Issue #26, Volume #2

When Everyone Else Is Selling, Of Course

And Why Buying Bonds Can Be Even Better

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| We might be on the verge of a market panic… Watch the VIX to know when to buy great stocks… Why bond investors can make more than stock investors during market panics… China fights tariffs with bigger government deficits… |

Can you feel the market beginning to “roll over”?

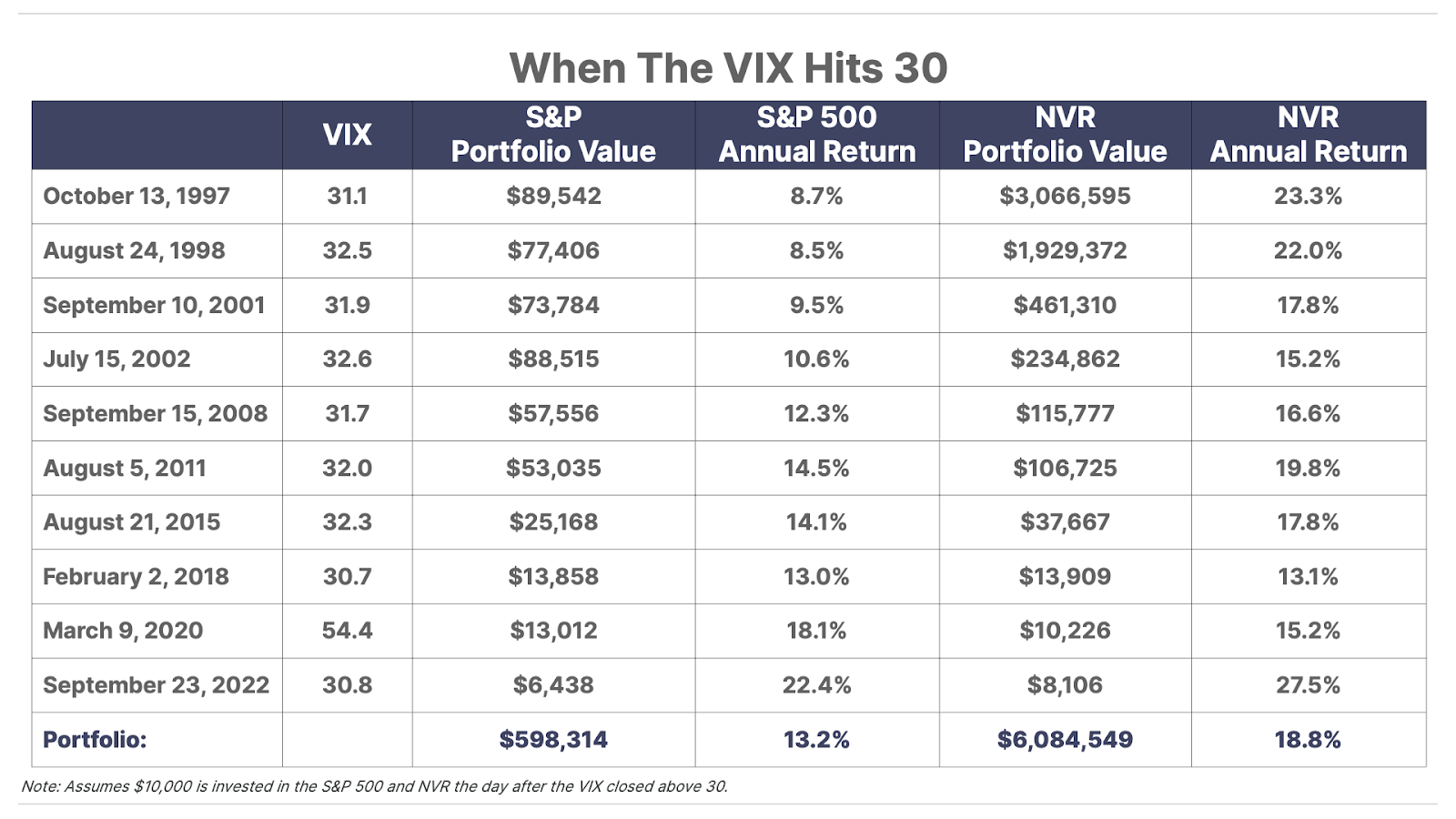

I can. Seems like we’re on the verge of a market panic to me. And, if you’re waiting for a good time to buy, you keep your eye on the VIX (CBOE Volatility Index).

