Issue #102, Volume #2

The World Is Broken – Use Its Flaws To Your Advantage

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| All the wealth in the world can be yours… I’ve never spoken publicly about these ideas… Adler is German for eagle… Adler is also a man set apart from the world… Homebuilders like low rates… P&Cs like higher rates… Today’s weak jobs report… New Tech Frontiers… |

The government is lying to you.

Constantly. Every day. Every week. Every month. Year after year. And if you believe their lies, you’ll lead the life of a slave. You’ll toil in misery, for your entire life. You will never escape poverty. You will never achieve independence.

If you believe what they tell you, you’ll only get what they give you.

And they will give you nothing.

On the other hand, if you understand how the world is broken, all the wealth in the world can be yours. All you must do is simply reach out and take it.

And I can show you how.

I’ve generated billions in returns for investors in my career. And so far, this year alone, I’ve made an entire fortune – more money than most families will see in their entire lives. My personal eight-figure portfolio is up more than 90% so far this year.

Did I get lucky again? After 29 years of successful investing, I don’t believe it’s luck.

Was I speculating? Buying risky options and tech stocks? Not at all.

In fact, I’d argue that my investing strategy is far less risky than holding cash. More than half of my portfolio is allocated to fixed income and gold. And nothing I’m doing is complicated. In fact, most of my gains in equities came from only three stocks: Philip Morris International (PM), Franco-Nevada (FNV), and Alphabet (GOOG).

Sure, this has been a good year. But these results aren’t atypical of this approach. Earning 50%-plus annual returns are easily achievable, on average – and without suffering the kind of drawdowns most investors believe are inevitable. In fact, this strategy has volatility that’s much lower than the market’s.

If you’re an experienced investor, your bullshit alarm is probably going off – at full volume. I don’t blame you at all. There’s an enormous amount of money spent every year on financial propaganda to convince you that these kinds of investment returns aren’t possible. But the truth is, under certain conditions, they are inevitable.

In any case, the statement above and these dynamics from my actual portfolio are from my Interactive Brokers account as of today. There’s no denying these facts.

Return: 90%

Beta: 1.0

Sharpe Ratio: 2.1

Sortino Ratio: 3.2

(If you don’t know what the Sortino ratio is, I urge you to look it up. A Sortino ratio above 3 is virtually unheard of. But, a high Sortino ratio is the exact goal of this strategy.)

You should also know that I’m far from the only person who understands both the theory and the execution of this strategy. And I’m certainly not the best in the world at this kind of investing. In fact, the world’s largest hedge fund was built using these ideas.

In short, I didn’t come up with this approach on my own. I was very lucky to be mentored by one of this strategy’s founding theorists. I’ve spent most of my adult life studying these ideas and figuring out where, and under what conditions, these strategies work best. (Unfortunately for most Americans today, that’s here, in America).

I am, as far as I know, the only leading theorist and practitioner who has ever spoken publicly about these ideas or our community. So if I end up dead, please know that I am happily married, I have two young children, and I have no desire, whatsoever, to kill myself.

If you still doubt what I’m saying, just ask yourself this question: How did a complete “nobody” writing a newsletter in Baltimore know more about Fannie Mae and Freddie Mac just before the Global Financial Crisis than every investment bank on Wall Street?

Just lucky?

Alright, then how did he know more about GM’s bankruptcy? And long before that, how did he predict the Russian default? How did this same person, without any technical background, foresee the rise of the entire internet – Amazon, Broadcom, Qualcomm, Adobe? How was he the first person to write about the shale oil boom (in 2010) and accurately predict that America would once again become the world’s largest oil producer?

How did someone without any family wealth or connections become a billionaire just by reading and thinking?

At the heart of our method, there’s a simple inversion. We’ve learned to use the government’s most powerful weapon of control to achieve our own financial ends.

I call these ideas and their execution in the markets, The Solution.

Don’t worry I’m not going to explain the entire backstory of how I came to know these ancient secrets of monetary theory. It would bore you to tears. But I will tell you that the core ideas behind The Solution were explained to me, in person, in the fall of 1998, by the most legendary of the Austrian School of economists, Dr. Kurt Richebacher.

