Buffett’s Secret For Beating Inflation

“The key force of economic advances is the entrepreneur, who on his own, without governmental cues or expert consultation or even a defined market, creates new goods, services, business plans, and projects.

“Economic growth and progress, job and welfare, markets and demand all stem from this creativity of the entrepreneur. Population growth, capital accumulation, economic efficiency, and even scientific advances are all less important than entrepreneurial creativity. And governmental interventions in the economy are distractions – ‘noise on the line’ – that nearly always retard expansion.

“Failing to see the centrality of entrepreneurial creativity, economists everywhere have counseled governments to attend to the money supply, aggregate demand, consumer confidence, trade imbalances, budget deficits, capital flows – to attend to everything except what matters most: the environment for innovation.”

– George Gilder, Knowledge and Power

The two most important entrepreneurs in the world’s energy markets today are Charif Souki and Toby Rice.

Twenty years ago, Souki founded and led Cheniere Energy (NYSE: LNG, $160). He built the first successful, large-scale LNG export facility in the United States. After a dispute with Carl Icahn, he left the company. He’s now building the first fully integrated (gas field, gas pipeline, lined LNG facility) in the United States – Tellurian (NYSE: TELL, $4.50). (See our June 17 issue for details.)

Rice and his two brothers built, from scratch, the leading gas producer in the Marcellus shale, Rice Energy. They then engineered a hostile take-over of venerable producer EQT (NYSE: EQT, $50), transforming it in about a year into America’s leading producer of natural gas via massive increases to drilling efficiency and huge, incredibly attractive acquisitions. The story of the Rice brothers and the rise of the economic dynamo they’ve built, EQT, is arguably the greatest entrepreneurial success of the 2020s. It was the subject of the first issue of this publication.

But the Rice brothers are just getting started. Like Souki, they realize the future of the world’s economy depends on “unleashing” U.S.-sourced natural gas. Their plan is to lead the U.S. to produce an additional 50 billion cubic feet (BCF) of natural gas a day, enough to power the world.

“The Marcellus as a whole has more gas reserves than Russia. So it’s an absolute powerhouse… this is like the Saudi Arabia of energy… With a $3.75 gas price, the Marcellus shale has the opportunity to increase natural gas production an incremental 35 BCF a day and be able to do that over a 10-year period of time and hold that ball, hold those lines flat for over 30 years.

“The biggest gas field in the world can be the biggest gas field in the world two times over. And the only thing that needs to make that happen is pipelines. And then also the LNG facilities to create the demand for [those] incremental volumes.”

– Toby Rice, CEO of EQT, The Power Hungry Podcast, June 3, 2022

Last week, EQT announced a $5.2 billion acquisition for Tug Hill, a privately held, mid-sized producer in the Marcellus whose assets and pipelines are adjacent to EQT’s.

EQT is getting almost another billion cubic feet a day of additional production from 300 drilling locations. That’s a 15% increase from EQT’s current daily production of 5.5 BCF. Tug Hill also owns 100,000 acres in the core of the Marcellus basin. This acreage has enough proven reserves to provide 11 years of continuous production with only maintenance-level amounts of capital spending.

EQT is also buying the associated pipeline gathering systems (95 miles of pipelines), which will allow EQT to reduce its own capital spending on gathering systems by 75%.

The deal, which was priced attractively at just 2.3 times the next 12 months’ estimated operating profits (27% free cash flow yield), implies a long-term price of $3 gas. That’s a 40% discount to the current long-term futures “strip” prices.

EQT is making the purchase with cash on hand, with half of the deal paid for in stock. Thus, this deal requires no additional leverage and is massively accretive in terms of cash flows, driving an estimated 10% increase in cash flow per share.

On the back of this deal, EQT’s forecasted share buyback this year doubled to $2 billion, and its debt repayment through 2023 increased to $4 billion.

It also reduces EQT’s production cost basis by $0.15 per million British Thermal Units (“MMBtu”), increasing its margins and driving down its “breakeven” price of gas. The deal increases EQT’s forecasted long-term free cash flow to $5 billion annually.

