The Parallel-Processing Revolution Will Take Time to Be Realized

History’s Lessons for Today’s Tech Investors

For the next two weeks in The Big Secret on Wall Street (through June 28), we’ll continue our exploration of the investment series we launched on June 7. We call this big story The Parallel-Processing Revolution – and it details the next step of the technological transformation that is driving (and that goes far beyond) artificial intelligence and machine learning.

In honor of Porter & Co.’s second anniversary, we’re making this vital four-part series free to all our readers. You’ll get a high-level view of this tech revolution and receive several valuable investment ideas along the way. However, detailed recommendations and portfolio updates will be reserved for our paid subscribers. If you are not already a subscriber to The Big Secret on Wall Street, click here…

Here are links to Part 1, which provides a series overview and tells how chipmaker Nvidia led the industry switch to parallel computing, and Part 2, chronicling two near-monopoly companies that power the production of chipmaking globally.

We share Part 3 of this series with you below.

She was a lonely computer geek working at the Stanford Graduate School of Business.

He was an equally lonely nerd across campus, managing Stanford’s computer-science lab.

They weren’t connected online. But, oh, how they wanted to be.

It was the early 1980s, and the building where Sandy Lerner worked was just 500 feet from Leonard Bosack’s. The two met on the Stanford campus and quickly fell for each other. But the course of true love needed some extra hardware in order to run smoothly.

The lovebirds’ two computer labs, as was normal at that time, ran on completely separate networks. And, almost two decades before the email-themed rom-com You’ve Got Mail became a box-office smash, there just wasn’t an easy way for two lovesick computer nerds to communicate with each other during their workday.

So Sandy and Leonard – like a much-nerdier beta version of movie stars Tom Hanks and Meg Ryan – set out to find a way to be together in cyberspace.

Separate networks? No problem. The two lovers set out to build a bigger network that linked the two buildings and allowed them to share software and databases. (And, maybe, a few private messages as well.)

Their invention, called the multi-protocol router, had the ability to add many computer networks to a single loop so the machines could all talk to each other. Along the way, Sandy and Leonard realized that the computer-connecting tool they’d developed was bigger than just the two of them.

In 1984 – by now, married – the couple left their jobs at Stanford, and maxed out some credit cards to start a fledgling computer business called Cisco Systems. The rest is history.

