Hershey is a powerful real-life example of my signature capital efficient investing approach. And it’s now approaching an attractive valuation for the first time in years.

A Classic “No-Risk” Investment Approaches a Buy Point

There’s no sugarcoating it…

It was one of the worst times in history to buy stocks.

It was late November 2007, and unbeknownst to most, we were just months away from the start of the worst financial crisis since the Great Depression.

My team and I – at my previous firm – had already issued dire warnings to readers about the coming collapse in housing, and the devastating impact it could have on the economy and the stock market.

Yet, despite those risks, I made one of the boldest recommendations of my career that month.

In an issue titled “Our Best No-Risk Opportunity Ever,” I practically begged readers to buy shares of beloved chocolate maker The Hershey Company (NYSE: HSY).

In fact, I predicted the stock would ultimately become the single best recommendation of my career – offering investors the rare chance to earn market-beating returns of 15% or more annually, for decades, with virtually no risk:

“This stock could easily become the best investment you make in your entire life.

“No matter what happens, it’s extremely unlikely that you’ll lose money in this stock, assuming you hold it for any reasonable (three to five years) length of time.”

– Stansberry’s Investment Advisory, November 2007

Unfortunately, in the 18 months following that recommendation, many of my worst fears also came to pass.

Contagion from the subprime mortgage market permeated the economy. Home prices crashed. Unemployment soared above 10%. Countless banks, mortgage lenders, and other firms went bankrupt – including, most notably, government-sponsored agencies Fannie Mae and Freddie Mac and “blue chip” automaker General Motors (GM) – just as I predicted they would. And the broad market indexes plunged more than 50%… and didn’t return to their pre-crisis highs for nearly six years.

Those prescient warnings earned me notoriety as one of the few analysts who correctly foresaw the crisis. But looking back today, I’m actually far prouder of my Hershey recommendation than of my warnings about Fannie Mae, Freddie Mac, and GM.

You see, despite all the turmoil of the Great Financial Crisis – and all the unprecedented events we’ve witnessed in the global economy and markets since – Hershey has delivered on my bold claims.

