We Promised Better Returns, And Less Volatility

How Are We Doing?

| This is Porter & Co.’s The Big Secret on Wall Street, which we publish every Thursday at 4 pm ET. Once a month, we provide our paid-up subscribers with a full report on a stock recommendation, and also a monthly extensive review of the current portfolio… At the end of this week’s issue, paid-up subscribers can find our Top 3 “Best Buys,” three portfolio picks that are at an attractive buy price. You can go here to see the full portfolio of The Big Secret. Every week in The Big Secret, we provide analysis for non-paid subscribers. If you’re not yet a subscriber, to access the full paid issue, the portfolio, and all of our Big Secret insights and recommendations, please click here. |

Harry Browne might be the most influential – in terms of investing – U.S. presidential candidate you’ve never heard of.

Harry was a respected figure in the world of economics and politics, who ran for president twice on the Libertarian Party ticket, and wrote 12 books that have sold over 12 million copies – including his 1973 classic How I Found Freedom In An Unfree World, and 1999’s Fail-Safe Investing.

He also has a personal connection to Porter – they first met at the 1996 New Orleans Investment Conference speakers’ dinner and later became members of the same close-knit libertarian economist circle, along with investor Doug Casey, investor and publisher Bill Bonner, and legendary world traveler and investor Jim Rogers.

Most importantly, back in the 1970s, Harry conceptualized a ground-breaking investment strategy called the Permanent Portfolio.

Harry Browne’s Permanent Portfolio is a “permanent” approach to investing. Using his strategy, you don’t have to buy and sell (or very rarely), and you don’t have to follow the news or anticipate the future. The portfolio is structured in a way that makes it difficult – essentially impossible – to lose money, no matter what happens to the economy, or to individual stocks.

Porter’s Permanent Portfolio – which paid-up Big Secret On Wall Street subscribers can view in full here – leans heavily on Browne’s work. But – Porter being Porter – he’s added his own twist to Browne’s ideas to increase the returns and decrease the risk.

How has that been working for us lately? Read on to find out…

How Browne’s Permanent Portfolio Works

Harry Browne’s core idea is deceptively simple. He suggested a four-part portfolio: 25% in stocks, 25% in bonds, 25% in gold, and 25% in cash.

What Harry Browne figured out was that in a global economy dominated by one government’s paper money, there would be a never-ending cycle of inflation, punctuated by short periods of deflationary recessions. As a result, Harry surmised, stocks would generally appreciate – but every now and then they would tumble, along with interest rates. And during those brief, deflationary periods, bonds would be the strong performers.

Likewise, Harry understood that cash would help moderate the volatility of both the stocks and the bonds in the portfolio – but that never-ending inflation would erode the value of money. Therefore, holding gold would counter inflation and pay off over time.

In short, you own stocks. You hedge them with bonds. And you hedge both of them with gold.

