Issue #27, Volume #2

In Distressed Investing, There Is A Magical Pattern

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| The master of high-yield bonds shares his methodology for picking stocks… Bonds rise first, and then a company’s shares follow… Combined shares and bonds pack a more powerful punch… Today’s poll – tariffs and the market, which way will stocks go?… |

Over the past week, Porter has been talking about how buying distressed bonds is providing him with a Second Life… and, more broadly, about how bonds are the investment world’s best-kept secret. They offer (if you buy the right ones) a high level of security… fantastic returns… and significantly less volatility than stocks. What are you waiting for?

And of course… which distressed bonds you buy matters a lot. Marty Fridson, the lead analyst for Porter & Co.’s Distressed Investing, is a pioneer of the entire asset class… Investor’s Digest called him “the most well-known figure in the high-yield world.” Marty joined Porter & Co. in March 2023. Since then he’s made 17 distressed-bond recommendations, which are up 16.4%.

However: Marty also has an impressive track record recommending stocks (in fact… he’s written an entire book – one of the seven books he’s written – about investing in stocks, 2023’s The Little Book Of Picking Top Stocks). And for the Distressed Investing portfolio, Marty has recommended six stocks, which (including closed positions) are up 39.4%, resulting in an average total portfolio return of 22.4%.

Today, Marty takes us under the hood of the Distressed Investing advisory, to see how he and his team find distressed equities – and he explains how the behavior of a company’s bond is often a precursor to how the same company’s shares behave.

Here’s Marty…

Distressed Investing’s primary focus is bonds, because that’s where the best low-risk, high-return opportunities exist.

But we also recommend distressed common stocks – because their behavioral relationship with their company’s bonds can combine to provide a boost to the overall return. These recommendations come about in two ways.

1. A Combined Position Sometimes we recommend a package of a distressed bond and the issuing company’s stock. Simultaneously investing in both is a way to get the benefits of the bond’s superior downside protection and the stock’s greater upside potential. This strategy maximizes the risk-adjusted expected return on the proposition.

In one case we recommended investing $1,000 for each combination of a bond, then trading around $800, plus shares of the company’s stock. Since then, investors who acted on this recommendation have earned 6% current income on the bond portion, and enjoyed a 10% gain on its price. The icing on the cake has been a 15% gain in the price of the shares… for a total combined return of 15.9% over 10 months.

2. Topping It Off Other distressed-stock recommendations arise from our “topping up” strategy – as in, getting a coffee refill at a diner. We implement it when one of our distressed-bond recommendations works out profitably, but the equity markets have not appreciated the company’s improved performance – so the share price has not risen along with the bond price.

By taking a profit on the bond and subsequently investing the proceeds in the stock, the investor can cash in a second time, thus topping off the initial investment.

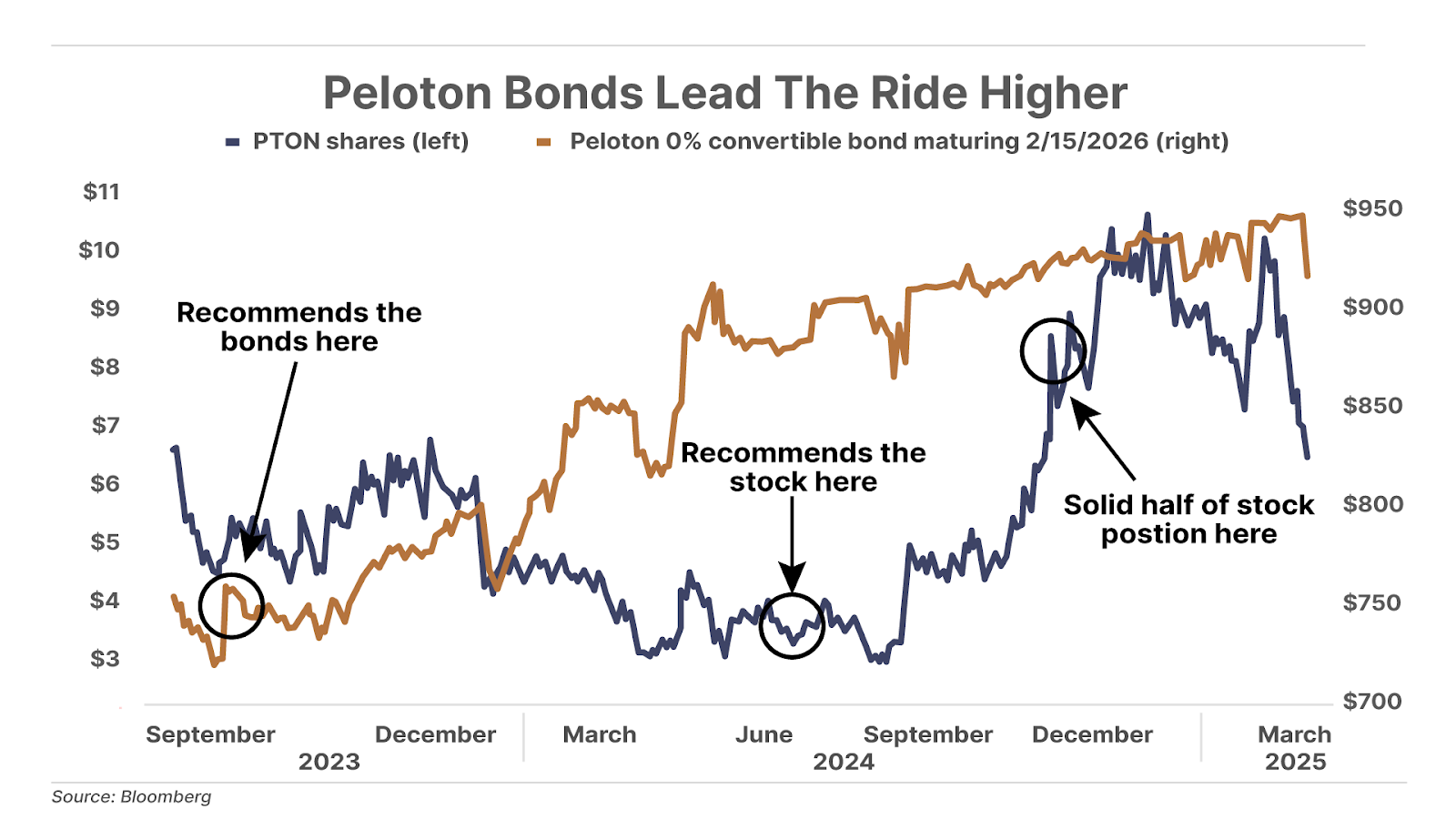

We’ve followed this topping-off method three times in our Distressed Investing portfolio – the most notable example being Peloton Interactive (Nasdaq: PTON). We recommended the company’s 0% convertible bond in October 2023. As the company began to return to profitability – as we anticipated – the bond rose too, and is now up 27% in those 17 months. Then, a year and a half after selecting Peloton’s bond, in June 2024, we recommended PTON shares, which have since soared 113%, earning a position on our Porter & Co. Top 10 list (we sold half of the equity position from the portfolio in November, to book a 124% gain).

Why Bonds Move First

The equity opportunity becomes available because the bond market (and bond investors) usually pick up faster than the stock market (and stock investors) on changes in a company’s financial health. By their nature, bond investors pay closer attention to shifts in balance sheet data – and the ability to cover interest charges – than equity investors do. Bondholders are less concerned with earnings-per-share (“EPS”) growth that may increase the company’s share price than they are about the risk that a cash flow shortfall will lead to a default on required interest payments.

In fact, from the bondholders’ standpoint, it’s a positive development if a company sells more shares – which dilutes stockholders’ ownership and reduces EPS. By raising more equity, the company enlarges the cushion between solvency and bankruptcy – providing more cash to pay off the debt.

The bond market’s quicker response to changes in a company’s trajectory is evident in both directions – when financial distress intensifies, as well as when a crisis passes. Consider, for example, the 2008-2009 Global Financial Crisis. The risk premium on high-yield bonds, defined as the yield premium over default-risk-free U.S. Treasuries, began rising in May 2007. At that point, the stock market wasn’t picking up any hint of the coming disaster. The S&P 500 didn’t begin to sell off until seven months later, in December 2007.

A year later, in December 2008, the high-yield bond risk premium began to fall, signaling an improving economy. But it wasn’t until March 2009 that the stock market got the memo, when the major indexes began to rise off the bottom.

We see the same pattern with individual companies. After the bonds have fully reflected the emergence from distress, the stock price’s improvement lags – shares typically require months to show upward price adjustment that aligns with the improved conditions.

There’s one more reason why bondholders lose no time in taking action when the earliest signs of distress appear. Once there are strains in the financial system, trading liquidity vanishes from the over-the-counter corporate bond market. Experienced bond investors sell while they still can. After that, it becomes more difficult to find a buyer, and prices fall even more.

It’s very different in the stock market. With equities, it’s much more liquid – there are always investors prepared to take the other side of a sell order, even though the bid may be down a lot from the last trade.

To be clear, a recovering bond does not always lead the appreciation of a company’s share price. Very often, it doesn’t. There are two words that we follow to identify attractive opportunities in distressed stocks – “pattern recognition.”

Looking For Financial Characteristics

I’ve seen many distressed situations in my decades researching high-yield bonds. The ones that worked out favorably for investors had certain financial characteristics. When we see those same characteristics in a newly distressed company, we get very interested.

The desirable pattern involves such things as the velocity of cash flow… seeing if it’s on a gentle downslope or if it’s fallen off a cliff. A downward trajectory is not always a bad thing. Maybe the company had a terrible year for unusual reasons that aren’t likely to be repeated.

For example, a leading motion-picture exhibitor was rebounding from the COVID-19 pandemic’s devastation of movie audiences when it hit a speed bump: A strike by screenwriters and actors delayed the production of films scheduled for release in 2024 – potentially sucking the lifeblood from the business. The company had fewer new movies to show, and its revenue suffered. But we knew the company had strong management that played its cards right. The setback was temporary as the strike was settled and the pipeline of releases resumed.

Another key factor is what’s happening with the company’s liquidity. It’s important to see if the company has enough cash, or assets that can quickly be converted to cash, to carry it through a rough period on the operating front.

Naturally, spotting a positive pattern of this sort doesn’t mark the end of the process. We have to dig into the company’s products – to see if demand for them is holding up – and into its marketing and research and development, to ensure that there is a steady pipeline for future sales.

We also need to be confident that management has the necessary experience to get the company through a stressful period. Have the top executives demonstrated a record of good decision-making? And it’s imperative to have employees with the right skills at all levels in the organization.

One more requirement is to avoid overconfidence and getting wed to a recommendation. Whenever a company gets into distressed circumstances, there’s a danger that things can go from bad to worse in a way that’s impossible to foresee. Even a company that fits the desired pattern perfectly can fall prey to unexpected changes in industry fundamentals or competitive conditions.

As analysts we have to say the most likely outcome is Scenario A, in which investors win big, but there’s also a low-probability Scenario B, where the stock declines even more. If Scenario B materializes, we don’t let our egos get involved. That’s just the way things work out sometimes and the right move is to take your loss and move on. The goal is to have more winners than losers, not to win every time.

Accordingly, we’re especially mindful of these risks when considering an equity recommendation, where the downside is less protected than it is with the debt. And once we do select a stock, when necessary we’re quicker to switch to a Sell than we are with a bond, advising investors to cut their losses.

But as our record demonstrates, our ability to recognize the patterns associated with success in distressed investing should give Porter & Co. subscribers confidence that profits on our winners will far offset the cost of an occasional distressed investment that doesn’t live up to our expectations.

Since I became senior analyst for Distressed Investing two years ago this month, following the strategies outlined above have worked out very well for the portfolio. We have recommended 17 bonds – we’ve closed seven positions for a total return of 16.5% – with five of the seven in the green. The 10 remaining bonds show a total return of 16.3% – with all but one showing a gain since we recommended them… As far as the stock side of the portfolio, things look strong there as well. We have made six recommendations, which as of March 6 have a total return of 39.4% – with four well into positive territory. Overall, the Distressed Investing portfolio is up 22.4%.

Next week, Marty and his team will be recommending shares of a company based on the “topping off” strategy. This company’s bonds have jumped 23% since being added to the portfolio a bit more than a year ago. Now, Marty sees the opportunity for the shares to rise as well… We will release that report on Thursday, March 13… If you’re not already a subscriber to Distressed Investing, see what we’re talking about here, or call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.

Three Things To Know Before We Go…

1. Another weak jobs report. This morning, the Bureau of Labor Statistics reported that U.S. employers added 151,000 jobs in February, below Wall Street expectations of 170,000 but above the 125,000 added in January. The unemployment rate also ticked higher to 4.1%, from 4.0% the prior month. While we could see more weakness in jobs ahead due to spending cuts and tariff uncertainty, for now, there is still little employment-driven reason for the Federal Reserve to reconsider its pause in interest rate cuts.

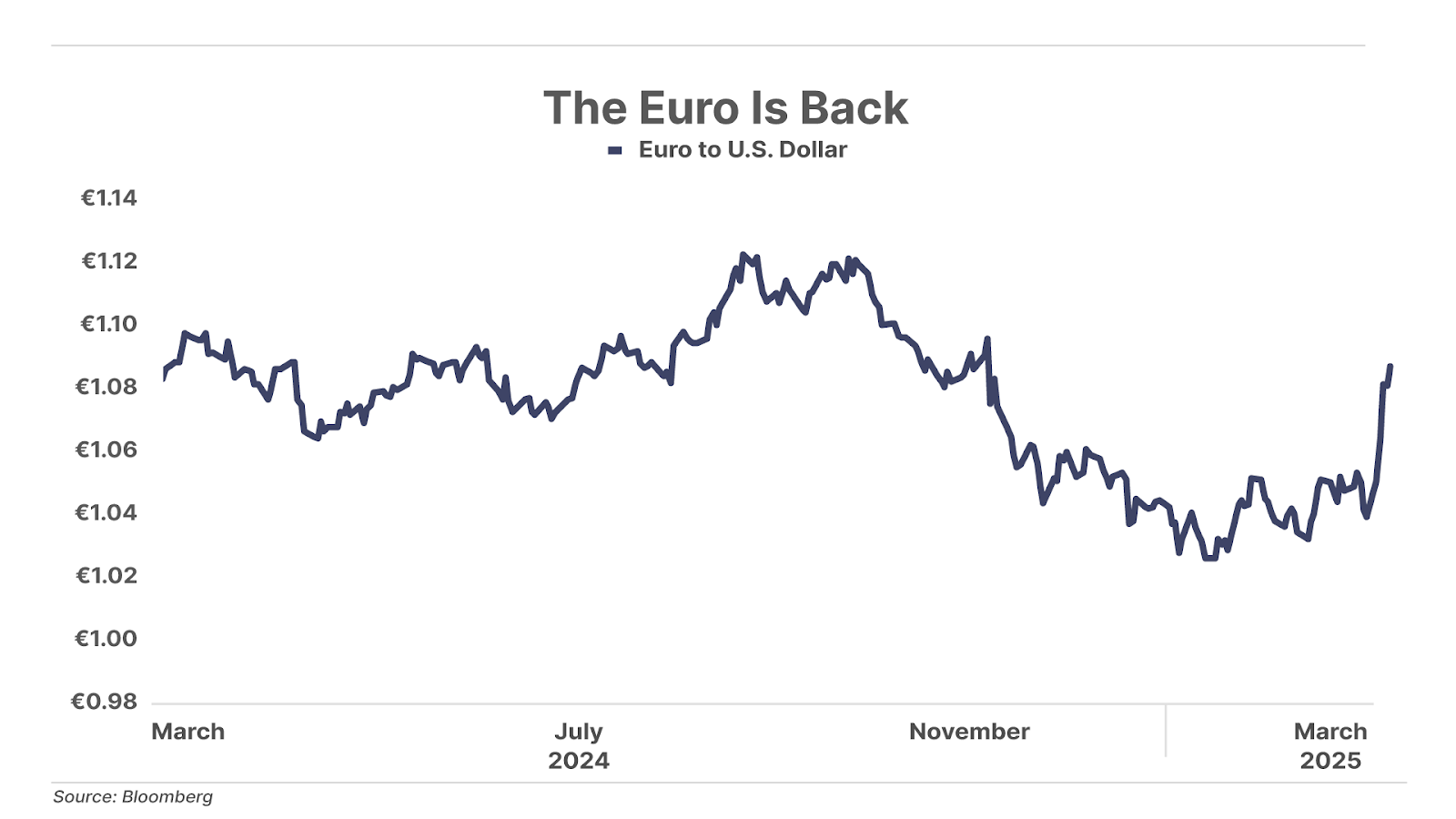

2. The euro is back. The European currency had its strongest week in 16 years, moving up 4.6%, to completely recover its post-U.S. election declines. The news this week of Germany’s historic stimulus – as it opens the purse strings for massive defense and infrastructure spending – bolstered the currency… and meanwhile, escalating concerns about the impact of tariff policies on the U.S. economy – and the dollar – benefitted the euro. The euro has strengthened despite a growing interest rate disparity with the dollar, as the European Central Bank cut rates again yesterday, to 2.5% – compared to 4.5% in the U.S. (current expectations are for rates to stay the same when the Federal Reserve meets next on March 18-19).

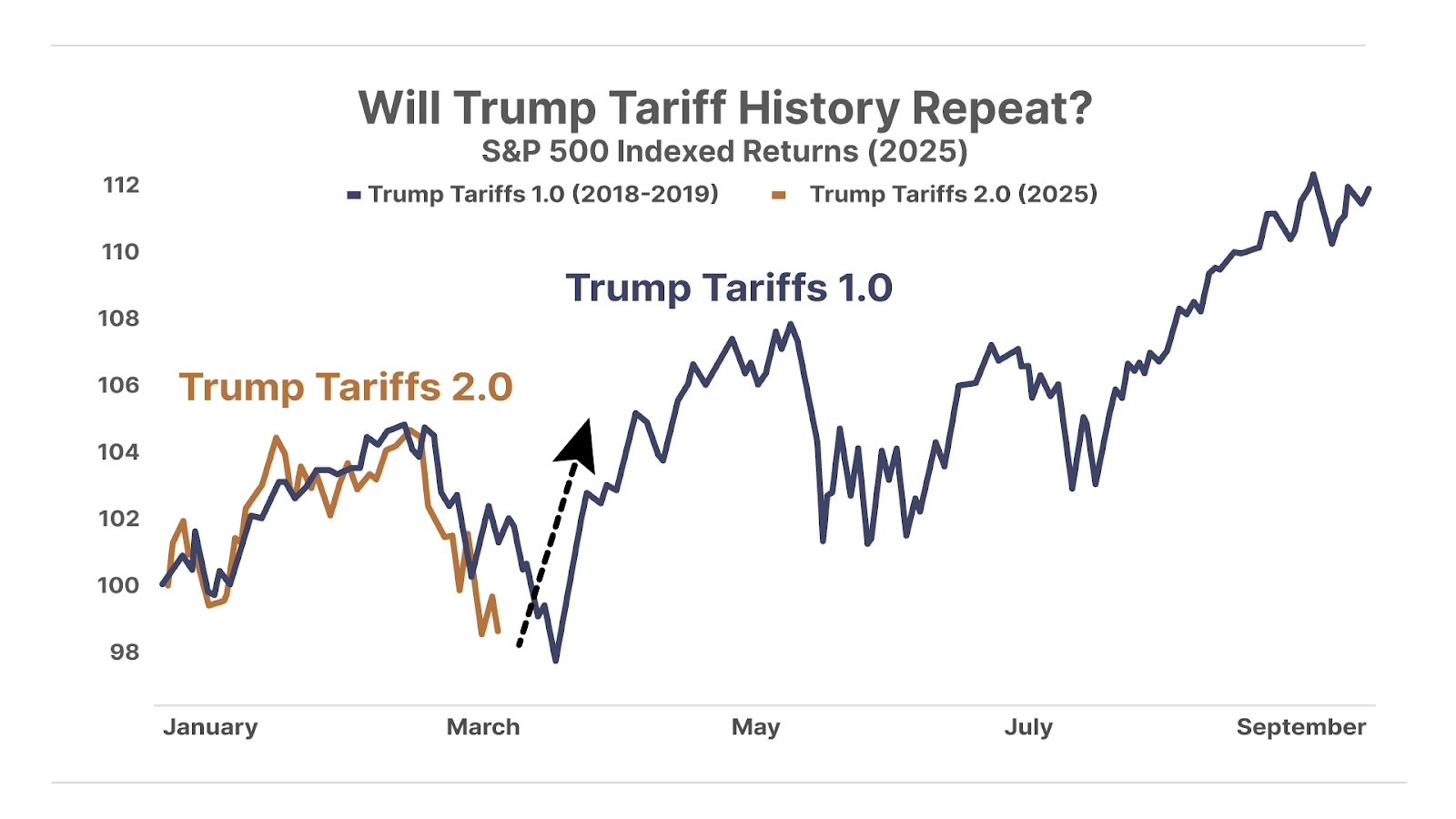

3. Trump delays tariffs on Mexico and Canada. Yesterday, President Donald Trump postponed 25% tariffs on selected imports from Canada and Mexico for another month. The delay only applies to products covered by the free trade treaty between both countries and the U.S. – leaving 62% of Canadian imports and half of Mexican imports facing the 25% tariffs that took effect on March 4. While the Trump tariffs have dragged down the U.S. stock market, how markets reacted to tariffs during Trump’s first administration suggests that stocks could recover soon (see graph below).

Reader Poll… How Tariffs Play Out In The Market

And One More Thing… The Bitcoin Reserve Disappoints Crypto Bulls

Last night, President Trump signed an executive order (“EO”) to establish a strategic Bitcoin reserve that will be funded by the Bitcoin the U.S. already owns – so it won’t cost U.S. taxpayers anything. The government owns 200,000 ($17.5 billion) Bitcoin seized as part of legal proceedings. The EO also establishes a U.S. Digital Asset Stockpile for other cryptos like Ethereum and Solana, but it mandates that the U.S. government only purchase Bitcoin through budget-neutral strategies. The market reacted negatively, sending Bitcoin down 4% to around $85,000. However, we view this move as bullish in the long term, as it could boost global confidence in Bitcoin and encourage other nations to follow suit.

Porter Stansberry

Stevenson, MD

P.S. As we discussed in yesterday’s The Big Secret On Wall Street, gold is a key component of Porter’s Permanent Portfolio… and should be part of every investor’s portfolio, too.

Usually, investors view gold as insurance: Against inflation, the inevitable crumbling of value of fiat currency, and uncertainty. For thousands of years, gold has been a store of value – though the rest of the economy may crumble, gold holds steady.

And gold has often – completely divorced from that dimension of its appeal – been a fantastic investment, as well. Over the past year, gold is up 36%… compared to the S&P 500’s 12%.

There’s another way to invest in gold, of course: but gold mining companies are infamously poor investments – they incinerate capital and deliver terrible long-term returns.

… EXCEPT for those that don’t… in which case, they can be life-changing investments

Long-time Porter friend Marin Katusa (Porter has also invested in some of Marin’s resources projects) is one of the world’s top experts on gold.

And he thinks gold is just getting started… and: He has ideas about how to invest in it.