Current Fed Chairman Jerome Powell wants to put an end to inflation. Unfortunately – for Powell, for markets, and for investors – it appears increasingly unlikely that he’ll get his wish.

Source: junkyardlife.com

The Federal Reserve Has No Way Out

If you’re new here:

Welcome! You’re reading “Something You Don’t Know,” Porter’s complimentary e-letter. It reveals a hidden market story, or dissects a largely misunderstood element of investing, every other Friday, at no charge. You can see our archive of earlier issues at this link.

“I swear I could see my breath when I got up.”

It’s been more than 40 years now, but Blaise Jones remembers it like it was yesterday.

Twice each week, the then-teenage Jones would drag himself out of bed at 4:30 a.m. to fill up the gas tank of his family’s station wagon. Going that early didn’t take the sting out of surging fuel costs, which averaged nearly $4 per gallon in today’s dollars at their peak. But it did allow him to beat the long lines that would inevitably grow at the pumps as the day wore on.

The colder months were the worst. During the winter, Jones’ father routinely turned their home’s thermostat down to near 60 degrees at night in a futile attempt to control their heating costs.

Around the same time, 20-something Tom Noonan worked at a grocery store. His job was to walk through the store with a box cutter and a pricing gun – often multiple times a week – to swap out price tags to keep up with ever-rising costs.

And Mary Hodder was just five years old.

But she’ll never forget the day her weekly allowance of five cents would no longer buy her favorite candy bar… its new price was an exorbitant 10 cents.

Stories like these are probably all too familiar to many folks who lived through the “Great Inflation” of the late 1970s.

(We recently wrote about the backstory here.)

Lengthy gasoline lines and soaring food prices are as quintessentially ‘70s as VW Bugs and leisure suits.

But the roots of that inflation trace back to the previous decade. The potent combination of aggressive fiscal expansion (to support President Lyndon B. Johnson’s “Great Society” program), and the easy-money policies of then-Federal Reserve Chair Bill Martin, set the stage for the dramatic consumer price increases.

The next Fed chair in line, Arthur Burns, tried to fix the problem in the early ‘70s by hiking interest rates aggressively. That helped cool inflation from a peak above 12% in 1974 to nearly 5% in 1977.

But Burns declared victory too soon. He started cutting rates even before inflation peaked in 1974, continued through 1977, and inflation ultimately came roaring back to highs near 15%.

It wasn’t until Fed Chair Paul Volcker took the reins in 1979, and hiked rates to nearly 20% – thereby pushing the economy into not one, but two devastating recessions – that the inflationary inferno was finally doused.

Volcker is remembered as a hero today – a confident leader who took on inflation and won. But the haze of history obscures the reality that at the time, Volcker’s victory over inflation was far from certain.

After over a decade of persistent price increases in excess of 7% a year on average – enough to more than double consumer prices across the board – even supposed experts were beginning to doubt that the problem could be solved.

In fact, as late as January 1980 – less than two months before the ultimate peak in inflation at 14.6% – White House inflation adviser Alfred Kahn publicly warned that “in the months ahead, I don’t think anyone can honestly expect an improvement.”

The “experts” feel differently about inflation today.

According to the government’s official metrics, prices have been rising above the Fed’s 2% target for nearly two years now. And inflation has clocked in above 6% – the highest rate since the end of the Great Inflation – for well over a year.

Despite this fact, many pundits still believe inflation to be “transitory,” a relic of COVID-19-related supply-chain disruptions that will naturally abate over time.

More worryingly, even those who are concerned about rising prices generally believe that the Fed can wave a magic “tightening” wand, and stop inflation in its tracks.

Fed Chair Jerome Powell certainly believes that’s possible…

According to Washington insiders, Powell has privately (and repeatedly) told his Fed colleagues that he “will not become ‘just another Arthur Burns.’” And his public comments, as recently as this week, suggest he remains committed to aggressively tightening monetary policy to fight inflation.

In testimony to Congress on Tuesday, Powell noted that recent data indicate inflationary pressures remain “stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.”

In other words, he isn’t done fighting yet.

Like Volcker, he wants to be remembered fondly for killing inflation, once and for all.

Unfortunately – for Powell, for markets, and for investors – it appears increasingly unlikely that he’ll get his wish.

Cold Pricklies, Not Warm Fuzzies

Bell bottoms, the AMC Gremlin, and disco have – thankfully – (mostly) remained relics of the ‘70s. But inflation hasn’t.

And unfortunately, in a number of ways today’s macro environment is far less friendly – and will be less amenable to inflation-fighting – than it was in the era of pet rocks… when higher rates were a (slow-acting but still lethal) silver bullet.

