Cheap money is grounding flights all over America – and that’s just the beginning.

Next Wednesday will be one of the busiest travel days of the year here in America. And if you’re flying somewhere, you’re likely a victim of cheap money.

That is… you’re suffering long delays… overworked staff… decrepit planes… and a customer experience that makes you wish you’d driven – no matter how far you’re going.

The airline industry in America has never been a beacon of efficiency or good customer service. But it’s been hitting new lows. One sign: In just the first half of 2022, more commercial flights were canceled in the U.S. than for all of last year.

Like many sectors of today’s economy, airlines are facing a crippling labor shortage. And it’s one of countless signals indicating an imminent economic dislocation in the months ahead.

But it’s more than that… and a lot of the fault lies where few people would think to look: Wall Street… and the devious, twisted incentives that cheap money created for short-sighted boardrooms all across America.

Buyback Bonanza Sets the Stage for Bailouts

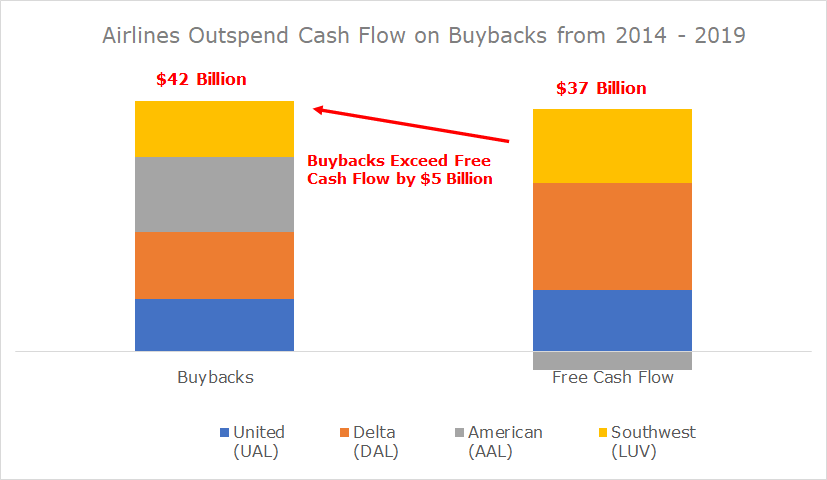

Over the last decade, America’s four major air carriers – Delta (NYSE: DAL), American (NYSE: AAL), Southwest (NYSE: LUV), and United (NYSE: UAL) – funneled all of their combined free cash flow into stock repurchases… and then some. Between 2015 and 2019, these four companies spent around $42 billion on share buybacks, while generating $37 billion in free cash flow.

In other words… not only did they use every penny of cash their businesses generated to buy their own shares… but they also borrowed even more to buy back shares.

The era of record-low interest rates allowed the airlines to leverage up their balance sheets to fund the buyback bonanza. The total debt among the four major carriers surged from $24 billion to $60 billion from 2014 to 2019, for a 148% increase:

Raising debt to buy shares isn’t smart. It’s especially not-smart for the airline industry, which – you’d think – should want to spend a significant portion of its cash on upgrading planes, investing in logistics infrastructure, and maintaining equipment for the ground crews servicing the planes… rather than buying back shares.

But airlines haven’t done this… if you need any evidence of this, just board a plane.

Their reasoning: why waste money on delivering a good product, when you can engineer earnings growth with borrowed money? And if money is almost free – the airlines (and much of the rest of corporate America) reasoned – why not?

For a while, the financial alchemy of borrowing money and using all available cash to buy shares, worked wonders. Earnings per share – the all-important Wall Street metric – is computed by dividing earnings by total shares outstanding… when a company buys back its own shares, the denominator of that equation shrinks (since bought-back shares are taken out of the calculation). And hey presto, earnings go up.