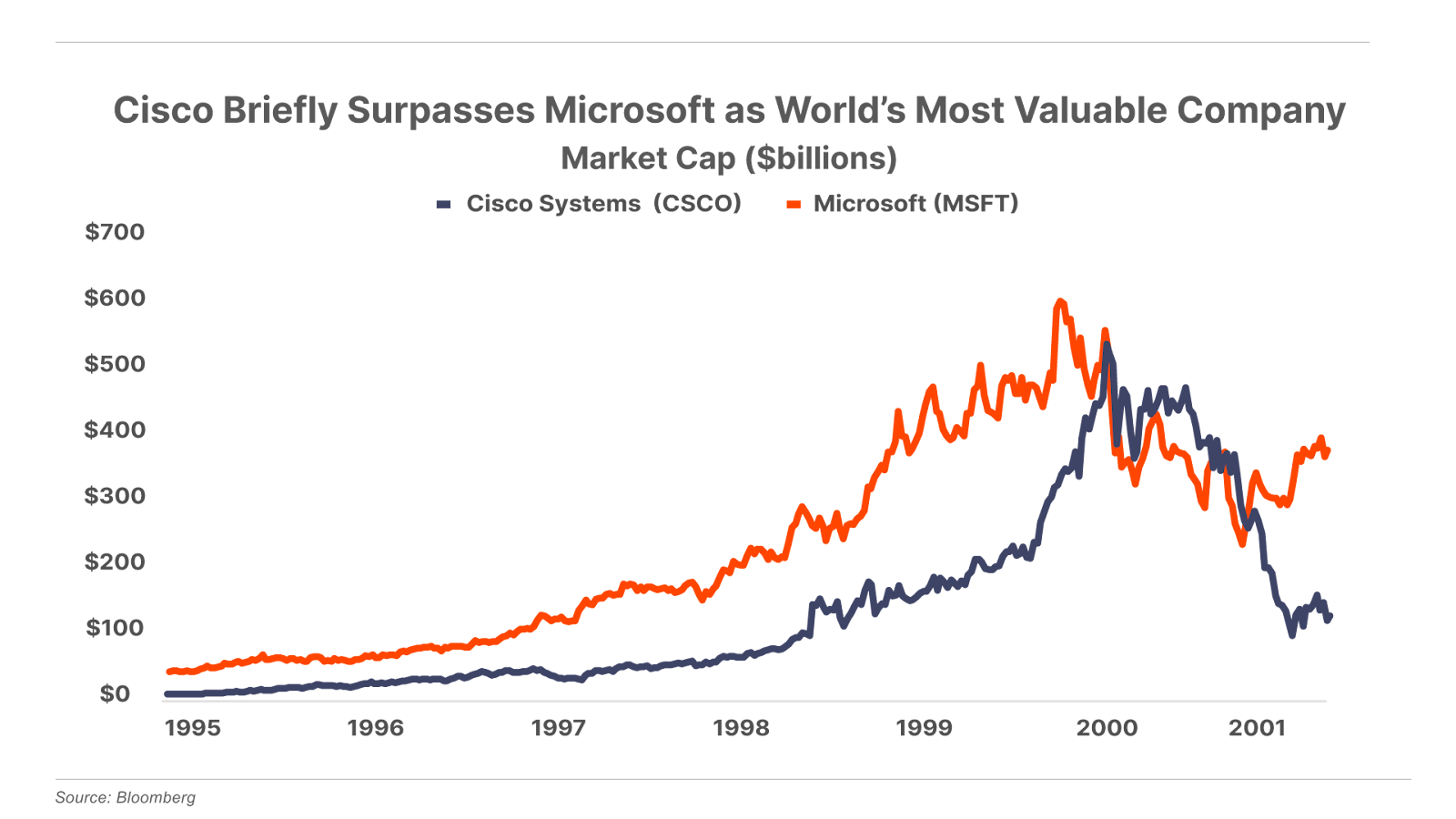

Cisco (CSCO) became arguably the most important company of the 1990s internet revolution. It was (and remains) the leading provider of networking hardware – routers and switches – that formed the physical backbone of the burgeoning internet.

The company that grew out of a Stanford University love affair ended up connecting lovers… and computers… and computer-lovers, all around the world. Following its initial public offering (“IPO”) in 1990, the stock averaged an impressive 100% annualized returns over the next 10 years.

By March 2000, CSCO shares had soared above $80 per share, making it the most valuable company in the world with a market cap of $570 billion – briefly surpassing the reigning leader, Microsoft (MSFT). And analysts began to predict that Cisco would become the world’s first trillion-dollar company.

Sadly, Sandy and Leonard’s story doesn’t have a Hollywood ending.

The IPO process brought in a flood of venture capital, along with activist-investor interference. Cisco got an ambitious new CEO who fired Sandy in 1990. Leonard soon left the company in solidarity. But, now that they weren’t bound together by the complex ethernet cables of Cisco, their marriage amicably unraveled. Today, they’re cordial exes who still share some investments.