Richebacher called these ideas the secrets of the “Adler.” And it was the most important, most compelling idea I’d ever heard. It still is.

Most people understand Adler as the German word for eagle. But to Richebacher and to a very select group of economists around the world, the word means something else entirely.

In our community, an Adler is a man set apart from the world because of the quality of his perception. He sees the world far more completely and far more accurately than others and uses that understanding to maintain his independence. An Adler is a man whose power, authority, and complete independence are achieved with his mind. And rather than using his mastery to control or influence the world, he uses these advantages to remain apart.

I’ve wanted to become an Adler ever since I heard that description. Let me help you become one too.

Here’s a crucial insight: the government’s Social Security system is a Ponzi scheme. There were never any contributions. The payments were never anything other than an additional tax. The capital was never invested – it was spent. As a result, there’s no way to finance the promised benefits. So to keep it going, the government must commit an enormous fraud.

Who will that fraud destroy? Most Americans. Let me show you how.

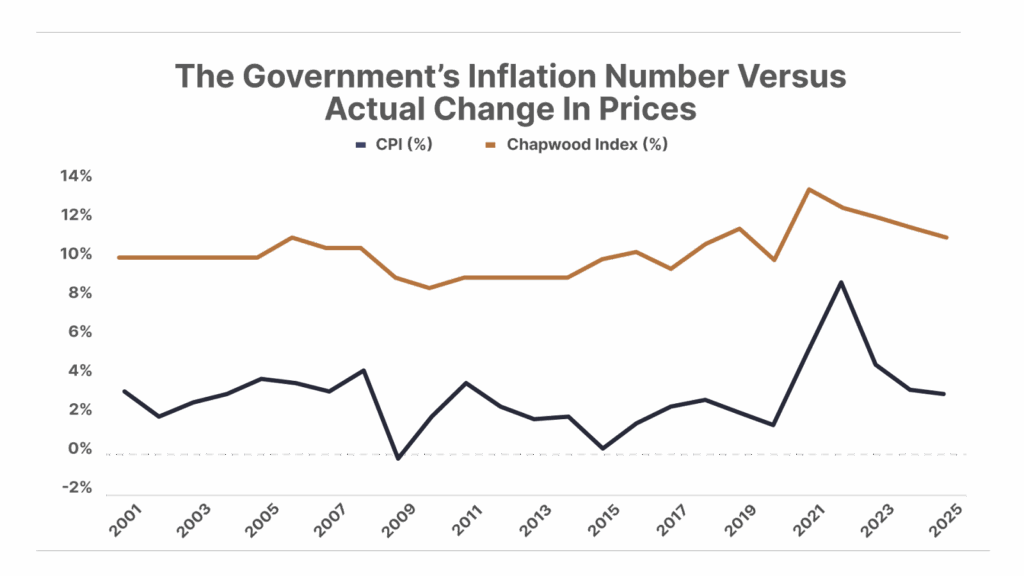

The chart below shows the government’s published rate of inflation, the consumer price index’s (“CPI”) annual rate of change versus the actual change in urban prices.

The Chapwood Index tracks a fixed selection of the 500 most-frequently purchased items for American urban households, including taxes, energy, food, consumer goods, and a variety of discretionary expenses. The Chapwood Index collects its data independently of the government.

If you believe the government, then, over the past 25 years, inflation has increased by 65% – about 2.5% per year – meaning that your purchasing power, as measured in dollars, has fallen by a bit more than half.

But, in fact, using actual urban prices, inflation has increased 935% – about 11% per year – over this period.

Why is the government lying? Because these lies are the only possible way to finance Social Security’s looming $100 trillion-plus obligations. In 1975, the U.S. Congress passed a law that requires Social Security to automatically increase its payments each year, to match the increase in CPI. And that, of course, is when the government started lying about inflation.

And what’s the impact of these lies over time? In 1975, the average Social Security recipient received benefits equal to 1.19 ounces of gold per month. In 2025, the average Social Security recipient receives only 0.55 ounces of gold per month. That’s less than half. And that erosion is going to accelerate… until the entire scheme simply fails.

Likewise, the government cannot possibly afford to pay an honest rate of interest on its $37 trillion in debt. If interest rates on government bonds were set by the free market, using real measures of inflation, the rate would be something around 15%. And the government would be bankrupt overnight.

