Issue #94, Volume #2

Revisiting Two Of Our Biggest Mistakes

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Great businesses are hard to find… These businesses last through major ups and downs… A capital efficient homebuilder… One of our biggest mistakes… We got spooked… Buffett makes a big buy… |

Editor’s note: Today, we are presenting part of an issue of The Big Secret On Wall Street that reinforces one of the central points that Porter likes to share with readers… It involves not just owning great businesses, but never selling them as well…

We will not be publishing the Saturday Stock Screen and Sunday Investment Chronicles for the remainder of August. Both will resume on September 6 and 7.

Many investors believe the biggest mistake you can make is buying a stock that performs poorly.

But those mistakes – while important (and money-losing!) – are not as bad a use of capital as the mistakes we’ve made by selling great businesses (or not buying them to begin with) because we got spooked following a lousy quarter or we were worried about macroeconomic factors like interest rates.

Few investors remember that many great businesses – including AT&T (T), ExxonMobil (then called Standard Oil) (XOM), and The Hershey Company (HSY) – continued to pay their dividends during the Great Depression, the worst economic crisis in American history.

Most investors probably don’t remember that many of the then-top technology companies – such as IBM (IBM), Intel (INTC), and Texas Instruments (TXN) – maintained their dividends during the dot-com bust.

And many investors may not even remember that many high-quality consumer businesses – like Walmart (WMT), Johnson & Johnson (JNJ), and McDonald’s (MCD) – didn’t cut their dividends during the 2008-2009 Global Financial Crisis.

The point is, no matter what happens in markets or the economy, great businesses tend to do well over the long run. So if you own one of these businesses and can afford to be patient, it’s almost always a mistake to sell.

Here at Porter & Co., we generally try to recommend only great businesses (outside of the occasional more speculative opportunity). As a result, virtually every time we’ve sold – or waited to buy – it has been a mistake.

In this issue we highlight two of the most notable of these mistakes we’ve made, and show you the investment returns we missed out on by being too conservative when buying and holding great companies.

The Best Business We Didn’t Buy

In the July 1, 2022, issue of The Big Secret On Wall Street, we highlighted the remarkable business model of homebuilder NVR (NVR).

Most homebuilders are poor long-term investments. That’s because they’re terribly capital inefficient businesses – they require enormous amounts of capital to operate.

They take on debt to buy up big plots of land in areas where they think they’ll be able to build and sell houses. And to be fair, when they buy the right properties, in the right places, at the right price, they can make a lot of money. That’s why most homebuilders like to tout the size and quality of their land holdings.

However, over time, these companies inevitably end up owning too much land, in the wrong places, purchased at the wrong price. When the economy hits a rough patch, these companies struggle as the value of their land holdings fall relative to their high debt loads.