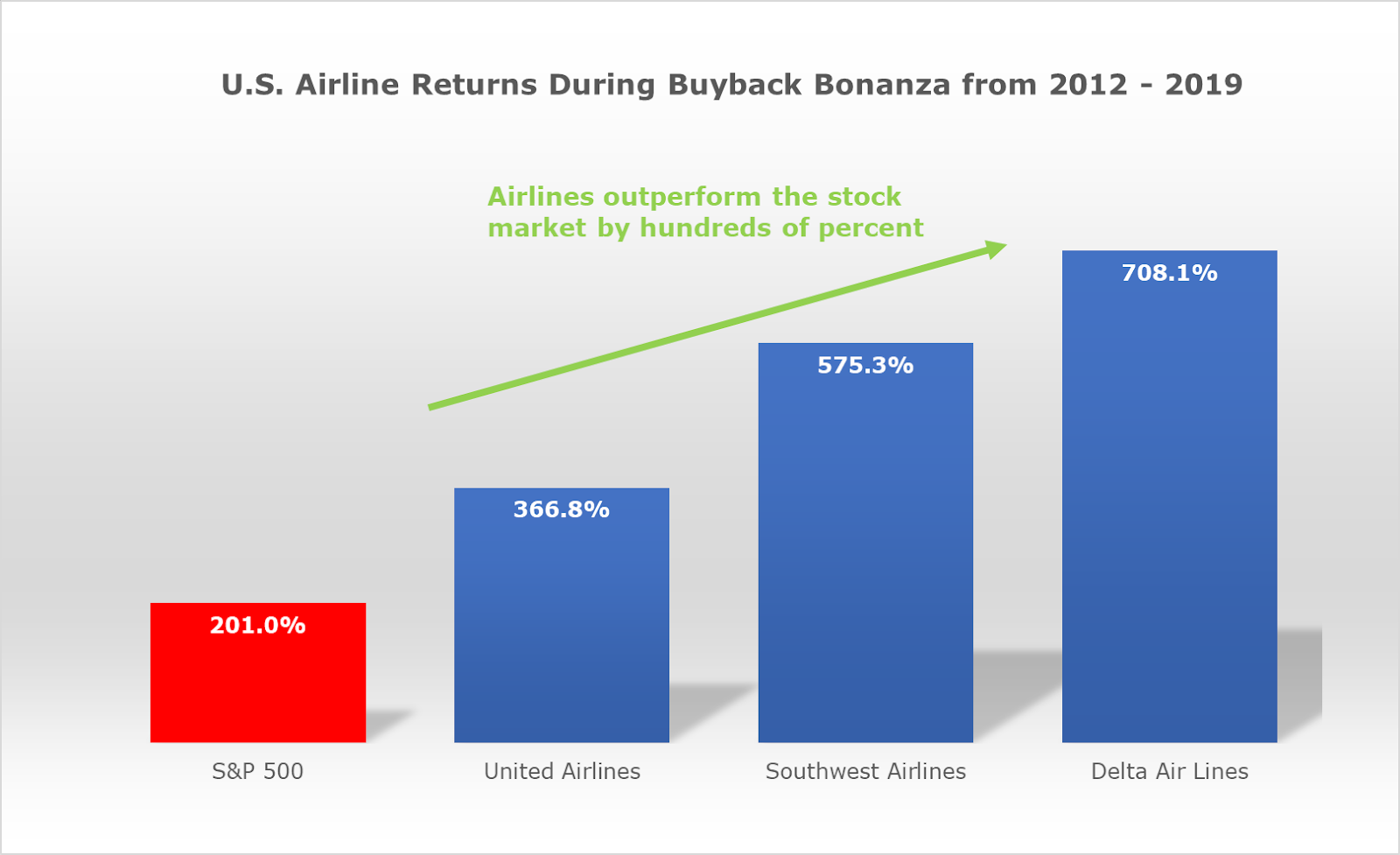

Investors loved it, and airline stocks soared into the stratosphere, beating the S&P 500 during the buyback bonanza of the last decade:

Meanwhile, airline executives – whose compensation was largely linked to the share price and earnings per share of their employer – were diving into bales of cash like Scrooge McDuck. Delta CEO Ed Bastian earned $17.3 million in 2019 alone. United’s CEO made $12.6 million in 2019, followed by $21 million the following year.

In the short term, (almost) everyone wins in this game: Shareholders are thrilled, and corner-office dwellers can buy their second yachts. But the rest of us peasants – those of us riding cattle car in aluminum tubes in the sky – are the losers. But do customers really matter when a share price is up five times in four years?

