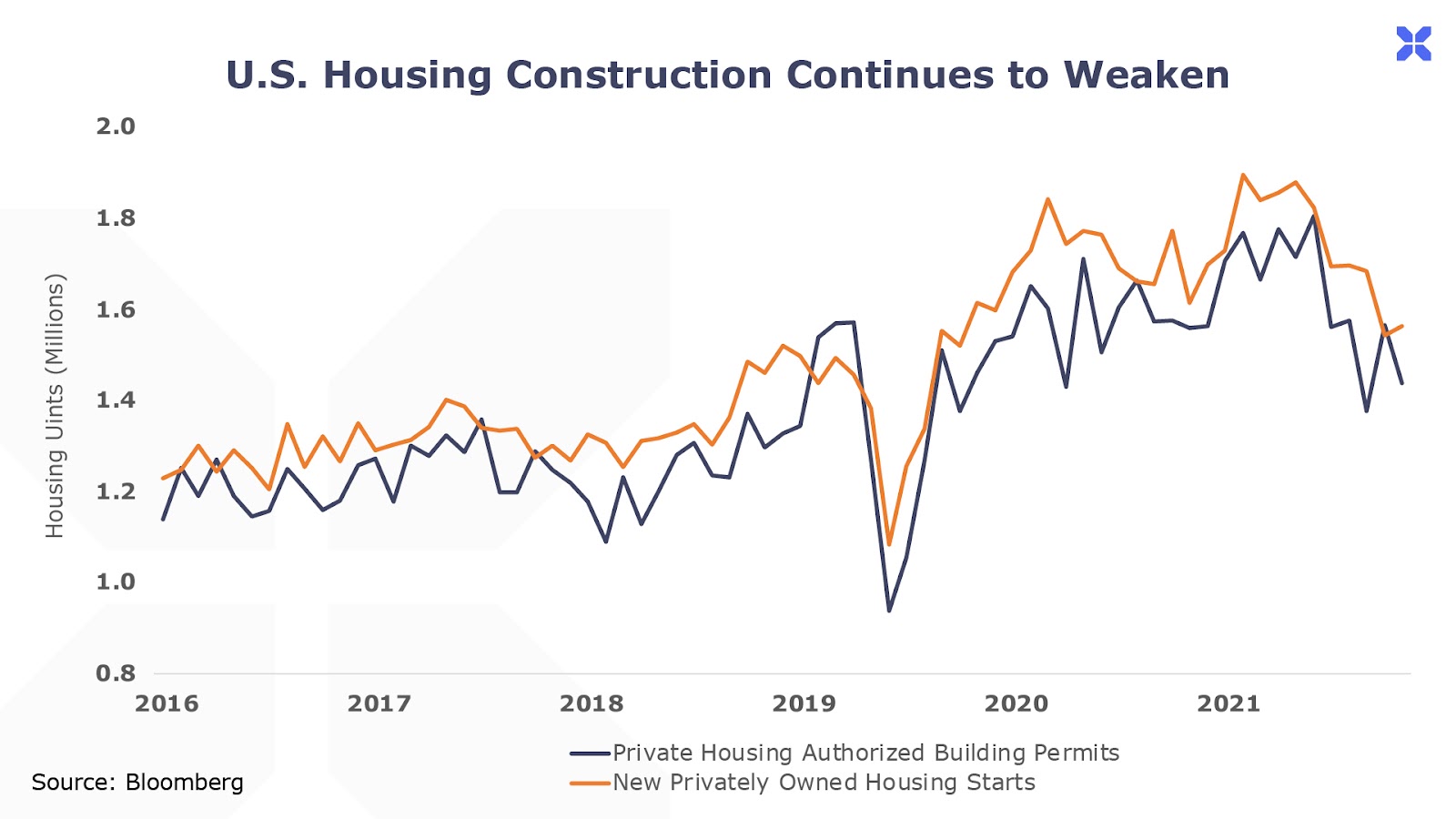

Homebuilders have reported fewer new construction starts every month since March. That’s the longest stretch of declines since the housing crisis of 2007. And homebuyers have even begun walking away from their deposits – cancellations are above 15% for the second consecutive month.

Porter & Co. is looking for a “maniacal” distressed debt analyst… see the end of this email for details…

—

Most people know that San Francisco was destroyed by an earthquake.

