Porter & Co. is looking for a “maniacal” distressed debt analyst… see the end of this email for details…

- “Battleship” Stocks That Are Truly Unsinkable

- The Magic of Capital Efficiency + Time

- The Difference Between “When” Stocks and “If” Stocks

Late last month, the Wall Street Journal passed along a “great” stock tip.

It was only about a decade late.

“Any stock that doubles in five years, outperforms tech giants over three years and beats more than 450 companies in the S&P 500 this year is clearly worth studying,” the story began. The author helpfully included three stock charts showing, unmistakably, that Hershey, America’s chocolate champion, had handily beat the stock market over the last one (+45%), three (+37.8%), and five years (+70.5%).

And how could it not? Hershey, as a business, is one of the greatest in the history of capitalism. On virtually every metric, Hershey is a vastly superior business. Its return on common equity (currently 59%) is routinely four or five times the S&P 500 average.

Nevertheless, we couldn’t help but chuckle. The author, who seemed to know all the facts about the business, also proved that he knew nothing about Hershey as an investment. After all, Hershey hasn’t only beat the market recently… it’s beaten it forever. The stock outperforms the S&P 500 over virtually any reasonable investment period. Hershey has paid a dividend every quarter for more than 90 years. It’s raised its dividend every year since 1974.

Hershey isn’t an “if,” for investors — it is a “when.” That is, the question isn’t whether or not you should invest in Hershey, the question is only when should you invest in Hershey?

At Porter & Co., our goal is to educate, entertain and enrich. While buying Hershey may not be very entertaining, learning about companies that have such powerful internal economics that they will inevitably beat the market, is, by a wide margin, the most valuable lesson we could ever teach you. We hope every subscriber will learn to keep a list of the world’s most timeless and highest-quality businesses… and strive to become a lifetime shareholder of all of these businesses.

Put Hershey at the top of your list.

Hershey is the quintessential “Buffett stock” – it is an elite, ultra-high-quality business, which, if held for a reasonable period, will always produce market-beating results. Why? Because Hershey, like a small number of other beloved consumer franchise companies, possesses an asset you won’t find on its balance sheet. Buffett calls this “invisible” asset “economic goodwill.”

We’d urge all new subscribers to learn more about the concept of “economic goodwill” by reading Buffett’s explanation of it in his 1983 Chairman’s Letter.

But, to summarize it quickly… Buffett discovered that the positive feelings people have for certain brands, like Hershey and Coca-Cola, to name two, can translate into much better – enormously better – returns on assets and equity. It’s the public’s goodwill that enables these companies to raise prices easily, and helps protect them from competition, ensuring their profitability over the decades.

Buffett’s key discovery: these advantages compound over time. Meanwhile, accounting rules forbid marking up the value of “goodwill” on balance sheets. This produces a “blind spot” in financial databases. It’s a key economic asset that’s invisible to accountants and to many investors.

The Wall Street Journal’s columnist didn’t explain any of this, of course. Even more importantly, he didn’t explain that, given Hershey’s ultra-consistent financial performance, the most important factor to consider when making an investment is the company’s share price. When you buy these kinds of stocks really matters, because they tend to grow slowly, and they tend to only trade at a low multiple to earnings rarely.

Most of the time, these super high-quality stocks are simply too expensive. If you buy at a high multiple of earnings, your total returns aren’t likely to be all that great. But… every now and then… maybe once every ten years or so… you’ll have a great opportunity to invest in these “forever” companies.

Porter first recommended shares of Hershey in November 2007 – right at the last big peak of stock prices, just before the global financial crisis. It was a very frothy time in the markets. But Hershey was overlooked by many investors, who were chasing commodity stocks and tech stocks at the time. Then the global financial crisis hit, and virtually every stock traded at a cycle-low multiple. As a result, Hershey traded below 20-times earnings throughout 2007, 2008, 2009, and 2010. Meanwhile, the business kept on doing fine. And… eventually… the market noticed.

Since Porter’s first recommendation, Hershey has seen total returns of 729% (15.2% annually) – almost 5 times the total return of the market. The S&P 500 is up 154% (8.6% annually) in the same period.