But the focus on goosing earnings – and not investing for the future, laying the groundwork for growth, or preparing for hard times – hit airlines where it hurt with the Covid-19 pandemic. Demand for air travel plummeted by over 90%. And because airlines had spent everything on their own shares, they didn’t have the cash to sustain themselves. And so – of course – they asked for help from Uncle Sam, who obliged with $54 billion in taxpayer funds, through a combination of grants and loans.

Shareholders and executives enjoyed all of the short-term upside from making an all-in bet on boosting the share price, while taxpayers took on the downside exposure: it’s corporate socialism at its finest.

But even $54 billion wasn’t enough to plug the gaping holes in airlines’ balance sheets. To reduce their cash burn, airlines used bailout money to induce employees to retire. In June 2020, Southwest offered what it called “the most generous buyout package in our history.” American Airlines provided a similarly cushy buyout package with up to nine months of pay and two years of health insurance. United workers who took a voluntary exit received up to $45,000 in health benefits per person.

While the government was funding early retirements for airline workers, it was also paying workers to not work, through various schemes like “paycheck protection” loans. This artificially reduced the available labor supply, setting the stage for what came next…

Inflation Crushes Airline Profits, Despite Booming Demand

The first COVID-19 vaccines were introduced in late 2020. Relaxed travel restrictions, combined with more fiscal and monetary stimulus, supported a gradual air travel recovery through 2021. By the summer of this year, demand had nearly fully recovered to pre-COVID levels. And then – wait for it – airlines didn’t have enough employees to meet rebounding demand.

At its trough, the total U.S. airline workforce was 12% less than pre-COVID levels. And that’s how 2022 has turned into the year of Airport Hell. Airplanes can’t take off without pilots or flight attendants, and planes can’t get serviced without ground crews.

Desperate airlines paid up to land staff – with United, for instance, offering a 5% raise to all of its 13,000 pilots, as well as a $10,000 signing bonus for many lesser roles like baggage handlers and ramp agents.

Meanwhile, thanks to the ongoing energy crisis, fuel costs rose sharply. Jet fuel costs more than doubled crude oil’s gains earlier this year.

That’s why airlines have lost money over the past couple of years, despite surging demand. The top four U.S. carriers posted a combined loss of $1.4 billion over the last twelve months. (Notably, the last time oil traded near current prices, in 2014, the top four airlines posted $5.8 billion in profits.)

And the already-bloated balance sheets of the airlines have only expanded. The top four airlines now have a combined $70 billion in net debt – up from $60 billion in 2019. The big dollar question then becomes… How will the airlines service this debt?

After all, if they can’t make money during an economic recovery with booming demand, what will happen during a recession? And worse… what happens when they need to refinance their mountain of debt, with interest rates at the highest levels in decades?

Don’t be surprised if airlines genuflect before Uncle Sam again to beg for another bailout, once the economy turns down in the months ahead. And also, don’t be surprised if the U.S. government – again – coughs up the cash (courtesy of you, dear taxpayer).

But if history is any guide, policymakers should instead stand by, and let the invisible hand have its way.

It’s Not Just Airlines

The problems facing the airline industry are a microcosm of the broader economy – which all trace back to the distorted price signals created by rampant government interference in the free market.

Consider an alternative world featuring clear-eyed capitalism and real price discovery. In this universe, the airlines that recklessly leveraged up their balance sheets pre-pandemic would have gone bust. And investors who supported that capital allocation strategy would have gone down with them.

In this scenario, better-run and financially stronger airlines would have absorbed the weaker players in bankruptcy liquidation, at a fraction of their book value. This would have reduced cost structures across the industry and directed resources into the hands of more responsible companies, placing them in a better position to weather future economic disruptions.

And without Covid support programs that allowed millions of workers to earn more unemployed at home, than if they were actually working, distortions to the labor market wouldn’t exist. Corporate America would have had the workers it needed… and fewer airline flights would have been cut because there were enough coffee servers on the plane.

It’s a lesson as old as time that governments – focused on the next election – choose not to learn: there’s nothing more expensive than “free money” from the government.

The sugar high of cheap money inevitably leads to a crash… if not something far worse.

Stocks Set to Drop by 50% as the Economic Hangover Arrives

Now, with global central banks – led by the Federal Reserve – engaged in the most aggressive monetary tightening campaign in a generation, the artificial economy erected upon the fragile foundation of cheap leverage and free money is collapsing.