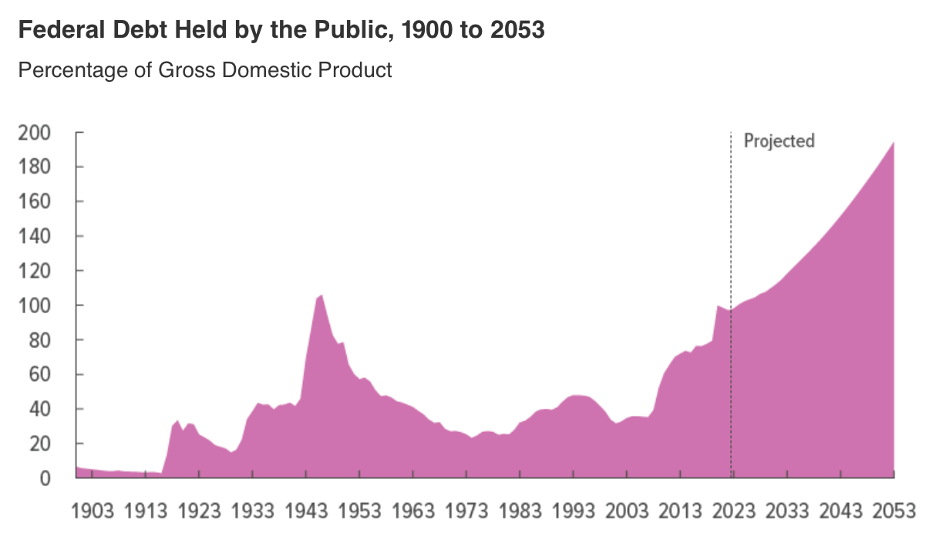

First, the U.S. government’s fiscal health is worse.

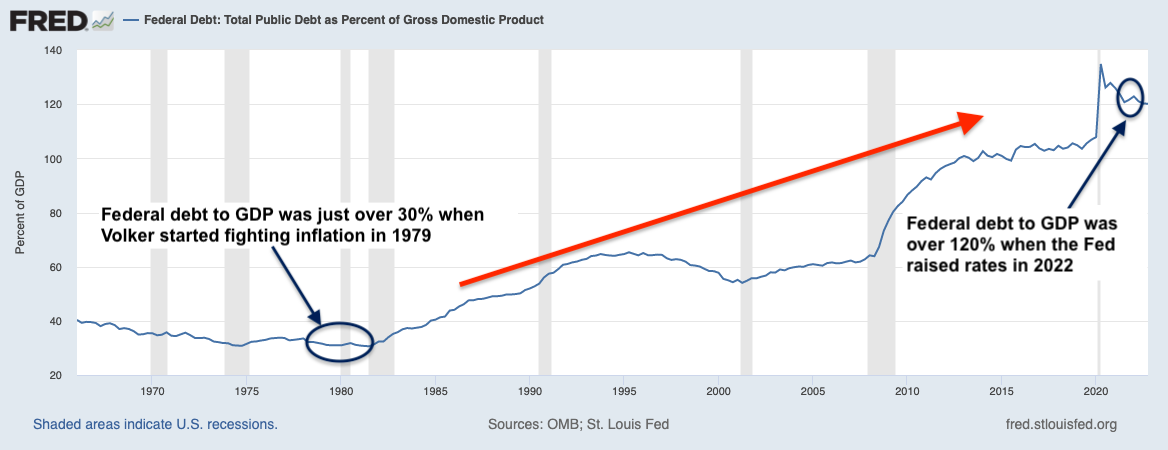

When Volcker started his all-out war against inflation in 1979, federal debt was equivalent to just over 30% of gross domestic product (GDP).