Cisco’s happily-ever-after was short-lived as well…

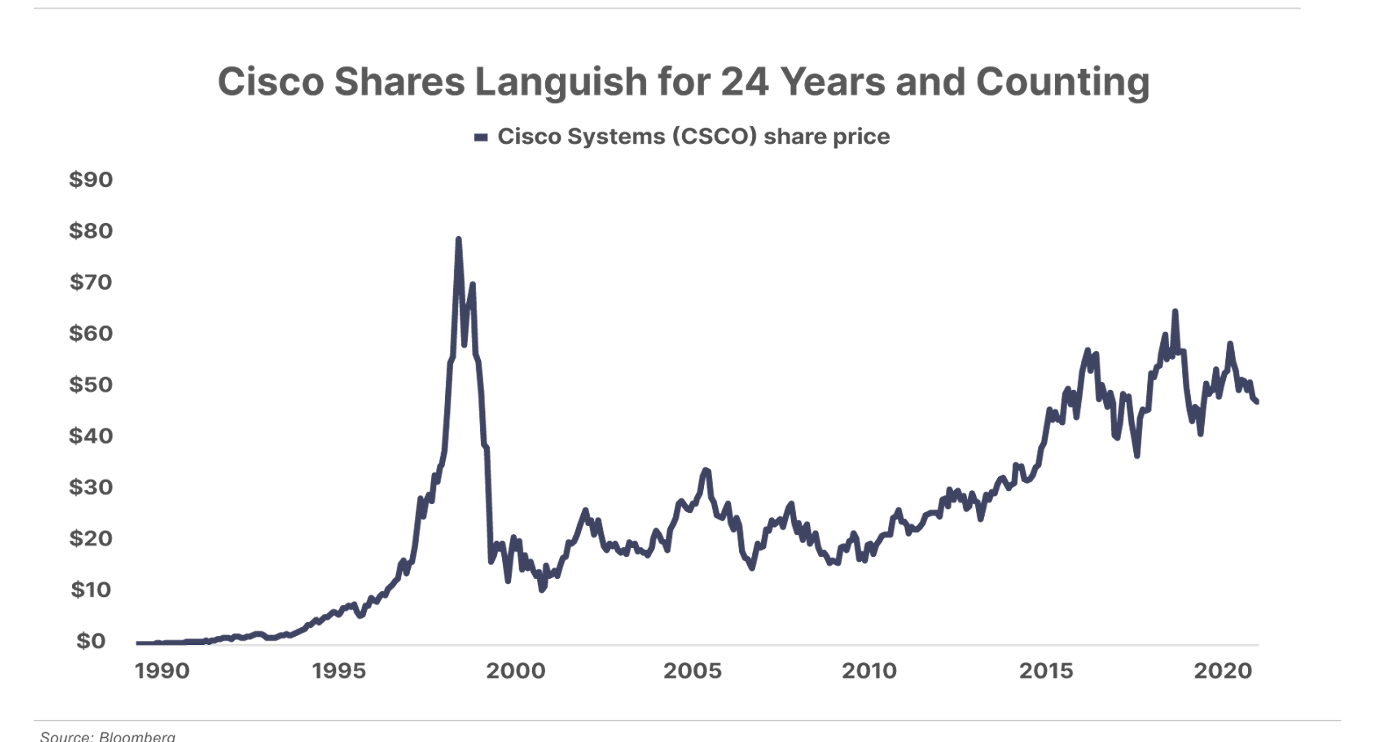

As it turned out, CSCO peaked that same month in March 2000 at $82 per share and plummeted as the dot-com bubble deflated. The shares bottomed nearly three years later at around $8, for a peak-to-trough decline of 90%. And today, more than 24 years later, they still haven’t returned to that dot-com record price.

Cisco’s dismal performance wasn’t caused by a dramatic reversal in its business. The only trigger was that the company’s revenue growth slowed from the strong 50%-plus average rate of the late 1990s to the high single-digit average rate of the following decades. Sometimes, a long relationship – or a long period of outperformance – ends not with a bang, but with a whimper.

Nvidia – whose performance we examined in the first part of our series on the Parallel-Processing Revolution – is an almost uncanny mirror image of Cisco in the 1990s. It’s so much like it, in fact, that Cisco’s former CEO, John Chambers, has recently gone on record protesting that Nvidia’s not like Cisco.

But the parallels are undeniable.

Nvidia has a chokehold on a vital piece of computing technology. Its powerful GPUs (graphics processing units) and proprietary CUDA (Compute Unified Device Architecture) platform are the modern-day equivalent of Cisco’s routers and switches. It’s been on an unstoppable growth streak, outperforming virtually every other asset on the planet over the past several years. And just this week, it (temporarily) passed Microsoft to clench the title of the world’s most valuable company, briefly sporting a market capitalization above $3.3 trillion.

Crucially, both companies – Cisco then, Nvidia now – have been riding the cresting wave of a massive, disruptive technological revolution. A picture that’s much bigger than any individual tech company… and, potentially, subject to an outsize correction.

The question is… when will the honeymoon period end?

