This is Porter & Co.’s The Big Secret on Wall Street, which we publish every Thursday at 4 pm ET. Once a month, we provide to our paid-up subscribers a full report on a stock recommendation, and also a monthly extensive review of the current portfolio… At the end of this week’s issue, paid-up subscribers can find our Top 3 “Best Buys,” three current portfolio picks that are at an attractive buy price. You can go here to see the full portfolio of The Big Secret.

Every week in The Big Secret, we provide analysis for non-paid subscribers. If you’re not yet a subscriber, to access the full paid issue, the portfolio, and all of our Big Secret insights and recommendations, please click here.

Many investors believe the biggest mistake you can make is buying a stock that performs poorly.

Like us, with The Big Secret on Wall Street’s December 2022 recommendation of Icahn Enterprises (IEP), which we closed after five months for a 51% loss. Or worse, our July 2023 recommendation of Altisource Asset Management (AAMCF) which fell 83% in less than six weeks. Both of these earned a spot in our portfolio’s Hall of Shame.

But those mistakes – while important (and money-losing!) – are not as bad a use of capital as the mistakes we’ve made by selling great businesses (or not buying them to begin with) because we got spooked following a lousy quarter or we were worried about macroeconomic factors like interest rates.

Few investors remember that many great businesses – including AT&T (T), ExxonMobil (then called Standard Oil) (XOM), and Hershey (HSY) – continued to pay their dividends during the Great Depression, the worst economic crisis in American history.

Most investors probably don’t remember that many of the then-top technology companies – such as IBM (IBM), Intel (INTC), and Texas Instruments (TXN) – maintained their dividends during the dot-com bust.

And many investors may not even remember that many high-quality consumer businesses – like Walmart (WMT), Johnson & Johnson (JNJ), and McDonald’s (MCD) – didn’t cut their dividends during the 2008-2009 Global Financial Crisis.

The point is, no matter what happens in markets or the economy, great businesses tend to do well over the long run. So, if you own one of these businesses and can afford to be patient, it’s almost always a mistake to sell.

Here in The Big Secret, we generally try to recommend only great businesses (outside of the occasional more speculative opportunity). As a result, virtually every time we’ve sold – or waited to buy – it has been a mistake.

In this issue we highlight a few of the most notable of these mistakes we’ve made, and show you the investment returns we missed out on by being too conservative when buying and holding great companies.

The Best Business We Didn’t Buy

In the July 1, 2022, issue of The Big Secret on Wall Street, we highlighted the remarkable business model of homebuilder NVR (NVR).

Most homebuilders are poor long-term investments. That’s because they’re terribly capital inefficient businesses – they require enormous amounts of capital to operate.

They take on debt to buy up big plots of land in areas where they think they’ll be able to build and sell houses. And to be fair, when they buy the right properties, in the right places, at the right price, they can make a lot of money. That’s why most homebuilders like to tout the size and quality of their land holdings.

However, over time, these companies inevitably end up owning too much land, in the wrong places, purchased at the wrong price. When the economy hits a rough patch, these companies struggle as the value of their land holdings fall relative to their high debt loads.