It was 5 in the morning, local time, on April 18, 1906. Within just 42 seconds, a 20-foot-wide crevasse formed along a fault-line that was nearly 300 miles long. The quake unleashed the equivalent of about 1,000 nuclear bombs of energy. More than 3,000 people died as structures collapsed – the largest number of civilians killed in a single incident in America until the September 11th terrorist attacks.

But it wasn’t the earthquake that destroyed San Francisco, as most people think. It was the fires that followed.

The danger of earthquakes was well known, so residents were denied earthquake insurance. But most people who lived in the city did have fire insurance.

Their solution? Set the remnants of their homes on fire – to collect the insurance. But because of the earthquake, the city’s water mains were broken. So there wasn’t any easy way to put out the fires. And as a result, it wasn’t long before all of San Francisco was on fire. The army garrison tried to snuff out the flames with dynamite and artillery shells. That didn’t work… and it caused a lot more damage. In total, more than 500 city blocks burned to the ground.

At the time, the world economy was – for the first time – truly global. Steamships and undersea telecommunications linked the world’s financial and commodities markets. And the damage to San Francisco would be felt across the global economy.

Slowly, claims were filed and processed for insured losses in San Francisco. By the fall of 1907, gold bullion was being shipped from every major financial center around the world to pay claims and rebuild San Francisco. The total bill for insured losses rose to $400 million, or about 1.6% of U.S. GDP in 1906 (equivalent to roughly $480 billion dollars today).

As capital was drained away from financial centers, interest rates rose sharply…. And kept rising, until there wasn’t any money available to borrow in the financial markets, at virtually any price. As the famous speculator Jesse Livermore reported at the time:

“Finally there came the awful day of reckoning for the bulls and the optimists and the wishful thinkers and those vast hordes that, dreading the pain of small loss at the beginning, were now about to suffer total amputation – without anesthetics. A day I shall never forget, October 24, 1907… No money anywhere, and you can’t liquidate stocks because there is nobody to buy them. The whole Street is broke at this very moment.”

The Dow Jones fell 50% from its previous peak. The panic of 1907, and the crisis it set in motion, led to the bankers’ determination to establish a Federal Reserve system to prevent monetary panics of this kind. That led to all kinds of “innovations” in money and banking – up to and including the current global monetary system.

Today, of course, there’s nothing to prevent central banks from printing more money and extending limitless amounts of credit to prevent problems like the 1907 panic. And, if you think about it, the global pandemic of 2020-2022 was a bit like the San Francisco earthquake – but even larger. It cost the world something like 7-10% of GDP in deficit government spending.

And the bill for that spending is now coming due in the form of much higher inflation… and thus much higher interest rates.

The first industry to feel the impact is housing.

Yelling “Fire” in A Crowded Market…Over And Over Again

Homebuilders have reported fewer new construction starts every month since March. That’s the longest stretch of declines since the housing crisis of 2007. And homebuyers have even begun walking away from their deposits – cancellations are above 15% for the second consecutive month.