Where We Are in the Revolution

Over the past two weeks, we’ve introduced readers to one of the most critical stories in the financial markets today: The Parallel-Processing Revolution.

This revolution will enable all kinds of incredible new technologies, such as generative computer learning (aka artificial intelligence or “AI”), self-driving cars, human-level machine interfaces, and advanced robotics… along with products and services we can’t even imagine today.

It will drive exponential growth in productivity and efficiency as computers become capable of thinking like and interacting with humans for the first time.

Most importantly, it will generate unfathomable wealth for savvy investors. The AI market alone is estimated to grow fivefold to $3 trillion by 2032. According to Nvidia CEO Jensen Huang, this revolution could ultimately transform every industry that relies on computing – which includes every major industry today – and create $100 trillion in total value.

Even under the most conservative assumptions, we believe this revolution represents one of the best opportunities to build life-changing wealth through the stock market in the decades ahead. But doing so won’t be easy. There will be tremendous volatility along the way, so to profit, investors will need to be disciplined and patient.

Here at Porter & Co., we’re committed to helping our readers successfully navigate the ups and downs of this world-changing shift.

Naturally, this entails identifying the lucrative long-term opportunities in the most important companies leading this revolution, as we have done in the past two weeks – and will continue to do going forward.

However, it also means highlighting the risks to help readers avoid or minimize the drawdowns that are certain to occur along the way. And that is precisely what we’re doing this week.

Shades of 1999

The similarities don’t end with Nvidia and Cisco. As we noted in the series introduction, this burgeoning revolution is likely to follow a similar path as the broader 1990s internet boom.

Then, as now, a handful of companies with transformative technologies were poised to change the world and create massive wealth in the process.

Many of those companies ultimately delivered on their promise to change the world. They built the foundation of the internet-connected world we take for granted today.

But even the most successful companies took longer to deliver on the promise of wealth creation than almost anyone would have imagined in the late 1990s… And any investor who bought in at that time would’ve suffered through years – or even decades – of disappointing returns.

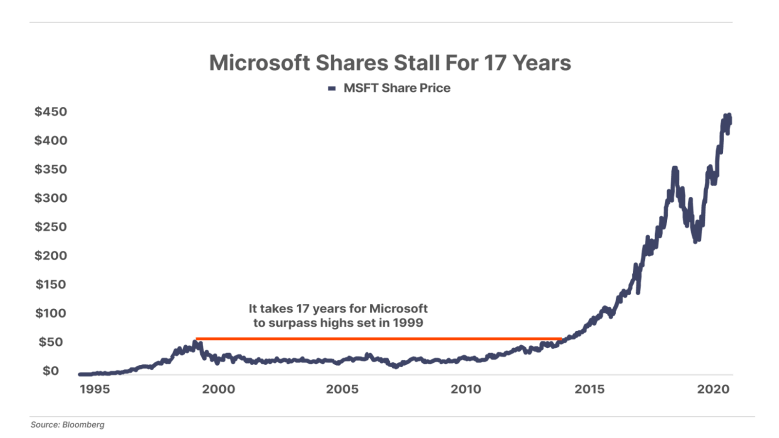

We previously shared the example of Microsoft – whose Windows operating system and Internet Explorer web browser played a pivotal role in the early growth of the World Wide Web.

Yet, even though Microsoft’s underlying business grew rapidly throughout the 2000s, its share price, as shown in the chart below, went nowhere for nearly 20 years after the initial mania ended.

Of course, Microsoft and Cisco were not alone. When the bubble burst, dozens of other would-be-dominant internet companies suffered massive price declines and years of dismal returns. For example:

- Amazon (AMZN) shares fell 95% following their dot-com peak and wouldn’t make a new all-time high for nearly 10 years

- eBay (EBAY) shares fell 80% and wouldn’t surpass their dot-com high for 12 years

- Priceline.com – now Booking Holdings (BKNG) – shares plunged 99% and didn’t return to their prior peak for 14 years

- Yahoo! (YHOO) shares lost 98% and were still trading roughly 75% below their prior highs when Verizon acquired the company in 2017 – nearly 18 years later

Countless other popular but less established companies – such as Webvan, Boo.com, Kozmo.com, and Pets.com – went bankrupt and never recovered at all.