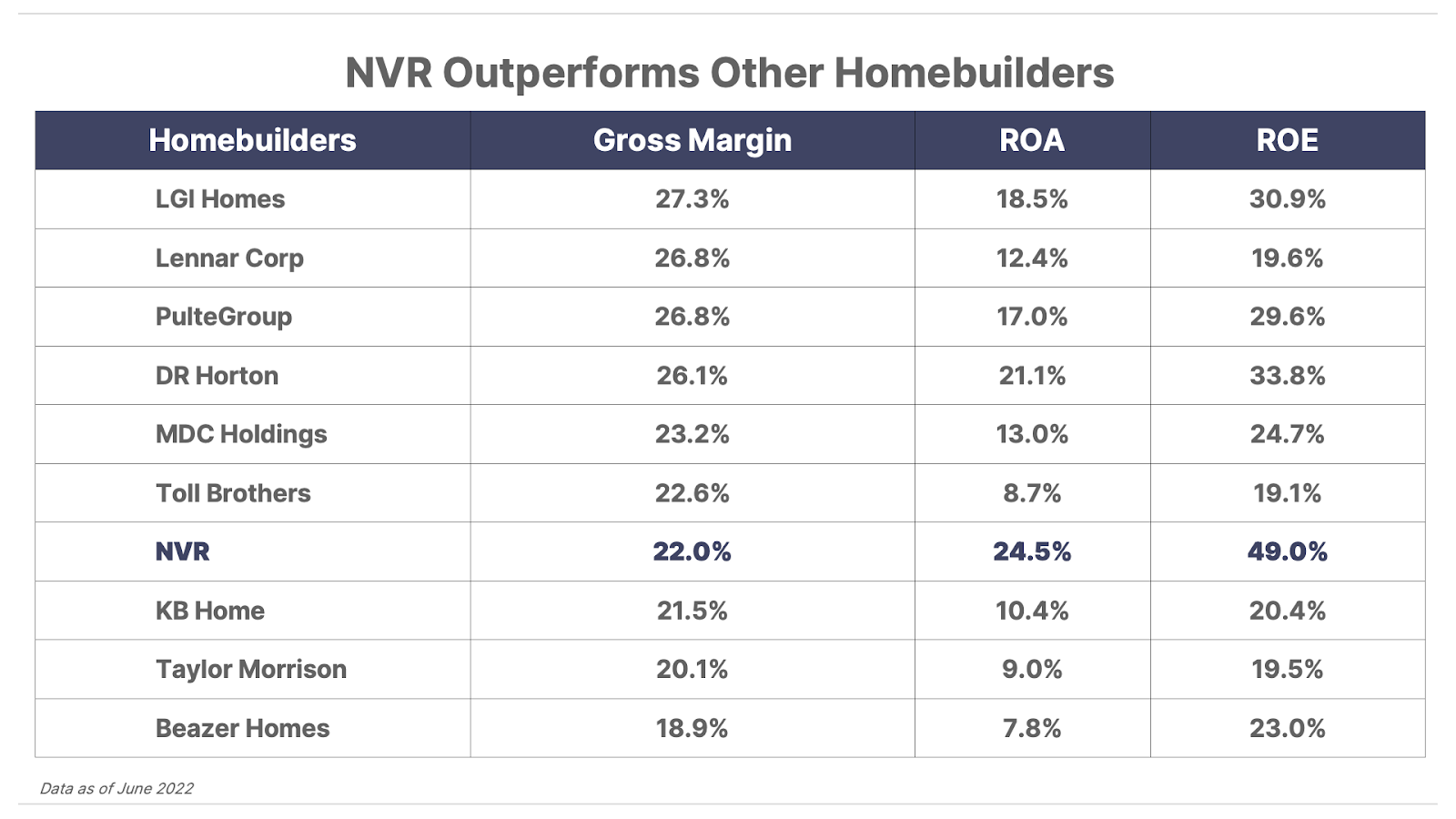

On the surface, NVR looks similar to other homebuilders. It builds homes in 35 metropolitan areas under a range of brands, such as Ryan Homes and Heartland Homes. It sells to both first-time home buyers and move-up buyers. And if you look at the company’s gross margins, you won’t find anything extraordinary. They’re roughly on par with most other large homebuilders.

But that’s where the similarities end. If you dig a little deeper, you’ll see that NVR’s return on assets (“ROA”) and return on equity (“ROE”) are significantly higher than other homebuilders. In fact, NVR’s ROE is more than double the industry average.

In other words, NVR is vastly more profitable than the average homebuilder.

Often when you find a company with such a big advantage in ROE, it’s because the company is highly leveraged. But NVR actually carries no net debt at all.

NVR’s secret is that it figured out a way to profit from massive capital investments without having to own those assets. And it happened almost by accident. As we explained in that issue…

NVR suffered a financial collapse during a national economic downturn. [It] filed for bankruptcy on April 6, 1991, on the heels of the U.S. savings and loan crisis. Its bankruptcy was complicated because [NVR] had a CFO, Anthony Satariano, who embezzled money from NVR’s finance operations.

[But] embezzling wasn’t the real problem.

NVR failed because of major changes to the tax code. The ‘86 tax reform removed tax benefits related to limited partnerships that invested in real estate. These incentives previously led investors to pile into real estate developments, leaving most of NVR’s key markets dramatically overbuilt. By 1990, NVR’s inventory was 50% above normal. Then a mild recession hit. Revenues from homebuilding fell in half over three years. The hundreds of millions worth of land on its books became a burden the company could no longer finance.

While it was still in bankruptcy (and unable to acquire additional land), the company pioneered a new business model. Necessity was the mother of invention.”

In short, instead of developing large tracts of land itself, NVR partnered with independent developers to buy “options” on lots. More from that issue…

NVR would still sell lots in NVR-branded communities. But rather than owning the land outright, NVR would pay a small fee – an option – for an exclusive right to resell the land to homebuyers. The developers were only paid for their lots after they were sold by NVR.

That put the entire risk of land prices on the developer. And it meant that NVR’s capital outlay – the cash it had to spend up front – was a fraction of what it would be following a more traditional model.

NVR then further reduced its capital needs by only starting construction after a new home was sold. Thus, it only built houses that were already paid for, via down payment and mortgage lending.

In this way, NVR was able to sell lots it didn’t actually own. And it could sell houses without having to finance their construction.”

This new business model gave NVR a huge advantage over other builders. So it decided to focus exclusively on this more capital efficient approach – in addition to pioneering faster and cheaper ways of building high-quality houses.

As a result, when NVR emerged from bankruptcy in 1993, it was able to build a detached home in less than three months (86 days) versus an industry average of around seven months.

This combination of high capital and operating efficiency has made NVR one of the best performing companies of the past few decades.

In fact, in the 20 years between 1996 and 2016, it had the highest returns on equity of any company with a market cap of $100 million or more – beating all the high-flying tech stocks of the dot-com boom and generating share-price returns of almost 30% annually, despite the mortgage crisis between 2008 and 2011.

