Issue #90, Volume #2

There Is No Sure Thing In Investing

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| When a closed-end fund trades at a discount… No easy money… Unless you’re a high-powered financial operator… “The one essential indicator” usually is not… Was Trump right to fire the BLS commissioner?… |

Editor’s note: Today, Porter turns the Journal over to Distressed Investing senior analyst Marty Fridson.

Marty has a long background in trading, investing, and finance… Over a 25-year span with Wall Street firms including Salomon Brothers, Morgan Stanley, and Merrill Lynch, he became known for his innovative work in credit analysis and investment strategy.

In today’s Journal, Marty warns readers about being sucked into investments that seem like a sure thing… like a closed-end fund trading at a huge discount to its net asset value.

Marty takes it from here…

“This one’s a no-brainer.”

When talking about investment ideas, this phrase refers to someone who has no brain as opposed to an idea that’s an obvious winner.

Like people who assume that when a closed-end fund (“CEF”) is priced at a discount to its net asset value (“NAV”) – the value of the fund’s assets minus the value of its liabilities – it’s some kind of an anomaly that points to easy money.

There’s no such thing as a sure thing in investing… Let me explain.

Like its cousin the open-end mutual fund, a closed-end fund owns an underlying portfolio of stocks, bonds, or some other instrument. The difference is this: When you buy or sell a share of an open-end fund, the transaction price always equals the market value per share of the underlying portfolio. In contrast, CEF shares can trade at a discount or a premium to its NAV.

The opportunity to purchase CEF shares for less than the value of the assets they represent sounds like free money. But there’s a catch. You can’t swap your CEF shares for a basket of the assets they represent, sell the basket, and pocket the difference.

Unless, that is, you’re a high-powered financial operator who can acquire a huge block of a CEF’s shares, engineer a liquidation of the underlying portfolio, and distribute the proceeds to the shareholders – including himself.

This kind of activist investing coup happens once in a while, but don’t count on a windfall like that in choosing a CEF to buy. The price may very well remain below NAV.