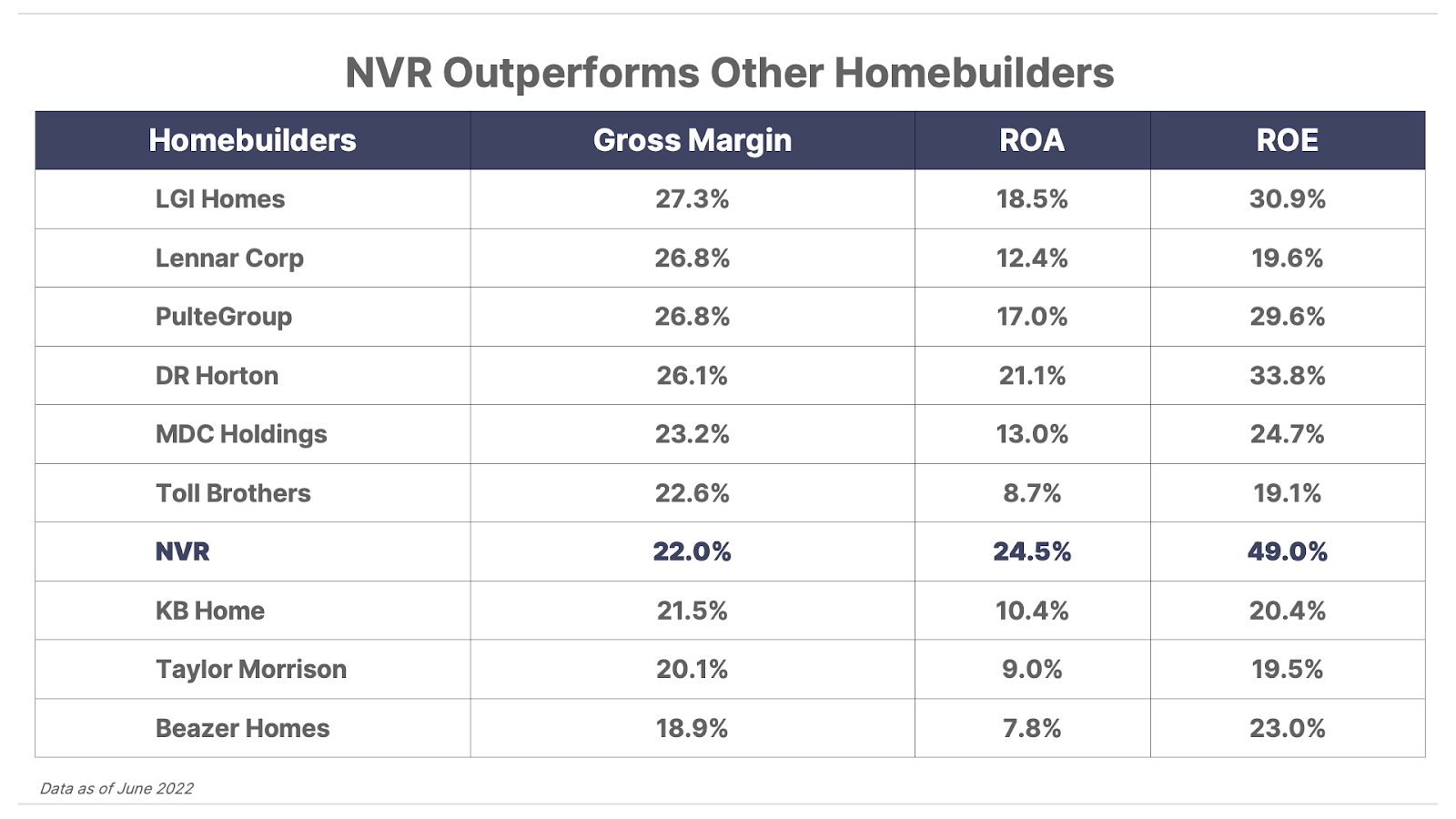

On the surface, NVR looks similar to other homebuilders. It builds homes in 35 metropolitan areas under a range of brands, such as Ryan Homes and Heartland Homes. It sells to both first-time home buyers and move-up buyers. And if you look at the company’s gross margins, you won’t find anything extraordinary. They’re roughly on par with most other large homebuilders.

But that’s where the similarities end. If you dig a little deeper, you’ll see that NVR’s return on assets (“ROA”) and return on equity (“ROE”) are significantly higher than other homebuilders. In fact, NVR’s ROE is more than double the industry average.

In other words, NVR is vastly more profitable than the average homebuilder.

Often when you find a company with such a big advantage in ROE, it’s because the company is highly leveraged. But NVR actually carries no net debt at all.

NVR’s secret is that it figured out a way to profit from massive capital investments without having to own those assets. Instead of developing large tracts of land itself, NVR partnered with independent developers to buy “options” on lots.

This new business model gave NVR a huge advantage over other builders. So it decided to focus exclusively on this more capital efficient approach – in addition to pioneering faster and cheaper ways of building high-quality houses.

It was able to build a detached home in less than three months (86 days) versus an industry average of around seven months.

This combination of high capital and operating efficiency has made NVR one of the best performing companies of the past few decades.

In fact, in the 20 years between 1996 and 2016, it had the highest returns on equity of any company with a market cap of $100 million or more – beating all the high-flying tech stocks of the dot-com boom and generating share-price returns of almost 30% annually, despite the mortgage crisis between 2008 and 2011.

NVR is one of the relatively few businesses we consider “must own,” and it was a long-time holding of Porter’s Stansberry’s Investment Advisory portfolio at his previous firm.

So when shares dipped below $4,000 per share – trading at roughly half its average price-to-earnings (P/E) ratio of 15 – shortly after Porter launched Porter & Co. in the spring of 2022, we took notice. However, we did not recommend readers buy shares at that time…

That’s because we believed interest rates were likely to rise dramatically, which would cause the economy to slow and trigger a significant reduction in housing demand. While this would not be an existential threat to NVR like it could be to other homebuilders, we believed NVR’s earnings were likely to fall by 50% or more in the short term, and give us a much better entry price in the stock.

