Issue #140, Volume #2

How Sweeping Changes To Global Banking Regulations Will Vastly Increase Demand For Physical Gold

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Gold bars arriving at JFK… Triple the previous inflows… The world’s money supply is at stake… The Bank for International Settlements in Switzerland… The revenge of the regulators… Gold is becoming money again… Bankruptcies soar… Trump’s farmer bailout… |

No one had ever seen anything like it.

Early this year, planes full of gold bars were landing nearly every day at New York’s Kennedy Airport and nearby Newark Airport in New Jersey.

In the first quarter, U.S. banks imported $75 billion worth of gold bars into the country. That’s roughly triple the previous record of quarterly inflows. JPMorgan alone took delivery of more than $4 billion in gold, against gold futures contracts expiring in February. That was the second-largest single delivery in the history of the COMEX – the futures and options market for gold and silver.

If you heard about any of this (and you probably didn’t), you were told these massive gold purchases weren’t meaningful… just “trading desks” or “arbitrage.” Later in the spring, the line was that it was because of the risk of tariffs being imposed.

No one – absolutely no one – told you the real reason. There are very good reasons why no one will talk about this…

There are enormous sums of money at stake. In fact, what’s at stake is all the money in the world. The most important change to the world’s monetary system since 1971 is happening: Gold is being re-monetized.

To understand what’s taking place, you have to understand what counts as “money” in the world’s banking system. Since the end of World War II and the Bretton Woods agreement, which established the current system, the monetary base of the world’s financial system has been U.S. government obligations – U.S. Treasury bills, notes, and bonds. And because the dollar (after August 1971) was no longer linked to gold at a fixed rate, gold played no practical role in the monetary system at all.

Today, the Bank for International Settlements (“BIS”), headquartered in Basel, Switzerland, sets international banking standards among the G20 group of industrialized nations. And the critical rule-making body at the BIS, The Basel Committee on Banking Supervision, is a consortium of central bankers and regulators from 28 jurisdictions, including the U.S. Federal Reserve, the European Central Bank, and the People’s Bank of China.

Starting in 1988, “Basel I” introduced a comprehensive framework for standardizing capital requirements for the world’s largest commercial banks. These rules introduced the concept of risk-weighted assets, meaning that different kinds of assets would count (or be discounted) by regulators toward the required reserves of each bank.

As a concept, this makes a lot of sense. The AAA-rated obligations of Apple (AAPL) are worth a lot more in a crisis than a junk bond from an unknown small foreign company.

An unintended consequence of these regulations is that they have the impact of deciding what “money” is in the global economy. Money is whatever assets count 100% toward capital ratios and liquidity ratios at commercial banks.

You and I might think gold – or Bitcoin – is the perfect form of money. But until those assets are valued as highly by the world’s banking system, they’re not money. U.S. Treasury bonds have been rated as the highest-quality banking reserve asset for decades – and officially since 1988, when Basel I went into effect. Thus, as far as the banking system is concerned, the dollar is money, and gold is not. But now that’s changing.

In 2004, Basel II took effect. These rules allowed banks to use “sophisticated” risk models, which in effect allowed banks to set their own reserve standards and use internal calculations for risk weighting everything from corporate loans to mortgage-backed securities.

You’ll never guess what happened next…

Following the financial crisis, in 2010, Basel III was published. These rules were, more or less, “the revenge of the regulators.” They’re designed to make sure the world’s largest banks have enough assets and enough liquidity to survive a 30-day, real-world “stress” test. As a part of this major reform, gold is being massively upgraded as a reserve asset and in a way that I believe will make it more attractive than U.S. Treasuries.

In short, gold is about to become money again.

To understand what’s going on here, you have to understand the two critical parts of Basel III. (I certainly wish there was an easier way…. Nobody wants to read banking regulations!)

Part one of the new regulations is simply tougher standards around risk-adjusted assets. No real changes from the past – just more objective and uniform standards. But part two of the new standards is about liquidity and matching durations for certain illiquid bank assets. And these new regulations will transform the world’s monetary regime.

First, there’s a new basic liquidity standard, the Liquidity Coverage Ratio (“LCR”), which requires banks to hold high-quality liquid assets (“HQLA”) worth at least 100% of projected 30-day outflows in a stress scenario.

The other new liquidity standard is the Net Stable Funding Ratio (“NSFR”) – it mandates that banks use longer-duration funding mechanisms to match their illiquid investments. In other words, banks can’t use overnight funding mechanisms to fund, say, 15-year mortgages.

The details are complex, but the bottom-line is this: there are going to be sensible requirements for how banks both safeguard their deposits and supply credit to the market.

These new rules pose profound trade-offs for banks. Consider the most important reserve asset: Level 1, HQLA.