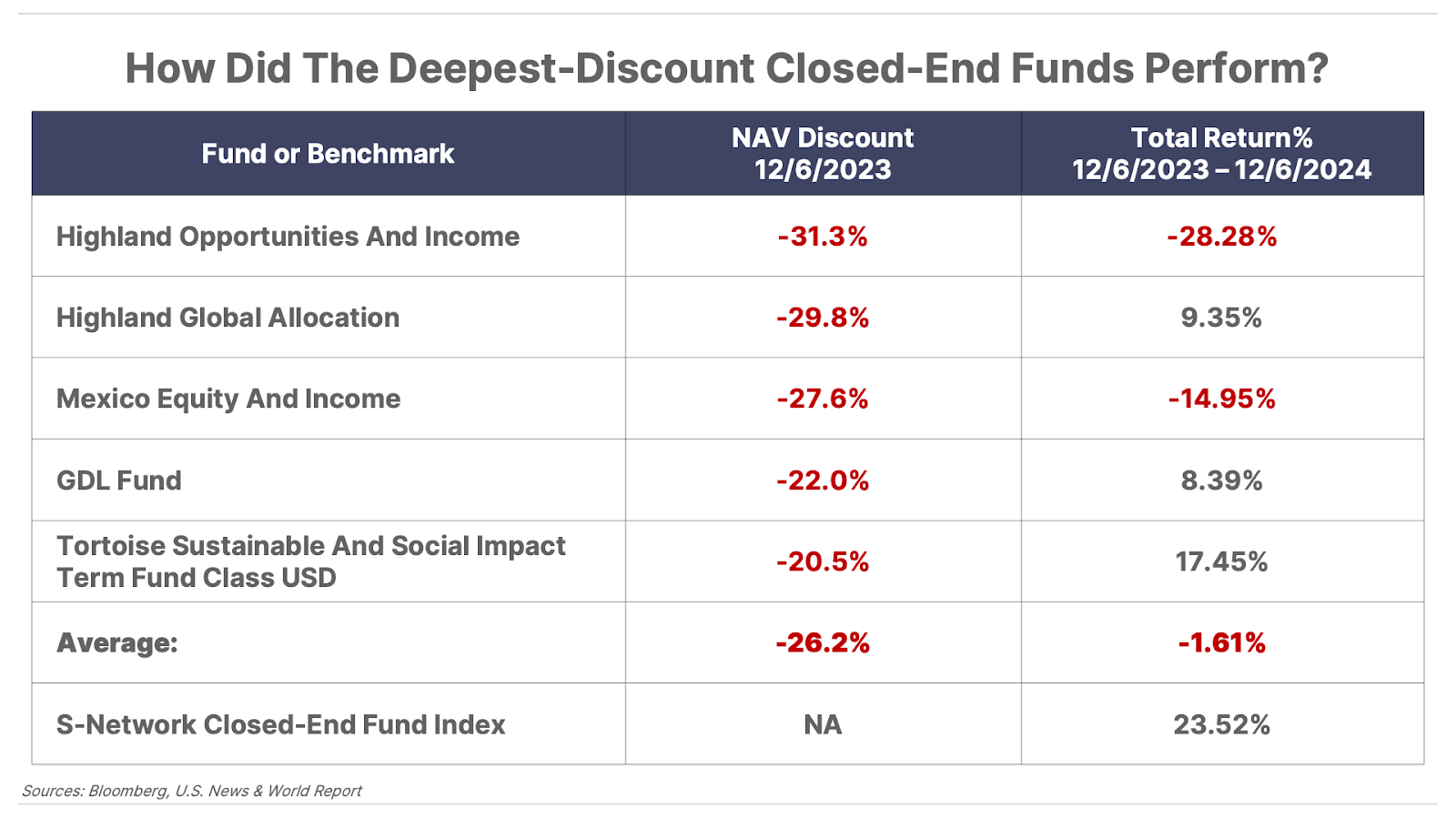

Consider Highland Opportunities And Income Fund (HFRO). At the end of Q2 2024, it was drastically discounted, at 51.55% below its NAV. Did investors wake up, realize the shares were a steal, and boost the price to the “correct” level?

No, they did not.

Highland Opportunities finished Q2 2025 in an even deeper hole, 56.08% below its NAV. Total return for the 12-month period was negative 9.26%, compared with positive 13.17% for the benchmark S-Network Composite Closed-End Index.

Rather than constituting an anomaly, a discount to NAV often represents a rational judgment by the market if management has consistently subtracted value and there’s no compelling reason to suspect it’s about to change. There are certainly cases of CEFs falling to deep discounts and then going on to deliver spectacular returns. The point is just that a price below the value of the underlying assets is only one factor to consider in determining whether you’ve found an honest-to-goodness bargain.

In December 2023, U.S. News & World Report published “5 Funds Trading At The Biggest Discounts To NAV,” which talked about how “pricing inefficiencies” in CEFs allow “savvy and risk-tolerant investors to lock in a potential bargain.” I was curious to find out how those seemingly mouthwatering opportunities had worked out.

Not so well, it turns out.

Over the next 12 months, all five of the touted funds underperformed the CEF index. Two had double-digit negative returns, dragging the group’s average into the red. Highland Opportunities And Income, which as we saw fared badly in the most recent four quarters, was the worst of the bunch.

On the one hand, ignoring CEFs altogether would be taking the wrong message from all this. But on the other hand, this little income secret is not all it’s cracked up to be either. With their typically high yields, they can be excellent vehicles for investors interested primarily in generating current income. Sometimes you wind up with a hefty capital gain on top of that. But spotting the best picks requires more than looking at what an enthusiast called “one essential indicator: the discount to net asset value.”

Comparing a CEF’s price to its NAV is a form of value investing. Distressed investing – in both bonds and stocks – is likewise premised on buying a security for less than it’s truly worth. Without the proper research and experience, it’s easy to look at a deeply discounted stock or bond and see a massive upside potential. But more often than not, they are value traps – cheap stocks that stay cheap… or get even cheaper… and bonds priced way below face value that in many cases stay that way. Closed-end fund buyers face the same potential pitfall.