So instead, we added NVR to our Watchlist, and recommended readers look to buy the stock when it traded below $3,500 per share.

Unfortunately, we never got the chance.

The Housing Crisis That Wasn’t

We misjudged the impact of rising interest rates on the housing market.

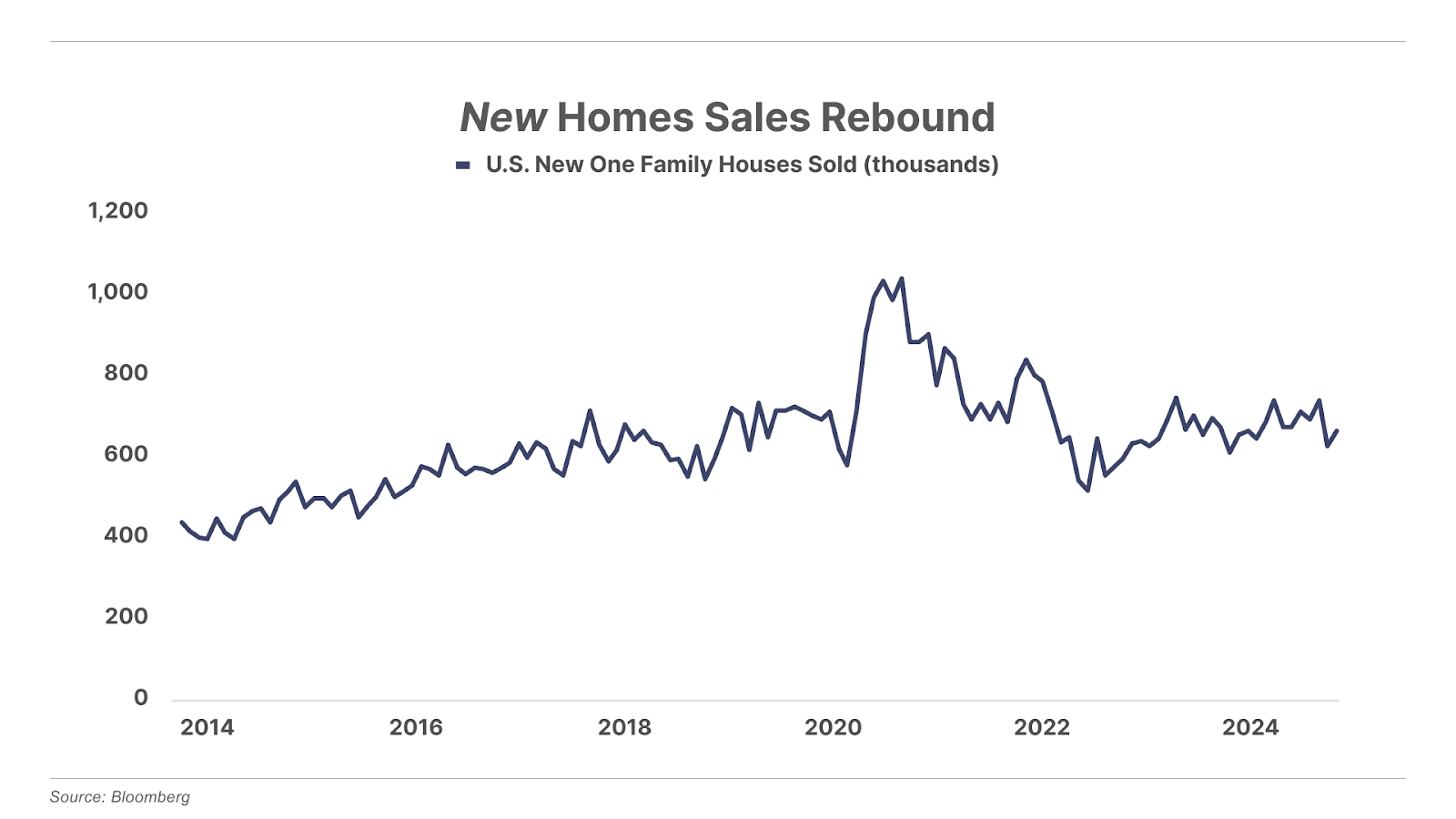

While higher rates did discourage some would-be home buyers who could no longer afford to buy a house, they also discouraged many would-be sellers who didn’t want to give up the historically low rates on their existing mortgages – which they had locked in years earlier.

