Issue #12, Volume #2

Where To Invest During A Lost Decade

This is Porter & Co.’s free e-letter, the Daily Journal. Paid-up members can access their subscriber materials, including our latest recommendations and our “3 Best Buys” for our different portfolios, by going here. Recent issues of the Daily Journal are here.

| What to do when facing a lost decade in equities… Boring companies with some very exciting returns… If we had a crystal ball in 1969… Apple (AAPL) disappoints again… Porter opines on a podcast. |

Imagine you had an investment crystal ball – you could see the market’s future.

In 1969, you watched Warren Buffett shut down his investment partnership. He complained there were no attractive investments given his large (at the time) amount of capital ($100 million). But, because of your crystal ball, you knew he was completely wrong. You knew that the top 50 stocks in the S&P 500 – the so-called “Nifty Fifty” – were going to soar.

Total returns in these stocks during 1970, 1971, and 1972 were astounding. As a group they were up almost 30% annually. By the peak of the market (in 1972) their valuations had become “Tokyo-like” – McDonald’s (MCD) had a price-to-earnings (P/E) ratio of 86; Polaroid’s P/E was 91; and The Walt Disney Company’s (DIS) was 82. (Tokyo-like refers to the incredible Japanese stock mania of the 1980s, when the average P/E ratio on that market reached 70.)

When my children were younger, they’d do foolish things in the house. Like throw a football in the living room. Our family mantra is kindness always, no exceptions. So, rather than simply scold them, I’d ask them calmly: What happens next, boys? And they’d sheepishly answer, “Something is gonna get broken, and we will have to clean it up.” Sometimes they’d go outside with the ball. Sometimes something would get broken, and they had to clean it up.

When you participate in a market mania, I can tell you what happens next. Something will get broken, and you’ll have to clean it up. If you’d bought the Nifty Fifty in 1969, your portfolio was down almost 95% five years later – despite the incredible returns of the early ‘70s..