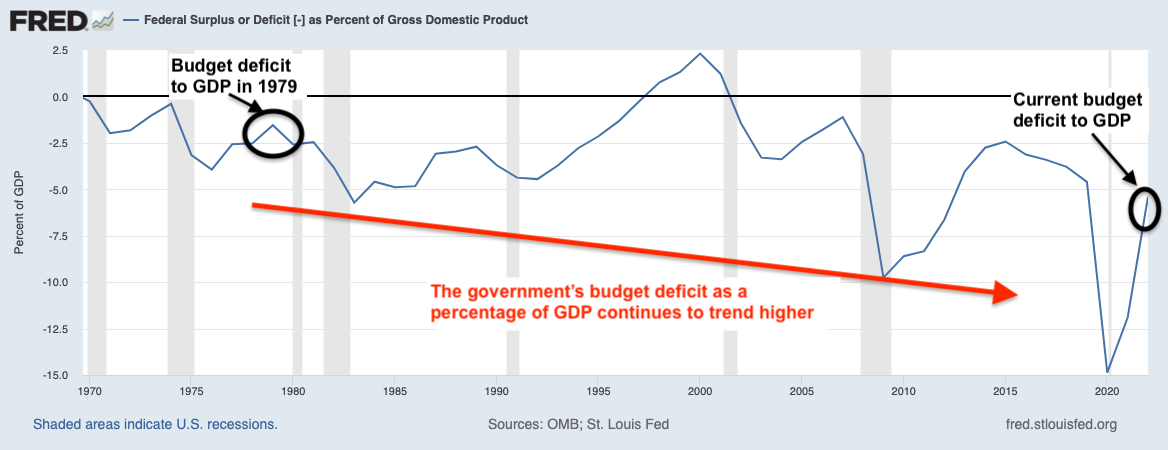

Meanwhile, the government’s budget deficit – that is, how much money the government spends in excess of what it brings in through taxes – was under 2% of GDP at the time.

This combination of relatively low debt and deficits allowed the Fed to raise rates aggressively – to nearly 20% at their peak – with only a moderate increase in the government’s interest burden.

By the time Volcker declared victory in the fight against inflation in 1983, rising interest expense had increased the government’s annual deficit by around four percentage points to roughly 6% of GDP.

The situation is starkly different this time. Like the characters in the hippie children’s book, we find ourselves with far fewer “warm fuzzies” to go around.

Debt and Deficits Are Out of Control

Today, U.S. government debt-to-GDP sits near 120%, while the current deficit is over 5% of GDP – more than double what it was when Volcker started his fight.

This combination means even modest interest rate increases can cause the government’s interest expense to soar.

For example, if the Fed were to raise rates another 1.25 percentage points to 6% – only slightly higher than the market’s current estimate of the “terminal rate” for this cycle – the government’s interest expense would ultimately rise more than threefold to roughly $2 trillion per year. That’s more than the federal government spent on Social Security and Medicare combined last year… more than double its entire defense budget… and more than three times what it spent on education.

That figure also equates to nearly half of this year’s projected federal tax receipts – and 8% of GDP – in interest expense alone.

And yet… raising rates to 6% would still represent only about half of the cumulative rate hikes Volcker needed to halt inflation between 1979 and 1981.

If you do this same math with higher terminal rates of 8%, 9%, 10%, or more, the numbers quickly become untenable. Soaring interest costs would grow to consume all of the money the government brings in through taxes, even well below peak Volcker-era rates.

In simple terms, the government’s massive debt burden limits how high the Fed can actually raise rates to fight inflation.

But this isn’t the only meaningful difference between the 1970s inflation scenario and today.

The second difference is the nature of the inflation itself.

