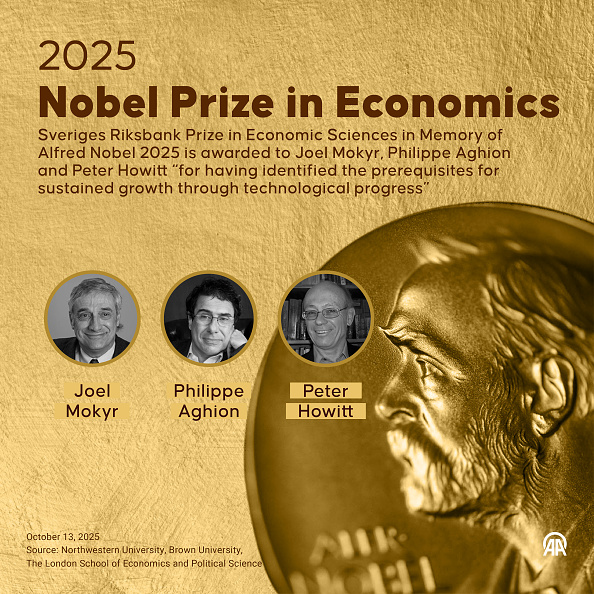

The Nobel Prize Honors Innovation

Today, the Nobel prize was awarded to three economists for their decades of contributions to understanding how technological progress has transformed societies over the past two centuries, lifting billions out of poverty, improving health, and raising the overall standard of living.