This is an index that measures the risk premium embedded in the pricing of put options. (Put options are leveraged investments betting that stocks will decline). You’ll notice that when the VIX goes above about 30 or so, it’s usually a very good time to buy high-quality stocks.

The St. Louis Federal Reserve tracks the index on its website, going back all the way to 1990.

One good strategy to use is simply to stockpile cash (and investment ideas) until the VIX crosses 30. Then deploy your capital into the market. It’s hard to be patient, but there will always be opportunities to buy. During my career (which began in 1996) notable opportunities to buy high-quality stocks by using the volatility indicator occurred in: 1997, 1998, 2001, 2002, 2008, 2011, 2015, 2018, 2020, and 2022.

That’s roughly one opportunity every three years. And you’ll notice the last such opportunity occurred almost three years ago (hint).

Below is a table showing the exact days when the VIX first closed above 30 and the investment outcome today if you’d simply invested $10,000 into either the S&P 500 or NVR (NYSE: NVR), the ultra-high-quality homebuilder that I’ve been recommending for almost 20 years.

Please note: I’m showing the day the VIX first closed above 30. Typically, the volatility spike goes higher than 30. And, sometimes, like in 2008, volatility goes much, much higher. In those cases, buying on the first day that volatility closes above 30 could be “too soon.” But, of course, it’s impossible to buy the exact bottom (or sell at the exact top). Watching volatility just gives you reasonable short-to-medium term entry points. And those opportunities, even if far from perfect, can still make a big difference in your investing, especially if you wait to buy the market’s best businesses.

In the short term, waiting for a volatility spike can massively improve your investment performance. And even over the very long term, having a good entry price still matters.

If instead of buying at a relatively low price, you’d happened to buy at the highs of these same years, your results would have been materially worse – especially in high-performing companies.

If you bought the S&P 500 on VIX spikes above 30 (as shown above), your annualized return over the last 28 years would be 13.2% – enough to turn $10,000 invested on each spike into just under $600,000.

Meanwhile, buying around the highs of these same years (instead of during a big selloff) would have only grown 7.9% annualized, producing $348,305 in gains, or 30.1% less.

And if you bought NVR on VIX spikes above 30, your annualized return over the last 28 years would be 18.8% – enough to turn $10,000 invested on each spike into more than $6 million!

What really matters? Understanding which stocks are going to produce far higher than average results is important. But knowing when to buy matters a lot too.

Investing is, in some ways, like a rigged carnival game. Think of the stock market as a financial ring toss.

Sure, it looks like a perfectly reasonable and fair game, because that’s how it’s designed to look. At the carnival, players are constantly reminded “every player wins a prize.” In the stock market, you’re constantly taught that stocks go up. On average, investors earn 8% a year, just as the sign says.

Meanwhile, the reality is, a relatively small percentage of companies (like NVR) end up garnering all of the profits over time. And an even-smaller percentage of investors end up collecting all of the gains too.

Here’s a sobering fact. The only reason your total returns will be so much higher if you’ll wait for volatility to spike before you invest is: those are the same days most investors are panicking and selling.

And, I’d be willing to bet that, if you’re honest, a lot of people reading this message actually lost a lot of money on those dates above, instead of waiting to hoover up all of the “alpha” those mistakes created. (Alpha is the fancy financial term for returns in excess of average, adjusted for volatility.)

Investing is, mainly, a game of patience and expert knowledge.

Investors who have both do very well. They never allow their emotions to interfere with their knowledge. They are unwavering because they know exactly how to win. And even though they might never mention it to you, they also know exactly why you’re going to lose: ignorance, emotion, greed, impatience.

Give yourself an honest scorecard. Are you the player or the patsy?