Not All Inflation is the Same

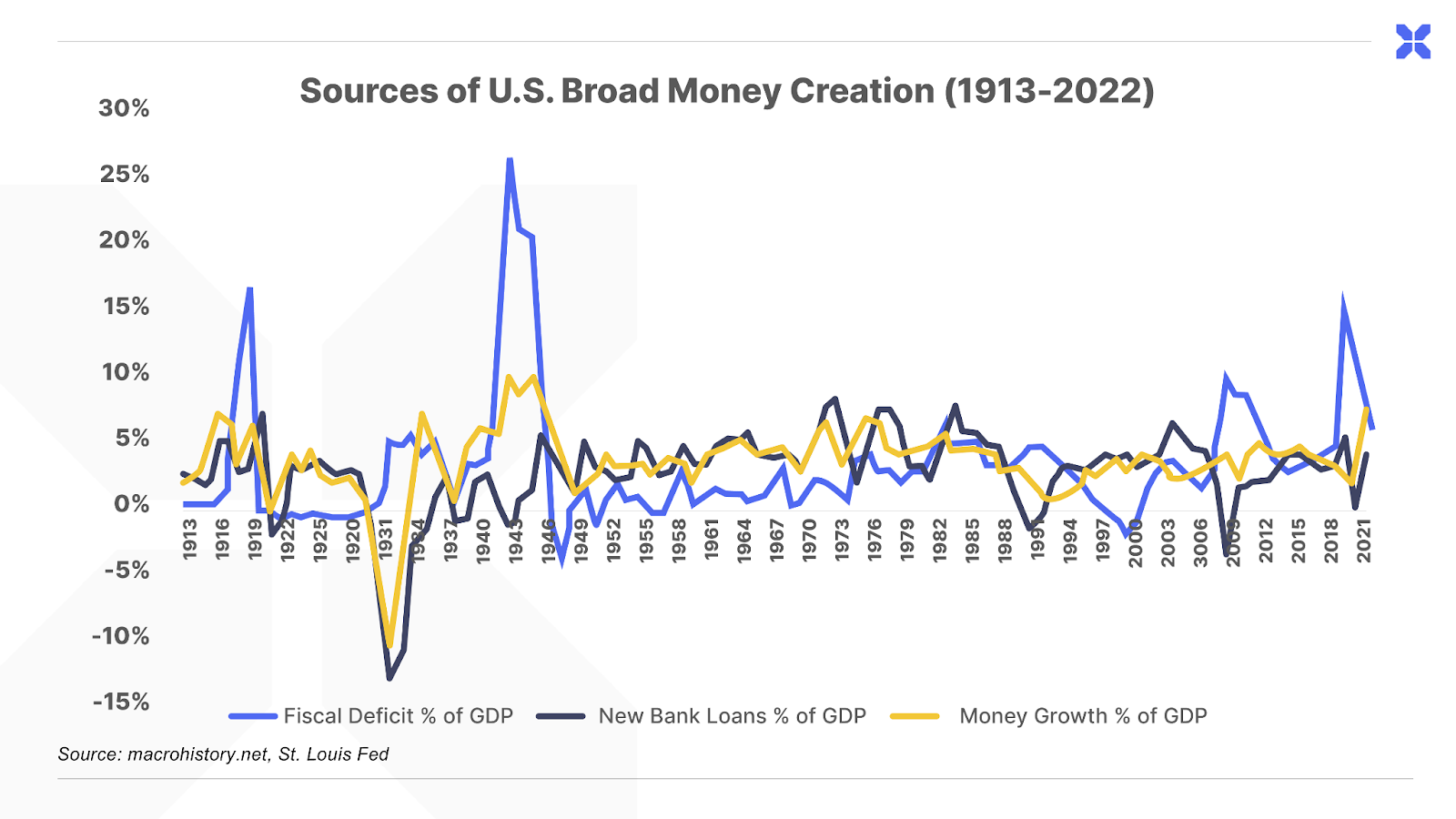

We talk about inflation as higher prices… you pay more for milk, gas, rent, and pretty much everything else. But most of what we measure as “price inflation” results from an increased supply of money in the economy… that is, a greater number of currency units, whether that’s real paper dollars or (more commonly today) simply digital entries on computer spreadsheets.

And there are two primary ways the money supply can grow: through new bank lending, or rising fiscal deficits – a.k.a. government money-printing.

Rising fiscal deficits certainly played a role in the 1970s inflation. But increased bank lending was arguably an even more significant driver. Total bank loans and leases grew at an 11% annualized rate between 1970 and 1980.

That isn’t the case today.

The recent increase in the money supply was almost entirely the result of massive COVID-related fiscal deficits.

We’re referring to the roughly $4 trillion in Fed easing and roughly $5 trillion in “stimmy” and business “loans” (that didn’t have to be paid back) to keep people buying stuff while they were locked up.

Rapidly shifting consumer trends (moving out of cities, working from home, etc.) and supply-chain disruptions added fuel to the inflationary fire.

Unfortunately, no matter how high the Fed raises interest rates, this situation isn’t going to improve.