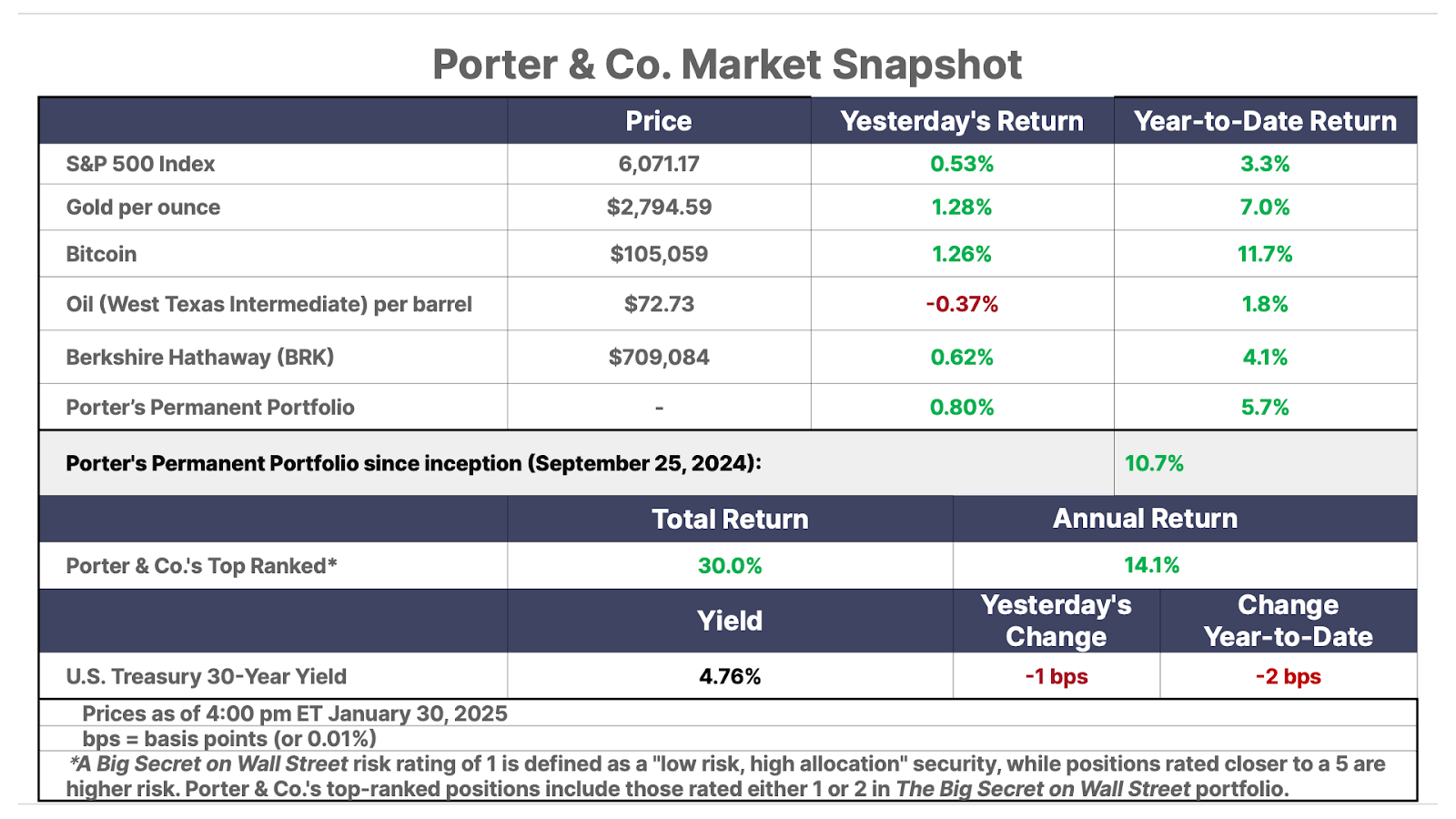

Today, we have the exact same scenario. Buffett has taken his chips off the table. If you look at the most recent Berkshire Hathaway quarterly report (3Q 2024) you can see that in his insurance subsidiaries, Buffett has increased his U.S. Treasury bill holdings (cash) by $150 billion in the last year. He now holds more T-bills than equities ($288 billion versus $271 billion). We know from press reports and other securities filings that he’s continued to sell stocks, and that his cash balances are now well over $300 billion.

But, meanwhile, the Nifty Fifty… whoops… I mean the Magnificent 7 (Amazon, Apple, Google, Meta, Microsoft, Nvidia, and Tesla) have continued to hit new highs. According to GAAP (Generally Accepted Accounting Principles), Tesla now trades at a P/E ratio of 197. We are well beyond Tokyo levels. As a group, the Magnificent 7 has been trading at around 50 times earnings.

These extreme valuations and the concentration of so much investment capital into so few stocks will lead to “a lost decade” for investors who hold the Nasdaq 100 or even the S&P 500. Equity valuations will revert to the mean and, even if these businesses do extremely well, their share prices won’t.

These unpleasant facts lead to an important question: What should investors do when facing a lost decade in future equity returns?

I’ve suggested a number of potential strategies in the past, including using a “permanent portfolio” strategy. We’ve recommended holding at least 25% of your portfolio in short-term fixed income (cash). It’s also wise to look for opportunities in distressed corporate bonds, where equity-like returns can be earned without any equity valuation risk. And, of course, there are special situations, like “Trump’s Secret Stocks,” and many others, like the small-cap biotech stocks – recommended by Erez Kalir in Biotech Frontiers – where you can avoid equity valuation risk.

Here’s another strategy that I believe will work.

To succeed in a lost decade, look for “lost stocks.”

What are lost stocks? They are businesses that create incredible wealth, not through the expansion of their equity multiple (like Tesla) – but instead by their own internal cash generation plus excellent capital allocation.

These companies are run by excellent investors hiding inside businesses that everyone ignores.

Lost stocks use things like share buybacks and special dividends that don’t register as yield or total return on investment databases (such as Bloomberg). These strategies make their incredible performances harder for analysts to discover.

And these businesses are the absolute masters of capital allocation. They create enormous value by investing their cash flows in the best possible ways, whether that’s buying back their own shares or buying other businesses.