If you want a far easier way to win – to make larger returns with less risk – then I would urge you to learn how to invest in high-yield bonds. In fact, if you compare the dates of those VIX spikes to the dates when bond risk spreads “blow out,” you’ll notice both things happen at the same time.

That’s why, just as the St. Louis Fed monitors the VIX index, it also monitors risk spreads in the bond market via the Bank of America High Yield Index Option-Adjusted Spread Index.

When investors get scared, they sell risk – in both the stock market and the bond market.

But the bond market offers investors three big advantages that you won’t find in stocks.

#1. In the bond market, a lot of this panic selling is “forced”

As bonds are downgraded, banks and other financial institutions often must sell them to maintain average credit ratings on their portfolios. This can produce even bigger price dislocations than in stocks.

#2. All of these bonds are guaranteed – by law – to pay off at face value, no matter what the price they’re trading at now

Thus, investors can know – as long as the company doesn’t go bankrupt – exactly what their total returns will be, yield and capital gain. They can also know exactly when they will get their capital back. It’s impossible to know these things with stocks, which makes “guessing” which stock to buy in the midst of a market panic a heck of a lot harder.

#3. Corporate bonds bought at discount during market dislocations can offer incredible income, with cash yields well above 15% annually

When you’re making more in cash yield than you can make in the stock market (on average), it’s awfully hard to lose money.

As a result, it’s often possible for bond investors to make even more than stock investors during market panics, especially over the short to medium term – while taking far less risk. That’s why I urge investors who haven’t been successful in stocks to please at least try investing in bonds. I’ve seen it completely change people’s lives, taking them from terrible investors to great investors.

And… in his last issue… Distressed Investing senior analyst Marty Fridson said he’s seeing his first signs that a major opportunity in the bond market is just around the corner.

So, I hope you’ll watch my video about why I’m making corporate bonds – bought at a discount – the foundation of my “second life.”

One thing, though.

These “spikes” – when stock market volatility soars and when risk-spreads get blown out in the bond market, they typically only last for three or four days. Or less. Thus, if you do not have your “shopping list,” – if you’re not completely ready to buy, with cash in the account and orders lined up, ready to go, you will often miss the opportunity.

That’s why, I’m urging you: Do. This. Today.

Learn everything you need to know from Marty about buying these bonds at the right time. And be ready to execute. These opportunities could arrive next week… next month… or even tomorrow.

Three Things To Know Before We Go…

1. Trump’s tariffs take effect (for now). On Tuesday, the Trump administration officially imposed 25% tariffs on a broad swath of imports from Canada and Mexico, after initially delaying them for a month. However, later in the day, Commerce Secretary Howard Lutnick announced that the president will “probably” reach compromise deals with the two countries that would involve scaling back at least some of these new tariffs. And as we go to press, reports suggest the White House is already considering another one-month delay on tariffs on imported autos.

2. Germany and China governments ramp up fiscal spending. Just as the U.S. federal government is hoping to reduce stimulus and budget deficits, foreign governments are going in the opposite direction. Germany is mulling plans to create a $500 billion infrastructure fund to boost its military and overall economic growth. And China announced an increased budget deficit target of 4%, the biggest in over 30 years, to promote domestic spending and reduce the impact of U.S. tariffs. This shift in global money flows likely means that stock markets outside the U.S. will continue surging ahead of American stocks.