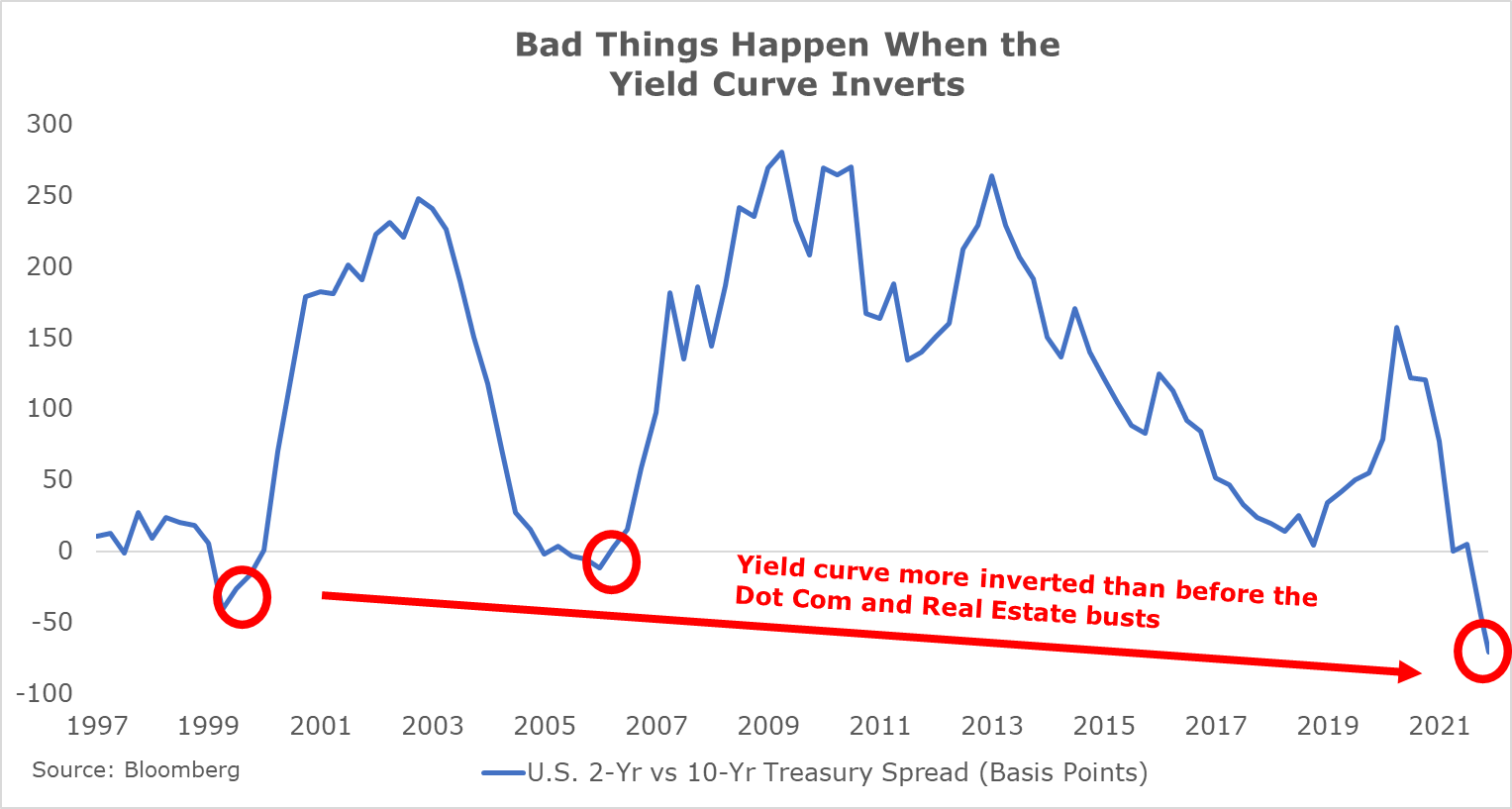

The warning signs are everywhere: the acute labor shortage, spiking inflation, deflating asset prices, and the slowdown in corporate profits… and the inverting yield curve — which is one of the most reliable recession indicators.

The yield curve reflects the relationship between short and long-term interest rates. In a normal economic environment, long-term interest rates should be higher than short-term rates – since lending money for a long time is riskier than lending it for a shorter time.

