In today’s special edition of Something You Don’t Know, you’ll find an important briefing from credit analyst and author Martin Fridson, who leads Porter & Co.’s Distressed Investing team.

An Urgent Update from Our Distressed Investing Director

Editor’s Note:

Below, you’ll find an important briefing from credit analyst and author Martin Fridson, who leads Porter & Co.’s Distressed Investing team.

Martin is “the most well-known figure in the high yield world,” according to Investment Dealers’ Digest. Over a 25-year span with brokerage firms including Salomon Brothers, Morgan Stanley, and Merrill Lynch, he became known for his innovative work in credit analysis and investment strategy. Now, he’s the director of Porter & Co.’s new Distressed Investing advisory, where we examine the “greatest legal transfer of wealth in history.”

Friends,

In the space of three days, we’ve witnessed the second and third largest bank failures in U.S. history. Both Silicon Valley Bank and Signature Bank were profitable, with investment grade credit ratings as of last Wednesday. Price drops of 63% and 38% last week show that the collapses were huge surprises to the market.

Banks are a special breed of companies. They can seem to be going along fine and then wham!—depositors lose confidence. The bank is hit with massive withdrawals and suddenly it has a liquidity crisis. This is very different from the long, drawn-out deterioration that typically moves industrial companies and retailers into the distressed category.

So far, the most conspicuous spillover effect from the bank failures has appeared in the market for U.S. Treasury bonds…

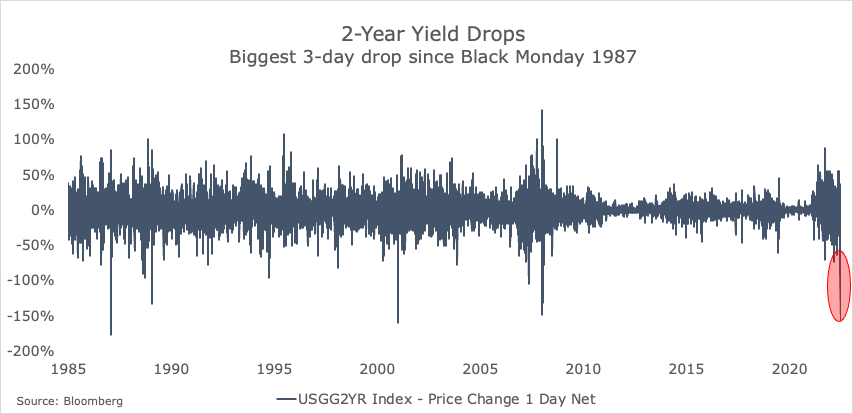

The yield on the two-year Treasury, which had been marching higher all through 2023, plunged from 4.89% to 4.58% on Friday, March 10, a very big one-day move in that market. This is a clear sign that investors are scared and running for safety.

In that kind of panic-fueled environment, it’s natural to expect attractive opportunities to arise in stocks and bonds that fall to distressed prices even if they don’t deserve to.

It’s true at present that certain other regional bank stocks like First Republic, PacWest, and Western Alliance Bancorp have sold way off and could rebound as the fright triggered by the two recent failures subsides. That doesn’t automatically make those stocks bargains, though. They face the same risk as Silicon Valley and Signature did of an unpredictable, out-of-left-field loss of confidence by their depositors.

One effect that could create very short-term opportunities is in the bonds of banks that experience liquidity squeezes, then obtain support from regulators.

For instance, on Friday, Silicon Valley’s 3-1/8% due 6/5/2030 plummeted from 47.87 to 36.74. At 11:00 a.m. on Monday it was quoted at 43.27, up 18%. But going after that kind of very short-term profit is a trade, not an investment.

An Index and an Indicator to Keep An Eye On

If the current turmoil in the banking sector spreads to the broader corporate market, we can expect to see an increase in the number of bonds trading at distressed levels. The standard definition of a distressed bond is one I introduced 30-odd years ago – a yield 10 percentage points or more above the yield on a comparable-maturity Treasury bond.