In short, like its deal to purchase Chevron’s Marcellus assets, this is a major acquisition that Toby Rice has engineered to materially improve the company’s profitability, reserves, and production – without taking on any new long-term debt. Deals like this wouldn’t be possible without EQT’s industry leadership, as Tug Hill CEO Michael Radler emphatically explained:

“EQT is the face of the new energy paradigm. Toby Rice’s vision around U.S. LNG is something we believe in and because of our significant ownership position, are excited to be a part of that vision.”

There’s a concept Porter calls “economic gravity.” It exists when there’s a dynamic, visionary leader in an industry who’s able to rally the best people and the best assets to work together. That scale, energy, and vision draws more and more entrepreneurs toward it, to work together, creating even more “gravity,” and drawing still more economic energy toward it.

The most obvious example of economic gravity is with Berkshire Hathaway, where, with Warren Buffett’s genius, an enormous conglomerate was created across a vast array of different industries. Historically, in energy, you saw this most dramatically with Standard Oil.

Today, we’re also seeing it with EQT.

If you haven’t bought EQT shares yet, it’s not too late. A company producing reliable free cash flows of $5 billion annually with a proven growth strategy should be worth at least $100 billion. EQT’s current enterprise value is only $25 billion. In other words, absent the volatility of natural gas prices, EQT should be worth 4 times more than its current value. And we believe that higher natural gas prices are inevitable as more and more of the world’s electrical generation switches from coal to natural gas, which gives EQT even more upside.

The key to growing production and capturing the highest prices for energy is reaching global markets via LNG exports. That’s the same strategy Souki is pursuing at Tellurian, by linking the Haynesville shale directly to the world’s markets with its huge Driftwood LNG project. And, while Souki is ahead in this race for now (his LNG facility is under construction), EQT is the country’s largest gas producer and the leading acreage holder in the world’s largest gas field.

That’s not to say that Tellurian, with an enterprise value of only $2 billion, isn’t a great investment. It is, because it is currently at a much earlier stage of development than EQT, and thus it’s much cheaper to buy. The returns on Tellurian should be at least 10 times over the next 10 years.

But in our eyes, EQT is the best possible mix of reserves, acreage, pipelines, and management. In terms of scale, no other energy company in the world has more to gain by linking its production to the world’s markets via LNG.

And by the end of this year, we expect the Rice brothers to announce their biggest and most strategic deal yet, a major investment in an LNG facility to move additional production into foreign markets, where prices for gas can be 10 times what they are in the U.S.

When that deal is announced, the future implied value of EQT’s production will soar. And its “economic gravity” will impact the entire industry on a global scale.

EQT’s Coming Out Party: Europe’s Energy Crisis

Last week, Russia officially halted all natural gas exports to Europe.

The Kremlin announced that it would keep the gas taps shut off until the collective “West” lifted sanctions against the country. In other words, absent an immediate resolution to the Ukraine conflict and a thaw in geopolitical tensions, 40% of EU natural gas supply is now offline indefinitely.

As EU spokesperson Tim McPhie said, Russia’s “weaponization of energy supplies [means that the continent will] phase out Russian fossil fuels in Europe.”

There’s just one problem: Replacing 40% of Europe’s natural gas supply won’t happen overnight. The European Commission estimates a total cost of €210 billion into infrastructure supporting new gas supplies, including new LNG import terminals, to eliminate the continent’s energy dependence on Russia. But even these aggressive investments won’t allow Europe to fully replace Russian energy supplies until 2027.

More immediately, Goldman Sachs estimates that spiking energy prices will cost European households a whopping additional €2 trillion next year. In a note to clients, the bank explained that Mr. Market has underestimated the scope of fallout from this energy crisis:

“In our view, the market continues to underestimate the depth, the breadth and the structural repercussions of the crisis… We believe these will be even deeper than the 1970s oil crisis.”

While European asset prices have begun pricing in the fallout from the worst energy crisis in modern economic history (a freefall in European stocks, bonds, and currencies), so far, U.S. markets have mostly shrugged off this energy crisis as a purely European problem.