NVR is one of the relatively few businesses we consider “must own,” and it was a long-time holding of Porter’s Stansberry’s Investment Advisory portfolio at his previous firm.

So when shares dipped below $4,000 per share – trading at roughly half its average price-to-earnings (P/E) ratio of 15 – shortly after Porter launched Porter & Co. in the spring of 2022, we took notice.However, we did not recommend readers buy shares at that time…

That’s because we believed interest rates were likely to rise dramatically, which would cause the economy to slow and trigger a significant reduction in housing demand. While this would not be an existential threat to NVR like it could be to other homebuilders, we believed NVR’s earnings were likely to fall by 50% or more in the short term, and give us a much better entry price in the stock.

So instead, we added NVR to our Watchlist, and recommended readers look to buy the stock when it traded below $3,500 per share.

Unfortunately, we never got the chance.

The Housing Crisis That Wasn’t

As we expected, U.S. interest rates – and mortgage rates in particular – did continue to rise dramatically as the Federal Reserve tightened monetary policy. The average rate for a 30-year fixed rate mortgage rose from around 5% in the summer of 2022 to nearly 8% by October 2023.

However, we misjudged the impact of rising interest rates on the housing market.

While higher rates did discourage some would-be home buyers who could no longer afford to buy a house, they also discouraged many would-be sellers who didn’t want to give up the historically low rates on their existing mortgages – which they had locked in years earlier.

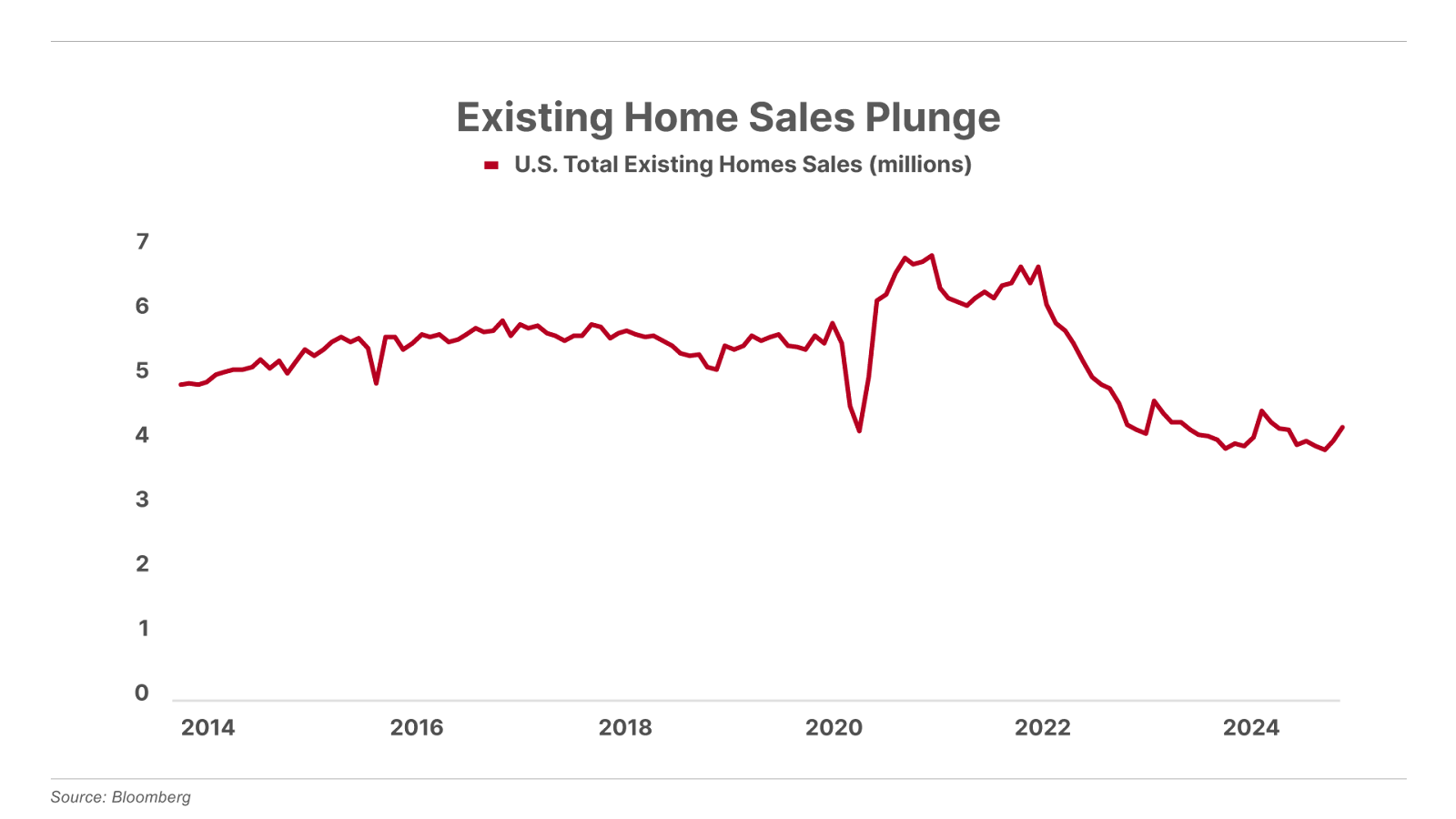

As a result, existing home sales plunged by more than 30% and have remained well below their pre-COVID trend ever since.