Those extraordinary returns only occurred because Hershey is an incredible business… and because Porter recommended buying it when it was trading at a reasonable price. Today Hershey is up 45% over the last year. It is now trading at close to 30-times earnings. Hershey is a “when” stock. And now is not the time to buy it.

But… what if there were another incredibly capital efficient business out there, one that’s beloved by the public, that has one of the world’s strongest consumer-facing brands…? And what if that stock’s share price has been sent reeling because of the lingering after-effects of the pandemic…? Oh, and what if it was one of the most all-American stories ever… and involved pizza?

The Most Expensive Pizza of All Time

On May 22, 2010, Jeremy Sturdivant, a 19-year-old student, saw a strange request from an online internet forum…

Laszlo Hanyecz, an early Bitcoin programmer, was offering 10,000 bitcoins in exchange for the delivery of two large pizzas to his Florida residence. Sturdivant fulfilled the order, sending two Papa John’s pizzas to the posted address. Moments later, the 10,000 bitcoins showed up in Sturdivant’s wallet, just as promised.

It was the first physical purchase made with bitcoin, and today is celebrated by crypto enthusiasts worldwide in the annual “Bitcoin Pizza Day” every May 22. It was also one of the most expensive financial mistakes of all time. In 2010, those 10,000 bitcoins were only worth around $40. Had Sturdivant simply held onto these coins, they’d be worth around $170 million today.

You probably think that’s the most amount of money ever lost on pizza. Nope.

In 1960, James Monaghan and his brother Tom were running a small pizzeria called Dominick’s in Ypsilanti, Michigan. It was a thriving enterprise, overwhelmed with demand from thousands of hungry college students at nearby Eastern Michigan University. But after eight months, James began feeling overworked. He wanted to focus more on his day job… at the local post office. No kidding. So James traded his 50% stake in the business for his brother’s beat-up Volkswagen.

Today, that 50% in what was Dominick’s would be worth $5 billion. And the story of how that came to be is something every investor should know.

The Birth of America’s Fast-Food Tradition

America’s fast-food boom began at a small San Bernardino hamburger stand.

The new restaurant concept founded by brothers Maurice and Richard McDonald was a complete departure from the traditional sit-and-serve or drive-through restaurants of the time. Mcdonald’s was custom engineered with one goal in mind: speed.

Instead of having individual cooks prepare meals from start to finish, the kitchen was divided into separate stations where each employee specialized in a single task. That’s how the McDonald brothers re-imagined the concept of a traditional kitchen to be more like an automotive plant assembly line, which they called the “Speedee System.”

The Speedee System slashed wait times for food orders from the traditional 20+ minutes to sixty seconds. Much faster prep times multiplied the order volume, allowing McDonald’s to underprice its burger rivals by around half. Finally, the most valuable feature of this business model was its scalability. By developing processes that could be replicated, McDonald’s could rapidly expand across the country through franchising.

Paid-up subscribers will recall from our franchise retailer recommendation (now up 15% since our September recommendation), we like the franchise business model. Franchises are vastly more capital efficient and have much stronger onsite management teams, which translates into much higher-than-normal returns on invested capital (ROIC).

What is ROIC?

Return on Invested Capital (ROIC) is the amount of money a company makes in profit (net income, after tax) divided by the amount of capital that’s invested in the company (equity + debt). What it shows you, of course, is how much money is being earned against the total amount of capital employed in the company. High returns on invested capital is a very good indicator of a capital efficient investment.

