Issue #42, Volume #1

And Why It’s Worse Than The Subprime-Mortgage Crisis

This is Porter & Co.’s free daily e-letter. Paid-up members can access their subscriber materials, including our latest recommendations and our “3 Best Buys” for our different portfolios, by going here.

Three Things You Need To Know Now:

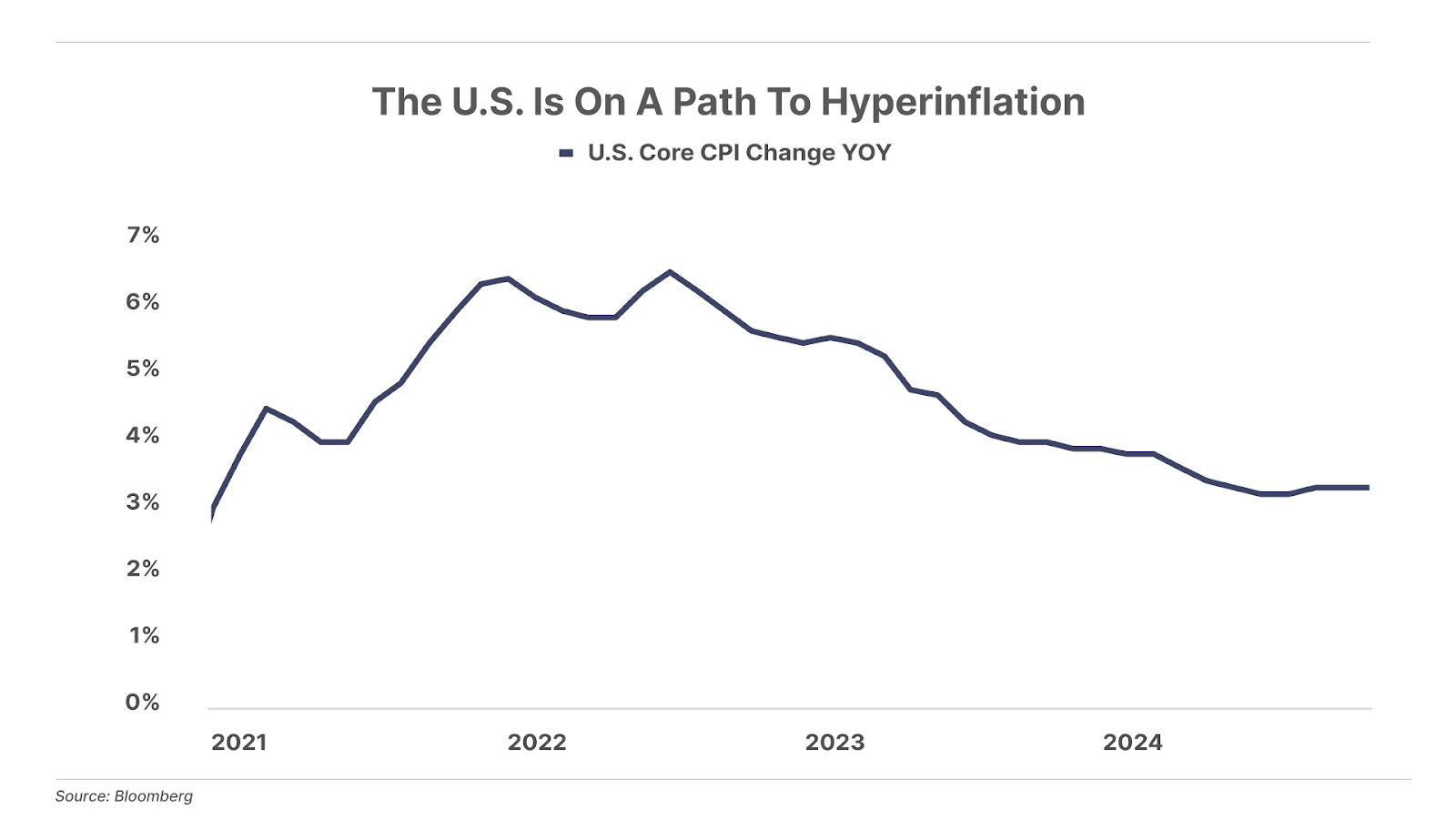

1. This will be the last Fed cut in this cycle. Government deficit spending continues to propel inflation, which hasn’t fallen below 3% despite weak private-sector employment and a 33.5% jump in corporate bankruptcies this year. Deficit spending in the last two months was $624 billion, putting the country on track for a highest-ever $3.5 trillion deficit in 2025. We are on the path to hyperinflation. When asked about the likelihood that President-elect Donald Trump would actually cut government spending, Grok, the AI tool built by Elon Musk, says, “The chances that Trump will significantly reduce U.S. federal spending appear low… While intentions might be there to cut spending, substantial reductions in federal spending are unlikely.”