As a result, existing home sales plunged more than 30% and have remained well below their pre-COVID trend ever since.

This dramatic decline in existing homes for sale meant that new home sales actually held up surprisingly well, despite significantly higher mortgage rates.

Steady demand for new homes has allowed many homebuilders to perform well despite a general weakening in the broad housing market. And NVR, because it is a high-quality business, has been among the best performers.

As you can see in the following chart, NVR shares have gained 110% since we added it to our Watchlist (instead of recommending readers buy it). The shares trade for around $8,200 today.

Our Second Homebuilder Mistake

Unfortunately, that wasn’t our only mistake with homebuilders.

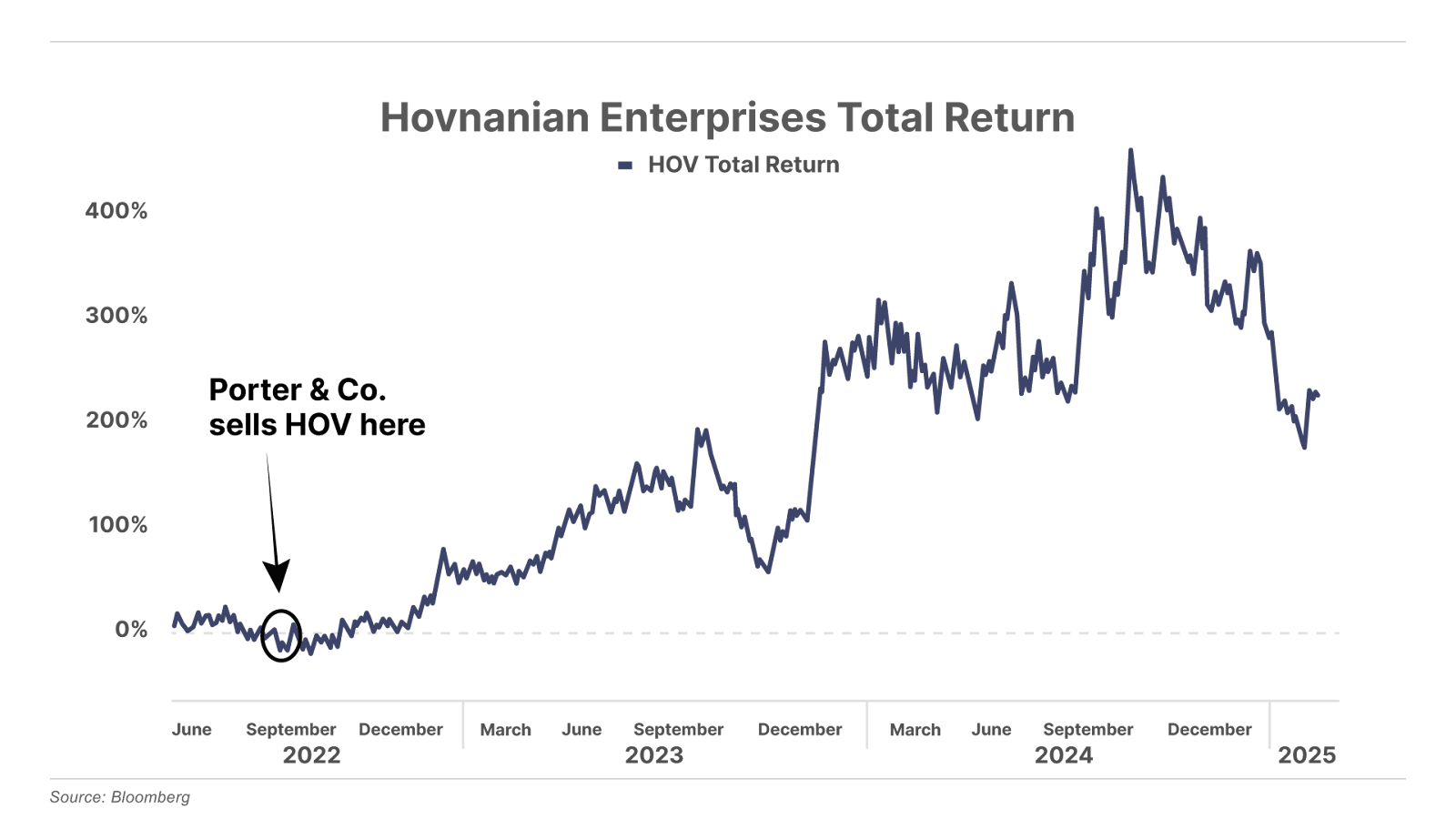

You see, while we added NVR to our Watchlist, we recommended readers buy shares of “the next NVR” instead: Hovnanian Enterprises (HOV).