What this means in practice is two things.

First, anyone who doesn’t quickly convert their dollars into high-quality assets will quickly see their wealth evaporate.

And second, real interest rates are much higher than the current nominal rates being charged.

Thus, an Adler sees immediately that the surest and safest path to wealth is borrowing as much capital as possible, with fixed rates, against high-quality assets. If you’ve made a lot of money buying homes with mortgages, you’ve made these exact gains. The house didn’t get more valuable. It depreciated. But because the dollar is being so quickly devalued and because the interest rate was so far below the actual inflation rate, you generated a massive gain.

Punishing savers and rewarding debtors and speculators is a horrible way to run a society. I’ve written many times before how financial debauchery causes social debauchery. And these problems will get worse – much worse.

But, in the meantime, there’s a virtually fool proof way to amass a huge fortune, and it’s sitting right in front of you. I call it The Solution.

The Solution

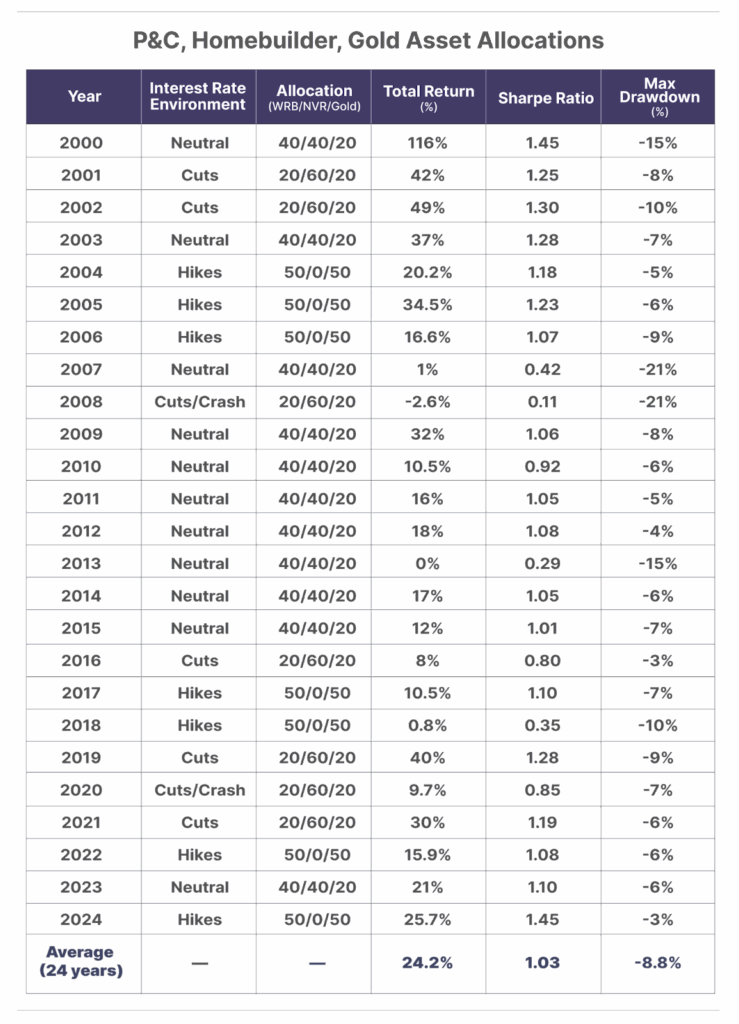

Use high-quality P&C insurance companies to compound capital over time. These firms benefit from the Cantillon Effect. This is a core monetary tenet of the Austrian school of economics. It was discovered by a French economist (Richard Cantillon) during the John Law-era monetary inflation of the early 1700s. What it explains is why firms that get access to newly created money first derive virtually all of the benefit of any ongoing inflation. In our economy, P&C insurance companies are a primary beneficiary of the Cantillon effect. And that effect, in part, explains why Buffett has usually kept more than 50% of Berkshire’s capital in P&C firms. He’s the ultimate Adler.