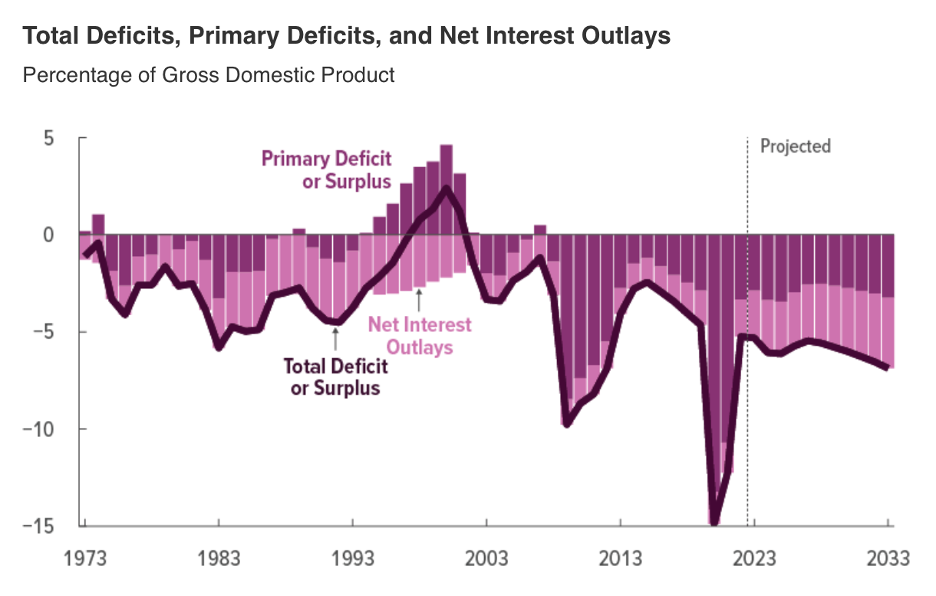

The latest report from the Congressional Budget Office (CBO) projects U.S. fiscal deficits are likely to rise significantly in the years ahead, as money the government has already earmarked for Social Security, Medicare, and other programs grows to a larger and larger percentage of the total budget. Specifically, the CBO expects deficits to grow from around $1.5 trillion (5% of GDP) this year to nearly $3 trillion (8% of GDP) by 2033.

These deficits would add another $20 trillion-plus to our current $31 trillion of debt, pushing total debt-to-GDP to nearly 150%.

That averages out to more than $150,000 in debt for every man, woman, and child in the U.S. today.

These kinds of projections are often laughably optimistic, and that’s certainly the case here.

For example, this projection inexplicably assumes that inflation will move significantly lower again over the next ten years.

Yet, as we mentioned before, growing deficits are, by definition, inflationary. And that’s particularly true when existing debt burdens are high, like they are today.

In this environment, rising deficits lead to significant increases in interest expense (especially if interest rates are also rising sharply), which then require even larger deficits to finance, creating a vicious feedback loop.

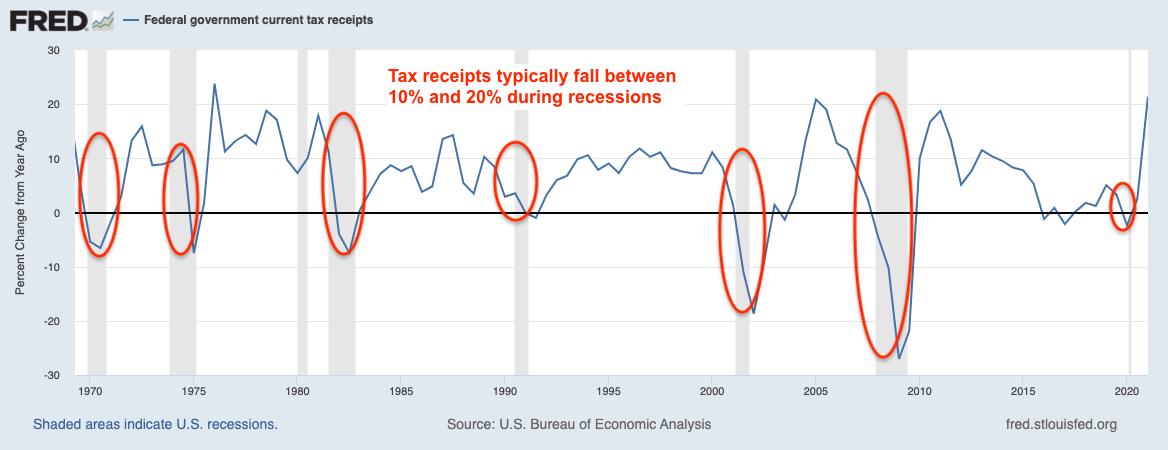

The CBO projections also assume that the economy will avoid falling into a recession at any point over the next ten years. Our experience during the Great Inflation – which included no less than four separate recessions between 1970 and 1982 – suggests this is unlikely.

If the economy should also fall into a recession, the resulting drop in government tax receipts (due to some combination of rising unemployment and falling asset prices) would only compound this problem further.

For perspective, tax receipts have typically fallen between 10% and 20% during recessions. A similar decline today would represent a shortfall of up to $900 billion. That would require a near doubling of the federal deficit – to more than 9% of GDP – just to maintain the same level of spending.