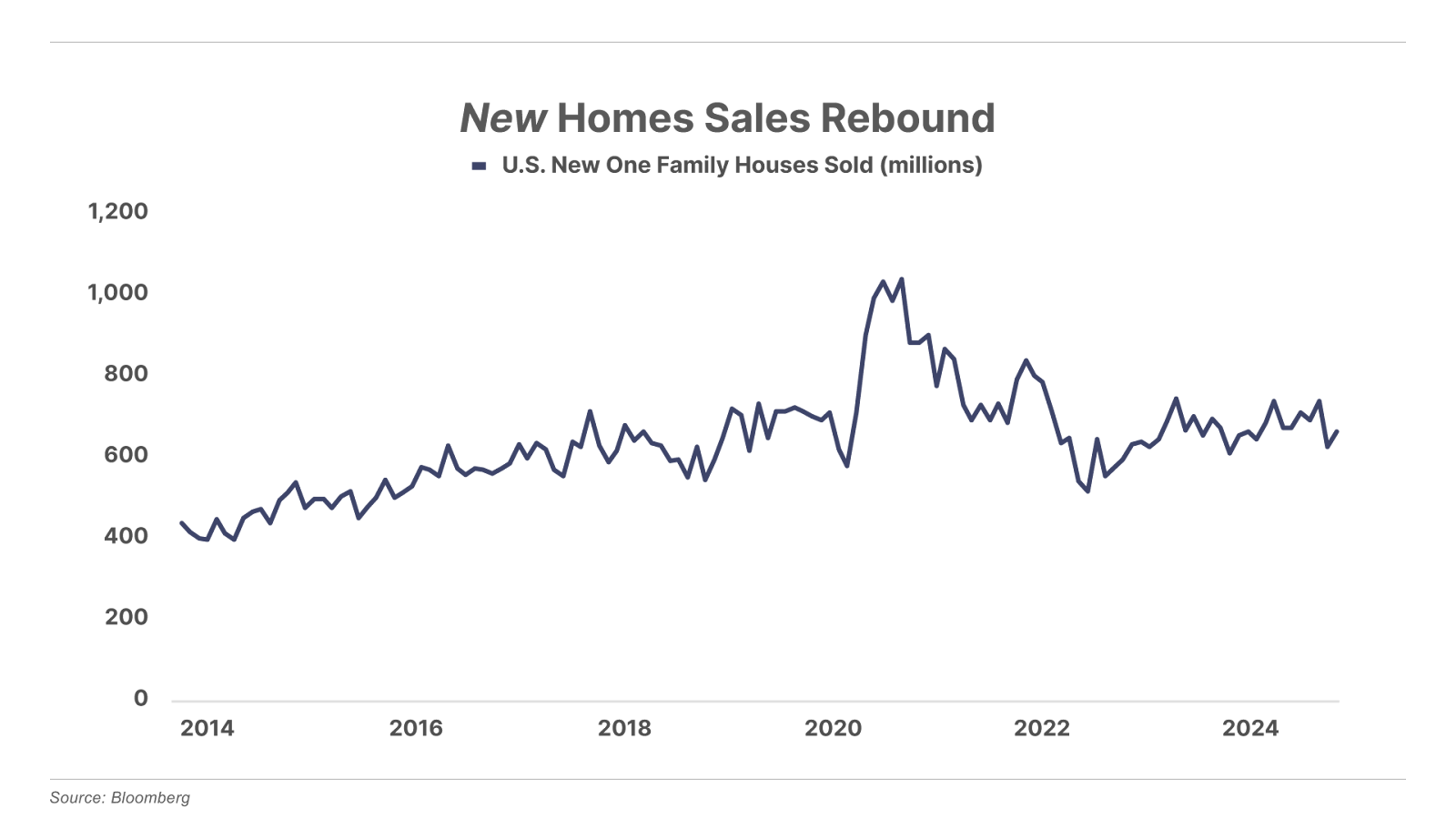

This dramatic decline in existing homes for sale meant that new home sales actually held up surprisingly well, despite significantly higher mortgage rates. They, too, initially declined in 2022. However, new home sales rebounded quickly and have since returned to their pre-COVID trend.

Steady demand for new homes has allowed many homebuilders to perform well despite a general weakening in the broad housing market. And NVR, because it is a high-quality business, has been among the best performers.