That’s a big mistake.

One of the central themes we’ve tracked since starting this publication is the rise of America as an energy exporting superpower. Specifically, the rise of American LNG exports, which will increasingly link the U.S. domestic gas market to international prices. That’s why U.S. natural gas now trades at the highest levels since 2008, at over $8 per thousand cubic feet (mcf).

And since natural gas provides the key fuel source for American electricity generation, this price spike is crushing households with crippling utility bills. Bloomberg recently reported that an incredible one in six U.S. households is late on its utility bills. That’s 20 million American families, the largest number ever recorded.

Things will only get worse as peak demand season for natural gas hits this winter. Prepare to see more headlines like this in the coming months:

The article goes on to explain…

“After enduring months of rising prices from the gas pump to grocery checkouts, New Jerseyans could see their annual heating bills soar this fall and winter as inflation and global tensions drive up natural gas prices. State regulators on Wednesday approved double-digit rate increases for four gas providers serving millions of customers in the state, with prices expected to rise by hundreds of dollars on an annualized basis for some people.”

As Toby Rice explained recently, abundant energy supplies are the basis for modern life:

“Simply put, the more energy you can give people, the better the quality of life. And so if you want to make an impact, provide the world with cheap, clean, reliable energy…

“If people think that they can attack oil and gas, and it’s only going to be felt by the oil and gas producers, wrong. You attack a company, you’re attacking that company’s customers, and you attack our pipelines, you prevent our ability to reinvest in drilling and bring more supply to the world that’s going to translate to higher prices, like exactly what is going on in the country, and what is going to what is really going to be happening in New England this winter.

– Toby Rice, The Power Hungry Podcast, June 3, 2022

The ripple effects go beyond just higher heating and utility bills. Energy impacts every economic activity on Earth.

The world’s supply chain problems don’t have anything to do with transportation anymore. Shipping prices (as tracked by the Baltic Dry Freight Index) are down 75% from their recent peak. Supply chains are now constrained because of energy prices.

In Europe, shortages of electricity and natural gas have forced shutdowns of everything ranging from steel to plastics to chemical manufacturing.

But the bigger problem is going to be food.

More than 70% of European ammonia production (the critical ingredient in nitrogen fertilizers) is now offline. At the start of last year, farmers in Western Europe could buy ammonia for about $250 per ton. Today, that same ton of fertilizer costs $1,250. If European gas supplies remain disrupted and these sky-high fertilizer prices persist, the International Fertilizer Association estimates a 2% drop in global corn, wheat, rice, and soybean production.

For perspective, that would be equivalent to OPEC announcing an oil production cut of 2 million barrels per day. Prepare for a global shock in food prices to go along with crippling costs for energy, heat, and utility bills.

The energy crisis won’t be contained in Europe.

Earlier this week, the U.S. Bureau of Labor Statistics reported a higher-than-expected inflation number with the CPI up 8.3% in August. A big driver was spiking food costs, which rose 11.4% from last year, the biggest increase in 43 years. The report showed prices of staples like bread increasing by 16.2%, chicken rising by 16.6%, and milk jumping 17%.

The inflation report sent stocks into a tailspin, with the S&P 500 plunging by over 4% in a day, the biggest decline since June 2020, during the height of the pandemic. Higher interest rates are coming: The market-implied odds of a 75-basis point increase at the upcoming Fed meeting next week increased from 69% to 91%.

Many sectors of the U.S. economy are already in a recession.

“People keep saying, are we going to be in a recession? We’re in a recession. Anybody who thinks we’re not in a recession is crazy. The housing market is in a recession & it’s just getting started. So it’s probably going to be a difficult 12 to 18 months in our industry.”

– Restoration Hardware CEO Gary Friedman

The biggest problems for investors are still several quarters away, and are likely to stem from much higher consumer and corporate default rates. Reports surfaced earlier this week that borrowers in Goldman Sachs’ credit card portfolio were falling behind on their payments and defaulting at rates “well above subprime lenders.” Deutsche Bank credit strategists likewise predict noninvestment-grade bonds will see average default rates exceed 10% in 2024, including default rates above 40% for the lowest-ranked (CCC) bonds.