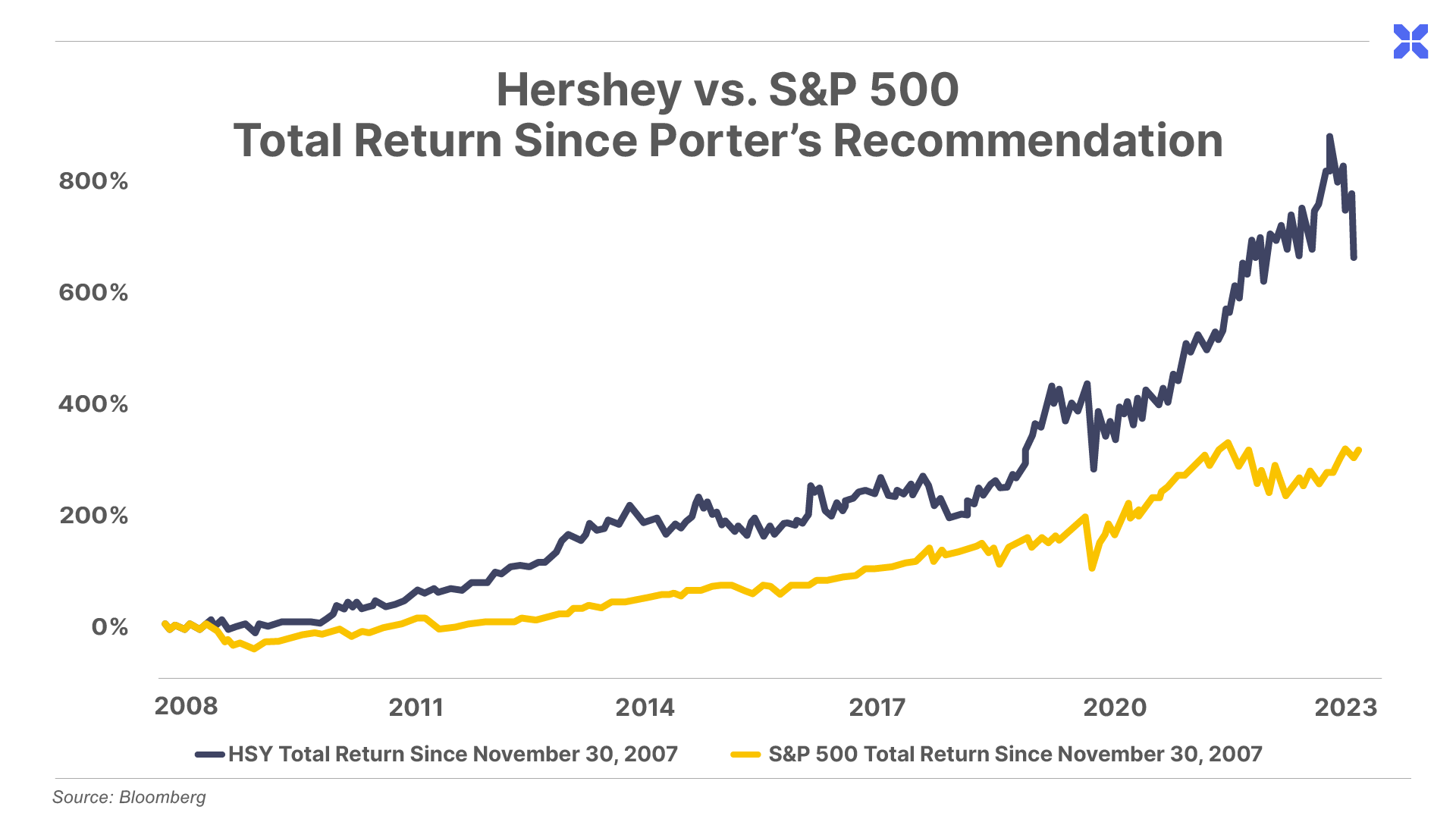

Between November 30, 2007, and May 1 of this year, HSY had generated a total return of 901% – more than three times the S&P 500’s return of 284% over that time. That represents a 16.1% compound annual return over 16 years, versus 9.4% for the S&P 500.

HSY shares have pulled back sharply over the past few months, as the company has tempered near-term growth expectations following a series of inflation-related price hikes.

However, even including this recent decline, the stock has delivered total returns of nearly 700% (13.8% annualized) to date. And I have no doubt it will continue to compound investors’ capital at the same mid- to high-double-digit rate for years to come.

How I Knew Hershey Was a “No Risk” Investment

The reasons I was so confident recommending Hershey in 2007 – in spite of the terrible macroeconomic outlook – are as simple as they are profound:

- Hershey is a remarkably “capital efficient” business.

- It was trading at a reasonable price.

If you’re new to Porter & Co., you may not yet be familiar with “capital efficiency.”

This term refers to the fact that not all profits are created equal. In short, when a business earns money, there are two primary places those earnings can go:

- Profits can go back into the business to be spent on “capital expenditures” (i.e., replacing or upgrading the business’ fixed assets including buildings, vehicles, machinery, land, etc.), or…

- Profits can go back to the business’ owners (i.e., returned to shareholders). Shareholder returns can come directly from dividend payments, or indirectly through share repurchases – when the business buys back its own shares in the open market. The latter reduces the total number of shares outstanding, thereby increasing the ownership stake of remaining shares.

You can think of capital efficiency as the ability of a company to convert its profits into shareholder returns, rather than having to sink them back into the business.

Of course, all businesses must reinvest some portion of their profits toward capital spending, as part of the inevitable replacement or upgrading of plant and equipment, among other requirements.

But the most attractive companies are those that have minimal capital requirements – that are capital efficient – which maximizes the amount of cash that can flow back into the pockets of shareholders.