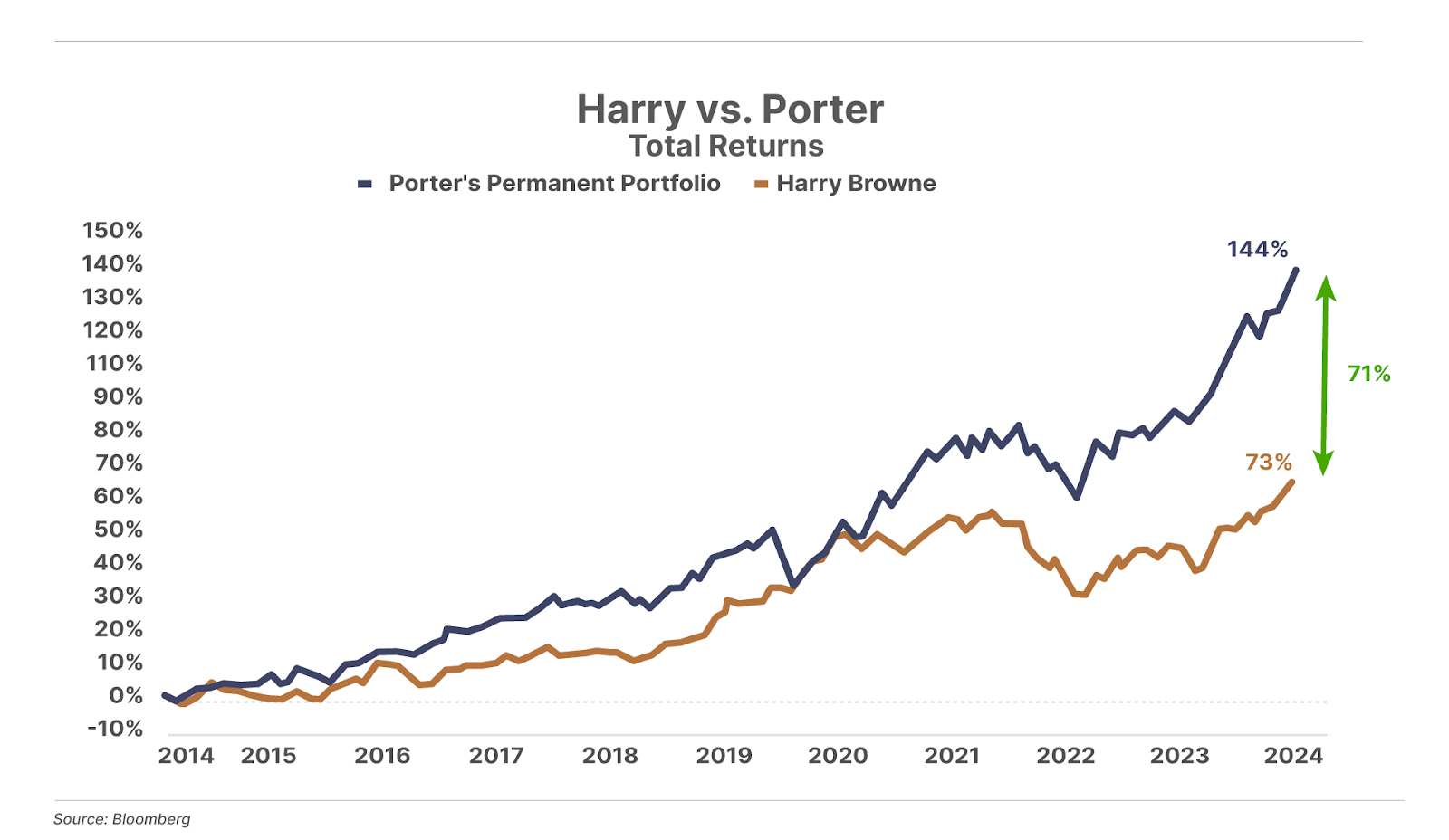

The Permanent Portfolio mutual fund (PRPFX), based on Browne’s concept, has compounded at around 7% a year since 1987, with extremely low volatility. Its largest peak-to-trough decline since 1989 is 27.2% (132 days) in 2008. The long-term average return for the overall stock market is 8% a year, while the largest stock market drawdown was 50.4% from September 2007 to March 2009.

What Browne invented was a way of capturing virtually all of the upside of the stock market, with much less of the volatility.

You might think that’s impossible. But in the late 1980s, Browne’s ideas were put into practice by Ray Dalio at his investment firm, Bridgewater Associates. These ideas, and the consistent, low-volatility results they achieved, helped Bridgewater become the world’s largest hedge fund company, today managing more than $100 billion.

All Weather, Bridgewater’s name for its Permanent Portfolio, expanded slightly on Browne’s allocations. All Weather has 30% in stocks, 40% in bonds, 15% in intermediate-duration fixed income (in lieu of cash), 7.5% in commodities, and 7.5% in gold. Dalio’s strategy produced slightly higher long-term compound results, of 7.5% a year (versus Browne’s 7%).

Dalio figured that because Harry’s portfolio had much less volatility than the S&P 500, it could be leveraged (borrowing money to invest) safely and would then reliably beat the market’s annual return. Harry Browne’s Permanent Portfolio is about 40% less volatile than the S&P 500. If you applied leverage in this portfolio, you could increase the returns to more than 10% annually – while still having less volatility than the stock market as a whole. You could, in theory, get market-beating results consistently, while not taking any additional risk beyond what investors normally face in the stock market.

Dalio put this theory into action. His All Weather fund used virtually the same allocations as Harry’s Permanent Portfolio. Then, Dalio took this supersafe portfolio and applied leverage to it, to increase the beta (the volatility relative to the overall market) up to the market’s level of around 1. Leveraged 50%, Harry’s portfolio will earn almost 2x what the market does!

And that’s how Dalio built what he calls Pure Alpha at Bridgewater, which is one of the largest hedge funds of all time.

But the portfolio we’ve built should perform even better than that.

Porter Stansberry’s Permanent Portfolio is designed to increase Harry’s returns by 2x, without increasing the risk, at all, and without using any leverage (unlike Dalio’s version).