Given that the U.S. economy relies upon consumer spending, the weak consumer will soon start hitting corporate profits. This will eventually lead to layoffs, creating further weakness in consumer incomes, driving a self-reinforcing recessionary cycle. It’s no coincidence that in the same week Goldman reported a spike in default rates on its credit portfolio, the company also announced its largest round of layoffs since 2008.

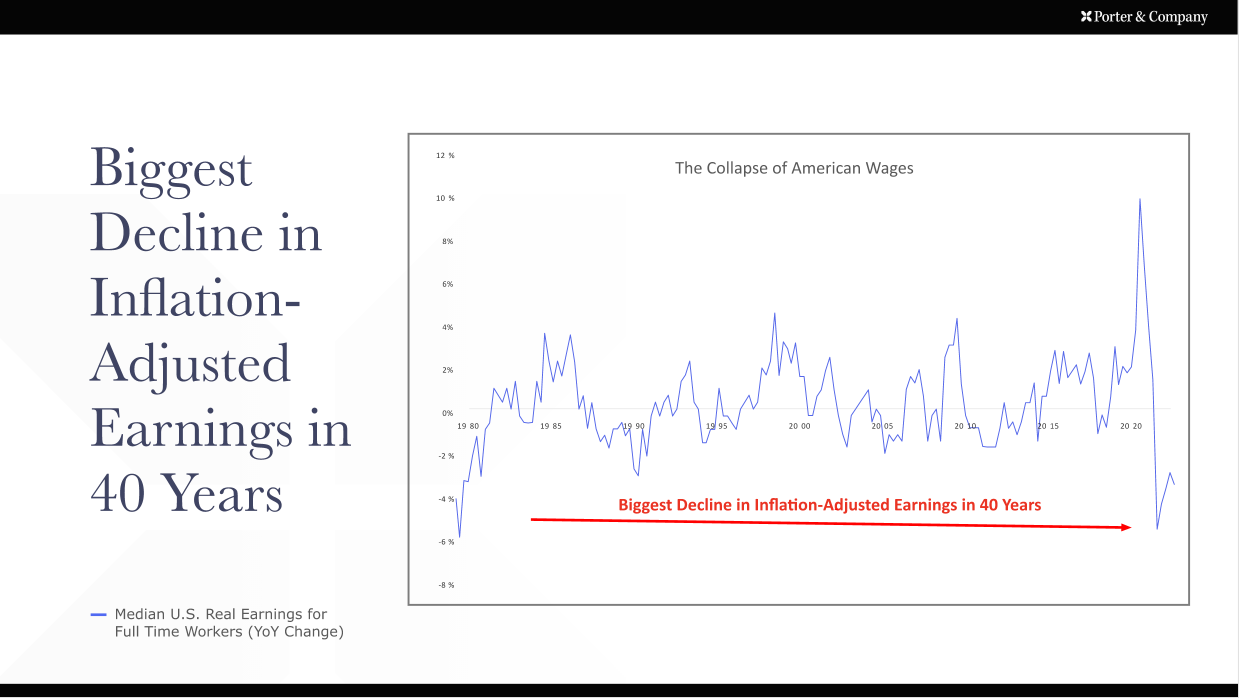

The bottom line: The shockwaves from the European energy crisis are spilling over onto American shores. The early signs of economic distress we’re seeing now will soon snowball into a full-blown recession. Inflation is crushing real consumer incomes, compounded by higher borrowing costs, pushing more and more Americans out of the middle class. No data series shows this better than the collapse in real (i.e., inflation-adjusted) wages, which are plunging at the fastest rate in 40 years:

The stage is set for a repeat of the 1970s style stagflation.

Investors should prepare for a period of slowing economic growth and persistently high inflation, which will require an entirely different investment approach from what’s worked over the past 40 years.