When long-dated interest rates fall below short-term rates, it’s a five-alarm warning signal for the economy, and the stock market. This “yield curve inversion” is the market’s way of saying that a recession is on the way – because the market is saying much lower rates are coming in the near future.

Expectations for a future collapse in interest rates mean the market is pricing in a sharp economic downturn looming on the horizon. This has happened just before every recession since World War II.

Most recently, it happened in 2000 and 2007, and it’s happening now in a big way — with the sharpest yield curve inversion in 40 years:

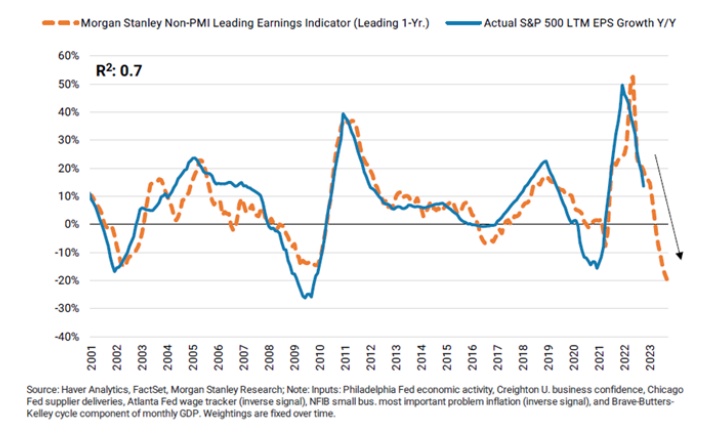

What’s next? A collapse in corporate earnings. That’s what Morgan Stanley’s research team recently called for, with their indicator for estimating forward earnings growth, which points towards a sharp contraction in 2023:

Meanwhile, traders on Wall Street continue bidding the market up in the hope that Fed chair Jerome Powell will deliver the much-anticipated “Fed Pivot” and signal the end of rate hikes

But it’s a hollow wish… because the pivot – which will eventually come – will instead mark only the next chapter of the market’s worries.

That’s because the cause of the Fed’s pivot won’t be good news: interest rates will stop rising only following a massive jump in unemployment, which will push inflation lower – but also crush demand. That said, the thinking is that a recession would be bullish for stocks because it would mean lower interest rates.