P&C firms have one notable weakness: they are sensitive to interest rate cuts, as their large portfolios of bonds will produce reduced cash flows when rates are lowered. Therefore, to minimize volatility and to maximize returns, we “hedge” our core position in P&C with high-quality (asset-light) homebuilding stocks. These businesses perform strongly during interest rate cutting cycles, as cheaper financing leads to more home sales.

And we hedge the entire portfolio primarily with gold since we believe that the U.S. dollar is heading for collapse. Thus, during periods of interest rate hikes, when stocks in general do poorly – especially homebuilders – we increase the gold allocation of the portfolio to 50% and reduce homebuilders to zero.

What did this strategy produce over the past 25 years – with only two stocks and gold?

- 24-year average total return: 24.2%

- Average annual Sharpe ratio: 1.03

- Average max drawdown: negative 8.8%

Here is a detailed annual table for the regime-timed portfolio – consisting of P&C company W.R. Berkley (WRB), homebuilder NVR (NVR), and gold – showing the interest rate environment, resulting allocation, total return, Sharpe ratio, and max drawdown.

For advanced practitioners, it isn’t hard to use these exact same ideas, along with borrowed capital, to produce extraordinary returns. Most investors believe using margin (borrowed money) is dangerous. And, yes, for most investors it is. But for an Adler, it’s a one-way bet: the interest rate isn’t covering the inflation rate. It’s no different than mortgaging a house.

Is The World’s Greatest Investor About To Shock Wall Street?

In just a few weeks, a move decades in the making could be revealed — and when it is, it could ignite the next great gold rush. Savvy insiders are quietly positioning now… before Buffett makes it official. Garrett Goggin has already pinpointed four tiny-gold-miners that could 100X once the announcement hits. It’s the perfect moment to be greedy — before the herd wakes up.

Click here to get Garrett’s Top Four gold picks now – before the world’s greatest investor pulls the trigger.

Three Things To Know Before We Go…

1. Labor market cracks. The non-farm payroll report released today revealed that U.S. employers added just 22,000 jobs in August – well below the 75,000 economists expected. It sent the unemployment rate up from 4.2% to 4.3%. Meanwhile, the revisions to prior months’ data showed that employers actually shed 13,000 jobs in June. The growing weakness in America’s labor market bodes poorly for the future economic outlook.

2. Rates are moving lower. Following this weak jobs report, the odds of at least a 25 basis point rate cut at the Federal Reserve’s September meeting rose to 100% (up from 98% on Monday). In addition, the odds of a 50 basis point cut rose to 12% from 0% earlier this week. But what’s particularly noteworthy is that long-term rates – including the yield on the benchmark 10-year Treasury note – also moved sharply lower. While the combination of massive government deficits and weakening demand for Treasury debt (see number 3 below) are likely to push yields higher over the long run, this move suggests the Trump administration may get its wish for lower borrowing rates, which would be welcome news for consumers and would-be homebuyers.