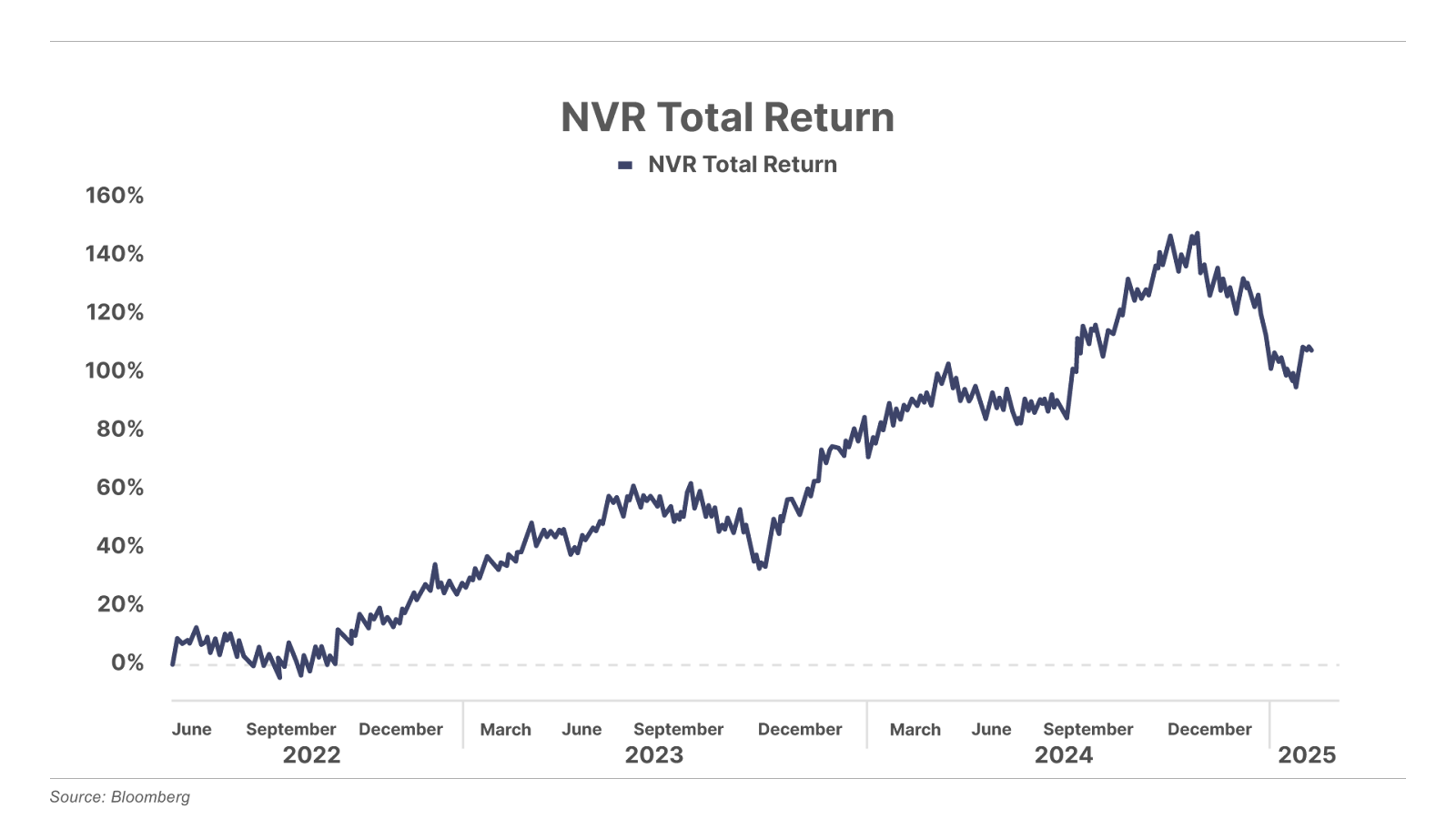

As you can see in the following chart, NVR shares have gained 110% since we added it to our Watchlist (instead of recommending readers buy it). The shares trade for around $8,300 today.

Our Second Homebuilder Mistake

Unfortunately, that wasn’t our only mistake with homebuilders.

In fact, it wasn’t even our only mistake with homebuilders in that issue.

You see, while we added NVR to our Watchlist, we recommended readers buy shares of “the next NVR” instead: Hovnanian Enterprises (HOV).

Hovnanian’s turnaround story was similar to NVR’s. As we explained in the issue:

Few homebuilders suffered as much as Hovnanian and still survived the mortgage crisis of 2008-2011.