Why Our Portfolio Is Different (And Better)…

Our goal with Porter’s Permanent Portfolio was to improve the portfolio’s average returns without increasing the volatility of the portfolio, to create a superior Sharpe Ratio, which measures how much return is achieved per unit of risk. We’re trying to create a portfolio that can produce returns in the most efficient way possible, with the least amount of volatility.

Borrowing heavily from Harry Browne, we could construct a portfolio that is essentially just like the Permanent Portfolio: 25% stocks, 25% bonds, 25% gold, and 25% cash.

Today, you could build a very low-cost Permanent Portfolio using only four ETFs:

• Stocks (25%): S&P 500 ETF (SPY)

• Bonds (25%): 20+ Year Treasury Bond ETF (TLT)

• Gold (25%): Gold Shares ETF (GLD)

• Cash (25%): 1-3 Year Treasury Bond ETF (SHY)

If you re-balanced these positions each year, you’d achieve very low-risk returns that are close to the market’s returns. But… we think there are a few simple ways to improve these results substantially, without increasing risk. Here’s how.

We launched Porter’s Permanent Portfolio last September with a notional $1 million that we spread across the different segments.

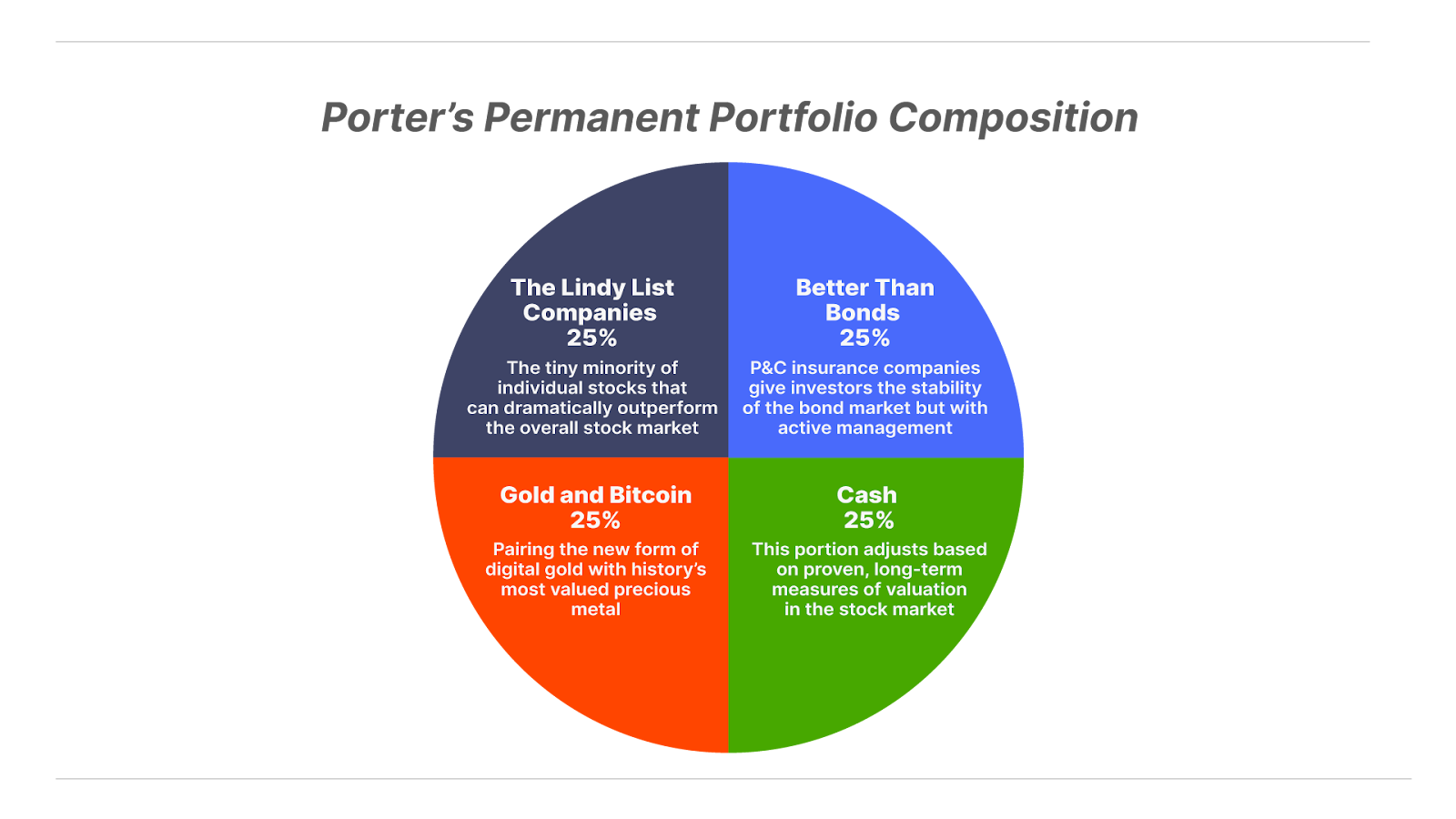

First, rather than simply allocating 25%, or $250,000, of the portfolio to long-term government bonds, which are at risk from inflation, we suggested investors should own high-quality property & casualty (P&C) insurance companies instead.