While this idea should be relatively easy to grasp, capital efficiency remains one of the least understood concepts in finance – even among Wall Street professionals. But it’s been at the heart of our investment approach at Porter & Co. since the beginning. As I explained way back in that same 2007 issue…

“This is only common sense. If a company is able to return more of what it makes every year to its shareholders, then the compound return of its stock will be much, much higher over time than the returns of another business that grows its sales and profits at a similar rate but reinvests all that it earns back into its business.

“There’s no great wisdom in this conclusion: It’s simply a matter of basic math. And yet this concept is utterly beyond the scope of almost every individual investor. I have never seen it mentioned in a single Wall Street report, either.”

– Stansberry’s Investment Advisory, November 2007

Not coincidentally, capital efficiency is also the “secret” behind legendary investor Warren Buffett’s investment success…

“This idea – the importance of corporate capital efficiency – is the key to understanding Warren Buffett’s success as an investor. He never mentions the words “capital efficiency.” Instead, he talks about the importance of returns on net tangible assets and the value of economic goodwill. Don’t let the accounting language distract you: Both concepts are measures of capital efficiency…

“I have come to believe evaluating capital efficiency gives us a permanent edge in the market, as almost everyone else ignores this crucial variable… Few people even understand the concept.”

– Stansberry’s Investment Advisory, November 2007

Relatively few companies in the world actually meet this lofty standard. But when you find one that does, it’s like discovering an untapped gold mine. Some well-known examples include Coca-Cola and American Express, both of which Buffett has owned for decades.

Buffett describes these kinds of companies as “Inevitables.” We also refer to them as “forever stocks.”

These are companies that have such valuable brands and such timeless business models that it is hard to conceive of an environment where their businesses would underperform the S&P 500.

They are economic juggernauts that do not face extinction because of technological change or the constant fluctuations of the world’s economy. They are as close to a “sure thing” as exists in the financial world.

Hershey certainly fits the bill.

The company has been around since 1894, and owns a portfolio of some of the most iconic candy brands of all time, including Hershey’s, Hershey’s Kisses, Reese’s, Kit Kat, Twizzlers, Almond Joy, and Jolly Ranchers.