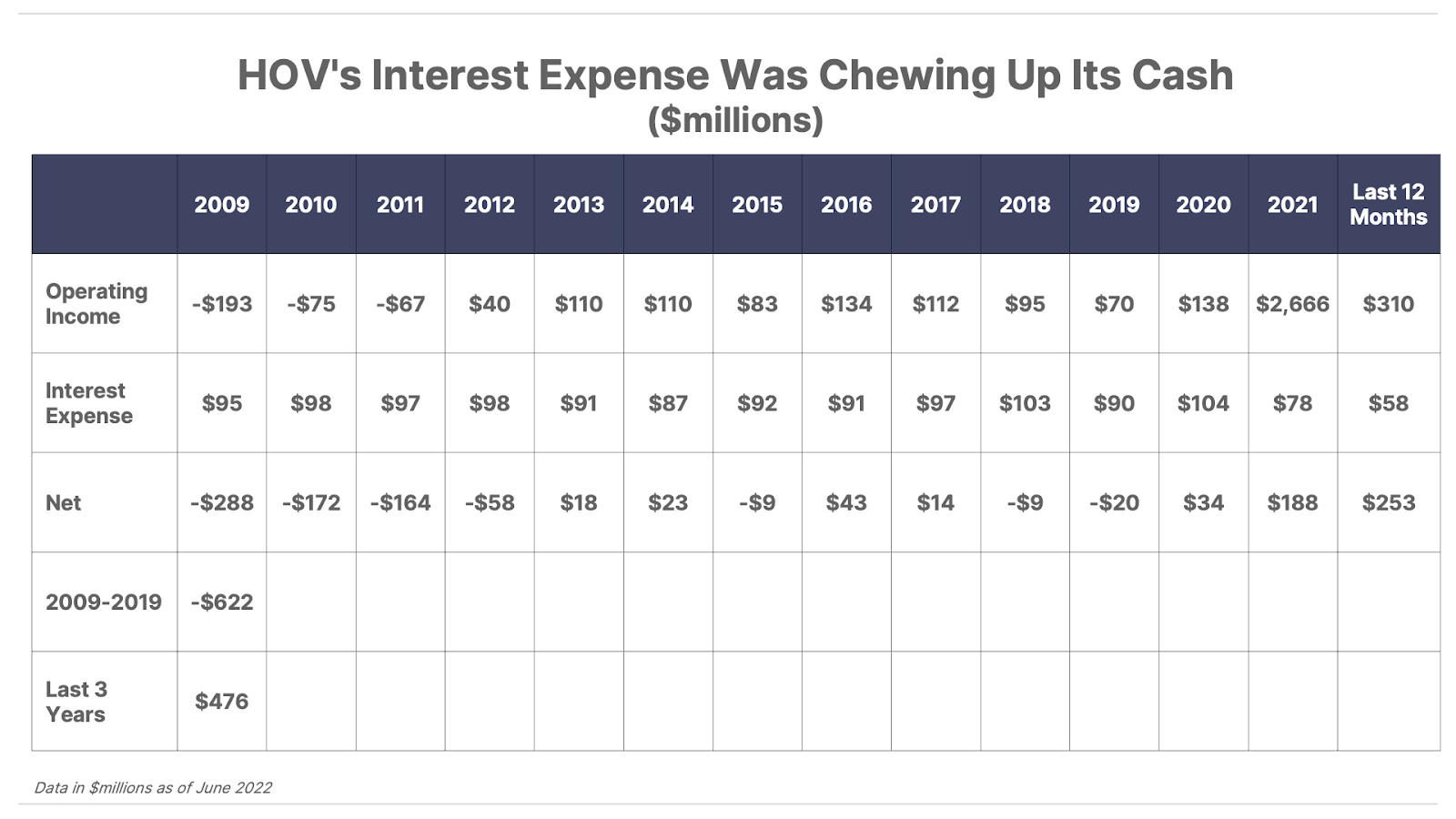

Hovnanian’s losses were horrendous. The company wrote off $1.6 billion worth of real estate between 2008 and 2012. It was still writing off significant amounts of real estate holdings as late as 2017. Beyond the write-offs, the company was so poorly managed that it couldn’t even make money on operations from 2007-2011.

Meanwhile, the company was drowning in debt. HOV spent around $100 million a year on interest expenses every year from 2008 until 2021. That consumed virtually all of the company’s operating income…”

The chart below shows this trend at the time of our recommendation.

As you can see, even a decade after the 2008-2009 crisis, Hovnanian was still spending more to service its debt than it could make building and selling homes.

However, recent major improvements to operations had led to better operating margins. As its debt load fell, the company had begun to produce substantial amounts of net income, setting the stage for a meaningful turnaround at Hovnanian.

What were these major improvements to operations? As you can probably guess, Hovnanian adopted key elements of the NVR business model, most notably using options, rather than traditional land development, to acquire building lots.

This shift was quietly transforming Hovnanian into a fantastic business. In 2021, it generated gross margins of 21%, an NVR-like 29% ROA, and a better-than-NVR 53% return on invested capital.

Yet because of the company’s long history of poor performance – and its still junk-level credit rating – the market didn’t believe in this turnaround. Hovnanian was trading at a market capitalization of less than $250 million, which was roughly 40% of what it expected to earn, in cash, that year.

As we noted at the time, we had “rarely (and maybe never) seen such a high-quality business trading for such incredibly low prices, relative to earnings.”

So despite our concerns about higher rates and a weakening housing market, we wisely recommended readers buy shares of Hovnanian at that time, at a share price of $42.79…

The low stock price reflects the market’s belief that HOV could go bankrupt if the coming recession is bad enough or if mortgage rates move substantially higher. On the other hand, if the coming market contraction in housing isn’t as bad as feared, Hovnanian is probably worth 10x what it is trading for today.