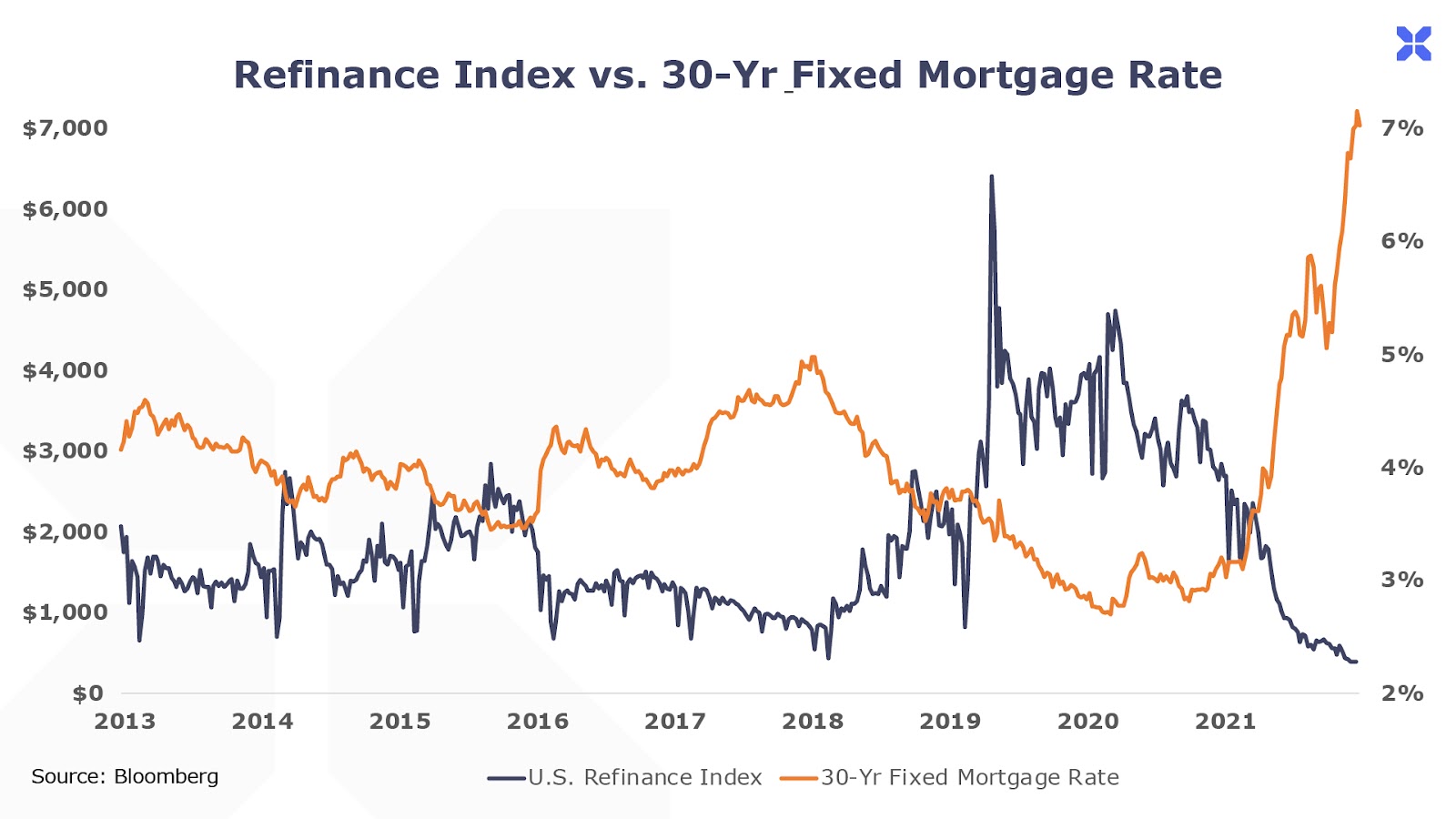

Likewise, mortgage applications have plummeted as rates have soared to over 7%. An index that tracks mortgage refinancing is now down 84%, with re-financing activity dropping to a 22-year low. Likewise, new mortgage applications are down almost 30% from a year ago.