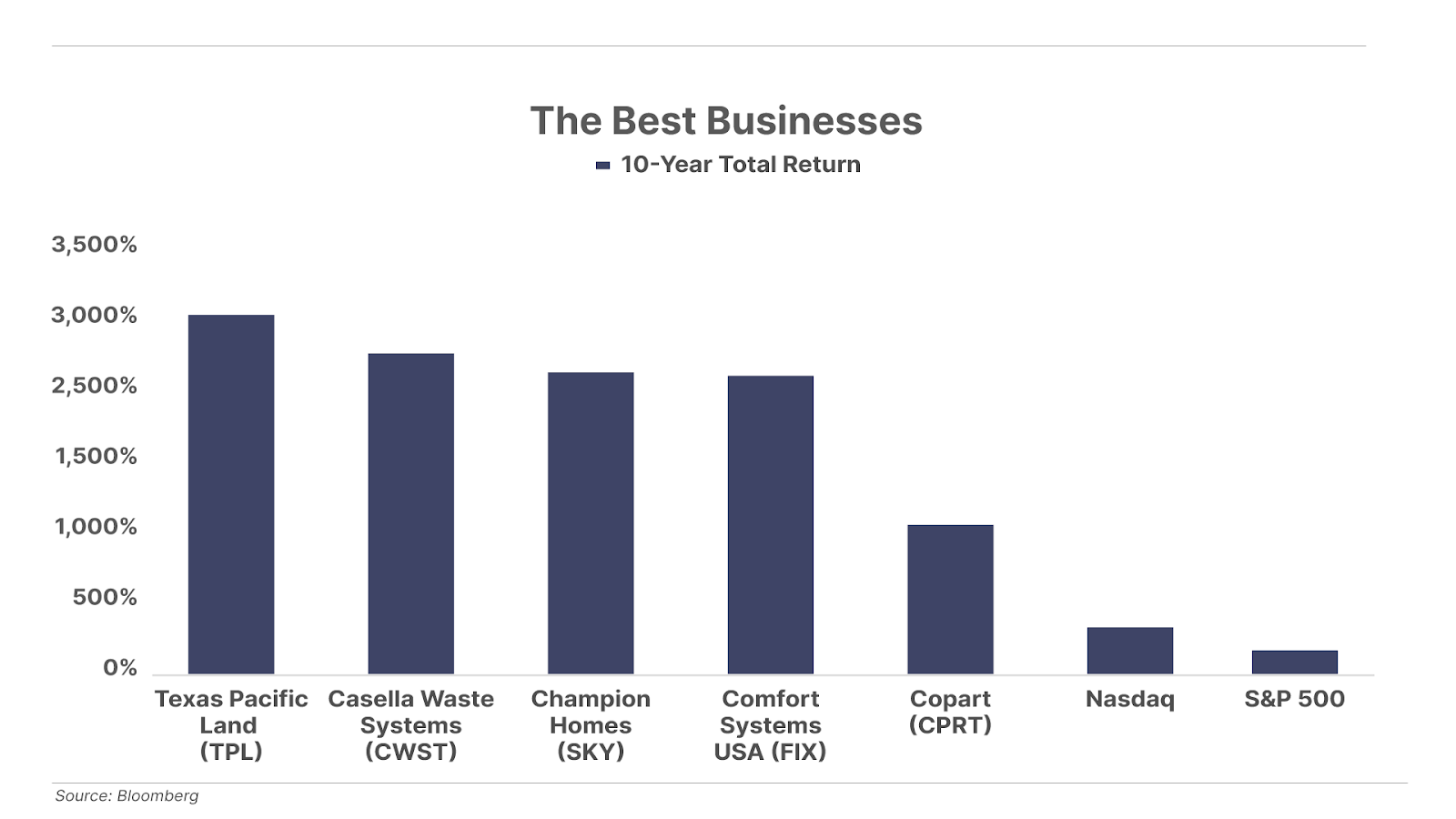

Here are five examples.