Hovnanian’s turnaround story was similar to NVR’s.

However, recent major improvements to operations had led to better operating margins. As its debt load fell, the company had begun to produce substantial amounts of net income, setting the stage for a meaningful turnaround at Hovnanian.

What were these major improvements to operations? As you can probably guess, Hovnanian adopted key elements of the NVR business model, most notably using options, rather than traditional land development, to acquire building lots.

This shift was quietly transforming Hovnanian into a fantastic business. In 2021, it generated gross margins of 21%, an NVR-like 29% ROA, and a better-than-NVR 53% return on invested capital.

Yet because of the company’s long history of poor performance – and its still junk-level credit rating – the market didn’t believe in this turnaround. Hovnanian was trading at a market capitalization of less than $250 million, which was roughly 40% of what it expected to earn, in cash, that year.

As we noted at the time, we had “rarely (and maybe never) seen such a high-quality business trading for such incredibly low prices, relative to earnings.”

So despite our concerns about higher rates and a weakening housing market, we wisely recommended readers buy shares of Hovnanian at that time, at a share price of $42.79…

Unfortunately, mortgage rates moved above 6% just a few months later. HOV shares – which had been trading as much as 25% above our recommendation price – quickly turned lower. And we got spooked – fearing that our worst-case scenario was playing out – and on September 29, 2022, we recommended readers sell Hovnanian for a 14.7% loss.

Shares would ultimately bottom less than one month later, and absolutely soar over the next two years. If we had simply held on to HOV shares, we would be up more than 250% today.

We had the chance to buy and hold two great businesses trading at fair (or incredibly cheap!) prices. And whenever you have the chance to do that, selling (or not buying in the first place) is almost always a mistake.

These mistakes cost far, far more than the money we’ve lost over the years buying a business that does not perform.

So what’s the solution? That’s simple: Buy great businesses – especially when they’re trading at great prices. And do our best to never sell them… Ever.

Expect us to follow this rule more closely in The Big Secret portfolio going forward.

If you’re not already a subscriber to The Big Secret On Wall Street, click here to learn more… or call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.

Is 2025 The Best Time To Get Rich In American History?

One genius investor now predicts that the first 365 days of the Trump presidency will be the best time to get rich in American history.

Over the next 12 months…

One specific investment is set to potentially blast off by up to 12,000%.

If he’s right, two “wealth drivers” colliding now will create the greatest ever wealth-building opportunity for regular Americans. Must be in by August 30. Free instructions here.