This is an area of the markets that Harry Browne didn’t understand well. Just as Browne’s portfolio strategy was based on mitigating risks, these businesses are directly involved in pricing and mitigating risk.

P&C firms, which have a proven track record of underwriting risk successfully, own and actively manage huge portfolios of bonds. These firms are, more or less, a gigantic pile of bonds with an underwriting unit on top. Owning these companies gives investors the stability of the bond market, but with active management (to help avoid losses due to inflation) and the additional underwriting profits that may accrue.

In other words, our portfolio still owns a huge amount of bonds – but indirectly, through the “wrapper” of an insurance company.

(If you’re not clear on why property & casualty stocks are the world’s best investment – no hyperbole – Porter explains it all here… and also explains how to find the best insurance companies.)

Second, rather than simply holding the S&P 500 for our 25% equity allocation, we believe long-term investors should focus on holding the tiny minority of individual stocks that can dramatically outperform the overall stock market. These winners, which we call The Lindy Forever Companies, and which Warren Buffett calls “Inevitables,” have proven over decades that they will outperform the overall market.

Relatively few companies in the world meet this lofty standard. But when we find one that does, it’s like discovering an untapped gold mine. Some well-known examples include Coca-Cola (KO), Johnson & Johnson (JNJ), and Philip Morris International (PM), which is why we have included these (along with others) in Porter’s Permanent Portfolio.

So, while we matched Harry Browne’s 25% ($250,000) recommended equity allocation, we made a subtle, though significant, change to the strategy by only owning “inevitables,” rather than the entire market.

Third, there’s a new form of gold on the world’s markets – Bitcoin. While we’re not going to delve into a full explanation for why we think Bitcoin will remain a fixture in the world’s economy for centuries, we believe it has many advantages over gold that will continue to attract investors – so we recommended allocating 25%, or $250,000, to a combination of gold and Bitcoin-related assets here.

Fourth, while Harry Browne’s Permanent Portfolio constantly rebalanced (annually) to have 25% in cash, we believe in adjusting the cash portion of the portfolio on the basis of well-proven, long-term measures of valuation in the stock market. We’ll periodically assess a range of measures of value and valuation, to determine whether to boost, or reduce, our cash allocation.

When the market is deeply undervalued, we’ll hold almost no cash. And when the market is extremely overvalued, we’ll hold at least 25% ($250,000) in “cash” through a select handful of safe, cash-like funds which pay a solid yield. Our willingness to modulate the amount of cash in our portfolio should provide us with significant improvements to long-term results.

How Porter’s Permanent Portfolio Is Performing

Again, our goal with Porter’s Permanent Portfolio is to produce strong absolute returns – roughly double the long-term performance of Browne’s original portfolio – with significantly less volatility than the major equity indexes, no matter what happens in the economy or the markets along the way. And the past several months have certainly put that objective to the test…

Investors have had to weather unprecedented uncertainty around the future paths of economic growth, corporate earnings, and monetary policy following President Donald Trump’s November election victory and the resulting tariffs and Department Of Government Efficiency (“DOGE”) spending cuts his administration has implemented since.

So, how have we done so far?

Frankly, the results have been even better than we could have imagined.

