- MAJOR BANKS TRADING AT LESS THAN HALF BOOK VALUE…?

- BOOK VALUE ISN’T REAL.

- WHEN WILL THE ECONOMY BE REAL…?

Pay attention, snowflakes.

There’s a world of difference between what you think you know, and what can be known.

Said another way, the hard part isn’t figuring stuff out. The hard part is figuring out how much of what you think you know, just isn’t so.

Life is a mystery. And nature keeps her secrets.

In 1927, German physicist Herman Heisenberg promulgated the uncertainty principle. According to Heisenberg, it is impossible to know both the precise position of a particle and its exact momentum.

In other words… the more you know where or what something is, the harder it is to estimate where it’s going.

Think about that the next time you’re sure you know a business… or a person… inside and out.

The uncertainty principle is often confused with another, confounding twist to physical reality – the observer effect.

Just by observing something, you alter it.

When evaluated using thermodynamics, for example, a standard mercury thermometer must absorb some thermal energy, thereby altering the state it is intending to measure. And please… please don’t even try to understand the impact of this idea in quantum mechanics. It’s the real life “looking glass.”

We have long noted that these two important laws of nature have analogs in financial markets.

In the market, the two “twists” of reality translate thus:

1. The Uncertainty Principle: The more certain you are about your investment thesis, the more likely you are to be proven wrong – at least in the short term.

2. The Observer Dilemma: The more people that follow your predictions, the harder it becomes for your followers to make money.

All That’s Gilder Is Not Gold

George Gilder is an old friend and mentor of ours. He is also one of the few, complete geniuses we have ever met.

During the roaring technology bull market of the 1990s, no one offered better advice to investors than George. No other newsletter writer (or sell side analyst) knew more about technology. George studied at Cal Tech. He wrote the foundational book on Silicon Valley, Microcosm, in 1985. When the Internet became commercialized, George’s Gilder Technology Report was like “finding the fountain of youth or a money tree or something,” Dick Sears told The New York Times back in 2003, to describe incredible results of the Gilder Technology Report’s stock recommendations during the bull market.

When a stock was added to the Gilder Technology Report, it would immediately rocket higher – sometimes by 80%.

George’s technical knowledge of the software protocols and the architecture of the microchips powering the Internet was unimpeachable. Likewise, his conviction that the Internet was going to change everything was messianic. He was certain.

That’s when the trouble started.

George’s track record, his incredible intellect, and his overwhelming certainty led everyone to read his investment newsletter. He became the first celebrity guru of the Internet. George was earning $100,000 (!) per speech. Investment bankers wanted to take his newsletter publishing company public and were offering him $200 million for the business!

Meanwhile, George consistently warned readers that, like Sir Isaac Newton — “I can calculate the motions of the heavenly bodies, but not the madness of crowds.” George could not predict stock prices. At least, he did not warn his subscribers that investor enthusiasm had gone way, way, way too far. As George put it, “I don’t do price.”

George Gilder wasn’t wrong. The Internet did change everything. Many of the investments he championed (like Qualcomm) have performed incredibly well for investors. But, the more certain you are about your investment thesis, the more likely you are to be proven wrong. George drew such a crowd into these stocks that their prices soared to levels that made it virtually certain that a crash was inevitable.

And that’s what happened to poor George Gilder in 2001.

“My whole optical paradigm crashed, and it crashed on my head… [my subscribers] didn’t lose 50% or 80% percent of their money, they lost 98 percent of their money.”

George soon found himself in debt to a former partner and in trouble with the IRS. Worst of all, his church had invested heavily in his ideas… and gotten wiped out.

When the bull market dies, the greatest bull in the market leaves Trinity Church in a coffin. Every time.

There are many legendary examples of these two ideas at work in finance, but the most famous examples are magazine covers.

Only ideas of great certainty wind up on the cover of The Economist magazine. And lots of investors follow that magazine and take its work seriously. According to the laws of finance then, you’d expect these ideas to be woefully, and embarrassingly, wrong.

In 2016, two Citigroup analysts, Greg Marks and Brent Donnelly, decided to study The Economist covers in detail. They selected 44 different covers, which in their analysis conveyed an obvious bullish or bearish sentiment. They found that, almost 70% of the time, investing the other way – fading the cover – was the winning strategy. Buying the asset (if the cover was bearish) produced an 18% return, on average, over the following year. And selling short the asset (if the cover was bullish) produced a return of 7.5%.

My favorite example: The Economist cover from March 4, 1999, Drowning in Oil. That cover marked virtually the precise bottom in energy prices and commodities. Oil would rally from $7 a barrel to almost $150 a barrel ten years later.

We suspect these two laws of finance, The Certainty Principle and the Observer Dilemma, will also impact the legacy of Ben Bernanke and central banking. Never has the world been more certain of a lie: that central banking works.