These businesses are like Wall Street’s mobile-home parks. They are some of the best businesses in the world, but few investors know where they are or how much cash they produce. They’re always out of sight. For example…

- Texas Pacific Land (TPL) – up 2,900% last 10 years, 66x earnings

- Casella Waste Systems (CWST) – up 2,632% last 10 years, 926x earnings

- Champion Homes (SKY) – up 2,434% last 10 years, 35x earnings

- Comfort Systems USA (FIX) – up 2,406% last 10 years, 33x earnings

- Copart (CPRT) – 1,141% last 10 years, 40x earnings

We’ve written a lot about Texas Pacific Land over many years (I first recommended it to investors in 2012) – so you’ve probably heard of it, but most investors haven’t. It operated, for decades, as a secret investment partnership. Incredibly simple business: huge land bank, producing leasing revenue, mineral royalties, and, lately, revenue from a rapidly growing water business. It was virtually impossible to get any information about the business. And all while, it kept buying back massive amounts of stock. From 1994 through 2013, Texas Pacific reduced its share count by 44%.

Casella Waste Systems is a serial acquirer in the garbage business. Nobody goes to Aspen or Davos and talks up their trash company. And that’s why it’s been able to buy $2 billion worth of high-margin waste-management businesses over the last decade at cheap prices, creating massive value for shareholders.

And… my favorite… Champion Homes, which builds mobile homes. Talk about the opposite of a glamour stock! How has it driven such incredible returns? Simple: it has great gross margins for a homebuilder (24%) and uses its cash profits to make great investments, both in its shares via buybacks, and in other mobile-home manufacturers. Again, nobody at Davos is bragging about the latest developments in trailer homes. Over the last decade, total shares outstanding have declined from 135 million to 57 million.

Why is this company my favorite? There’s nothing better than making money off the poor. Why? Because, like Ayn Rand taught, they have always been with us. People who make terrible life decisions still need a place to live. And that’s a market that’s never going away.

Comfort Systems USA makes it very easy to understand heating, ventilation, and air conditioning (“HVAC”). They buy HVAC businesses – having done over $1 billion in acquisitions over the last decade.

And the last example, Copart, is, like Texas Pacific Land, an incredible story of hiding in plain sight for decades. They own more than 200 junk yards in 11 different countries. Junk yards? Yep, that’s right. And guess what? Gross margins are close to 50%! Copart produces $1.5 billion in cash each year. This capital flows back into its own operations for growth (and more junk yards) and into its own shares ($1.4 billion in buybacks last decade).

As you can tell by their valuations, these “lost” stocks aren’t lost anymore. And just to be clear… I’m not suggesting you buy these stocks. They are, though, the kinds of unglamorous, underappreciated businesses operated by managers who are brilliant allocators of capital that can be astonishingly good investments.

And… when the correction comes… these are exactly the kind of businesses that you should keep in mind. Lost stocks can save you from a lost decade.

Three Things You Need to Know Before We Go…

1. Inflation remains a problem. This morning, data from the Bureau of Economic Analysis showed the Federal Reserve’s preferred measure of inflation – known as the personal consumption expenditures (“PCE”) price index – rose 0.3% in December, and was up 2.6% year over year. Though in line with Wall Street analyst expectations, it remains stubbornly above the Fed’s official 2% target, and is only likely to reinforce the central bank’s “wait and see” stance. Bottom line: Don’t count on another rate cut anytime soon.