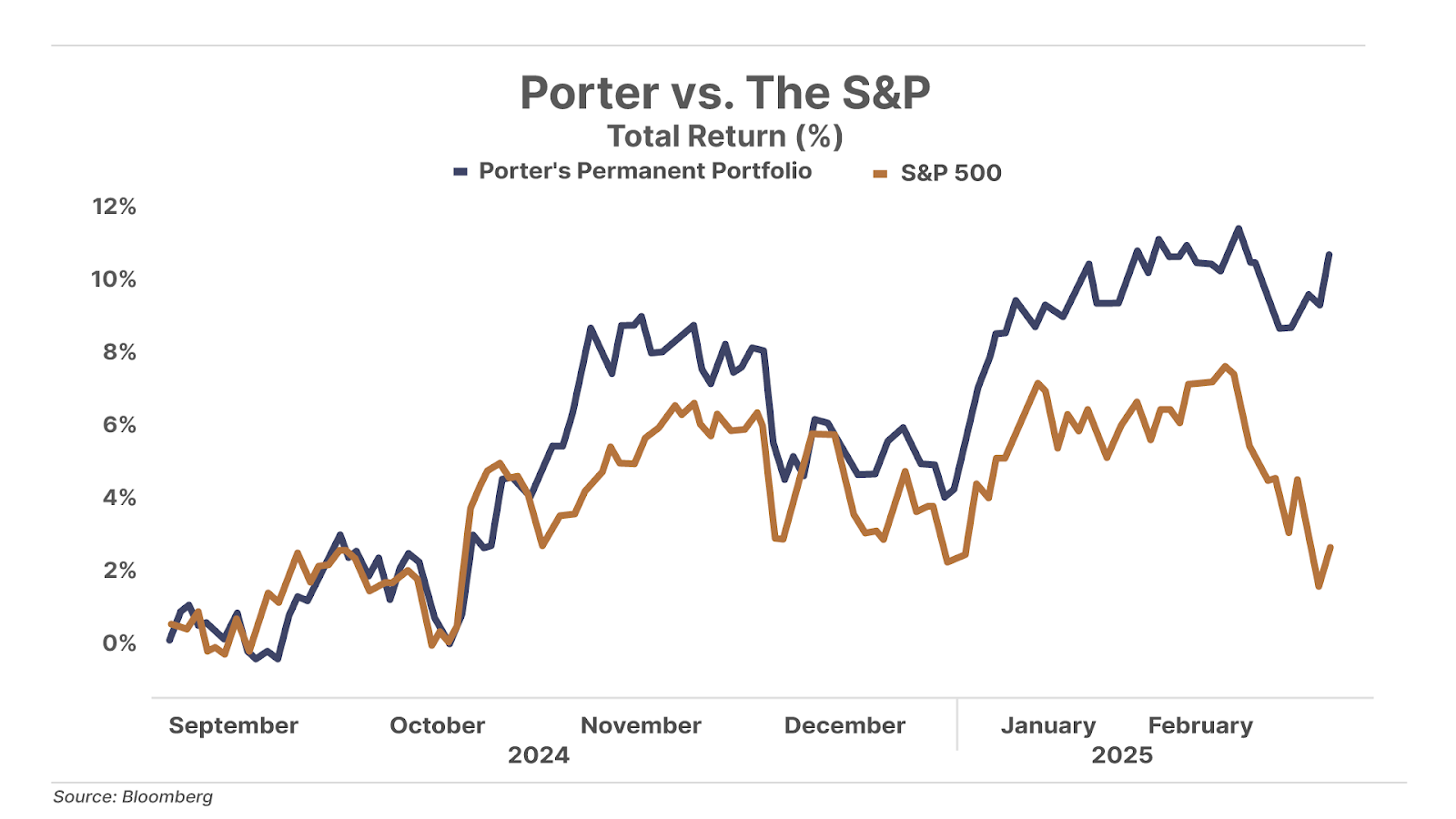

Over the roughly five months since we launched Porter’s Permanent Portfolio on September 25, it has delivered a total return of 11.0% (26.7% annualized) versus just 2.7% (6.2% annualized) for the S&P 500.

Of course, while we’re thrilled to have dramatically outperformed the broad market over this period, that isn’t our goal (and isn’t necessarily sustainable over the long run).

As we mentioned earlier, our goal is to double the return of Browne’s original portfolio while taking less risk. And we’re happy to report we achieved that goal as well.

In fact, the 11.0% return of Porter’s Permanent Portfolio was more than five times better than the 2.0% (4.6% annualized) return in Browne’s original Permanent Portfolio over the same period.

Better yet, we achieved this outperformance with less risk than Browne’s original portfolio, or the broad market.

The Sharpe ratio of Porter’s Permanent Portfolio over this period was 2.0, compared to 1.99 for Browne’s portfolio and 0.20 for the S&P 500. Generally, a Sharpe ratio of less than 1 is considered a poor risk-adjusted return, while a ratio of 2 or more is considered quite good.

Our portfolio also had a beta of 0.52 – meaning it was roughly half as volatile as the S&P 500 – versus a long-term beta of 0.60 for Browne’s Permanent Portfolio.

In short, Porter’s Permanent Portfolio has been everything we hoped it would be… and more.

The Secret Sauce Behind Porter’s Permanent Portfolio

Our portfolio’s dramatic outperformance to date is the result of three key factors…

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care Concierge, Lance James, at 888-610-8895.