These are “risk” free liquid assets, like cash or sovereign bonds. These assets count at full value toward reserve requirements with no limits on their portfolio weight. These assets are highly liquid safety nets. They can keep a bank afloat even during the worst crisis. That’s good for safety. But these assets are expensive to hold from an opportunity-cost perspective. They yield little to nothing. And although they don’t present default risk, they do carry duration risk… long-dated sovereign bonds can still lose value (marked to market) if inflation and interest rates rise (just ask Bank of America).

Down just a notch in terms of quality and liquidity is Level 2A. These are assets like AAA-rated corporate bonds and mortgage securities. These assets only count toward reserves at 85% of face value and are capped at 40% of the portfolio. These are still effective as a reserve asset and they offer slightly higher yields than sovereign bonds. Next is Level 2B. This is riskier fare like high-grade covered bonds, which face a 50% reserve value haircut and a portfolio cap of 15%.

It’s this mix of assets that banks must balance to maximize returns on equity yet retain stability.

Hoard too much cash? Lending dries up, profits sag. Stretch for higher returns by holding corporate bonds instead of Treasuries? A recession can trigger downgrades and fire sales, costing the banks billions.

It’s a difficult balancing act that’s gotten much tougher lately because of the rising volatility of sovereign bonds and the growing risk of a sovereign funding crisis.

Under Basel II, physical gold didn’t really exist as a bank reserve asset. Yes, technically it counted as a Level 1 asset – there was no haircut on its market price. But in other, more important ways, it didn’t count at all. In terms of liquidity regulations, gold was treated as a speculative commodity fit for trading desks, not capital reserves. And unallocated “paper” gold (claims on bullion) fared worse, haircut to 50% of face value for reserve calculations. These regulations made gold a very unattractive asset for banks, especially compared to U.S. Treasuries.

Basel III flips this script. It makes gold a very attractive reserve asset for banks and, in my view, the very best reserve asset.

Under Basel III, allocated gold (that’s physical gold kept in bank-controlled vaults) is treated as the highest-quality asset: Level 1, with full HQLA status. That’s full 100% credit for gold’s price, unlimited portfolio allocation, and zero required long-term stable funding.

Thus, under the new rules, gold is money again. It’s on par with U.S. Treasuries as a reserve asset according to the regulators, and some ways it’s clearly superior: there’s no duration risk, it’s uncorrelated to fiat-currency volatility, it’s a counter-cyclical asset, it’s counterparty-proof, and it’s globally fungible. It also can’t be automatically seized by the U.S. (Russia lost all its dollar reserves after its invasion of Ukraine.)

These new regulations will cause seismic changes in the demand for physical gold over the next three years.

To understand why, consider a $1 trillion bank like JPMorgan. If JPMorgan swaps $20 billion of AAA corporate bonds (which only count 85% of their face value toward reserves) for physical gold, that will unlock $3 billion (15%) in reserves without any capital drag, freeing perhaps $15 billion for loans. And yes, the same could be accomplished by exchanging for U.S. Treasuries. But this change in the rules will make the contrast between gold and Treasuries stark: The regulators say allocated gold is the same as Treasuries and there’s no duration risk in gold.

For banks, this isn’t an academic issue. Large commercial banks own $5 trillion to $10 trillion in Treasuries. If the 10-year yield spikes to 6% because of weak demand or growing fiscal risks, there could be a panic in the Treasury market, suddenly sending bond prices down.

The UK’s 2022 gilt meltdown offers a real-world example of these risks. Short-lived Prime Minister Liz Truss’ unfunded spending increases (like Trump’s) ignited a yield surge – 30-year gilts were up 160 basis points in days, triggering $100 billion in pension fund losses.

For U.S. banks, a Treasury market parallel would see yields gaping 200 basis points (2%) overnight. That would result in a 16.2% face-value decline – instantly. If you’re holding tens of billions worth of bonds, that’s a major risk. As these risks grow, more and more of the world’s banks will buy gold instead of Treasuries, just as central banks have been doing since the start of the Russia-Ukraine war.

While full implementation of Basel III will not be completed until at least 2028, most of its provisions took effect in July. If U.S. deficits breach 7.4% of GDP in 2026 (which is a baseline estimate by rating agency Fitch), the top 30 global commercial banks will begin adding substantial amounts of physical gold as a replacement for Treasuries. Slowly at first, perhaps. But remember the line from the movie Margin Call:

If you’re the first out of the door, that’s not called panicking.”

Gold is money again.

The Next Enron? Meet AI’s Ticking Time Bomb

Watch Porter Stansberry and Ross Hendricks detail how OpenAI’s Enron-like behavior has created a multi-trillion-dollar ticking time bomb across the entire stock market.

Plus: the one money move they recommend making to protect your wealth from what’s fast-becoming the single greatest threat to your portfolio.

Warning: Interview goes offline tonight at midnight. Watch now.