Searching for value can pay off, but an indispensable rule of investing is to consider incentives. If you buy a discounted CEF, then watch it become even more discounted until you offload it to some other bargain hunter, the company that operates the CEF continues to collect its management fee on the same number of outstanding shares. In Distressed Investing specifically, and Porter & Co. in general, we aim to give readers the advice we would want if the roles were reversed… We focus on how wealth is safely built, how it’s protected, and how ordinary folks can achieve true financial independence… So far, our record is pretty good.

If you’re not already a subscriber to Distressed Investing, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on becoming a subscriber.

Is The World’s Greatest Investor

About To Shock Wall Street?

In just a few weeks, a move decades in the making could be revealed – and when it is, it could ignite the next great gold rush. Savvy insiders are quietly positioning now… before Warren Buffett makes it official. Garrett Goggin has already pinpointed four tiny gold miners that could 100x once the announcement hits. It’s the perfect moment to be greedy – before the herd wakes up.

Get Garrett’s top four gold picks now – before the world’s greatest investor pulls the trigger.

Three Things To Know Before We Go…

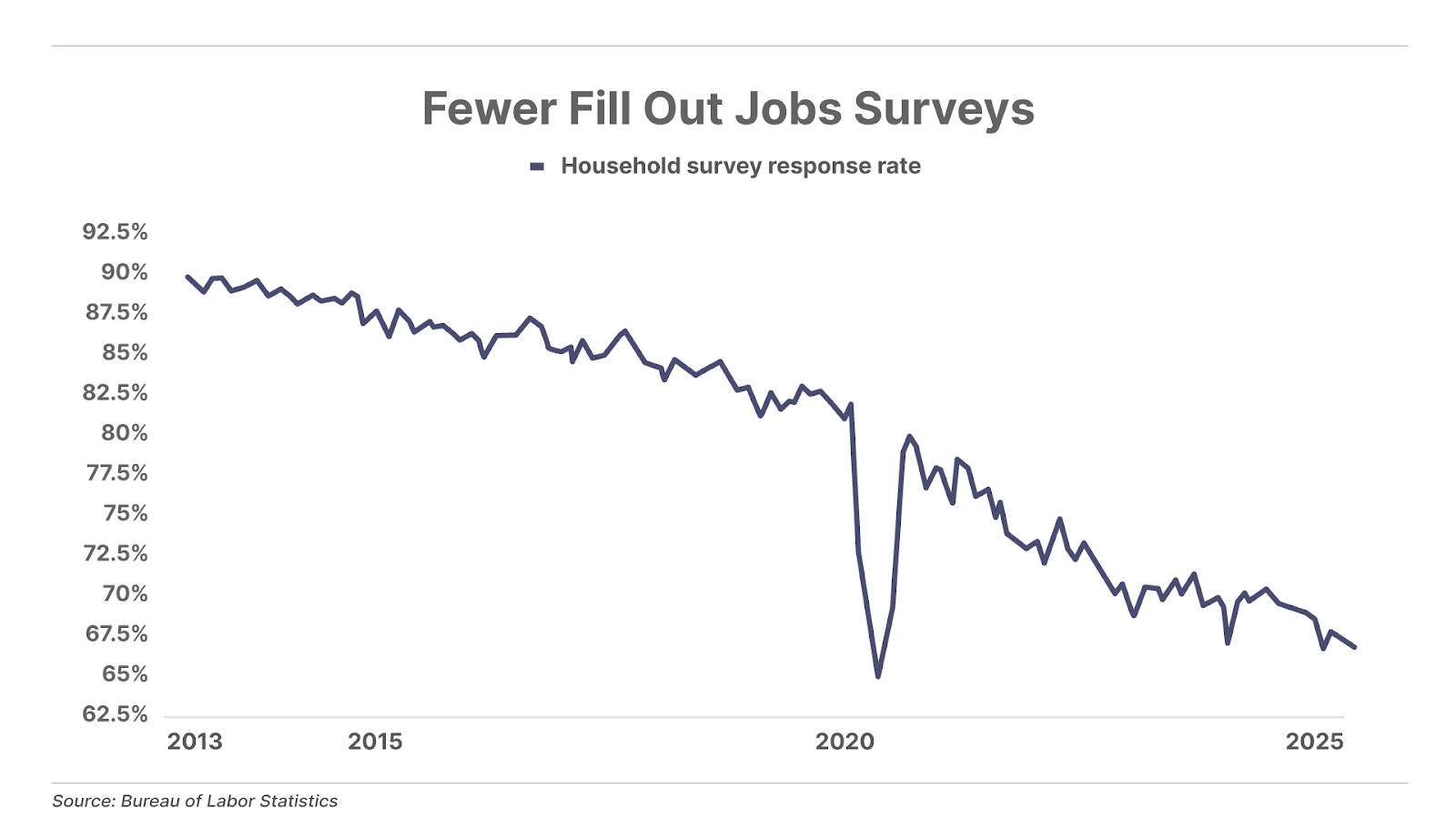

1. Was Trump right to fire the BLS commissioner? On Monday we noted that President Donald Trump had fired the head of the Bureau of Labor Statistics (“BLS”), alleging that the agency has been “rigging” employment data to hurt his administration. While we disagree with Trump’s premise – the BLS has routinely revised employment data for years under both Democrat and Republican presidents – the bureau was arguably in need of a shake up. As the chart below shows, the BLS has seen the response rate to its household survey – upon which its monthly jobs report is based – plummet from above 90% to just 67% over the past 12 years. With such an incomplete data set – and BLS’ inability to boost the response rate – it’s no wonder these initial reports have become so useless. (Our “Mailbag” below contains readers’ views on the firing.)