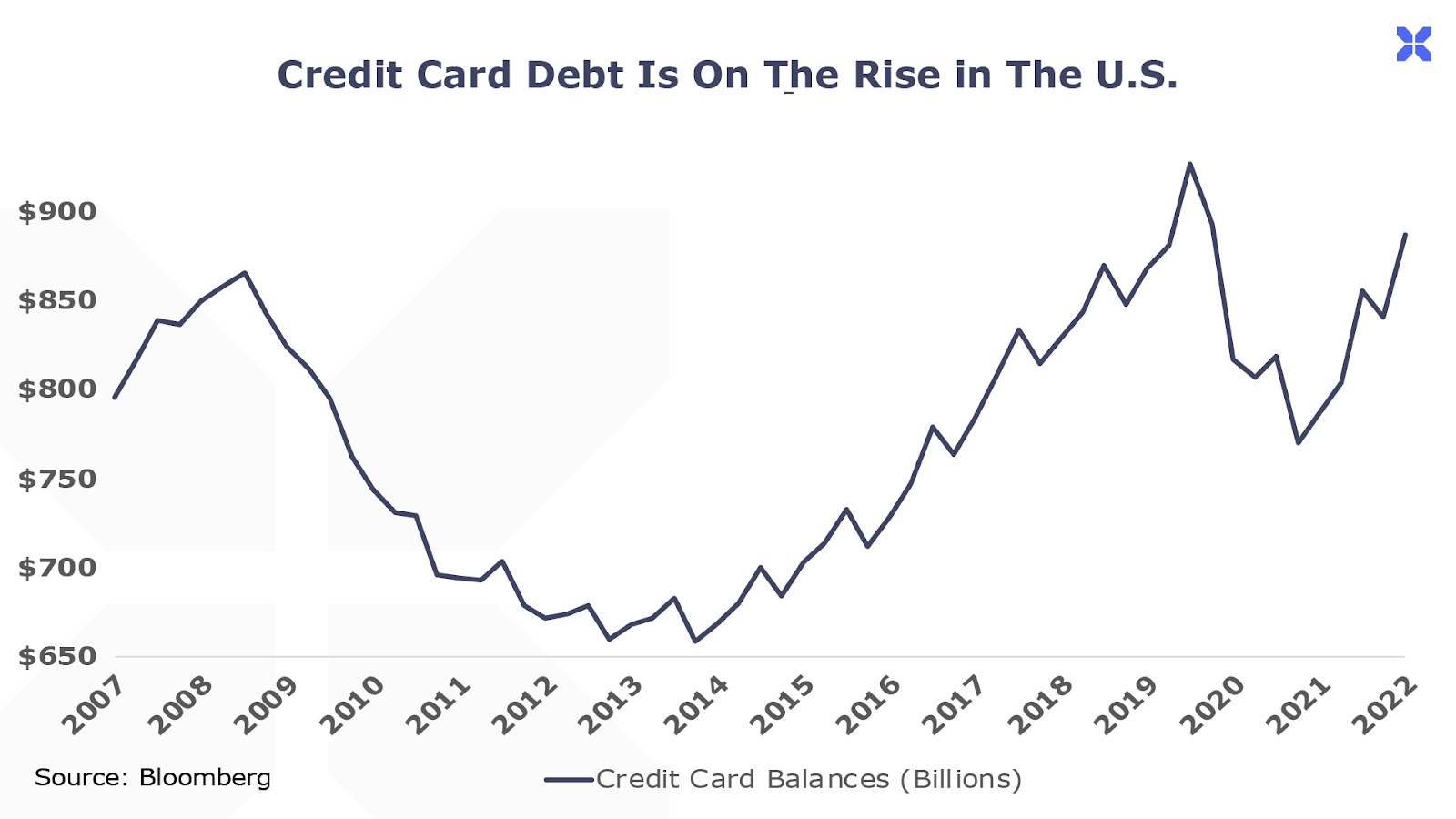

Most people won’t worry too much about housing. It’s “only” 10% of GDP. But…housing punches far above its weight in terms of economic impact. Mortgage refinancing costs directly impact the consumer’s ability to take equity out of their homes for spending.

We are already seeing this, as consumers have been adding to credit card debt at the fastest pace in 20 years.

Of course…credit card-funded spending can’t (and won’t) last for long.

As monetary conditions continue tightening, it’s increasingly likely that we will see a crisis. And not just in housing and consumer spending.

According to Wells Fargo, corporate debt held by non-financial companies is at an all-time high of nearly $12 trillion. And virtually all of this debt will have to be refinanced, sooner or later, at much, much higher rates of interest. Just through 2026, 43% of this debt will come due.

You can think about this “maturity wall” this way…

This year, over $600 billion comes due. Next year, over $800 billion comes due. In 2024 and in 2025 over $1 trillion comes due. That’s tantamount to a San Francisco earthquake every year, for the next five years.

And that’s not including the changes happening to the sovereign debt markets, where around the world central banks are reversing years of “quantitative easing.”

Don’t count on the cost of capital falling back below 10% for most companies. It won’t.

That means equity valuations and stock prices will continue falling on average. And it also means that the risk of a synchronized, global financial panic continues to grow. The “Minsky Moment” we’ve been warning about hasn’t arrived yet. And when it does, we think the 1907 panic will look like a picnic.