If rates don’t go above 6% and demand for housing continues and doesn’t collapse, Hovnanian could become an investment grade credit by the end of next year – 2023. That’s because it is using the NVR model and is now incredibly capital efficient. An investment-grade company that’s earning something around $300 million per year should be worth at least $2.5 billion, not $250 million (its current market cap)…

Thus, we see buying HOV today as a lot like buying NVR back in ’96, as it was finally emerging from bankruptcy. Nobody saw NVR coming, because most investors simply do not understand how much more profitable it is to sell capital goods – like houses and energy – without having to own the underlying assets.”

Unfortunately, mortgage rates did move above 6% just a few months later. HOV shares – which had been trading as much as 25% above our recommendation price – quickly turned lower. We got spooked – fearing that our worst-case scenario was playing out – and on September 29, 2022, we recommended readers sell Hovnanian for a 14.7% loss.

Shares would ultimately bottom less than one month later, and absolutely soar over the next two years. If we had simply held on to HOV shares, we would be up more than 220% today.

The Third Time Is (Not) A Charm

Despite our continuing concern about the housing market, we found another opportunity in homebuilders in early 2023 that was simply too good to ignore.

Our thesis was simple: Dream Finders Homes (DFH) was even more like NVR than Hovnanian Enterprises.

In fact, outside of NVR, it was the only other publicly traded homebuilder that was using the same 100% asset-light playbook. Yet it had two distinct advantages.

First, because it was much earlier in its growth trajectory than NVR – it had been founded less than 15 years earlier, in 2008 – it was growing much faster. For comparison, Dream Finders had been growing revenue by 40% annually, versus a less-than-10% annual rate for NVR.

Second, the company was trading at a remarkably cheap valuation of just 6x earnings – a 50% discount to NVR’s 12x earnings – because of its (temporarily) lagging profit margins. As we explained in the April 28, 2023, issue of The Big Secret on Wall Street…

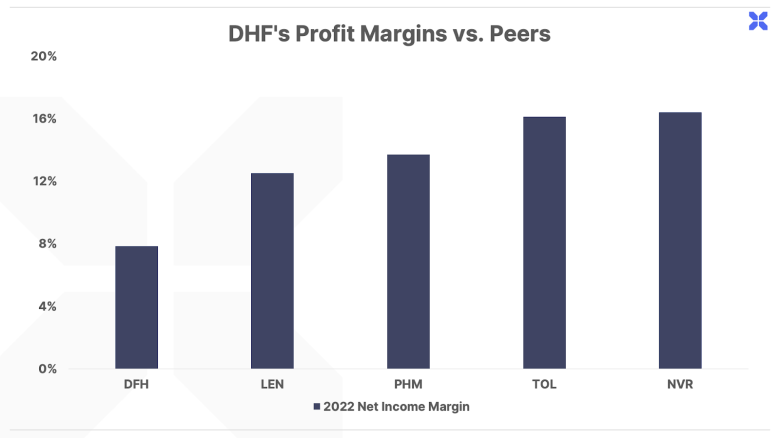

Even though DFH doesn’t pay for its land up front, it still incurs substantial costs for labor and materials… And, unlike its larger competitors, DFH can’t spread those costs across a huge customer base.

Established home builders typically generate net profit margins ranging from 12% to 16%. Because DFH has not yet grown to similar levels of sales volumes, the company’s current profit margins are roughly half of its peer group’s, at 7.8% in 2022:

But thanks to DFH’s rapid growth profile, the company is quickly expanding its profit margins. Over the last four years, profit margins have more than doubled from 3.3% to 7.8%.

We believe the market is making a mistake in punishing DFH with a discounted valuation, by over-emphasizing the company’s low profit margins today, and ignoring the company’s outsized growth and potential for margin expansion in the years ahead… DFH’s profit margins are increasing as it grows in each of its markets, and that’s a trend we expect will continue over the long term.”

Due to this combination of depressed valuation and rapid growth potential, we believed Dream Finders could actually exceed the market-crushing returns NVR had produced since Porter first recommended it in October 2007.

Our thesis has played out even better than expected so far. In that issue, we laid out a future path for DFH shares to return 1,000% based on revenue reaching $3 billion with a 7.8% profit margin in 2024. As it turns out, the company likely generated $4 billion last year and hit our 7.8% margin, explaining why shares have rallied over 50% since our original recommendation.

Selling A Great Business Is Almost Always A Mistake

Unfortunately, we weren’t along for most of that ride.

Mortgage rates began to soar immediately after our recommendation, from just 6% in April 2023 to nearly 8% in October 2023.

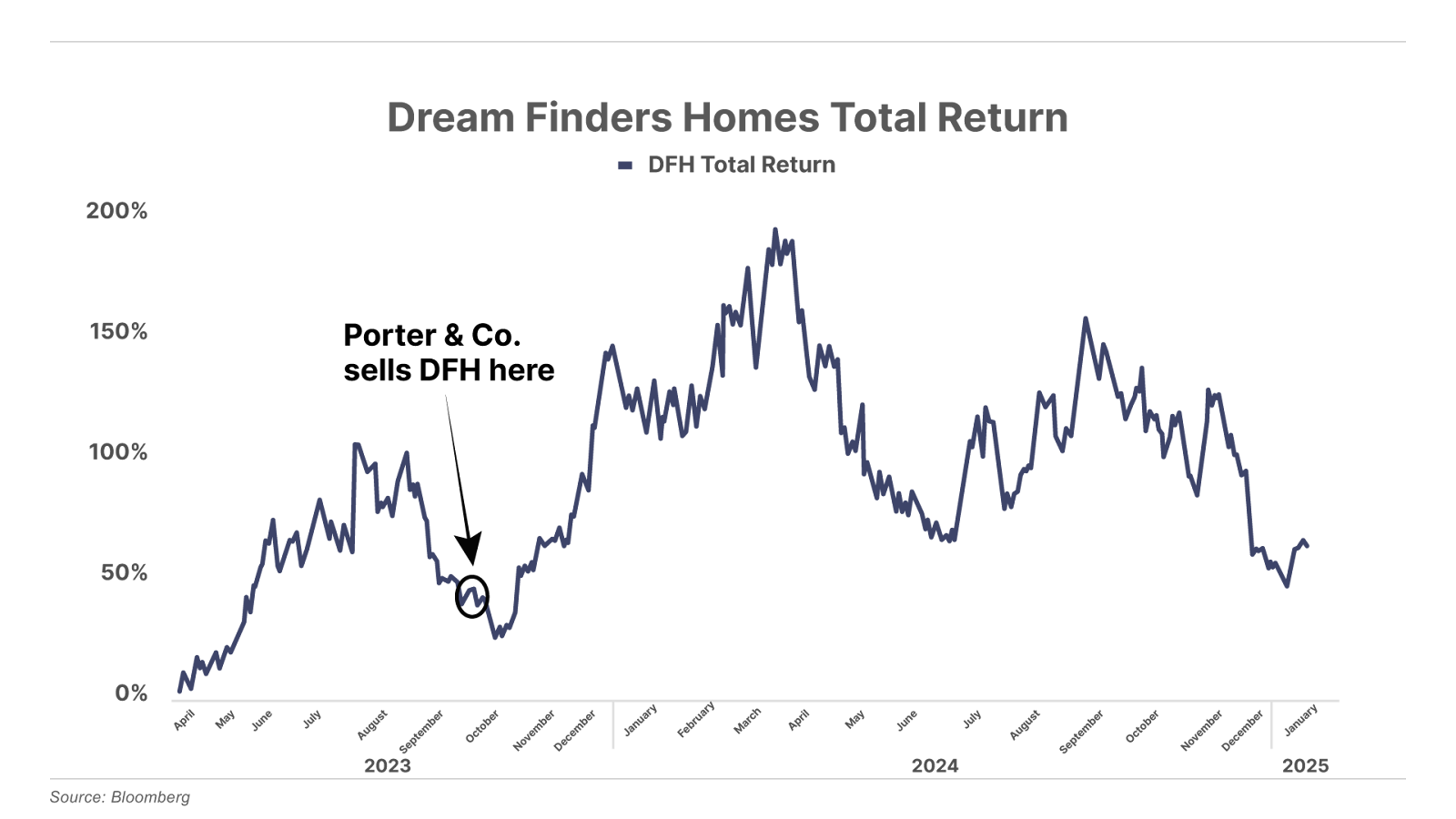

Once again, we got spooked – letting relatively short-term macro concerns undermine our confidence in an otherwise fantastic business – and recommended readers sell Dream Finders Homes for an impressive 38.95% gain. But once again, selling was a mistake.

Shares bottomed just a couple of weeks later. And even after a significant correction last year, shares are trading more than 63% higher today than when we first recommended them.

Again, in hindsight, we clearly underestimated the resiliency of the U.S. housing market, and the new housing market in particular.

But that wasn’t our biggest mistake. Our biggest mistake was thinking that those short-term concerns really mattered in the long run.

We had the chance to buy and hold three great businesses trading at fair (or incredibly cheap!) prices. And whenever you have the chance to do that, selling (or not buying in the first place) is almost always a mistake.

These mistakes cost far, far more than the money we’ve lost over the years buying a business that does not perform.

So what’s the solution? That’s simple: Buy great businesses – especially when they’re trading at great prices. And do our best to never sell them… Ever.

Expect us to follow this rule more closely in The Big Secret portfolio going forward. And don’t be surprised if we revisit these names (along with those on our Big Secret Watchlist) in the months ahead.

If you’re not yet a Big Secret subscriber, you can get full access to our recommended portfolio and Watchlist right here.

In the meantime, we continue to urge subscribers to raise some cash if you haven’t done so already. Holding a comfortable cash cushion when stocks are generally expensive (like they are today) is one of the simplest ways to ensure you’re able to weather short-term market drawdowns in great businesses you intend to hold for the long run. Having plenty of cash also allows you to add to those positions at bargain prices when other investors are panicking.

Porter & Co. Stevenson, MD

This content is only available for paid members.

If you are

interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.