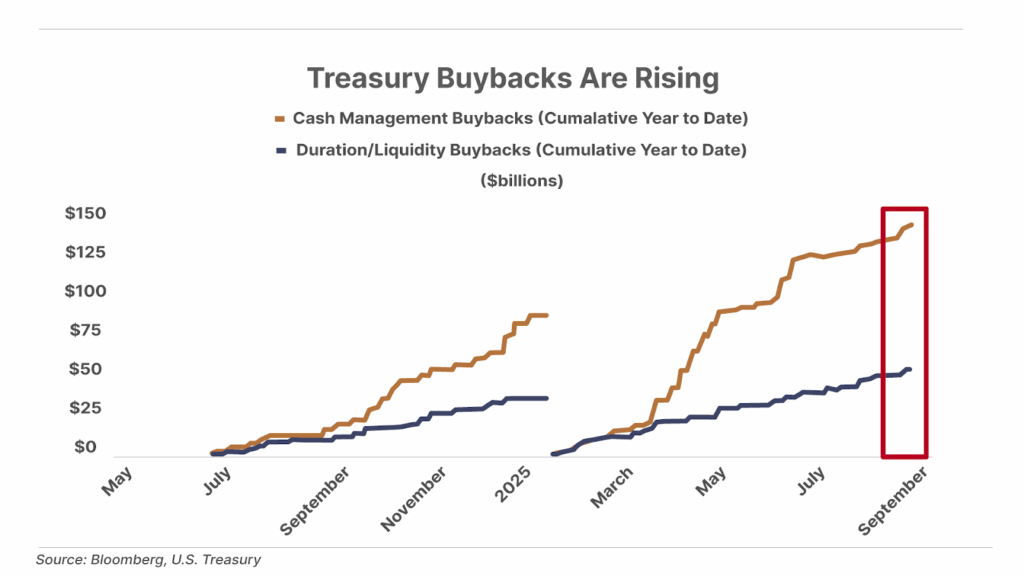

3. The U.S. just made its largest Treasury buyback in history – $10 billion. This follows its July decision to double the frequency of buybacks for 10- and 30-year bonds to improve market liquidity. So far this year, the Treasury has repurchased $138 billion in bonds – nearly twice the $79 billion total for all of 2024. While these buybacks have helped stabilize trading and maintain orderly markets, they also underscore a more fundamental challenge – demand for long-term Treasuries remains weak. Without intervention, yields on these bonds may be significantly higher, raising concerns about the long-term sustainability of U.S. borrowing and growing deficits.

And One More Thing… Falling Rates Aren’t Just Great For Consumers…

They’re also like rocket-fuel for technology stocks – particularly the early-stage technology (and biotech) companies our colleague Erez Kalir covers in Tech Frontiers, which just released a new recommendation yesterday.

In fact, it’s helpful to think of these stocks as long-duration equities… or the equity siblings of long-duration bonds – bonds that mature in the distant future. Their duration makes them especially sensitive to changes in interest rates. Think of a zero-coupon 10-year Treasury – a bond with no coupon payments and only a single “bullet” maturity 10 years down the line. A 1% change in interest rates will translate into a nearly 10% change in the price for this instrument.

Young technology businesses resemble these zero-coupon, long-duration Treasuries: Their positive cash flows tend to lie far in the future. And the farther into the future those cash flows lie, the more sensitive that company’s stock is to changes in interest rates.

In other words, we’re about to enter an incredibly bullish environment for these (tech and biotech) stocks. Which in turn means there has never been a better time to join Erez’s Tech Frontiers service. And for a limited time, you can try this service for yourself at the best price we’ll ever offer. Click here to get started now. Click here to access yesterday’s Tech Frontiers issue.

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

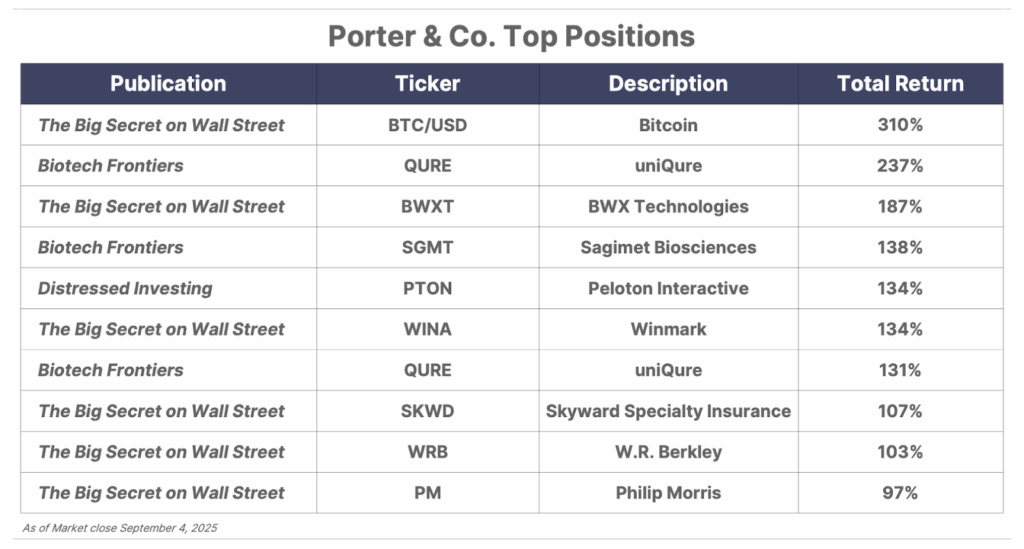

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care Team at 888-610-8895 or internationally at +1 443-815-4447.