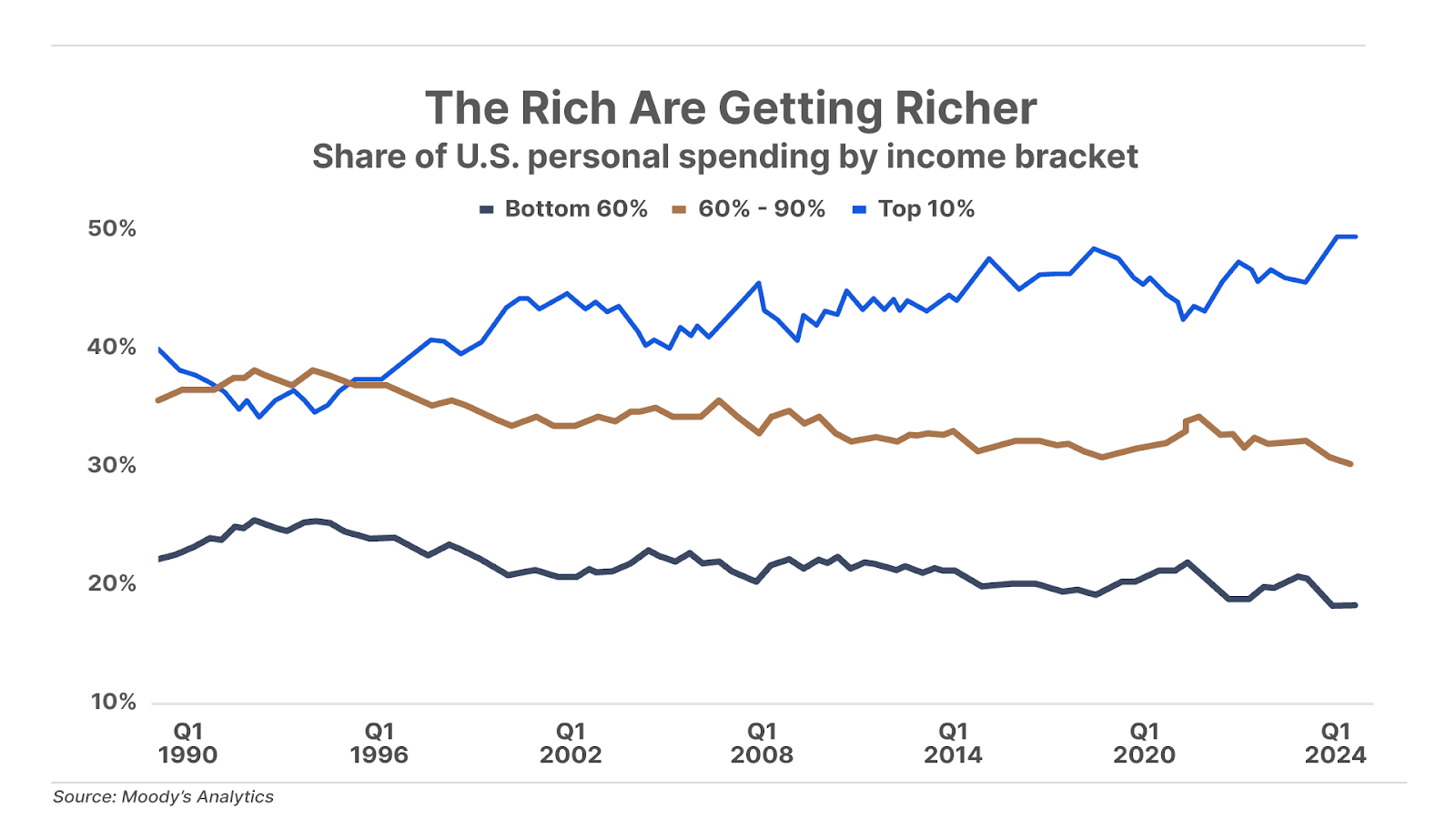

3. The wealthy drive the economy as the middle class falls further behind. The top 10% of earners now account for 50% of all consumer spending, up from 36% in 1995. This lopsided concentration of spending makes the economy vulnerable – if a financial shock were to hit top earners, and their income plunged, the ripple effects throughout the economy would be severe. So it’s no surprise that consumer debt has ballooned and credit card defaults are on the rise: the middle class is struggling.

And one more thing… New Research From Porter & Co.

This week, Porter & Co. Partner Pass members are receiving two new issues… Today, we are publishing the second recommendation of Asymmetry, a service that uncovers undervalued investments with limited share-price downside and huge upside potential – featuring a deeply undervalued international oil producer with barrels of reserves that the market is resolutely ignoring.