Three Things To Know Before We Go…

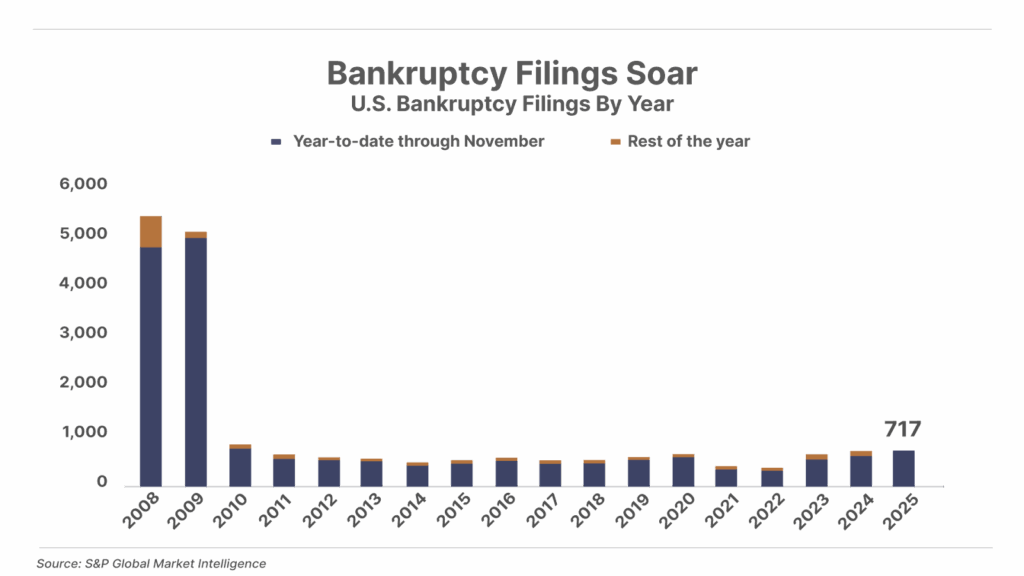

1. Corporate bankruptcies reach a post-financial-crisis record. According to S&P Global, 717 large U.S. companies have filed for bankruptcy year-to-date through November. This exceeds the full-year total for any year since 2010. Large bankruptcies are up 93% since reaching a post-crisis low of 372 in 2022.

2. Trump announces farm aid package. President Donald Trump plans to unveil a $12 billion aid package for farmers struggling with the financial fallout from U.S. tariffs. The relief includes up to $11 billion in one-time Farmer Bridge Assistance (“FBA”) payments for growers of commodities like soybeans, corn, cotton, rice, and sorghum – the commodities hit hardest by China’s retaliatory tariffs. China, the largest buyer of U.S. soybeans, has only fulfilled about one-third of its recent trade commitment, leaving that market severely depressed. The funding, drawn from the taxpayer-funded Commodity Credit Corporation, is intended to act as a temporary bridge until trade conditions stabilize.

3. Natural gas prices hit multi-year highs. U.S. natural gas soared above $5 per thousand cubic feet (“mcf”) last week, reaching the highest level since 2022, when Russia’s invasion of Ukraine sparked a global gas shortage. This time, the supply shortage and price increase could be longer lasting, driven by record high U.S. exports of liquefied natural gas (“LNG”) and the boom in gas demand for power generation from the artificial-intelligence revolution. Still, with gas prices up more than 70% in the last year, these two long-term trends could fuel the next natural gas supercycle.

And One More Thing… Poll Results

In Friday’s Daily Journal, following our report that many Wall Street investors are getting nervous about the amount of debt being used to drive the artificial-intelligence (“AI”) data-center buildout, we asked readers: “Do you think the AI bubble will collapse in 2026?”

The results… 61% of survey takers selected “Yes – it will burst,” while 39% are more bullish, selecting “No – AI stocks will continue to climb.”

Tell me what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Mailbag

In Friday’s Daily Journal, Porter highlighted the precarious situation the U.S. government finds itself in, given the mounting levels of debt and the ever-increasing amount of spending. A number of readers provided feedback.

Porter,

In 1965, I took freshman economics as a blowoff course (my major was electrical engineering). The prof was a self-made millionaire who sold home-delivery ice to folks with ice boxes without electricity in the 1940s in rural Arkansas. He was a fantastic teacher. He preached the same sermon you did today, except his example was the Weimar republic, and the Roosevelt spending spree of the 1930s. I soaked it all up.

As you predict it will be in the U.S. this time, sooner or later. Especially, as you predicted, the third rail, Social Security, will collapse in a few years. I predict they will nationalize the IRAs and 401(k) plans to fund Social Security. People who deny you did not understand basic economics, nor study it at all. Of course, that is what the politicians trade on.

You may be a voice in the wilderness, but keep it up. Maybe some will listen.

Raymond H.”

I am truly sorry for the U.S. governmental system because I am sure you are right. We need you as U.S. president and a big bunch of people like you in Congress.

Ken W.”

First thanks for all the hard work and insight you and your team provide. I had to write after seeing your “belly-laugh” picture.

Mario F.”

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.