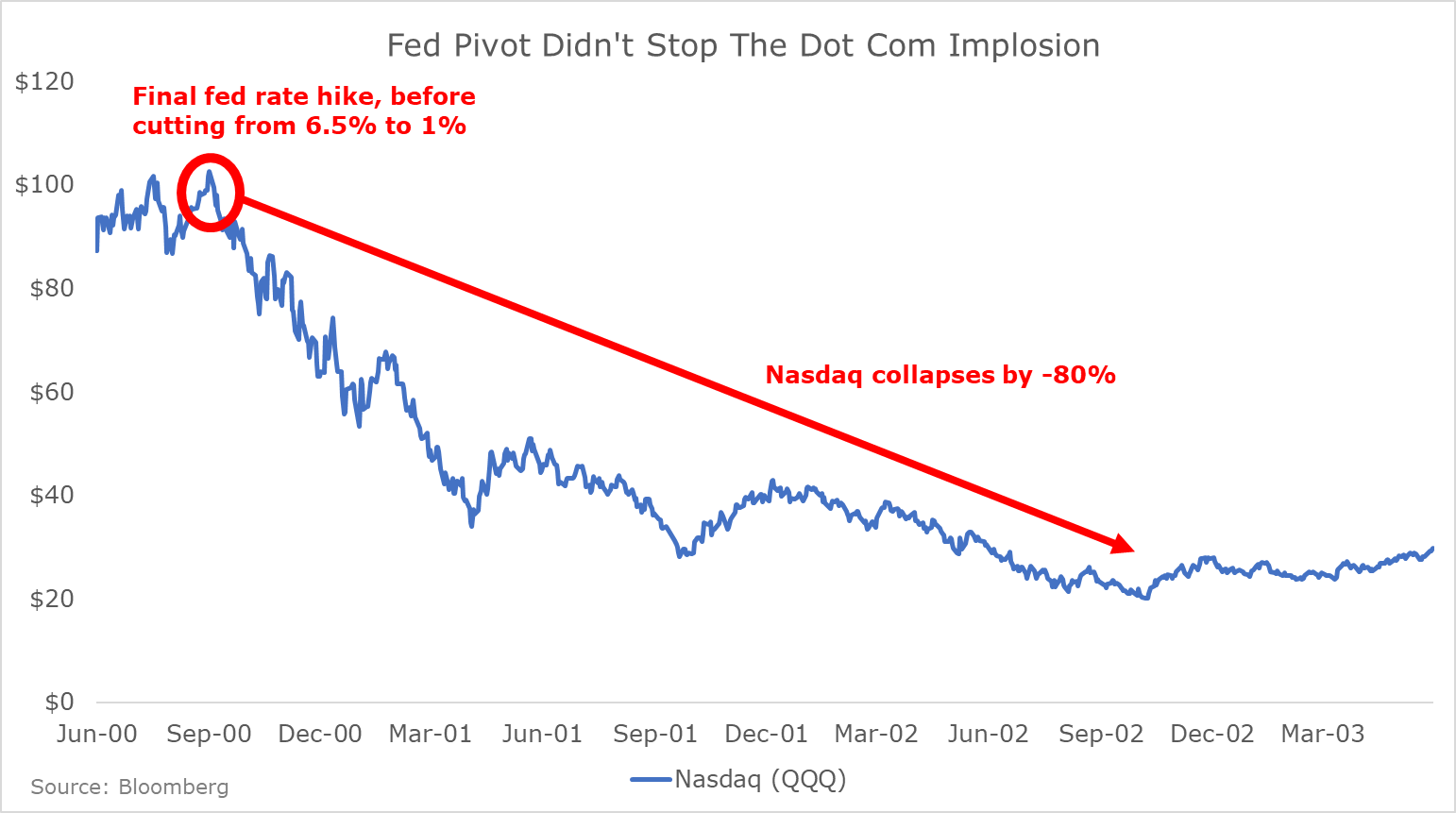

There’s just one problem… history.

This is what happened when the Fed slashed interest rates from 6.5% in mid-2000 to a then-record low of just 1% by early 2003:

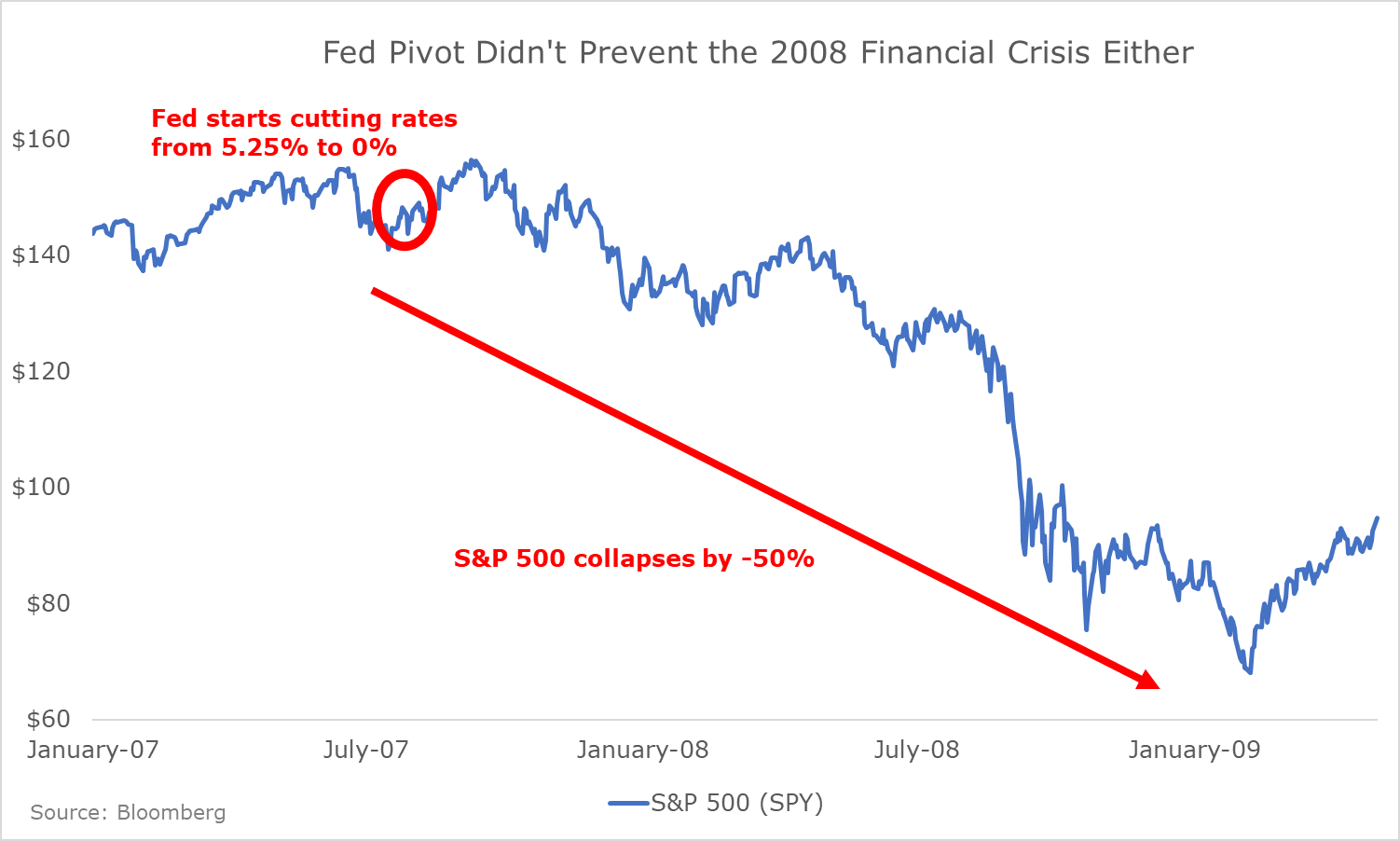

Similarly, the Fed started cutting interest rates in August of 2007… just before the stock market peaked and then entered into a 50% decline.

Now is a time for caution in markets. It makes sense to sell into the recent rally that’s based on pivot hopes. We think there’s as much as 50% or more downside from today’s S&P 500 price of around 4,000.

How? In a typical recession, earnings fall by roughly 20-30%. From the recent high of around $220 in S&P 500 earnings per share (EPS), that implies a drop to roughly $155 – $175 EPS going forward.

Then, pick your earnings multiple for where stocks bottom. The last time the economy faced a recession combined with high inflation was in the early 1980s. Back then, stocks traded for mid-single-digit earnings multiples. But let’s be optimistic and say that stocks trough at 12x earnings in the upcoming recession.

That implies an S&P 500 price target of between 1860 – 2100 at the bottom of today’s bear market.

That’s why we urge patience in today’s market. From the wreckage of the coming bear market, a once-in-a-decade opportunity will emerge to buy world-class merchandise at fire sale prices.

Raise cash and get your shopping list ready, so that you’re prepared to act when the time comes.

In the meantime, you can still find rare opportunities in today’s market.

Here’s How We’re Playing the Next Phase of the Energy Crisis

We’ve been writing about this story since June. Just recently, much of what we’ve predicted is beginning to happen. The energy crisis in Europe is spreading to America.

It will strike New England first. And the cat’s out of the bag: on October 27, the CEO of New England’s largest energy company sent a desperate letter to the White House.

“This represents a serious public health and safety threat,” Eversource CEO Joe Nolan wrote in a letter to President Joe Biden. He then begged Biden to use the federal government’s emergency powers to make sure natural gas will be available in New England this winter.

There’s only one problem. There’s nothing Biden or anyone can do at this point. All available natural gas is on its way to Europe.

Worse still, New England is where the energy crisis in America will start. Yesterday, a United States regulatory agency warned:

A QUARTER OF AMERICANS ARE AT RISK OF WINTER POWER BLACKOUTS AND GRID EMERGENCIES

Now hold onto your hat, because here’s the shocking part: according to our research, there are people in power that actually planned this crisis.

That’s why we created this video presentation that tells the whole sordid tale. Do yourself a favor. Check out this shocking video.

Porter reveals, by name, who caused this crisis, and why. And most importantly, who stands to get rich from it…

Also in the video, about halfway through, Porter lets you in on a way you could make 10-50x returns on an American energy company that’s set to go up like a moonshot if the lights go out in Boston this winter…

You’re not going to want to miss this: CLICK THE PICTURE TO WATCH: