Issue #17, Volume #2

Why Do People Insist On Making Investing So Hard?

This is Porter & Co.’s free e-letter, the Daily Journal. Paid-up members can access their subscriber materials, including our latest recommendations and our “3 Best Buys” for our different portfolios, by going here. Recent issues of the Daily Journal are here.

For subscribers to Porter & Co.’s Distressed Investing, and Partner Pass members (including our new members!)… stay tuned for Marty Fridson’s latest recommendation, which will be released on Thursday at 4 pm ET. In the meantime, check out the Distressed Investing portfolio.

| Coca-Cola has been an extraordinary aggregator of wealth… $40 invested in 1919 has turned into $626,688… Buying businesses like this is a certain path to real wealth… Fed throws cold water on more cuts… Did you see what shares of insurer Mercury General did? |

Investors around the world should celebrate on May 8.

On that day in 1886, John Pemberton poured the very first Coke at Jacobs’ Pharmacy in Atlanta, Georgia. It cost 5¢.

And so began one of the greatest aggregations of wealth in human history.

Coke’s hyper-growth phase followed the introduction of its uniquely shaped bottle in 1915. A group of investors purchased the company for $25 million in 1919 and subsequently sold 400,000 shares to the public at $40 each. Coke’s business was so well known and appreciated by investors that upon its New York Stock Exchange listing (September 5, 1919), the brokers assigned it the symbol KO. The company was a knockout.

There has never been a more powerful consumer brand or product that is more beloved. Coke’s advertising in the 1930s, featuring Haddon Sundblom’s paintings of Santa, is responsible for most of the world’s Santa iconography.

Coke is the second most universally recognized word in the entire world, second only to OK.

Coke’s balance sheet today shows total assets of around $100 billion and total liabilities of around $75 billion, meaning that it rests on $25 billion worth of equity. And on that equity, Coke earns an incredible $15 billion, before taxes, interest expenses, etc. After these costs, it’s producing more than a 40% return on equity, year after year.

Those results produce stupendous amounts of wealth over time.

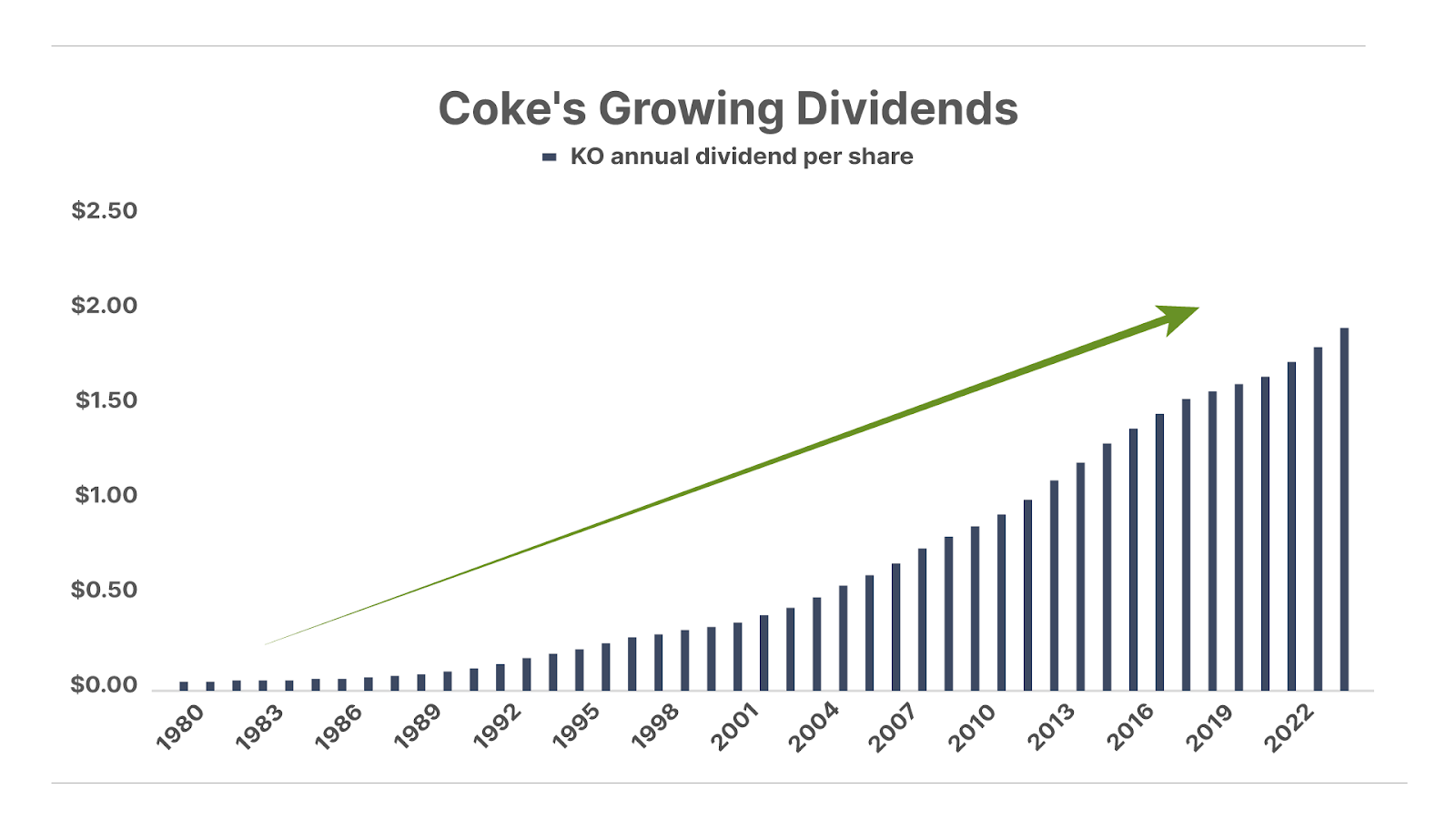

Coke’s stock has been split 11 times in its history, meaning that one share purchased in 1919 for $40 has become 9,216 shares today. With the stock trading around $68, that $40 has turned into $626,688 – or more than 15,000 times the initial investment in a little over 100 years.

But that only tells a small part of the story.

To understand the full picture, you need to understand that Coke has increased its dividends, virtually every year, since 1919. Specifically, Coke has increased its dividend every year for the last 62 years.

Just since 2010, Coke has returned almost $85 billion to investors, or 56% of its market capitalization in that year.

Owning Coke is like having a 20-year reverse mortgage, except, even after the house has been paid for, the disbursements continue to increase. Every. Single. Year.

Investing doesn’t have to be hard. We decide to make it hard… because buying small caps and tech stocks and trying to figure out which turnaround situation will double our money makes us feel like we’re doing something valuable. But the most valuable thing to do as an investor is nothing.

When I try to explain why this kind of investing is impossible to beat (over time, Coke’s incredible 40% annual returns on equity will produce unbeatable results for its owners) many of my subscribers complain that they are too old to take advantage of these kinds of opportunities.

But that’s not true.

Warren Buffett was 58 years old when he finished buying 400 million shares of Coke in 1988.

Buffett invested $1.299 billion, making Coke his largest-ever nominal investment (by far) at the time. The position was equal to 21% of Berkshire Hathaway’s equity, making Coke one of the largest investments Buffett has ever made on a relative basis, too.

Since 1989 – the first full year that Berkshire owned its entire Coke position – it has received a total of $9.6 billion in dividend income. And, of course, those payouts continue to grow.

Last year, Berkshire received $776 million in dividend income from Coke, which represents a 59.7% annual yield on Berkshire’s initial investment.

There’s simply no way to beat these results, over time.

Making these investments isn’t hard to do. It’s not hard to figure out which businesses can produce outsized returns on equity and that are virtually certain to continue doing so for many more decades. I’ve written a lot about Hershey (HSY) for the same reasons. And Philip Morris International (PM). And American Express (AXP). And McDonald’s (MCD). And Domino’s Pizza (DPZ). And NVR (NVR). And many others.

Here’s the biggest tell: If McDonald’s raised the price of a Quarter Pounder by 10%, would you notice? Or if the grocery store lifted the price of a two-liter of Diet Coke by 10%, would you buy a different brand? Or if Hershey increases the price of chocolate by 10%, will you stop buying it? Or what about if American Express increases its fees, would you even notice?

Most consumers wouldn’t notice.

Consumer brands with global distribution and beloved brands have incredible pricing power. They can continue to increase their prices, year after year. And, since they don’t have to create a new product every year, they can funnel all of those increases to sales and profits back to their shareholders.

Coke’s latest quarterly report shows it only grew unit volume by 1% last year. That doesn’t sound good, does it? But revenues were up 12% because of price increases, and the additional scale saw operating income grow 16% for the entire year.

What an absolute monster of a business.

Buying these businesses isn’t hard. Holding them isn’t hard. And there’s no more certain path to real wealth – wealth that will continue to grow, year after year after year after year.

Horse, meet water.

(Coke is typical of a Forever Stock: Companies in our Big Secret on Wall Street portfolio with a long history of outstanding management, performance, and innovation that investors should plan on holding forever. These businesses have a long-term record of delivering fantastic returns, thanks to a wide moat, a high return on capital, and a history of treating shareholders well. But when is the best time to buy these market-beating stocks, to ensure the best long-term returns? This is a major focus of The Big Secret… To learn more about The Big Secret, go here, or contact Lance James, our Director of Customer Care, at 888-610-8895, internationally at +1 443-815-4447, or via email at [email protected].)

Three Things To Know Before We Go…

1. Powell throws cold water on further rate cuts. In his semiannual testimony before Congress this week, Federal Reserve Chair Jerome Powell reiterated that the central bank is in wait-and-see mode. He noted that the economy is currently in “a pretty good place,” and said that he sees no reason to be “in a hurry” to cut rates – unless the job market weakens significantly or until inflation moves closer to the Fed’s 2% target. And right now (see below), neither appears imminent.

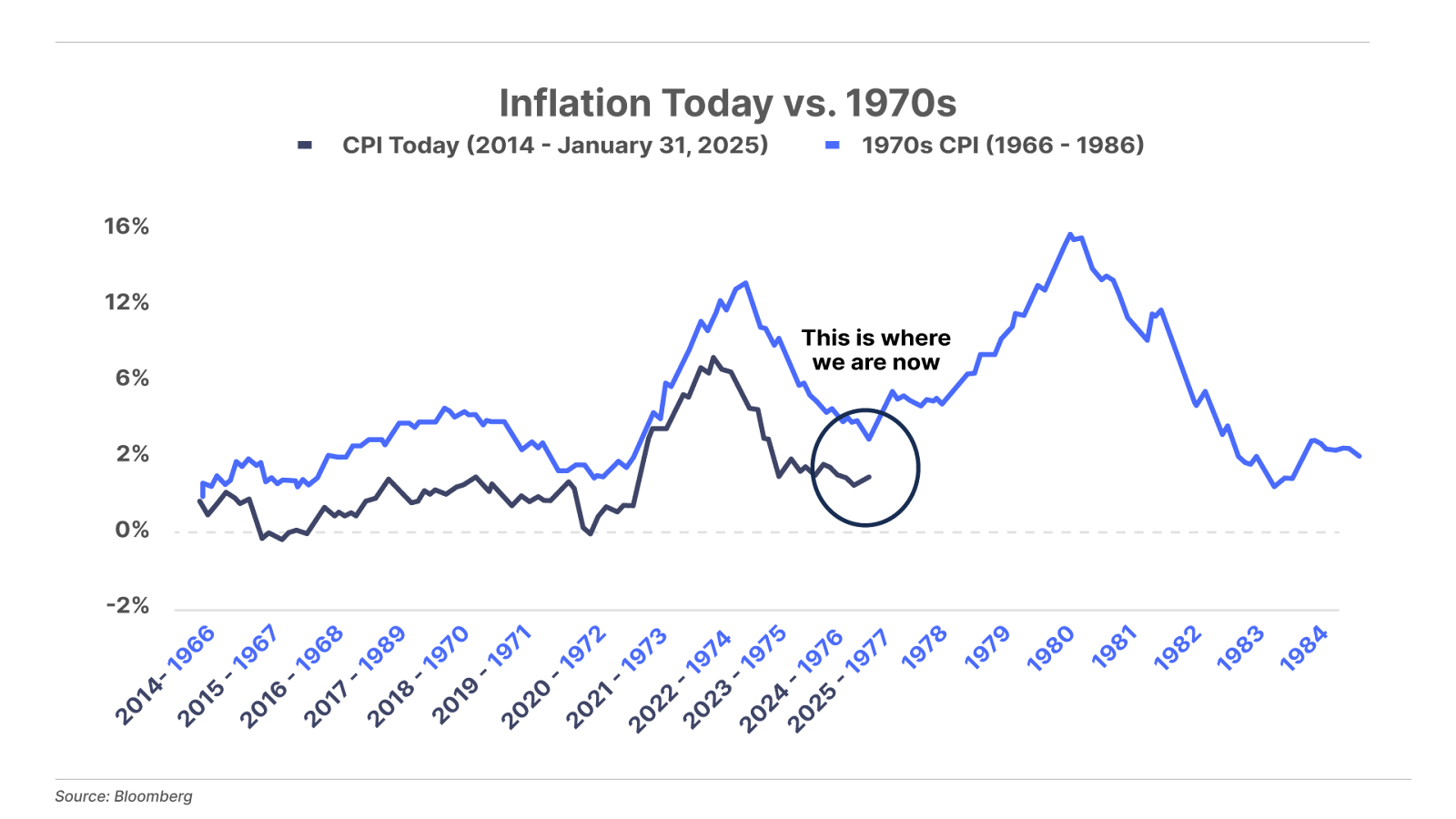

2. Inflation is moving the wrong way. This morning, the Bureau of Labor Statistics reported that the consumer price index (CPI) rose 0.5% in January, representing an annual inflation rate of 3.0%. Wall Street economists had expected a rise of 0.3%, or 2.9% annualized. Given Powell’s comments above – and the eerily similar path of inflation today versus the 1970s – it’s looking increasingly likely that the Fed’s rate-cutting cycle may already be finished.

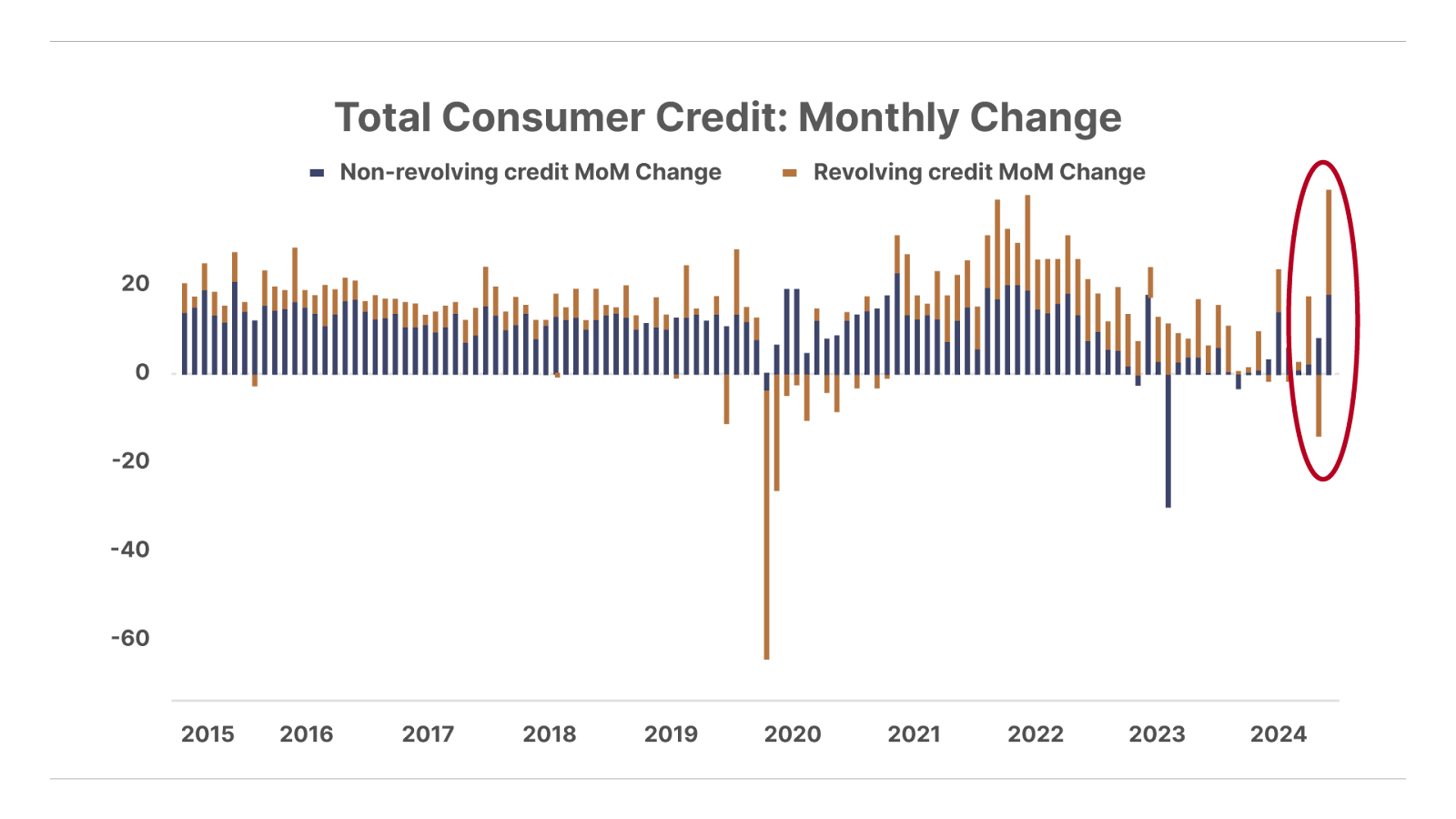

3. Consumer credit soars as Americans struggle to keep up with inflation. As inflation runs hot, more Americans are relying on debt to get through life. Total consumer debt surged by a record $40.8 billion in December, contributing to a $950 billion increase over the past five years. This brought total consumer debt to over $5 trillion. Financial pressure on households continues to escalate (and meanwhile, job openings are falling… and rents are falling …)… when will they finally reach their limit?

And one more thing… Did You Listen?

On January 22, Porter wrote about property & casualty insurance stocks – pointing out how these companies are going to be less affected by the California wildfires than most investors might think. Porter also suggested that the shares of insurer Mercury General (MCY) — which had fallen 25% in the week after the L.A. wildfires started, due to concerns over the company’s exposure – “might be a great opportunity over the next year” due to the market’s overreaction.

And sure enough… yesterday, Mercury reported a stronger-than-expected quarter, and its shares are up 17% as of 2 pm ET today from when Porter commented on them three weeks ago.

Poll Results… Will Philip Morris (PM) Outperform The S&P 500?

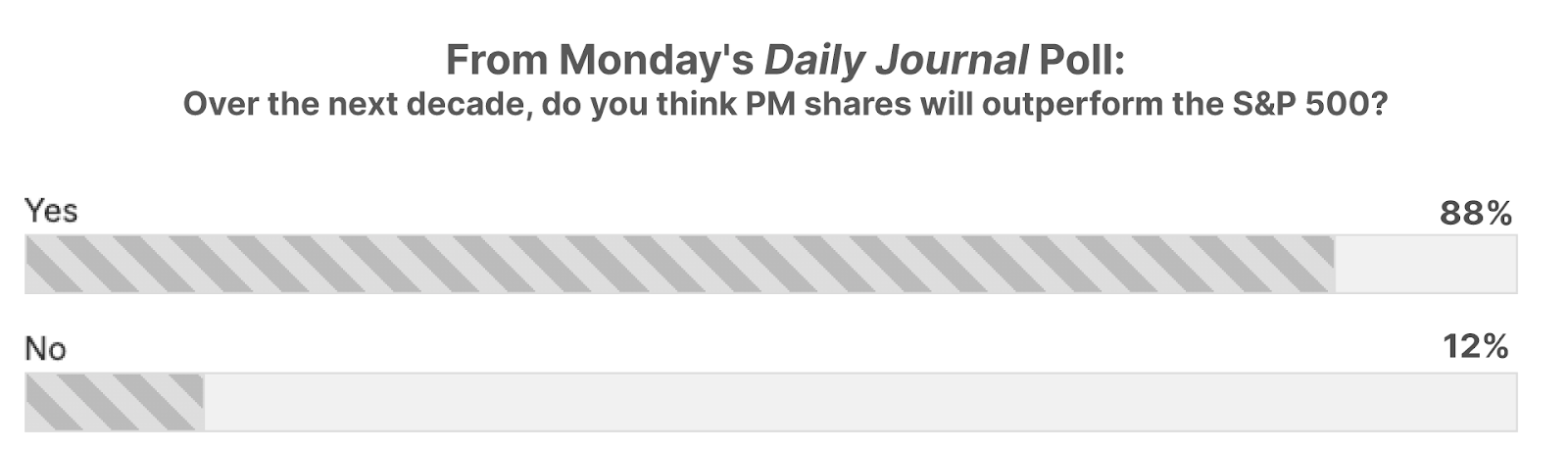

In Monday’s Daily Journal, Porter replied to a reader’s question about the seemingly high level of debt that Philip Morris (PM) carries, by explaining the difference between good debt that helps drive brand value (like Philip Morris has) – and bad debt that drags down performance. Pointing to PM shares’ 79% return since 2021, we asked readers if they thought Philip Morris would continue to outperform the S&P 500 over the next decade. And… 88% of survey takers feel that PM shares will indeed outperform the S&P over the next 10 years.

Good investing,

Porter Stansberry

Hudson Yards, New York City

As always, let me know what you think… good or bad, at [email protected]

P.S. Yesterday, we had an email problem… that dozens and dozens of our subscribers noticed.

Gary M. wrote, “The links in your email this morning entitled Trump’s Biggest Deal do not work.” Johannes H. said, “I am trying to read ‘Trump’s best deal ever,’ but when I try to read it, it states it is not available. Can you help?” Ron C. emailed us to say about Trump’s Biggest Deal, “This will not open on either my iPhone, desktop computer, nor my laptop. Please resend.” In reference to the rogue link, Gary G. wrote, “Error says ‘This page isn’t working.’”

And… we’re sorry.

In the spectrum of mistakes that we make… sending readers a link that doesn’t work ranks right up there – just below – recommending a stock that winds up in our Hall of Shame. (It’s happened just twice… which is two times too many. If you’re a Big Secret subscriber, you probably know what we’re talking about.)

So… just to be sure that everyone who got an error message on the link we sent… we’re posting it here – please click here.

This one works… promise.

And just to be sure… click here for the correct link.