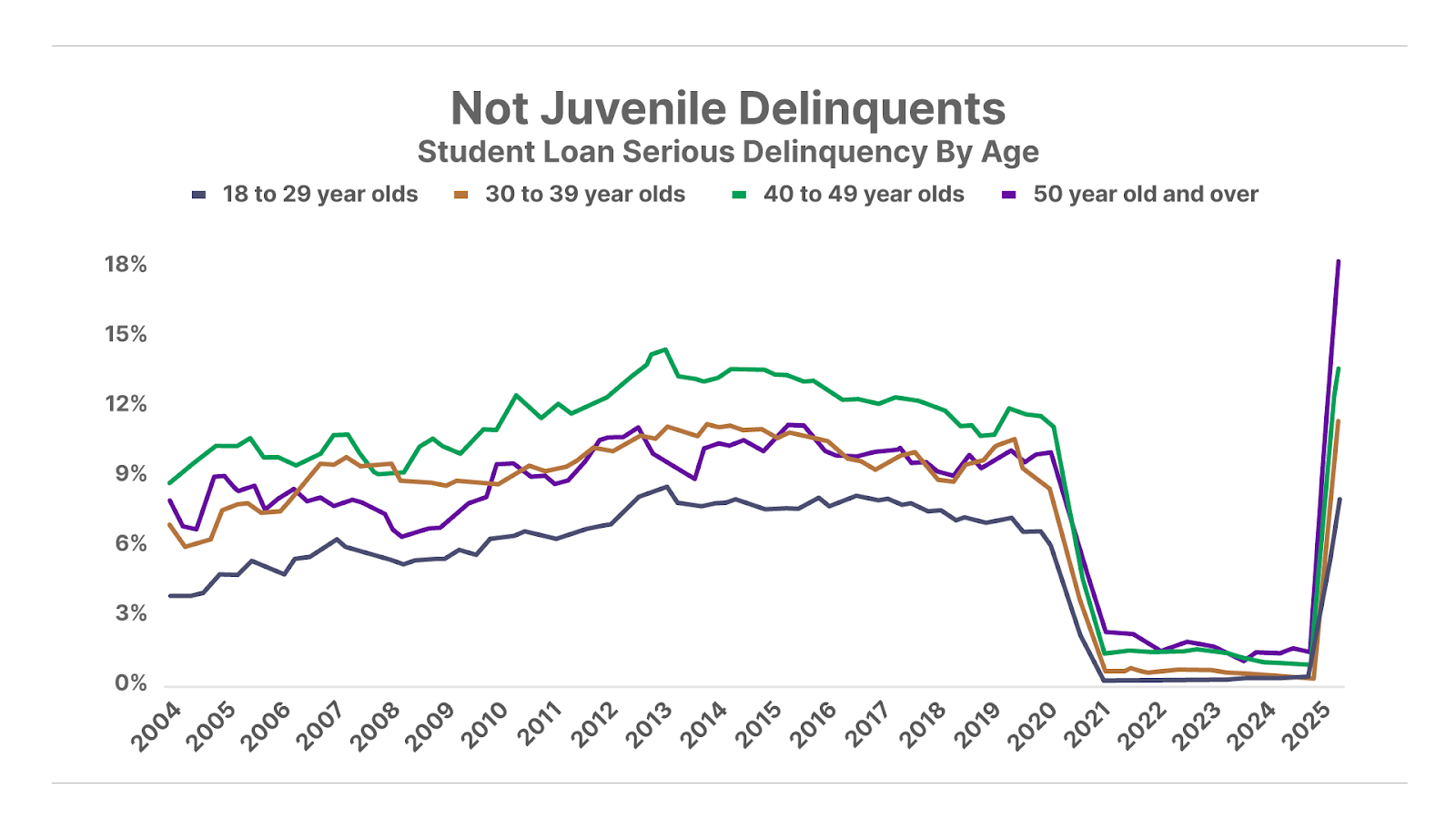

2. Student loan delinquencies surge. Following the resumption of student loan repayments this summer, the Federal Reserve Bank of New York’s latest Household Debt And Credit Report found that the percentage of student loans in serious delinquency moved sharply higher in Q2 across all age groups. The average delinquency rate rose to 10.2%, matching its previous record set in 2021, however the largest increase occurred in the oldest cohort – those aged 50 and older – with rates reaching more than 18%, well above the prior peak of around 12%.