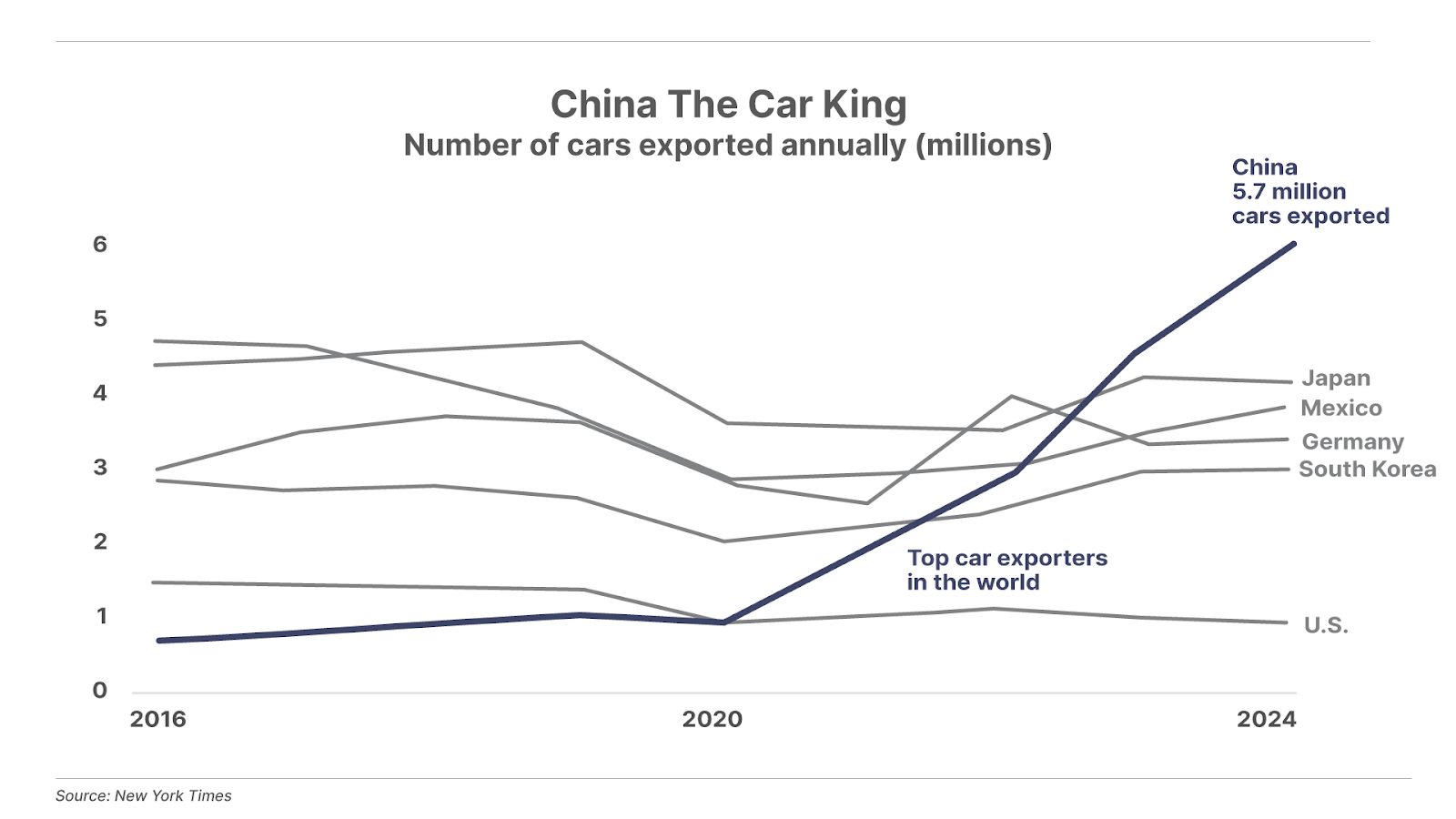

2. China is gutting the world’s auto markets. The price of TVs declined 98% after China joined the World Trade Organization in 2001, sending Sony’s (SONY) share price down by 61% to less than $10. Autos are next. China has gone from being a non-factor in the global auto market to, suddenly, the world’s largest exporter (!), with 5.7 million cars exported in 2024. Shares of Volkswagen (VWAGY) recently slipped below $10 and have declined 53% since 2021. Also at risk: Nissan Motor (NSANY, shares down 61% over the past five years) and Stellantis (STLA, shares down 7% in the last five years).