A Rolling Loan Gathers No Moss

Ever since the bailout of Long-term Capital Management in August of 1998, and the “Committee to Save the World” (the Feb 15, 1999 cover of Time Magazine, featuring Federal Reserve Chairman Alan Greenspan, Treasury Secretary Robert Rubin, and Undersecretary Lawrence Summers) the financial mandarins of the leading western economies have gathered power by consistently bailing out the banking system. They’ve done so primarily via the printing press, driving interest rates lower and sending the total debt of the system ever higher. Inflation has followed, as it must.

The pinnacle of Central Banking power is the Federal Reserve, under Ben Bernanke. He was recently awarded the Nobel Prize in economics, specifically because he used the Federal Reserve to inflate the U.S. financial system in ways never dreamed of before his tenure.

“Helicopter Ben” declared that there was no limit to the Fed’s power to inflate the money supply and nothing he wouldn’t do to protect the banks. His strategy led to a 10x increase in the size of the Fed’s balance sheet.

And… that’s led directly and indirectly to all kinds of problems in the U.S. Treasury markets, U.S. inflation, soaring economic inequality, and, perhaps most importantly for us today, an enormous number of “zombie” companies that threaten the solvency of the global financial system. Banks, rather than taking losses and writing down loans, have instead simply continued to refinance companies that are clearly insolvent.

Edward Chancellor, in his insightful new book The Price of Time, describes in detail the growing zombification of the major western economies.

“As in Japan, Europe’s zombie companies undermined the region’s economic dynamism. As in Japan, zombies gnawed at the vitals of Europe’s banking system. By 2015 it was estimated that European banks had more than $1 trillion of bad debts, a twofold increase since 2009 and roughly equivalent to a tenth of their private sector loans… Weighed down with old non-performing loans, European banks became reluctant to advance new loans. (The flattening of banks’ net interest margins by monetary policy exacerbated this problem.) A curious case of adverse selection appeared: more efficient firms and industries dominated by zombies were forced to pay more for their bank loans than those in other sectors.”

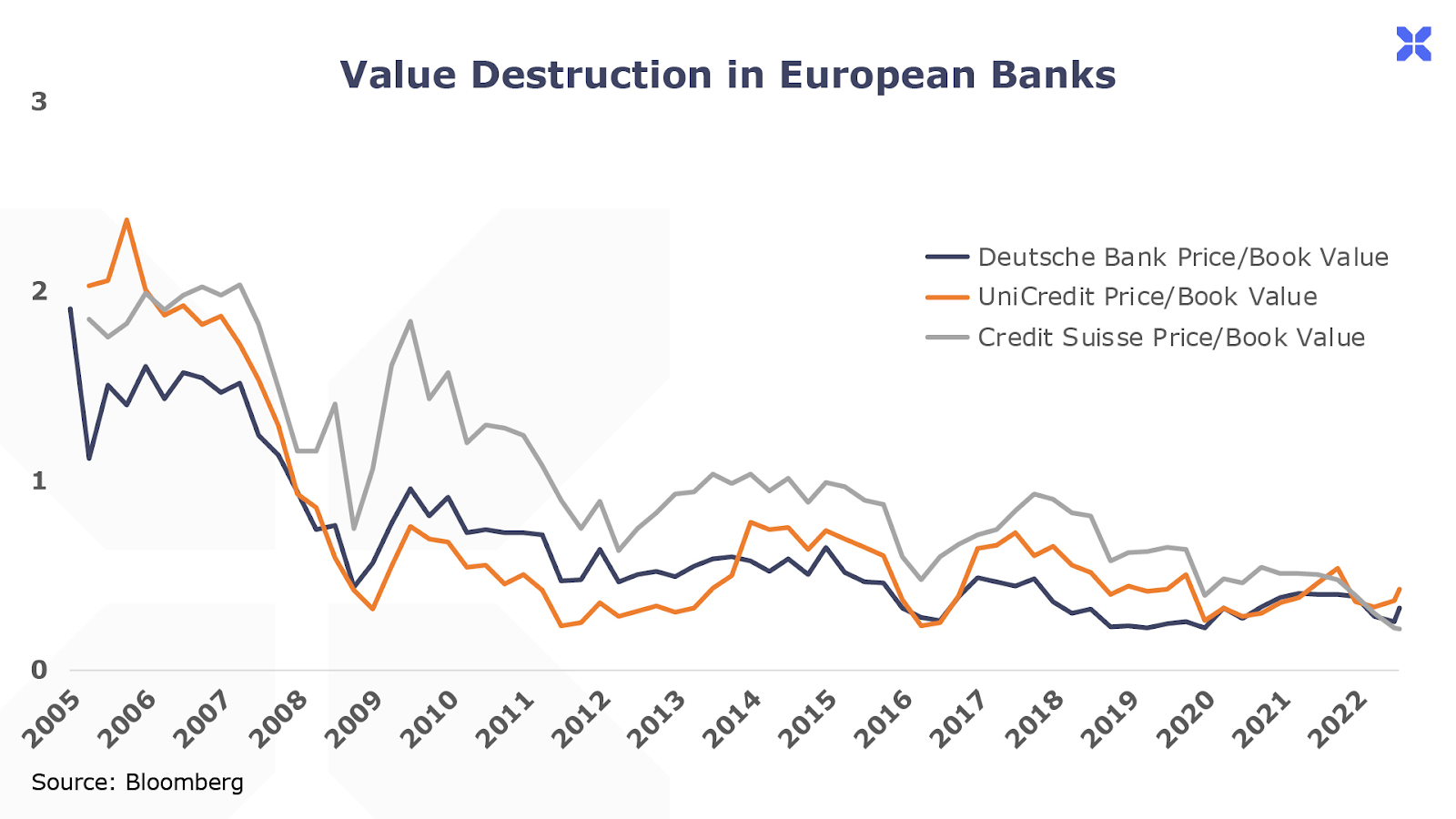

With no real rate of interest to serve as a hurdle for efficiency and with central banks providing unlimited funding, the role of banks to provide capital efficiently became impossibly corrupted. The result? An economy that can’t grow. In Europe, Italy’s banks are the most dysfunctional, led by the international disaster, UniCredit.

By removing the impact of creative destruction from banking, Bernanke and his peers around the world have built economies that no longer function. True, they don’t crash (at least, not yet). But nor do they work.

Again, Edward Chancellor says it well…

“In the fifteen years since the start of the euro project, Italy enjoyed no increase in income per capita and labor costs climbed relative to Germany’s, rendering Italian exports uncompetitive… Without adequate economic growth, Italy’s sovereign debt problems and the Eurozone’s existential crisis remained unresolved. As in Japan, easy money bought time, but time was wasted.”

As you can see in this long-term chart of Europe’s leading zombie banks, the market has long doubted the value of their assets. And the quality of these banks has consistently declined… meaning that the Bernanke solution has completely failed. Today, more than a dozen years after the first signs of a European sovereign debt crisis, the banking system remains completely dysfunctional, and the size and scope of the total debts has more than doubled.

Ben Bernanke, the most certain central banker of this generation, has won a Nobel Prize for nothing. It will not be long before he is widely known as a fool.

We don’t know whether the impending global financial “reset” will entail a debt jubilee, aka massive defaults, like Biden’s student loan bonanza. Or maybe we will endure a long period of inflation as debts are slowly worked out in pretend money. As Rick Rule is fond of saying: “We have two balls. Neither is crystal.” We don’t know – and can’t know.

But we do know this: it is impossible for the major western economic areas (the dollar, the yen, and the euro) to repay, in sound money, the debts their central banks have financed.

America has, in certain situations, like we mentioned – the U.S. student loan saga – chosen to default without ever making anyone “eat” a loan. The government bought all the loans, knowing full well that most of them would default. How did we pay for the losses? By printing more money. Will this continue…? Seems likely: A rolling loan gathers no moss.

But it also wrecks society. Maybe we will soon adopt an approach like Iceland’s during the Great Financial Crisis: “f*ck ‘em.” Iceland simply stopped paying on debt equal to 9x its GDP. Instead, it facilitated more (useless) Covid-19 testing.

But what we are certain of, is that the impact of these debts will greatly reduce the standard of living for most people over the next decade, at least. They also increase the volatility of the system, increasing the likelihood of suffering catastrophic losses. Our bet is that the purchasing power of the average major currency declines by at least 50% in the next five years. To break even, you’d have to double the size of your portfolio.

How best to achieve that goal?

It’s hard to beat the returns on invested capital in the pharmaceutical business. And it’s hard to imagine a more lucrative drug than a pill that cures obesity.

Of course, our certainty about this opportunity makes us worry. And sharing this idea with you makes a disaster more likely.

Investing is hard.

But gaining weight has never been easier.

The Growth of American Waistlines

It’s no secret that America is getting fatter. This shows up in the stunning statistics on obesity, defined as individuals with a body mass index (BMI) exceeding 30… that means that if you’re six feet tall and weigh more than 220 pounds, you’re considered obese.

Since the early 1950s, the American obesity rate has quadrupled from roughly 10% of the population to over 40% today. With more than 100 million Americans suffering from obesity, the problem has reached epidemic status. Obesity has become one of the leading causes of preventable death, as a key factor driving heart disease, stroke, diabetes and cancer.

Adults with obesity incur an estimated $1,861 in additional medical costs each year compared to those with a healthy weight. Spread across the entire country, that’s nearly $200 billion per year.

One reason behind rampaging obesity is the proliferation of sugar in modern foods. Americans consume an average of about 80 grams of sugar each day, or about twice the recommended amount. The problem is the ubiquitous array of high-sugar foods in the modern American diet, starting with our early morning coffee rituals.

Consider the official drink of the fall season – the Pumpkin Spice Latte – which is an adult milkshake disguised as coffee. This venti sized Starbucks indulgence contains 470 calories and 63 grams of sugar – or more than the entire daily recommended amount – in a single beverage:

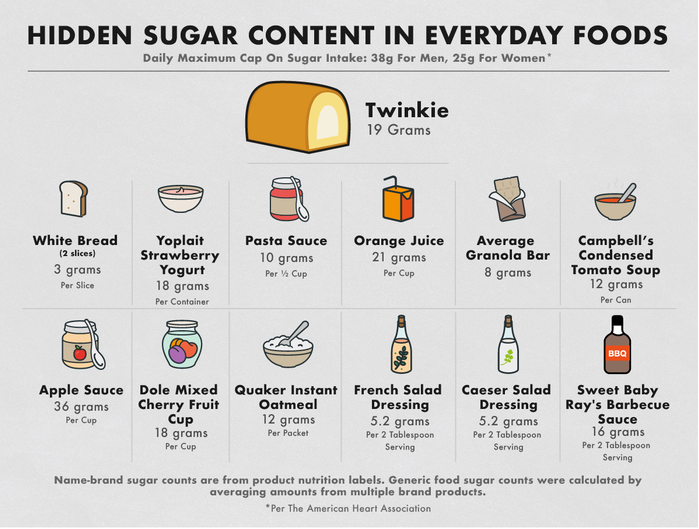

Starbucks is hardly alone. Today’s food industry injects sugar into almost everything we eat – from salad dressing to bread to cereal – as a low-cost way to boost flavor. By some estimates, roughly 80% of all items on grocery store shelves contain added sugar. Even foods considered “healthy” are often loaded with sugar, including protein bars, granola, soup, yogurt and countless other items:

Credit: Nina Teicholz

Another key factor is the trend towards super-sized portions. The average restaurant serving today is more than four times larger than in the 1950s:

More sugar and bigger meals have combined to fuel America’s exploding calorie count. The average adult in the U.S. today takes in 2,568 calories, up from 2,109 in 1970. As one research firm put it, this additional caloric intake is “the equivalent of an extra steak sandwich every day.”

A lot of the extra calories we consume go straight to our waistlines, given our increasingly sedentary lifestyle. Data from the Centers for Disease Control and Prevention (CDC) shows that 25% of Americans are sitting down for eight or more hours each day. And 44% of Americans don’t engage in even moderate physical exercise or activity.

Worse… America isn’t the only country suffering from this alarming trend.

A Global Epidemic

Obesity is a byproduct of rising global affluence, as a growing segment of the world’s 8 billion population enjoys the luxury of cheap and abundant food. Plus, rising productivity means we can generate more economic activity with machines and automation, requiring less human labor. But too much food and less physical activity has created an epidemic of obesity worldwide:

Given the dire health consequences of growing global obesity rates, the stakes couldn’t be higher to find a solution. And consumers certainly want a solution.

Look no further than the billions of dollars in sales from countless diet programs and exercise products each year, including the $2,500 Peloton bike craze that swept the nation during the pandemic lockdowns (how many of these bikes now function as high-end clothing racks rather than exercise equipment?).

A 2018 National Health and Nutrition Examination survey showed that 49.1% of American adults attempted to lose weight over the previous year. But despite their best intentions, CDC data showed that obesity rates rose to a new record high 42.4% that same year.

A Massive Problem with Few Solutions

Scientists and doctors have spent decades searching for the miracle weight loss solution, largely in vain. Bariatric surgery, also known as a gastric bypass, has been the most effective solution in recent years, involving the doctor cutting into the stomach and separating it into two sections. The top section becomes the new, smaller stomach, and the larger, lower portion is bypassed. The small intestine is re-routed to connect to the newly segmented, smaller top portion of the stomach (as seen on “My 600-Pound Life”).

A smaller stomach means patients need to consume less food to feel full. The procedure is an effective solution, helping patients lose up to 30% or more of their body weight. And shedding all of that weight delivers a major improvement to a variety of health outcomes, including a reduction in the long-term mortality rate (the death rate per unit of time) by up to 40%.

But bariatric surgery can cost $20,000 – $30,000. The procedure only takes about 90 minutes, but requires spending 2-3 days in the hospital, plus another few weeks recovering at home. And it often takes about 12 weeks before the patient can eat normal foods again. Roughly 15% of patients suffer complications, and 0.5% of patients die after going under the knife.

Still, more than 250,000 Americans undergo a gastric bypass operation each year, reflecting the lengths that overweight people will go to in an attempt to lose weight.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.