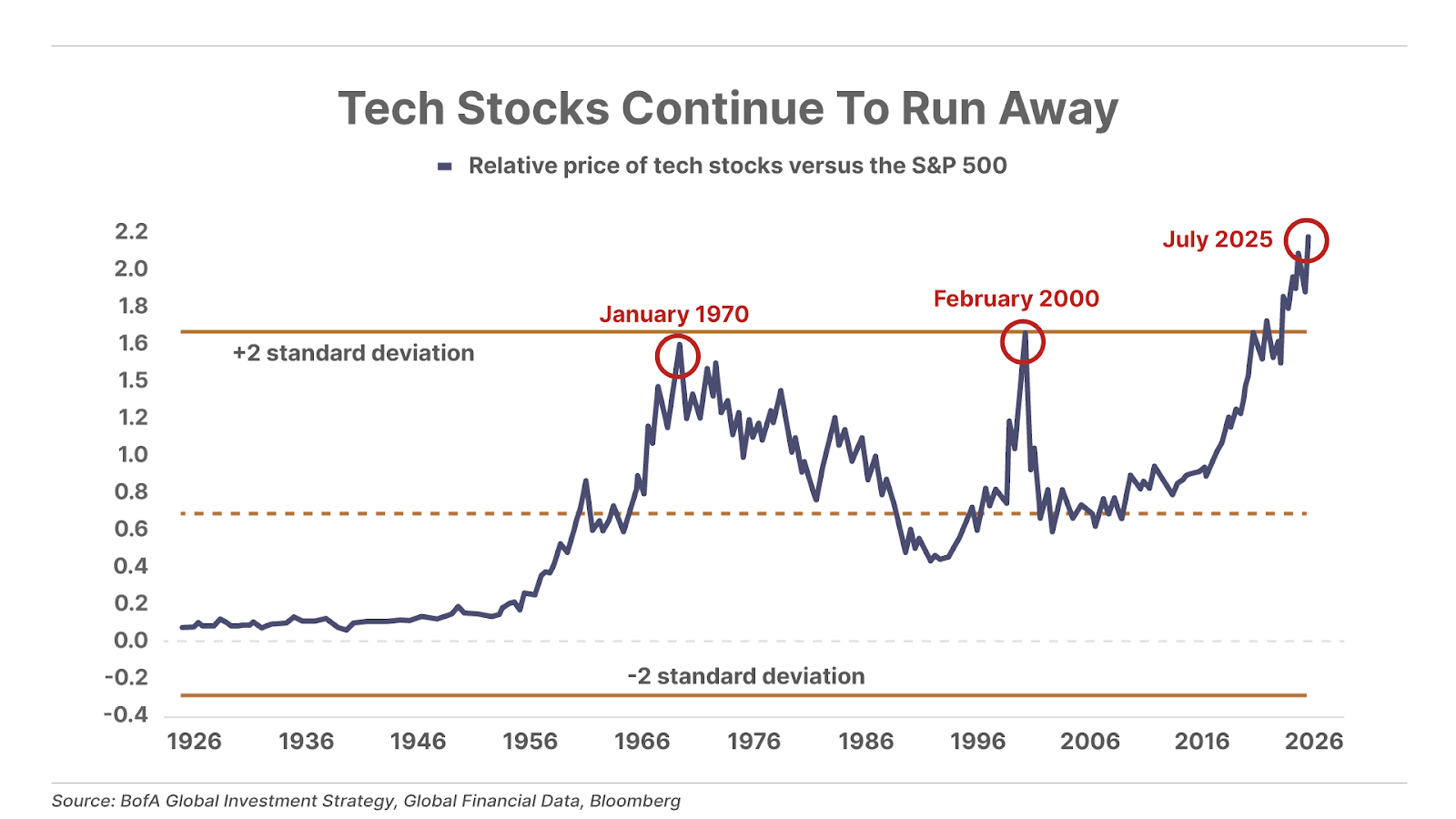

3. Tech eats the S&P. U.S. technology stocks now trade at the highest price relative to the overall S&P 500 on record going back 100 years. Meanwhile, the top seven tech stocks, known as the “Magnificent 7,” account for 35% of the total weighting in the index. The two prior extremes in January 1970 and February 2000 both preceded decade-long bear markets.

And One More Thing… Another Blowout Quarter For BWX Technologies

On Monday, the monopoly supplier of nuclear-reactor components for the U.S. Navy, BWX Technologies (NYSE: BWXT), delivered another stellar earnings report for Q2. Revenue increased 12% to $764 million, while earnings per share jumped 24% to $1.02, both exceeding analyst estimates. The company is benefitting from a robust pace of demand for nuclear-reactor components from its government contracts, plus double-digit growth in its medical radioisotope business. And the future remains bright for BWXT. Shares soared 12% to a record high of $179 following the results – for a total return of 213% from when we recommended buying shares of BWXT at $58 in December 2022. We had BWX Technologies as a Best Buy from March 2023 to August 2023 for an average return of 116%.

In next Thursday’s Big Secret On Wall Street, we will be releasing an updated list of Best Buys, three current portfolio picks that are at an attractive buy point. To get access to our latest Best Buys, click here to learn how to subscribe.

Tell us what you think: [email protected]