A 1970s Investing Playbook

The 1970s was a lost decade for most financial assets, with the exception of commodities. The conventional wisdom says investors can seek shelter from inflation in natural resources, like oil and gas producers or gold miners.

But there’s a far better way to beat inflation, and it’s one of the most important and valuable secrets in all of finance.

The greatest wealth compounder of all time, Warren Buffett, first explained the real secret to beating inflation with investments in his 1983 letter to shareholders:

“For years the traditional wisdom – long on tradition, short on wisdom – held that inflation protection was best provided by businesses laden with natural resources, plants and machinery, or other tangible assets (‘In Goods We Trust’). It doesn’t work that way.”

– Warren Buffett’s 1983 Letter to Berkshire Hathaway Shareholders

As Buffett explains, capital-intensive businesses, like those involved in natural resource extraction, may on the surface appear to generate a strong return during inflationary periods… but those earnings get sucked right back into the business via heavy capital requirements.

In other words, it’s not what you earn. It’s what you keep.

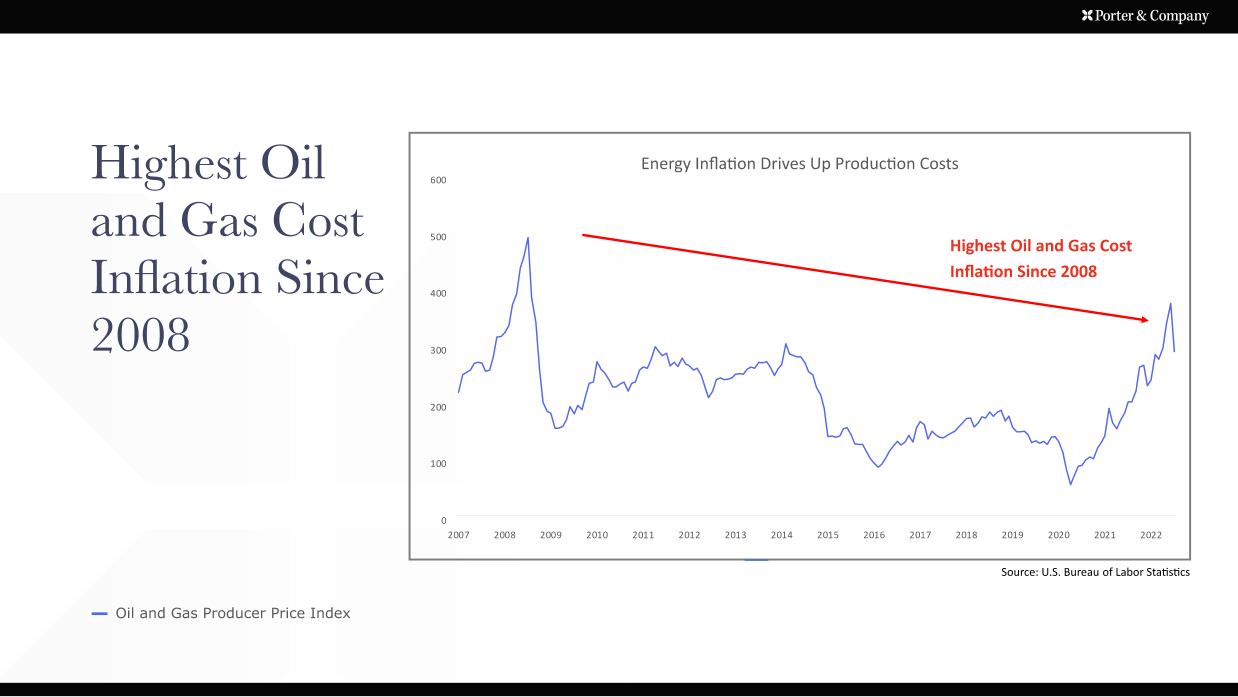

And when prices for commodities rise, so do the costs of producing those commodities. We can see this today – where the highest oil and gas prices since 2008 have corresponded with the highest input costs since 2008 for oil and gas production:

The other issue that resource extraction companies face is an even bigger challenge: they have to constantly rebuild their asset base. Resources companies are constantly liquidating their balance sheets. Those assets have to be replaced to grow production. But, in the face of rapid inflation, the cost of acquiring new reserves inevitably eats up a huge percentage of the firm’s cash flows. That’s why we recently recommended Viper Energy Partners – it’s the capital-light way to invest in the Permian Basin’s oil production.