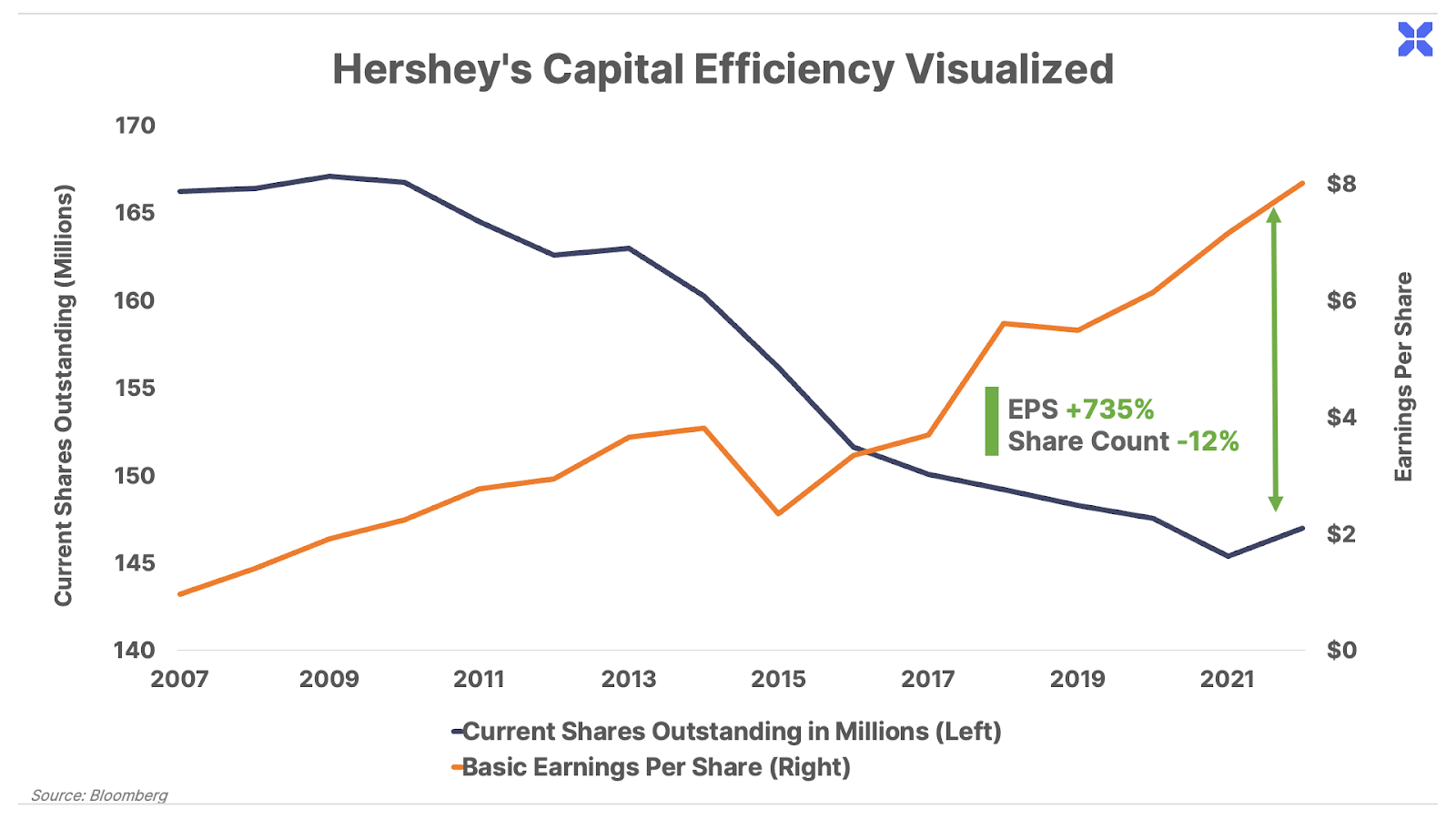

And it has for decades slowly but consistently grown revenues, earned thick profit margins, and returned a substantial (and growing) share of profits to shareholders – through both dividends and share buybacks.

My investment thesis back in late 2007 was straightforward. Hershey had dominated its market for generations, and I saw no reason it wouldn’t continue to do so for the foreseeable future – regardless of what happened in the market or the economy.

That’s exactly what happened. And in hindsight, it was a “no-brainer.”

However, identifying an Inevitable like Hershey is only half the battle. The second reason I recommended the stock had to do with valuation.

How I Knew It Was the Right Time to Buy Hershey

Valuation is simply the price you pay to buy a share of a business, and it plays a huge role in the potential returns you’re likely to earn from any investment.

The reality is even the highest-quality, capital-efficient business is likely to be a terrible investment if you pay too much for it. The key to success is waiting to buy these stocks when – and only when – they trade at a reasonable price.

What’s a reasonable price?

The best definition of “reasonable” is when you can buy a company at a price that constitutes an objective “margin of safety.” Ben Graham invented the concept in his famous book, Securities Analysis. (You can also learn about this concept in the much easier to read The Intelligent Investor. See chapters 8 and 20.)

A margin of safety exists in common stocks when the price is low enough that, at least hypothetically, the company could finance the repurchase of all of its outstanding shares and bonds – what’s known as the company’s “enterprise value.”

Today, Hershey’s enterprise value is $47 billion. That’s down from a peak enterprise value of $60 billion. Obviously the value of Hershey’s outstanding obligations (about $5 billion) doesn’t change very much. The decrease in the enterprise value is almost entirely a function of its falling stock price.

Hershey reliably generates $2 billion a year in cash. When investment grade corporate debt was yielding virtually nothing back in 2021, you could argue that Hershey could have easily financed borrowing $50 billion. But, today, the effective AAA corporate yield is 5%. That means the absolute maximum that Hershey could hypothetically borrow would be $40 billion.