Mailbag

In Monday’s Daily Journal, we reported that President Donald Trump fired the Biden-appointed commissioner Erika McEntarfer who heads the BLS following a weaker-than-expected jobs report. A number of readers sent emails expressing their view on the matter.

While the numbers over the past year are suspicious, I’m not sure that they were “cooked,” as President Trump suggested. However, the process of gathering the numbers is broken! The leader of the BLS should have recognized this and fixed it! But as the typical “do-nothing” Biden appointee, she didn’t.

Good riddance!

Regards, Bob L.

Well, there goes any credibility the U.S. government has in reporting anything. Who will ever believe us again?

Phillip L.

The president fired Erika McEntarfer for a good reason. She obviously was doing a poor job of reporting, which is her basic job. Good riddance. As far as rigging goes, who really knows except that the Biden regime lied, bribed, and in general made up whatever they needed to succeed in staying in office.

Thank you,

Dave E.

DJT is an ignorant, vindictive moron.

Ghassan K.

I think that the president needs to clean out all of Biden’s and Obama’s appointments that he can. They are idealogues and will not change their spots.

W.C.

Trump can’t take the blame for anything that goes wrong during his administration especially when it’s directly related to his actions, so in order to deflect blame he fires the messenger.

Ira H.

Good investing,

Porter Stansberry

Stevenson, Maryland