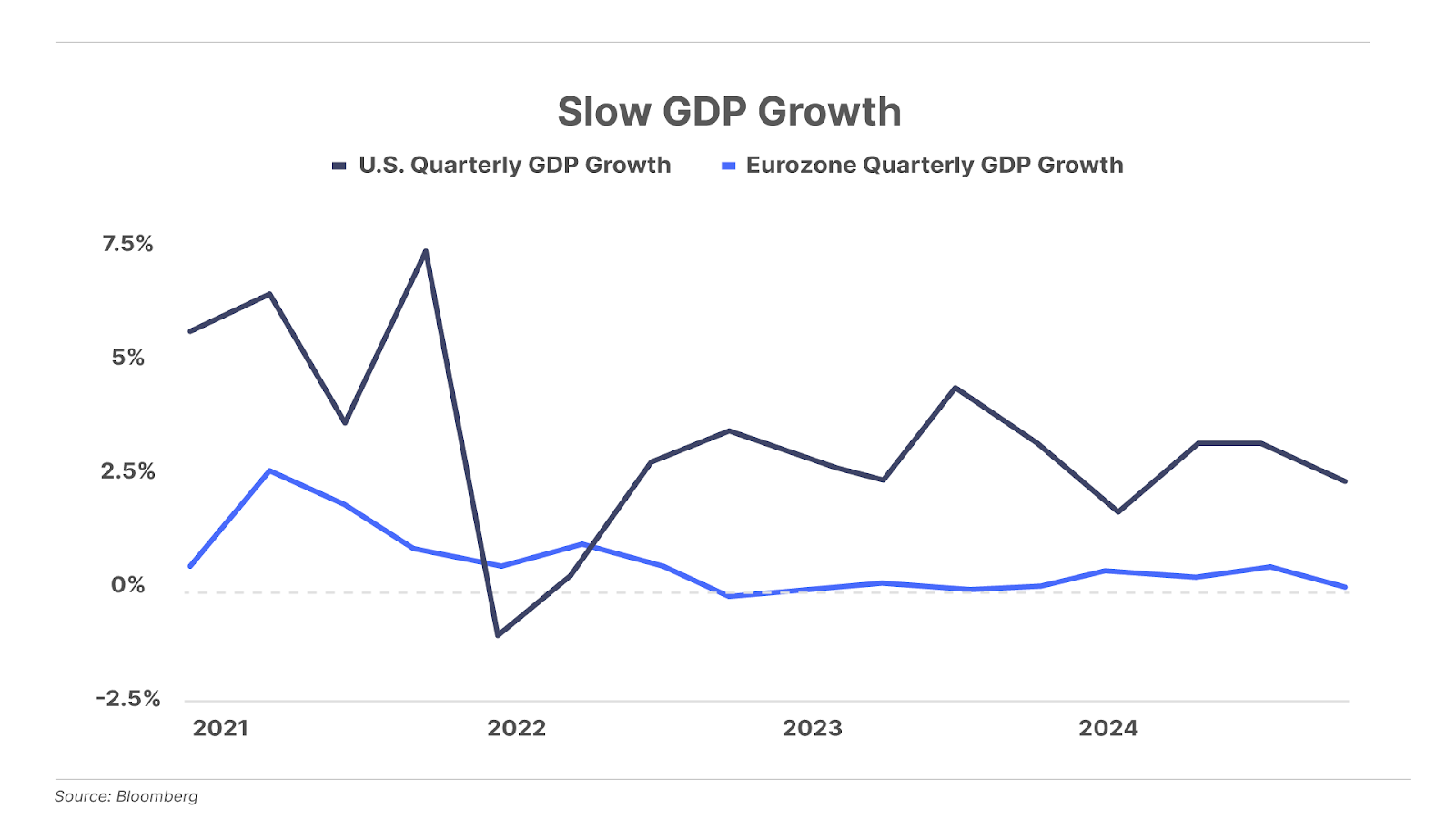

2. The global economy is weaker than advertised. U.S. Q4 GDP grew by 2.3%, falling short of Bloomberg’s consensus forecast of 2.6%. Growth in the U.S. isn’t so strong… and given how often GDP data is revised downward, it may be weaker than these initial numbers suggest. Still, though, the U.S. is trouncing no-growth Europe, where the economy didn’t grow at all during Q4 (and policymakers cut interest rates by a quarter point yesterday).

3. AI fails to reignite iPhone sales. Despite high expectations for an iPhone sales “supercycle” driven by the artificial intelligence features in the newest iPhone 16, Apple’s earnings report yesterday showed iPhone revenue declining by 1% year on year (“YOY”). This continues the tech giant’s trend of sluggish revenue since 2021. The company has kept earnings per share growing with an aggressive stock buyback program, but free cash flow has dropped by nearly 30% YOY to $27 billion in the latest quarter. Apple has become increasingly reliant on financial engineering over organic sales growth.