But this forecast likely just scratches the surface of the problem. Inflation could get much, much worse in the years ahead…

Three Big Reasons Inflation is Here to Stay

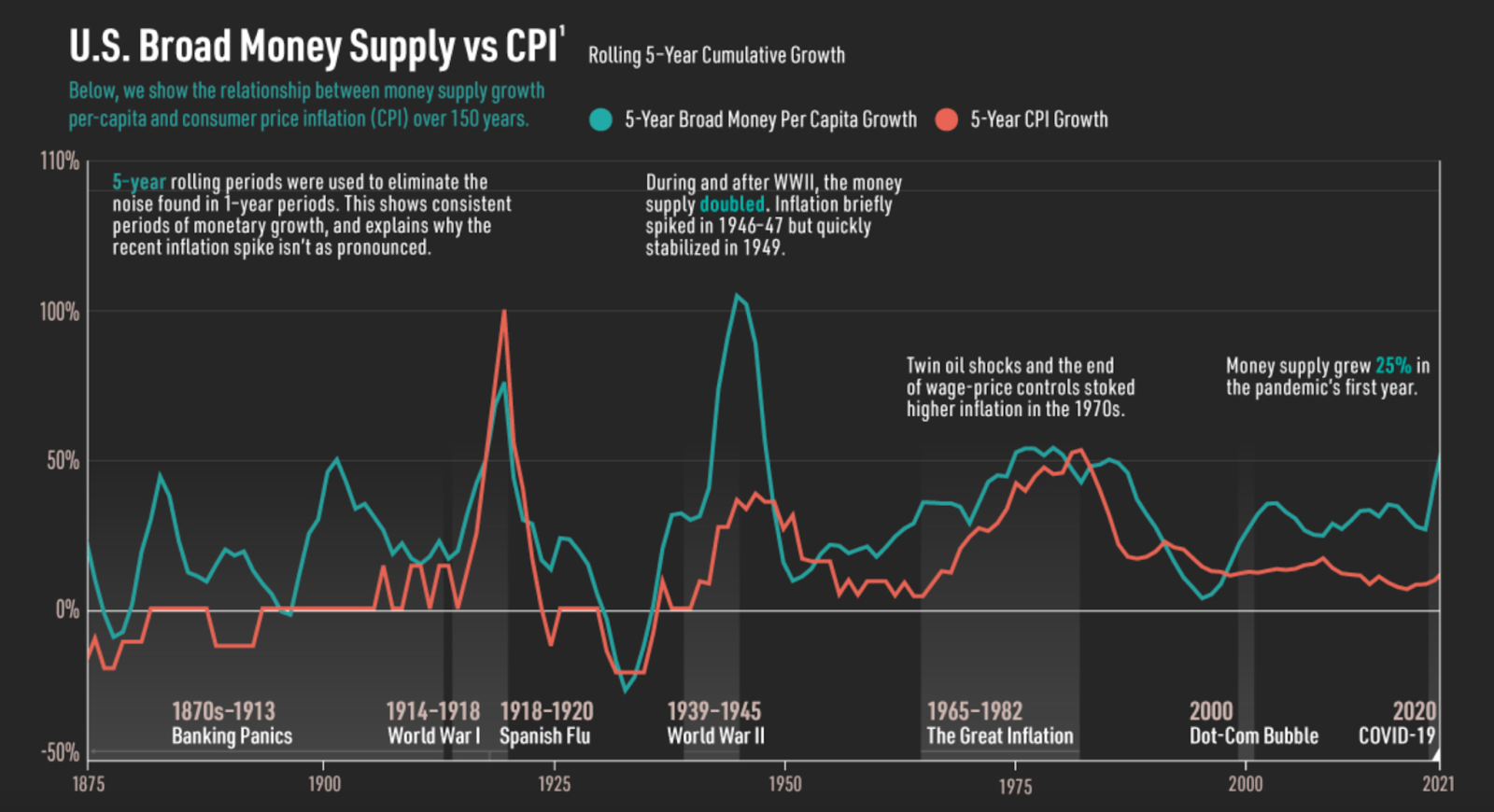

Earlier, we mentioned that inflation is primarily a result of increases in the broad money supply. And that relationship has held relatively steady for at least the last 150 years.

Whenever the money supply has gone up, consumer prices have generally followed. However, there were two notable periods when this wasn’t the case.

The first exception occurred during the late 19th and early 20th centuries. During this period, the money supply moved sharply higher, yet consumer prices remained relatively tame.

That was largely thanks to the Second Industrial Revolution, which brought us modern electrical power, the lightbulb, the telegraph, the telephone, petroleum refining, airplanes, automobiles, the assembly line, and more. These civilization-altering innovations were a powerful deflationary force that helped to offset the rise in the money supply.

The second exception occurred more recently, from around the mid-1990s through roughly the start of the COVID-19 pandemic. Again, money supply moved sharply higher during this time without a significant increase in consumer prices.