Yesterday, we published the second issue of High Conviction, a service for which we issue recommendations only when our level of conviction about an investment is at its highest… for businesses whose success is not just likely – it’s inevitable. Both of these new issues are also available to Partner Pass members on the Porter & Co. website.

Both are Partner Pass member only benefits. To learn more about becoming a Partner, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.

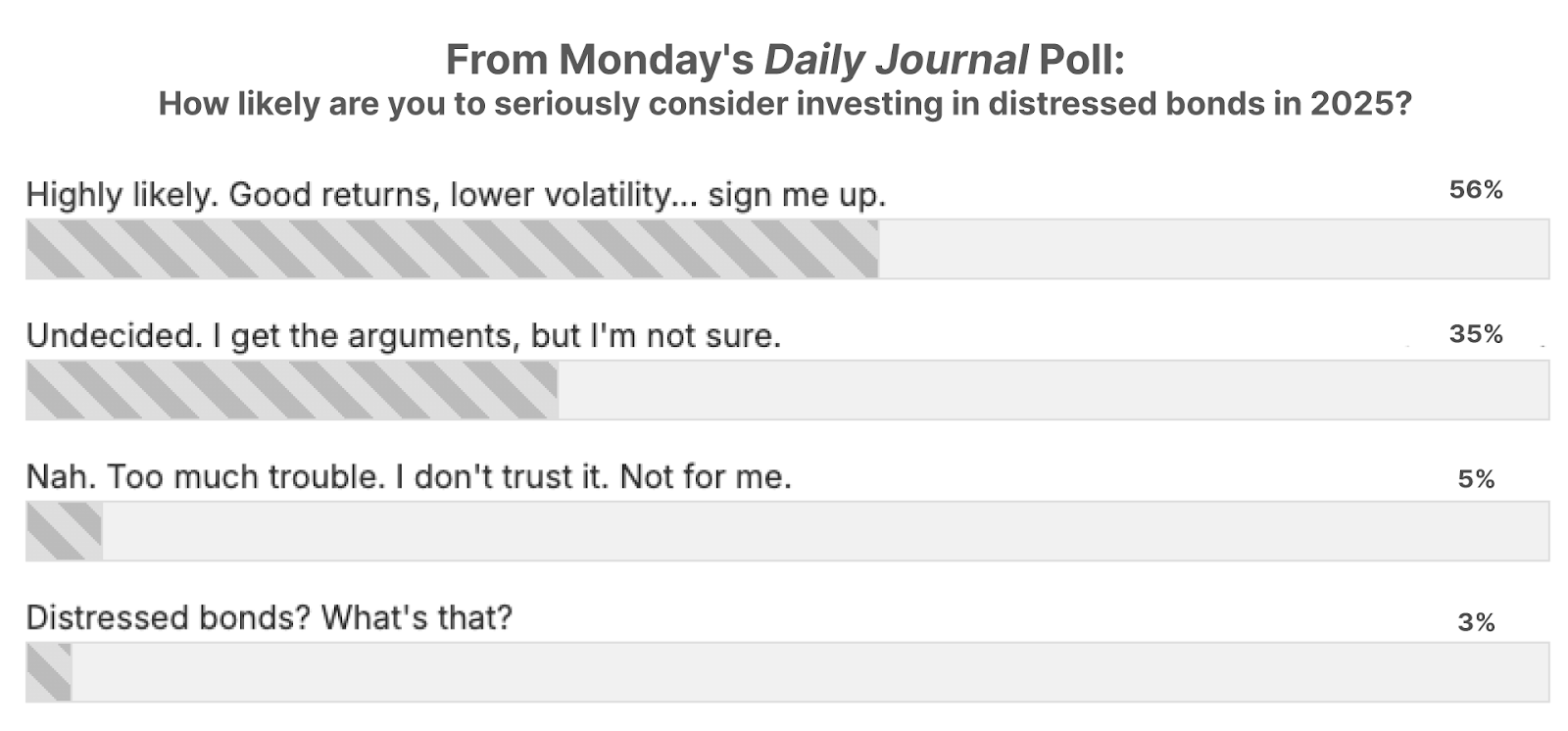

Poll Results… Will You Be Investing In Distressed Debt?

Porter ended Monday’s Daily Journal, in which he answered readers’ comments about their worst investing mistakes, by saying: “to build a second life is to focus on a little-known kind of investing that’s almost exclusively available to professional investors like Marty Fridson. But, with Marty’s help, I believe it’s possible… to make 30%+ gains annually, by investing in” distressed debt.

Then we asked… “How likely are you to seriously consider investing in distressed bonds in 2025?”

A majority of readers (56%) selected the option: “Highly likely. Good returns, lower volatility… sign me up,” and just over one-third of survey takers said: “Undecided. I get the arguments, but I’m not sure.” Only 5% went with, “Nah. Too much trouble. I don’t trust it.” (And 3% said they didn’t have a clue about distressed bonds!…)

(If you’re looking to get started… see Porter’s video here.)

Tell us what you think. We’d love to hear from you: [email protected]

Mailbag

In Friday’s Daily Journal, in explaining the safe and consistent returns to be earned investing in distressed debt, Porter said this about investing in stocks:

Most people (about 80%) are going to lose money when they invest in stocks. Even though the market seems like a fair game, it’s actually rigged to make sure that your emotions will betray you.”

In response, paid-up reader David A. wrote in to say…

We are a society that has grown into a “blame everyone else, but not oneself.” I have seen this in all areas of life today. Nobody wants to assume any accountability for his/her actions. Nobody!

We also think we can be the one person who invests in the market, and we will win every time. Oh, what egos we all have. We pay for excellent advice, then we stray from the advice provided, lose money, and, well, blame the person or firm that we trusted to give us the advice in the first place. You are right, most of us have no business getting into the market, if we are not going to take advice and hold the security for many years.”

Porter’s comment: I agree completely that everyone is ultimately responsible for themselves.

But I think much of life – and especially the stock market – is akin to a carney game. Like the ring toss, it looks like it’s a reasonable and fair game. But it’s an illusion. There’s no realistic way to win. The sign says “every player wins,” but out of the 25,000 people at the fair, only one or two are going to walk away with the giant monkey.

What’s really going on? The average player is getting fleeced. And those losses pay for the enormous winnings of a very few players.

A casino is a more honest business: it never claims that its games aren’t rigged.

Meanwhile, guys like Ed Thorp (have you read his books?) figured out how to “beat the dealer” by counting cards. Vegas responded by using fresh decks for each hand.

Even so, people still go to Vegas by the millions and try to count the cards.

People are foolish.

Meanwhile … in the stock market… the people who figured out how to win the carney game (by only investing in great businesses at reasonable prices and holding for the long term), like Warren Buffett and a handful of others, are consistently ignored.

Instead, people insist on throwing rings each day.

And they will get taken, again and again and again.

I guess someone has to pay for all the big towers in Manhattan.

As a financial publisher, one of the most frustrating realities is, the publishers who produce the worst information for investors – the ones who encourage the ring tossing – are the folks who will garner the subscribers and make all of the money.

People won’t pay for the information that actually works.

They will only pay to have their false assumptions reinforced.

Porter Stansberry

Stevenson, MD

P.S. Gold isn’t rallying… it’s in the midst of a major bull market.

Central banks are buying… and so are big institutions. The price of gold is up 39% over the past 12 months.

But…you wouldn’t know it. The media is obsessing over AI and tech stocks… and almost entirely ignoring gold. During the 2011 gold peak, CNBC ran an average of 12.4 gold-related segments per day. Today? Less than two.

In a world of escalating uncertainty, gold is insurance… and a proven – over millennia – way of retaining value over time.

How to best take advantage of the quiet gold boom? Porter looks to Marin Katusa, who for the past 15 years has been involved in, and helped finance, countless resource investments around the world – several of which Porter has personally been a part of.

Gold mines, copper mines, silver mines, oil and gas fields, lithium, clean tech, uranium… Marin’s done it. He’s one of the greatest experts in the world when it comes to gold, silver, and natural resources.

And Marin has ideas about what’s happening with gold… and how to best position yourself now. Go here to learn more.