But what about EQT?

It’s true, EQT won’t be able to replicate its asset base at anything like the prices it is buying proven reserves for now. However, the company’s plan to reach international markets (and garner vastly higher prices for its production) will dramatically change the economics of the business, making the value of its existing reserve five to 10 times more than before.

The size of EQT’s asset base (and the long-lived nature of these gas wells) means that their capital spending, while growing, likely won’t need to keep pace with their revenue growth. In fact, over the last five years, the company’s proven reserve base has almost doubled, to 23 trillion million cubic feet (Tcf), while its capital spending has fallen 50% from around $2 billion to around $1 billion. And… EQT is already sitting on a lot more gas that hasn’t been developed or “proven” yet. The company has over a million acres of land in the Marcellus that remains undeveloped, compared with the 500,000 developed acres.

In our view, EQT is a unique situation, a once-in-a-generation kind of business that can likely grow production for the next 30 years without having to acquire any additional resources.

But there aren’t many resource-extraction businesses like EQT.

Generally, the far better solution to profit from rapid growth in inflation is to own businesses that rely mostly on intangible assets, which include timeless consumer brands, patent-protected pharmaceuticals, or companies that have already spent the capital required to develop virtual monopolies (like companies that own critical pieces of infrastructure – think toll roads, for example).

Buffett says companies like these possess “economic goodwill.” That is, the value of their intangible assets grow every year, without corresponding increases to capital spending. That’s why Buffett’s biggest investments have historically all been “asset-light” and brand-rich. Businesses like Coca-Cola, American Express, Apple, and See’s Candy.

We have, of course, noticed the same unique financial advantages in certain companies. No offense to Buffett, but we think his description – “economic goodwill” – confuses more than it clarifies.

We describe these firms’ incredible ability to increase cash profits over time without corresponding increases to capital spending as “capital efficiency.” Their business models allow them to earn more money on each dollar of revenue over time, as the value of intangible assets grow with inflation.

We’ve long pointed out how extraordinary these investments can become over time. The best example is Porter’s 2007 recommendation of Hershey, which he predicted at the time would be his best “no risk” recommendation ever, growing at 15% annually. Today, 15 years later, Hershey’s shares have increased by 450%. With dividends reinvested, the total return tallies to 688% – or 15% a year. It’s incredible that investors can earn these kinds of outsized, market-beating returns from such a stable and slow-growing business. That’s the magic of capital efficiency.

Hershey doesn’t have to reinvent its process, which turns fresh milk into chocolate that won’t spoil. It doesn’t have to build new factories every year or create new brands. It merely has to maintain its positive appeal in the mind of the public, which it does primarily by making the same product it has been making for well over 100 years. That appeal allows it to raise prices continuously, more than keeping pace with inflation.

It’s the unchanging nature of the product that gives the business a nearly unbeatable advantage for investors. Whether you call that capital efficiency or economic goodwill, companies with these unique characteristics are the best way to hedge against periods of high inflation, as Buffett explains:

“A disproportionate number of the great business fortunes built up during the inflationary years arose from ownership of operations that combined intangibles of lasting value with relatively minor requirements for tangible assets… During inflation, Goodwill is the gift that keeps giving.”

– Warren Buffett’s 1983 Letter to Berkshire Hathaway Shareholders

As the European energy crisis unleashes a stagflationary tsunami across the globe, we’re looking for capital-efficient businesses that will survive – and thrive – during the coming financial and inflationary storm.

As more and more Americans slip out of the middle class because of spiking inflation and a slowing economy, there’s one trend we can count on: growth in discount retailers.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care Concierge, Lance James, at 888-610-8895.