Three Things To Know Before We Go…

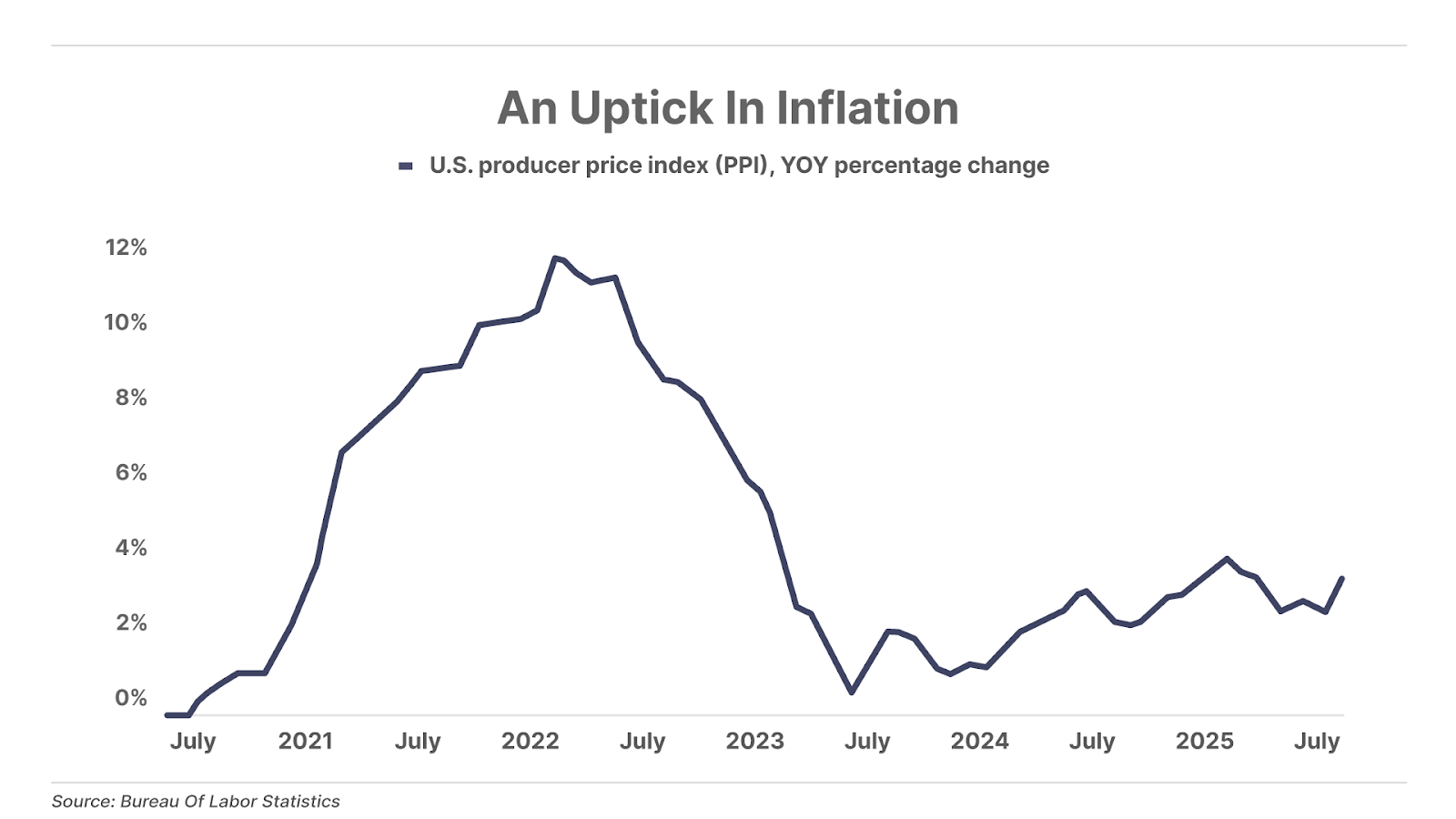

1. Producer price inflation surprises to the upside. On Thursday, the Bureau of Labor Statistics reported that its producer price index (“PPI”) – a measure of the selling prices received by U.S. producers for their output – rose 0.9% in July (3.3% year-over-year), versus Wall Street expectations of just 0.2% (2.5% year-over-year)… the largest monthly jump in more than three years. Rising producer prices often feed into rising consumer prices, suggesting consumer inflation could be headed higher. Despite this inflation surprise, the market still expects the Federal Reserve to cut interest rates next month, with the CME’s FedWatch tool showing a 90% chance of a 25-basis-point cut.

2. Buffett buys into UnitedHealth. Berkshire Hathaway’s latest 13F filing revealed the conglomerate has taken a new position in UnitedHealth (UNH), purchasing 5 million shares for $1.6 billion. The news sent shares of the healthcare giant up more than 10%. The purchase is another testament of Warren Buffett’s strategy of buying high-quality companies with strong fundamentals when they’re trading at an attractive price.

3. The latest sign of speculative frenzy. The share of retail options trading has surged to over 20% over total trading activity, a record high. The majority of options trading has historically been among large, institutional investors hedging their portfolios. But more recently, retail traders have turned to options as a way of juicing their market exposure with cheap but high-risk leverage – yet another sign of everyday traders venturing far out onto the risk curve in today’s market.

Looking for a smart way to trade with options? The Trading Club was built to take the other side of speculative trades, by primarily focusing on selling options for income, while also managing downside risk. Porter & Co. analysts offer step-by-step instructions and track it all in a live portfolio, which has grown from $100,000 to over $109,000 in just the first 75 days through steady and consistent gains rather than speculative bets. We’re opening The Trading Club for new members next week, stay tuned.