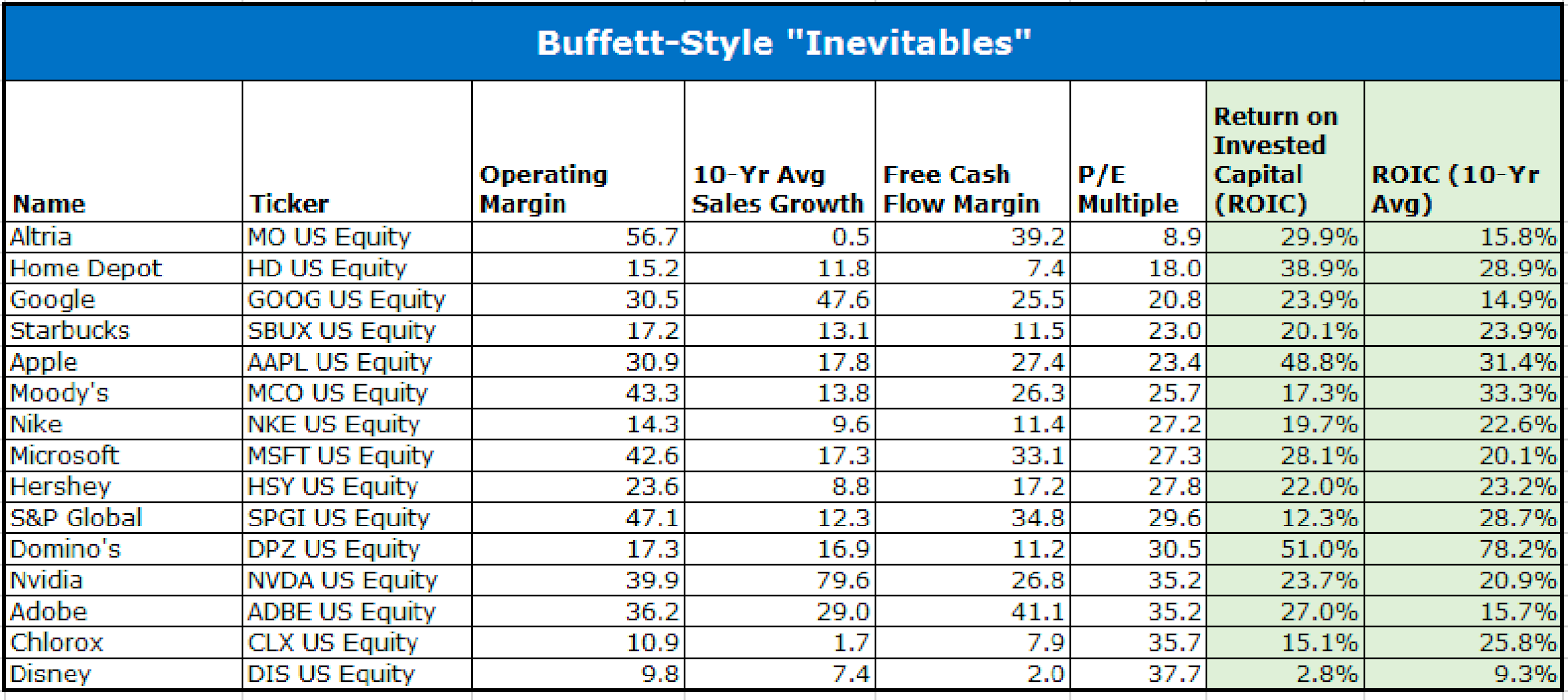

Let’s revisit our “Buffett Inevitables” list, comprised of 15 high-margin, capital efficient businesses. We originally published this list in July, here. This time, we look at these companies’ ROIC ratios.

All the stocks above have a 10-year average ROIC of 10% or greater, except Disney.

Let’s take Altria, a generational, capital efficient stock that we plan on holding forever. Altria’s 10-year average ROIC is 15.8%, meaning they made on average $15.80 in profits for every $100 they invested in the business over the past 10 years. Altria’s ROIC increased over the past 12 months to ~30%, meaning that it now makes $30 for each $100 of capital invested.

The difference in returns between two high ROIC companies and the S&P is clear, as shown below.

A High ROIC Company That Handily Beats Ronald McDonald

The lesson of McDonald’s – America’s most popular fast-food restaurant – is that consumers love convenience. McDonald’s isn’t gourmet. But it became the biggest restaurant company in the world by figuring out how to give consumers a product that’s good enough but is delivered with world-class efficiency and convenience.

But with a market capitalization of $200 billion, McDonald’s rapid growth days are behind it. That’s why today, we’re recommending a much smaller business that’s following the McDonald’s playbook. This business has established itself as the absolute leader in providing customers with the fastest, most convenient service among its quick service restaurant peers.

Thanks to its franchise model, it’s also a capital efficient business, generating 66% returns on invested capital. Since going public, its shares have handily outperformed McDonald’s shares, earning a 24% compounded return vs McDonald’s 17% over the same period.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.