And one more thing…

My great discussion on Commodity Culture. On January 16, I talked with the Commodity Culture podcast, where I told host Jesse Day that if the U.S. imposes 25% tariffs on all trade with the United States, the purchasing power of the U.S. dollar would fall 50% in the next 18 months – “it will be horrific for average Americans.” I told Jesse that the U.S. needs to “roll back the collectivism of the federal government,” but instead the Trump administration wants to add to it with the creation of another federal bureaucracy – the External Revenue Service. “I hope that it’s political bluster,” I said. We also talked about gold-mining stocks (I have opinions…), the collapse of General Electric, the surprising potential of Sony, and what might happen with today’s leading tech stocks. Click here to watch it.

Porter & Co. expands our weekend repertoire… Check your inbox tomorrow at 10 am ET, for the second issue of Saturday Stock Screen. Using a filtering strategy inspired by the late Charlie Munger, we launched this new subscriber benefit last week to give readers a behind-the-scenes look at how our analysts scour the 3,000-plus available stocks to find those worth digging into… and potentially becoming recommendations for The Big Secret on Wall Street. We concluded the issue with a look at a company that we feel is poised to benefit from the coming deregulation of natural gas – paid-up subscribers got the company name, ticker, and full details. This week, we reveal a company receiving a kick in the pants from an activist investor. Readers, it seems, love this free new benefit. Farrell B. writes: “Thank you for your new Munger screen and recommendation.” And Matt V. says: “This is great! More overdelivery by Porter and his team.” Look for it in your inbox tomorrow at 10 am ET.

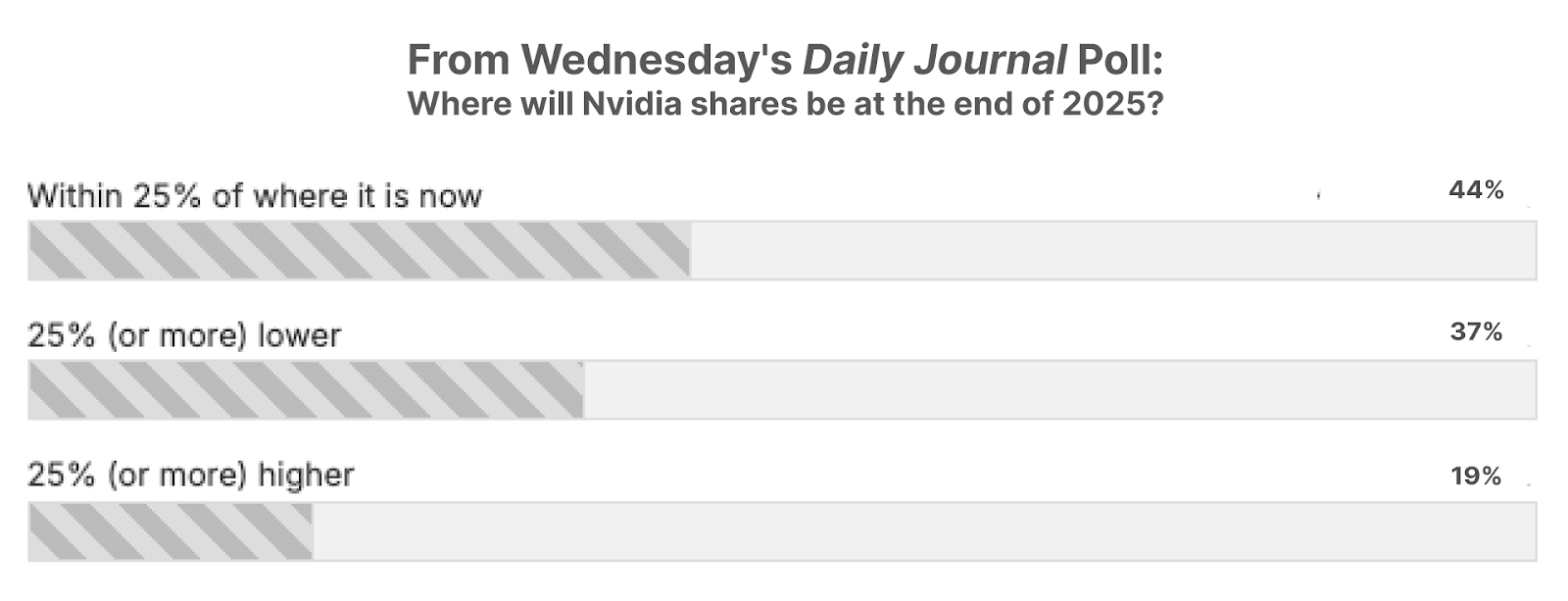

Poll Results… Where Will Nvidia Be At The End of 2025?