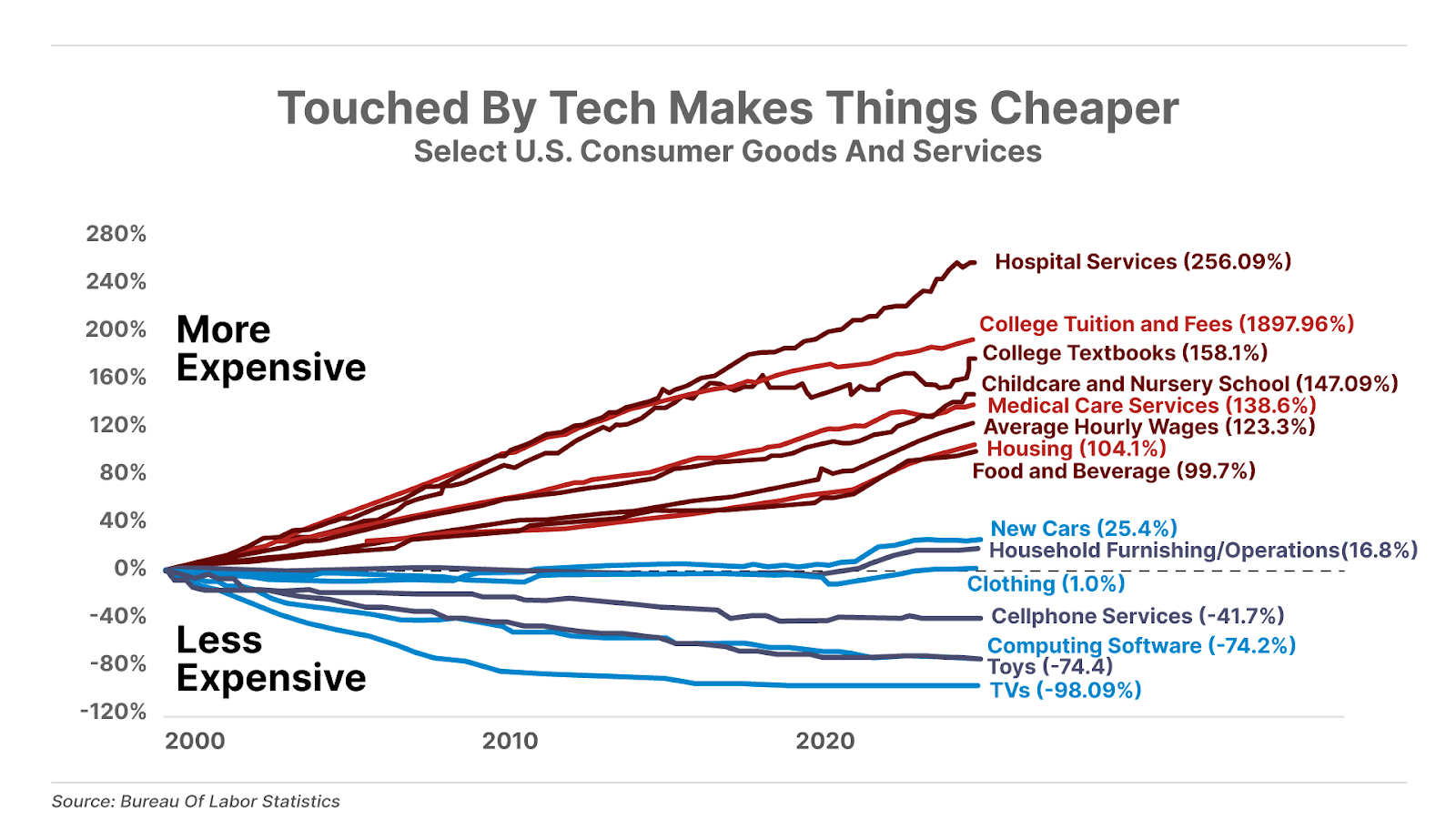

And One More Thing… Tech Drives Down Prices Despite Government Money-Printing

In a recent address at the Reagan National Economic Forum, tech investor Marc Andreessen showed the following chart pointing out that everything technology touches goes down in price – “TV sets, computer games, and electronics,” he said. Meanwhile, the major components of the economy have not been touched by technology and have seen prices rise over the last 25 years – housing, education, and healthcare as lead examples – as currency debasement continually erodes the purchasing power of the U.S. dollar.

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.