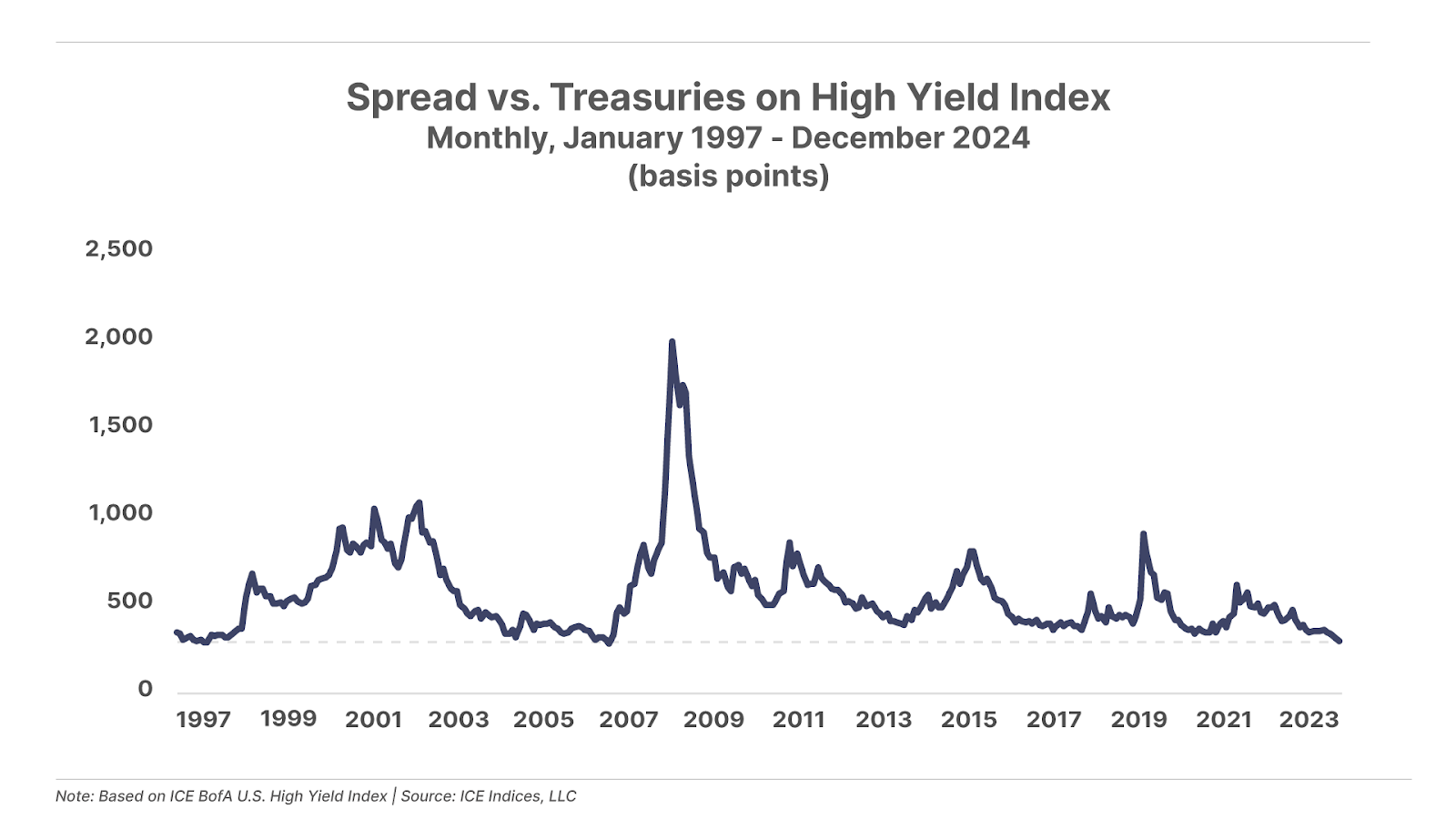

3. Credit markets hear no evil, see no evil. High-yield corporate bonds are now yielding 5.86%. On a risk-spread basis (that is, compared to similar duration U.S. Treasuries) these non-investment-grade corporate bonds are yielding less than two percentage points more than U.S. Treasury bonds. Porter & Co.’s high-yield analyst Andy Lipman says, “right now there seems to be demand for both babies and bathwater.” Maybe it’s different this time (lol), but in the past when the credit markets have been this sanguine about the risks to corporate bonds relative to government bonds, they have been woefully wrong, every… single… time… In fact, according to the definitive risk-spread index (the Merrill Lynch ICE Index), this credit market risk spread has only been “tighter” twice before.

The risk spread was this tight in September 1997, not long before the “Committee to Save the World” had to engineer the Fed’s first-ever hedge fund bailout (Long-Term Capital Management). And it was this tight again in 2007, shortly before the entire global financial system’s meltdown in 2008. I wonder what it will be this time… See the essay below for one possibility.

And one more thing…

Fartcoin’s total market capitalization has now reached almost $1 billion. These things – our government’s reckless deficit spending, the credit market’s Lake Wobegon outlook (where all bonds are better than average), the soaring prices of gold and Bitcoin, the record-level of equity prices, and the existence of nonsense like Fartcoin – are all related. This is what happens when the world’s reserve currency becomes wildly inflated, which in turn leads to massive financial-asset bubbles. And these manias never last. There’s a reason Warren Buffett has raised a record amount of cash (as a percentage of Berkshire Hathaway’s assets). He’s learned to be cautious when others aren’t. I hope you’ll do the same!