History Rhymes, But It Doesn’t Repeat (Exactly)

However, while the current phase of the Parallel-Processing Revolution is reminiscent of the later innings of the dot-com mania, there is one notable difference so far: Nvidia and other key players are not as egregiously overvalued today as Cisco and many other internet stocks were back then.

Granted, Nvidia isn’t exactly cheap at its current trailing price-to-earnings ratio (P/E) of 76 (and forward P/E of 45). But it’s nowhere near Cisco’s insanely-high trailing P/E of 220 at the March 2000 peak.

It’s a similar story for other ancillary companies we’ve covered so far – ASML (ASML), at 55x trailing and 45x forward, and especially Taiwan Semiconductor Manufacturing (TSM), at 30x trailing and 24x forward.

Despite clear signs of exuberance, these facts suggest the Parallel-Processing Revolution is not yet a full-fledged bubble. That, in turn, suggests that these stocks could easily continue to move higher – and get significantly more expensive – for some time before the rally ends.

The Pins That Could Ultimately Pop the Bubble

Of course, there are no guarantees that these stocks will ever reach the same valuation extremes seen at the peak of the dot-com bubble. And plenty of significant risks could derail this rally before they do.

The most obvious is the recent pace of spending on AI and machine learning. According to The Wall Street Journal, Nvidia has sold $50 billion of GPUs since the AI boom began. However, the companies actually using those chips in AI applications have only generated $3 billion in revenue to date (to say nothing of actual profits).

This imbalance is unsustainable over the long term. Unless the firms using these chips can ramp up revenue significantly, it’s likely just a matter of time before the flood of capital into Nvidia chips begins to dry up. That would cause the remarkable revenue growth of Nvidia and these related companies to slow, and valuations would suddenly appear much higher than they are today.

Notably, this scenario doesn’t even include the potential for any economic slowdown.

In any recession, chip spending would slow dramatically as both big-tech companies and AI startups would retrench. And despite the economy’s remarkable apparent resilience over the past couple of years, there are plenty of triggers that could cause a recession…

- Banks are still sitting on massive unrealized losses in Treasury debt and commercial real estate that could trigger another round of failures like in the spring of 2023

- Consumers are at risk of pulling back on spending as stimulus-fueled COVID-era savings have officially run out – hurting consumer-facing businesses directly

- And Uncle Sam must refinance a record $10 trillion in debt over the next 12 months, even as the largest foreign holders of Treasuries have effectively stopped buying

Any one of these risks – or another black swan not currently on our radar – could set off a bear market in stocks… and the high-rising chip stocks feeding the current boom will not be immune. In fact, given their popularity and relative valuations, they could see greater relative downturns than most.

Of course, as we noted last week, the Parallel-Processing Revolution’s dependence on Taiwanese chipmakers also creates significant geopolitical risk. China instigating a war with its neighboring island nation could sap an estimated $10 trillion from the global economy – five times the $2 trillion in losses experienced during the Great Financial Crisis – and decimate the revolution in the near term.

Pounce at the Right Time, But Patience Is the Key

Given the risks of near-term downside in Nvidia and related stocks, the safest approach for most investors is simply to wait to buy them.

Sooner or later – we suspect within the next 12 months – these stocks will suffer a severe drawdown that brings valuations down to levels that will lead to tremendous long-term returns. That is when we’ll pounce, and recommend readers take substantial positions in NVDA, ASML, TSM, and the handful of additional companies we’ll discuss in the coming weeks.

That said, given the potential for these stocks to soar even higher before that inevitable drawdown begins, we understand that some readers may want to invest in this trend now – or continue to hold these stocks if they already own them.

If you’re among them, we urge you to use trailing stops to protect yourself. While these names have tremendous upside potential, there’s no telling how far they could fall – and how quickly – in a bear market.

Trailing stops will help lock in any existing gains. But more importantly, they will protect you from suffering a catastrophic loss of 50%… 70%… or 90%… and ensure you have capital available to take advantage of the generational buying opportunities that are likely to follow.

For those looking to jump in cautiously or remain in prudently, TradeStops is a great tool to help you with this.

Porter & Co.

Stevenson, MD