copper prices doubled to $7 per pound, that’s only $1,540 of additional costs on a $428,700 purchase – or less than a 1% increase. Spread over a 30-year mortgage, that’s less than a $100 per year hit to the end consumer.

So, if the copper market needs to rebalance using the demand lever – since supply will not be coming online – prices will need to skyrocket before we see meaningful demand destruction.

With most commodities, a doubling in price will create substantial pushback from consumers to balance the market (think about the impact on gasoline consumption when prices at the pump double). But for copper, prices might need to rise by 5x – 10x before we see any meaningful pushback from consumers.

This unique demand inelasticity, in the context of unprecedented supply deficits, explains why the coming bull market in copper could be one for the record books. Here’s Goldman Sachs Head of Metals Nick Snowdon summarizing the situation in a recent Bloomberg interview:

“The thing about the copper market is that we’ve never been in such an extreme set of fundamental circumstances. We’ve never had to go to end demand destruction pricing to achieve a rebalancing. The bull market of the two thousands was nearly entirely solved by supply responses. And a very rapid increase in mine investment. That’s clearly not gonna be the majority solver this time… So we don’t rule out that copper could be a $50,000 (per ton), could be a $100,000 commodity.”

The $50,000 – $100,000 per ton price Snowdon references translates into about $25 – $50 per pound of copper. That would be a stunning increase of between roughly 7x – 15x current prices.

Before the latest price decline, top tier copper miners were printing money at recent prices of $4 – $5 per pound of copper. So, a scenario of $25 or beyond would present a massive windfall for the sector.

But we’ve found an even better way to play the coming copper boom…

This company offers a purely “green” way to invest in the green metal. A company that extracts copper from the waste streams of existing mines, eliminating the need for new mining capacity, and transforming environmental liabilities into cash flowing assets. Not only that, but this company runs on 100% renewable power, making it the ultimate ESG-approved vehicle to exploit higher copper prices.

Even better for investors, this business model offers a uniquely capital-efficient way to invest in copper. It doesn’t employ a single geologist on its staff, and hasn’t spent a dime on exploration for or developing copper mines. It’s a business with a proven model over the last 30 years, backed by long-term, strategic agreements to source a steady stream of low-cost copper for many years to come.

Finally, this business model is built to return capital to shareholders. Over the last 12 months alone, this company returned nearly 27% of its current enterprise value to shareholders, including a generous 13% dividend yield based on its current share price.

In other words, this company provides the same upside to higher copper prices as a traditional miner, but without the downsides of heavy capital requirements and an ESG target on its back. In short, this business is…

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care Concierge, Lance James, at 888-610-8895.