In addition to the rise of the Internet, the U.S. also benefited from three powerful trends that acted to hold inflation lower during this time.

- The first was a massive influx of cheap capital. Many of the world’s most productive economies and U.S. trading partners – including OPEC and other energy producers, Japan, China, and European countries – began recycling their trade surpluses and “excess savings” into U.S. Treasury bonds.

- The second was cheap labor. Immigration (primarily from Mexico and other parts of Latin America) and the rise of globalization and offshoring of supply chains (primarily to China) kept massive downward pressure on labor costs for decades.

- And the third related trend was cheap goods (again, primarily from China). A flood of cheap finished and intermediate goods – from steel to electronics to clothing to toys – kept consumer prices low via the “Walmart effect.”

Unfortunately, all three of these trends appear to be reversing now…

Due to rising energy costs, Europe no longer has a trade surplus to recycle into Treasury bonds. Japan is in a similar situation. And following the severe U.S. sanctions on Russia last year, many of our biggest remaining trading partners – including China and OPEC – have essentially stopped buying U.S. Treasury bonds for fear of confiscation.

Likewise, immigration from Latin America and elsewhere has fallen sharply in recent years, leading to a shortage of low-cost labor in the U.S. A falling labor participation rate due to aging demographics and COVID-19 has only worsened this trend.

Finally, most recently, trade wars and the post-COVID trend toward “reshoring” and “friend-shoring” – moving supply chains from China to the U.S. or more friendly jurisdictions – means the flood of cheap goods we’ve become accustomed to is drying up as well.

Over the past few decades, these trends acted as persistent headwinds for consumer prices. So it’s reasonable to expect their reversals to act as stubborn tailwinds for inflation going forward. And unfortunately, there’s very little the Fed can do to change this.

Vincent Deluard – Director of Global Macro at financial services firm Stone X, and one of the first Wall Street analysts to publicly warn about inflation following COVID-19 – likens this situation to a river.

For the past 20-plus years, the “current” was pushing inflation down, so the Fed could simply float along without having to worry about keeping prices under control. (In fact, they often worried that inflation was too low.)

Now, the current is pushing prices higher. Which means the Fed is now essentially “swimming upstream” in its fight against inflation, and has to work that much harder to make any progress at all.

With fiscal deficits likely to rise under even the rosiest conditions, these trends could keep a floor under inflation for the next decade or more.

Barring draconian cuts to entitlement and defense spending (both of which are political “hot potatoes”) or an unexpected productivity miracle, this leaves Powell in a difficult situation…

Between a (Pet) Rock and a Hard Place

If Powell continues to aggressively tighten to fight inflation, a sovereign debt crisis is likely unavoidable. Without central bank support, the U.S. (and other overly-indebted governments) will ultimately default as soaring interest costs overwhelm their ability to pay, causing our credit-based financial system to grind to a halt. (And this doesn’t even include the near-term risks of Congress’ looming debt ceiling showdown.)

Yet, if or when he begins easing again in an attempt to stave off these problems, inflation is likely to surge even higher and trigger a massive decline in the purchasing power of the U.S. dollar.

We don’t know which path Powell will choose. Given his comments, he may attempt to stick to the Volcker “playbook” as long as he can.

But our bet remains, that when real trouble begins, Powell (and other central bankers) will blink.

We believe that, sooner or later, the Fed will have no choice but to step in to support the sovereign debt markets as it always has. And Powell – like Arthur Burns – will stand by as inflation roars back with a vengeance.

This scenario may involve a type of quantitative easing (QE) known as “yield curve control” (YCC). This entails a central bank promising to buy an unlimited amount of bonds to hold interest rates below a maximum threshold.

YCC would essentially place a cap on the government’s interest costs, ensuring that the Treasury can continue to service its debt despite high inflation. Owners of Treasury bonds would still suffer significant losses in purchasing power, but they would technically be paid back in full (in nominal terms).

Allowing inflation to “run hot” like this could allow the government to gradually reduce its real debt burden – bringing debt-to-GDP back down to more reasonable levels over several years – while avoiding the pain of an actual default.