Coming up this week:

On Wednesday, the Fed is expected to issue another 25-basis-point rate cut… even though, this week, we’ll see new data released every day that indicates a stagnating economy and rising inflation. November retail-sales data, released on Tuesday, are expected to show only a slight increase of 0.2% (so much for Black Friday). Thursday’s Q3 GDP estimate is expected to sink from 4.9% to 4.7%, and November’s existing home-sales data are forecast to decline by 2%. And, to round out the week, November’s PCE (personal consumption expenditures) data, a key inflation measure, is projected to rise 0.2% after an 0.3% rise in October.

Poll Results… (Almost) Everyone Loves Bitcoin, It Seems…

While Bitcoin is hitting new highs today… and a majority – 54% – of respondents to our Friday poll think that Bitcoin will move up at least 20% in 2025 (it’s up 150% in 2024 so far). Just 12% think it’s headed significantly lower next year… and one in 10 readers doesn’t give a hoot about Bitcoin (though perhaps they should)…

Commercial Real Estate Looms As A Massive Market Risk

And Why It’s Worse Than The Subprime-Mortgage Crisis

The heads are finally starting to roll in commercial real estate.

Seattle’s leading commercial real estate mogul, Martin Selig, has defaulted on $240 million in mortgages on seven office towers. The loan collateral includes two of Seattle’s most prominent office towers, a recently redeveloped former Federal Reserve complex and a brand new 15-story tower at 400 Westlake Avenue. These were Class A office properties. Selig is the most prominent commercial real estate developer in Seattle. He once owned a third of all Seattle office space, including Seattle’s tallest building, the 76-story Columbia Center.