Last week, the number of distressed issues within the ICE BofA US High Yield Index rose from 146 to 166. That’s still just 9% of the total of 1,931 bonds in the index, which is not a high percentage by historical standards. We’ll be keeping a close watch on that indicator as a possible sign that some corporate issues are inappropriately getting taken to the woodshed.

Good corporate bonds are often unfairly punished in a broad selloff, when mutual fund managers need to raise cash to meet redemptions. They sell better-quality paper because there are still bids for those issues – while dealers avoid bidding on truly troubled credits.

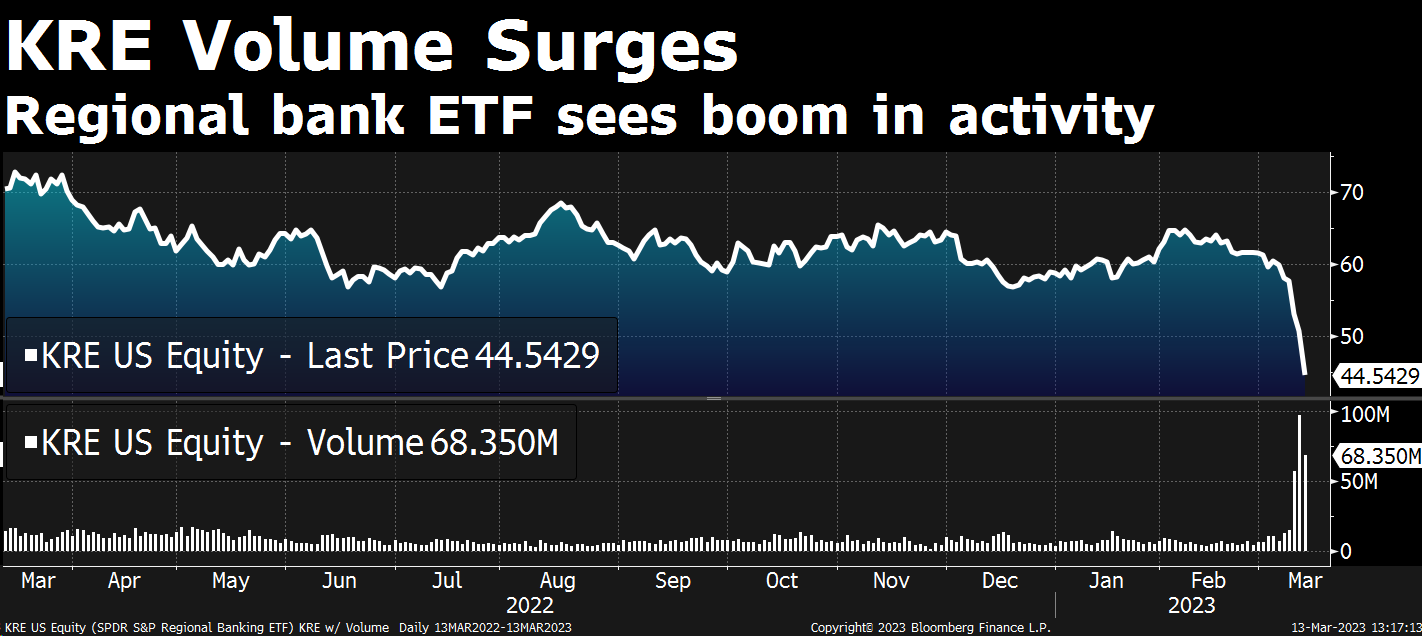

One other indicator worth watching is KRE. That’s the S&P Regional Banking ETF. It’s down 26% from a week ago versus just a 4% decline in the S&P 500. Regional banks are at the center of the current anxieties, so this security should act as a pretty good barometer.

A silver lining in the dark clouds overhanging regional banks is that their fragility may cause the Fed to slow down the pace of its interest rate tightening.

The futures market has already shifted away from viewing a 50-basis-point hike as the Fed’s most likely next move, seeing a 25-basis-point increase as more likely. Stocks would benefit from less severe Fed tightening, although there could be a negative, longer-term impact if the Fed turns out to have eased up on its anti-inflation efforts too early.

The bottom line is that despite the unprecedented speed of the SVB collapse and regulatory takeover, it’s still early days for the resulting market disruption.

Martin Fridson