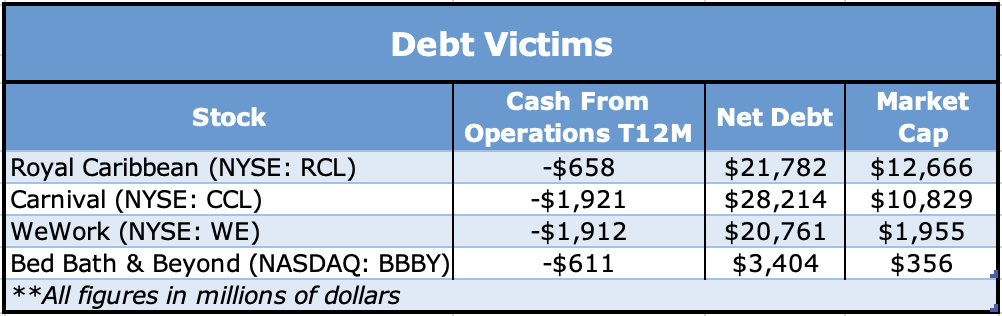

P.S. One of the secondary effects of much tighter monetary conditions will be soaring losses as corporations default on debt. Just as an example, below are four companies that owe more than a combined $30 billion… but currently are losing hundreds of millions every year from operations. It’s hard to imagine any future scenario where these equity investors survive with any value at all. And the bondholders will likely take severe losses too.

Maniac Wanted

(Distressed debt maniac, that is)

Distressed debt is a madman’s paradise.

You’re dealing with endlessly long and complex documents, byzantine capital structures, and hopelessly mismanaged corporations – all before lunch. Plus, you’ll know a bond dealer is lying because his mouth is open. So, why bother? Because no other segment of the financial markets can be so consistently profitable.

As debt maniacs know, there is no such thing as a bad bond – only a bad price.

Porter & Co. – a new, boutique financial research shop led by Porter Stansberry (founder of MarketWise) – is searching for a bona fide debt maniac. We need someone who knows all the ins and outs of distressed debt securities, and has followed that market for at least 20 years.

We are going to build the best distressed debt research team in history to take on what will be the most lucrative restructuring environment, ever. Almost $5 trillion in corporate debt will have to be refinanced through 2026. We think more than $1 trillion will end up distressed.

The team you’ll build for us will help allocate capital for our clients – the world’s leading hedge funds, high-net-worth investors, and major family offices. As our work is profitable and highly scalable, we have substantial budgets for salaries and bonuses. And as this field is extremely competitive, we take pride in paying for performance. If you like working with the best, you’ll like working with us. And if you like winning, you’ll love it.

We care little about academic or professional pedigree. We – and our clients – crave raw intelligence, dry wit, and earned confidence.

Porter & Co. is proudly unwoke. We are a bunch of God-damned incorrigible geniuses – there ain’t no HR department. Snowflakes need not apply. We don’t care what color your skin is. We don’t care whether you stand up or sit down to pee. And we don’t care what you do in your own bedroom. But if you can’t take a joke or if you can’t get along with other, brilliant and sometimes difficult people, you can’t work here.

We are all ultra-competitive: D1 college athletes, B-league intramural champs, ex-Wall Streeters, elite graduates from Ivy-league colleges and former leading subprime mortgage dealers (no one is perfect).

What we do care about is your work product. We only want to publish the best in the field. Can you find remarkable, asymmetric risk opportunities? Can you write cogently and with style? Can you educate and delight our subscribers? Our audience is very rich and very smart. You have to make them smarter and richer.

We find our work addictive and fun. How about you? If, as Buffett likes to say, you’re not “tap-dancing” to work in your current environment, please reach out to schedule an interview.

We’re headquartered in an upscale office space in a converted hayloft on a historic farm in Baltimore County, Maryland. We also have full-time employees on three different continents. For the right candidate, we’ll make the necessary remote work and compensation arrangements, but we’d encourage you to at least start your career with us at the farm. It’s like coming to summer camp every day… for billionaires.

If you’re reading this, you’ve proven one qualification already: Familiarity with and appreciation for what we do. We’re looking for a teammate that shares our view of the financial markets and our view of how the world really works. We’re hoping to find someone who wants to work with us to build something special.

If you’d like to join the Porter & Co. band as our distressed debt analyst, or know any good candidates, drop us a line at [email protected].