The loans matured in 2019, but Selig was able to avoid default for more than a year. Downtown Seattle office vacancy is currently 35%. That’s substantially worse than during the Global Financial Crisis (21%)! This unprecedented collapse in demand for office space has created a huge gap between what these buildings were appraised at when the loans were made (in 2019), and what these buildings would bring in an auction today. As a result, the sums owed on the mortgages far exceed the market value of the buildings, which make them very difficult to refinance.

But, so far, there’s been a huge amount of “pretend and extend” going on as bank managers have strong incentives to avoid foreclosing. Extending principal repayment dates, lowering interest rates – even offering a period of forbearance – is usually preferable to writing down a loan. As long as there’s some way to pretend that a loan can be made good, the banks don’t have to reserve against the losses, which immediately hit earnings and reduce bonuses.

But these perverse incentives have the impact of allowing losses to pile up inside banks, hidden from investors.

Sooner or later, as one loan after another is revealed to be rotten, investors panic (usually all at once) and begin to sell every bank that’s connected to the business.

That’s exactly what happened in 2008, with subprime mortgages. The subprime mortgages and the subprime underwriters all went bust in 2007. But the damage didn’t hit Wall Street for more than a year as one major investment bank after another simply pretended that its massive subprime losses were only temporary and could be restructured.

With leading investors like Martin Selig going bust, the obvious question investors should be asking is: how bad will the losses be when all of the B-players default too?

Well, according to S&P Global, more than $2 trillion of commercial real estate mortgages will mature over the next two years (’25 / ’26). The average interest rate on maturing loans (underwritten in ’20/’21) is only 4.3%. Good luck refinancing at twice that rate today.

Nobody is talking about this yet, but the size of this pool of distressed capital is much larger than the subprime mortgage market at its peak in 2005 ($625 billion).

The “extend and pretend” game the big banks played last year will only make these problems much worse in 2025, because nobody will know where the toxic waste is buried. (Here’s a hint: Bank of America.)

And, I don’t think people have figured out yet that the losses in commercial real estate are going to be much worse than the losses in subprime housing. Even a house that was owned by a terrible subprime borrower can still be cleaned up, repainted, and re-sold to a legitimate buyer fairly easily and cheaply. An empty, 50-year-old office building? Not so much.

Last month, one of Baltimore’s most prominent Class A office towers (201 N. Charles Street, 28-stories, 268,000 square feet) sold at auction for $2.55 million, or $9.51 per foot. It was sold to its leading creditor for $4.1 million in 2022. It sold in 2013 for $19.7 million. That’s an 87% decline in market price over the last decade.

Another $200 billion of office mortgages remain outstanding and will need to be refinanced before the end of 2026.

That said… it’s not all doom and gloom in the real estate sector… at all. Porter recently sat down with Brad Thomas, one of the foremost experts on REITs (real estate investment trusts), to talk about some of the compelling asymmetric opportunities in the sector. You can listen to their conversation here.

As always share your thoughts on this topic with me directly: [email protected]

Good investing,

Porter Stansberry

Stevenson, MD

Mailbag

Albert S. writes:

I am excited to be on your team and to learn from you. I am 60 and a lifelong investor. I started out of college (Penn State) working at Parket/Hunter in Pittsburgh as a registered rep but Black Monday hit (October 1987) and I decided to leave the industry. Anyway, I really like the way you think and I am looking forward to our relationship building over the years. I have two questions as a brand-new subscriber trying to better understand the service and your thinking. The first is, I have heard you on videos recommending being at least 25% in cash now, but I don’t easily see that recommendation in monthly updates or in the portfolio. Where would I look to more easily see that recommendation? The second question is, why not recommend a small percentage in a Managed Futures ETF like Simplified Managed Fund Strategy ETF (CTA) or the iMGP DBi Managed Futures Strategy ETF (DBMF) instead of just sitting in cash? They both have the potential to earn single-digit returns in a flattish type market, and if we do get a good correction, their value will go up, giving me more to invest in equities at that time. I am very interested to hear your thoughts on this topic. BTW, I am about 20% cash and 13% in managed futures at the moment. Thanks in advance!