On Monday, the tech world was blindsided by the news that Chinese AI startup DeepSeek launched a service that produces similar results as ChatGPT and other U.S.-based AI platforms – but at a fraction of the cost. Shares of leading AI chipmaker Nvidia (NVDA) plunged 17% in one day on the news. So on Wednesday, we asked readers where they thought shares of NVDA would end up this year… More than a third of survey takers think DeepSeek is long-term bad news for Nvidia, with 37% saying shares will be “25% (or more) lower,” with 44% saying shares will be within 25% of where they are now, and just 19% are super-bullish, selecting “25% (or more) higher.”

(Puzzled by what – exactly – Nvidia does, and produces… and how it fits in with the rest of the chip-boom subsector? Porter put together a presentation about what we call the parallel-processing revolution. It’s changing the world – and it’s a lot bigger than ChatGPT and DeepSeek. Learn more here.)

Mailbag

Let me know what you think by sending comments to [email protected]

Today’s question comes from D.W., who writes:

I own several data-center stocks. If it turns out [Chinese AI] DeepSeek is right about no more need for data centers, maybe we ought to ditch these stocks now before they go down more and just hang on to chip stocks.

I don’t really like data centers anymore – the possibility of them using up most of the electricity isn’t fair to everyone else, like schools and hospitals. We also can’t let electricity get unaffordable for average folks.

Porter’s comment: Thanks for your question.

Just to clarify our Monday Daily Journal about DeepSeek… I don’t think that the rise of more efficient large language models (“LLM”) is bad for the overall artificial intelligence (“AI”) industry, including the suppliers for things like GPUs, data centers, and energy. In fact, it will most certainly be a net positive development over the long run.

History shows that reducing the costs and resource-intensity of a new technology uniformly leads to more adoption of that technology, and thus ultimately more consumption –- a phenomenon known as the Jevons Paradox.

Think about the shale revolution. Did lowering the cost of hydrocarbon extraction cause any drop in demand for the supporting industries of oilfield services like drilling equipment of fracking chemicals? No, in fact it led to the opposite – as these efficiencies lowered the cost to end consumers. That fuelled new demand which, in turn, led to new record highs in shale production.

However, the shale business model also generated oilfield bankruptcies along the way. New technologies sometimes spawn waves of overinvestment that create excess capacity – resulting in some industry players going bust along the way.

The same will probably be true in the world of AI as companies develop more efficient LLMs. The companies that invested heavily into the more resource-intensive LLMs that are rapidly becoming commoditized, like OpenAI, could very well end up being victims. Likewise, chipmakers like Nvidia (NVDA) as well as cloud- computing providers like Microsoft (MSFT) may face trouble as LLM providers learn to do more with less, at least in the short-term.

This means there could be a painful digestion period as the hundreds of billions in capital expenditures into things like data center capacity, made based on yesterday’s assumptions about the resource-intensity of LLMs, may prove misguided in the near-term.

Good investing,

Porter Stansberry

Stevenson, MD

P.S. As today’s tech news illustrates… there’s a lot of money to be made by anticipating what’s next in the world of technology. And there’s a lot of money to be lost if you fall even just a step behind.

There’s one guy who I’ve learned over time is fantastic at anticipating what’s coming next in the world of tech. Jeff Brown has guided his subscribers to five-digit gains by getting in front of some of the biggest evolutions in technology.

And I mean way, way in front. Bitcoin in 2015… Nvidia in 2016 (an all-time great, even reflecting this week’s washout)… AMD in 2017… and Jeff’s readers have benefitting enormously.

Today, Jeff is focused on cryptos. President Donald Trump has made clear his intention to pave the way for America to become the global hotspot for cryptocurrencies… and Jeff is anticipating what cryptos are best positioned to benefit. Go here to hear about what he’s thinking now.