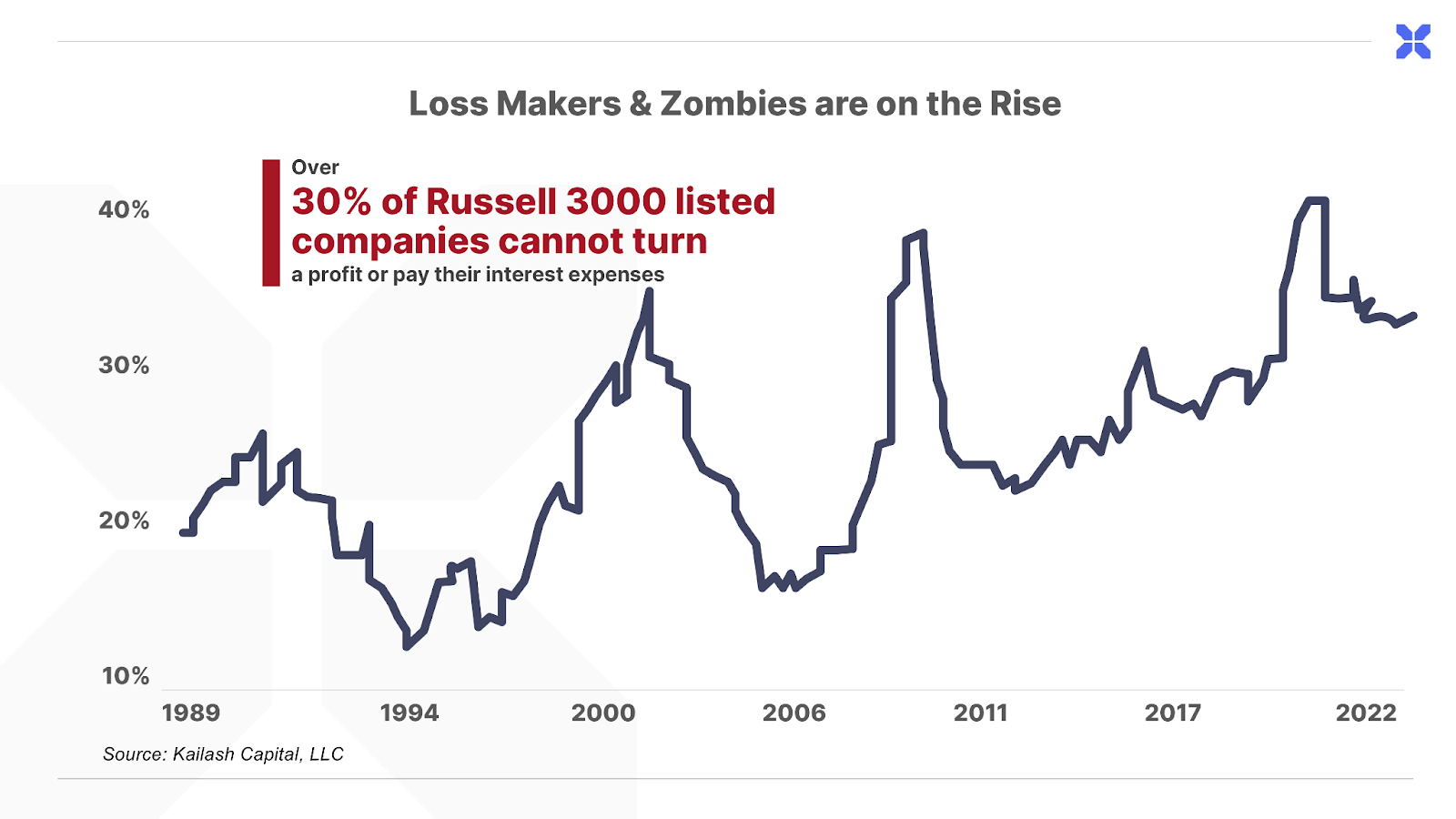

Unfortunately, this solution would be little consolation for the corporate debt markets.

Corporate credit spreads are likely to widen significantly even if the Fed holds Treasury yields steady. That means companies would be required to pay significantly higher rates to borrow money (or refinance) than they have in decades.

Yet, despite near-record profit margins and record-low interest rates on outstanding debt, many companies are already struggling. More than a third of the 3,000 largest publicly listed U.S. companies can’t afford to pay even the interest on their debt today.

More than $6 trillion of this debt comes due over the next three years. And as it does, many of these companies will be in serious trouble – unable to pay off their obligations or to refinance at higher rates.

This could create devastating losses in many corporate bonds… but also open up tremendous opportunities in “unfairly” distressed debt. We’re calling this once-in-a-generation market scenario “the greatest legal transfer of wealth in history.”

Porter & Co.

Stevenson, MD

P.S. If you’d like to learn more about the Porter & Co. team – all of whom are real humans, and many of whom have Twitter accounts – you can get acquainted with us here.