Please understand, I’m not suggesting that would ever happen. It’s merely a yardstick by which you can figure out a sensible relationship between what a company is earning and what it’s worth. Buying below this price doesn’t mean there’s “no risk” – it means there’s an objective margin of safety in the stock.

And the theory behind the measure of safety is fascinating. Investors generally have two choices when they want exposure to a corporation. They can either buy equity (the stock) or debt (the bonds). Equity is a lot more risky, because if a company defaults on its debts, the equity holders get wiped out and the company’s assets are used to repay the bond holders.

What Ben Graham figured out was, if the company can afford to buy back all of its stock and all of its bonds, then there was no real additional equity risk. If you bought high quality businesses at the right price, owning stocks wasn’t in fact any riskier than buying bonds. Buying at the right price allows you to have the upside of stocks, without the risk. That’s the whole point to having a “margin of safety.”

Keep in mind, this isn’t about trying to time the bottom in the market or in the stock price. That’s not necessary for excellent results. It’s far more important to realize: opportunities to buy great businesses at good prices are rare.

Another “No-Risk” Opportunity Is Approaching

I don’t bring up my Hershey recommendation simply to brag about my track record (believe it or not).

Rather, it’s a powerful real-life example of the capital-efficient-focused approach I discovered nearly 20 years ago, and that we continue to follow here at Porter & Co. today.

This approach is the surest, safest, easiest, and least stressful way to build real, life-changing wealth in the stock market.

Over the years, it’s offered my readers the opportunity to make incredible long-term returns – like 1,189% in Home Depot, 1,213% in Apple, 1,250% in NVR, 1,728% in Microsoft, and 4,014% in NVIDIA.

And as I’ve shown you today, it works even if you buy these stocks at the worst possible time for the overall market.

At Porter & Co., we believe the ideal investment portfolio would be constructed primarily from these businesses, as they are among the highest quality and offer the longest “runway” of any possible investment.

We urge subscribers to buy these businesses aggressively when they can be acquired at reasonable prices – and to never sell these positions. Over time you should aim to see this portion of your portfolio grow relative to all others.

To help our subscribers do just that, last year we created a list of our favorite Inevitables we’d most like to own. We’ve updated this list for all Big Secret readers below.

Astute readers will notice a handful of companies on this list – including Hershey – are approaching valuations where we would begin to get interested again.

Look at the P/E ratio chart of Hershey’s stock over the last 15 years. Hershey was trading at a reasonable price when we first recommended it, back in late 2007. And then during the Great Financial Crisis (2009). And then… briefly… in 2019. In total, over 15 years, there were probably about six to eight months during which buying Hershey was, without question, one of the best investments you could make.

Today Hershey is trading around 20x earnings. If the stock falls by about another 20% it will have an objective margin of safety. Historically, that’s been the case with Hershey at or below 17 times earnings. And I’d bet that will remain the case for a long time.

Hopefully the recession that we’ve been expecting arrives later this year. I suspect it will be a very severe recession and I expect most stocks will fall 50% or more.

Why? I think there are going to be very serious problems in the banking system, as inflation proves harder to eliminate than most people think, pushing interest rates higher and holding them higher for longer. This will cause a lot of defaults in commercial lending. And, in fact, this is already happening.

Commercial bank lending has already declined by 1.63% from its all-time high. This is only the 4th time in the last 50 years that commercial lending has declined by 1.5% or more. The other three times were ’75, ’01, and ’09. And in each of these cases, the S&P 500 fell more than 50%.

Why would I say “hopefully” this happens? Recessions and collapsing stock prices are what every rational investor hopes to see. These are prime opportunities to buy the very best businesses with a substantial margin of safety.

As always, our paid-up subscribers can count on us to tell them exactly when these opportunities arrive. If you’d like to join them, click here to learn more.

Porter Stansberry

Porter & Co.

Stevenson, MD

P.S. If you’d like to learn more about the Porter & Co. team – all of whom are real humans, and many of whom have Twitter accounts – you can get acquainted with us here. You can follow me (Porter) on Twitter here: @porterstansb.