Porter’s comment: Al, thanks for your note and your business. If you go to our website and look for my Permanent Portfolio, you’ll find an example of how I’d recommend handling your asset allocation: 25% stocks, 25% insurance companies, 25% gold and Bitcoin, 25% cash. Most subscribers focus on individual stock selections and that’s fine – buying and holding eight to 10 great businesses is all you really need to do. But, for folks who want or need a smoother ride, I recommend reading and understanding my approach with the Permanent Portfolio. In regards to managed futures ETFs, I plead ignorance. I haven’t done the homework necessary to feel confident in these approaches.

Scott M writes:

Long time reader here. Back in the day, The 12% Letter, Retirement Millionaire, Extreme Value, and Stansberry’s Investment Advisory were my investment GPS. My investment strategy in the past has been to focus on the forever-type investments with dividends in companies I understood. Every time I ventured away from that in the past I got burned. I am by no means what I would call “a high net worth” investor, but I’ve done well following your advice over the years. My forever investments are in a good spot providing six-digit income via dividends alone so in June I decided to focus my new 401(k) account entirely to Erez Kalir and his Biotech Frontiers recommendations. His $5,000 per position example that he uses in his write-ups is me… that’s what I can do at the moment in this account. Although I missed the quick gains at the beginning of the year, starting in June with $5,000 in every open position and following his recommendations to the letter (buy and sell), I’ve done extremely well. I got the double in Sagimet Biosciences (SGMT) and the-almost 250% in uniQure (QURE). I’m looking forward to being a $10,000 per position and beyond as I follow his expertise. I love what you’ve put together at Porter & Co., and I’m glad I found you again as soon as I did. Y’all are the best.

Porter’s comment: Erez’s work in Biotech Frontiers is simply the best growth-stock research I’ve ever seen published anywhere. He’s produced a 90% win rate and a 42% average return. Phenomenal. I’m very proud to publish Erez and Distressed Investing’s Martin Fridson, two analysts who are living legends in their markets and offer vastly more credibility than just about any other writers in the history of the investment newsletter business. Unless you’re already a Partner Pass member… I strongly recommend that you call my office today at 888-610-8895, (+1 443-815-4447 internationally) and find a way to join our Partner Pass subscription so that you can enjoy both of their publications next year (and for as long as we’re publishing them) for about the price of the profits from just one of their many good recommendations. And, hey, you’ll also get little ’ol me too.

P.S. In a guest essay in our September 10 Porter & Co. Spotlight, my old friend Tom Dyson at Bonner Private Research recommended the shares of Zim Integrated Shipping (ZIM). And then… keep on reading.

See… there aren’t many real geniuses in the investment business.

Tom is one of them… because he’s a savant at the single greatest investment challenge: your emotions.

Can you be patient enough? Can you be humble enough to cut your losses when it’s clear that you’re wrong? Can you remain disciplined to a winning strategy when there’s a drawdown?

Tom, more than any other analyst, has always understood this challenge and has faced it head on.

And he’s produced fantastic results. He piled into gold in the early 2000s… bought Bitcoin at $1 in 2013… I could give you a dozen more stories like that.

And one of them is Zim. The shares moved up 50% within two weeks.

Of course, not every recommendation that Tom makes appreciates so much, so quickly. Zim’s move was equivalent to a 400,000% annualized gain!

That’s incredible. However: the reason you should read Tom Dyson each week isn’t merely because he is a genius at investing and will bring you outrageously good investment ideas.

You should read him each week because he understands the emotional challenges of putting capital at risk and, unlike anyone else in this business, he can guide you through those challenges.

Tom won’t just give you great investment ideas: he will sit in the foxhole with you and fight.

Read him and you’ll see immediately what I mean.

You can access Tom’s research – at a special rate for Porter & Co. subscribers – here. It’s fantastic value for the money… I don’t know why anyone wouldn’t want to be able to tap into Tom’s brain.