| Below, you’ll find the latest market update and portfolio review from Porter & Co.’s Director of Distressed Investing, Martin Fridson. We release a full report with a new recommendation on the second Thursday of each month, and an update like this one two weeks later. Marty also provides the “Top 3 Best Buys” – a regular feature that highlights what he views as the three most attractive positions to focus on in the portfolio, to help those who are new to distressed investing get started. As always, please call Lance James, our Director of Customer Care, with any questions. You can reach him and his team at 888-610-8895, or internationally at +1 443-815-4447. |

U.S. President Donald Trump’s unveiling of his tariff plans didn’t play well in the credit market.

From Liberation Day on April 2 through Friday, April 11, the high-yield risk premium jumped by 84 basis points (1 basis point = 1/100 of a percentage point), from +342 to +426, as measured by the ICE BofA U.S. High Yield Index. (The risk premium is defined as the difference in yield between speculative-grade bonds and default-risk-free U.S. Treasury bonds.) To appreciate how big a change, in a matter of nine days, that is, consider that since 1996 there have been eight years in which the risk premium moved up or down by less than 84 basis points.

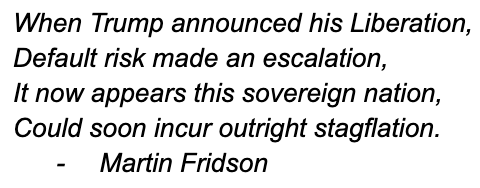

An increase in the high-yield risk premium generally indicates an increase in default risk. That message is corroborated by the rise in the distress ratio – the percentage of issues in the high-yield index with risk premiums of 1,000 basis points or greater. After ending March at 5.94%, the distress ratio climbed to 8.31% on April 11.

Reviewing the recent events, my former Merrill Lynch colleague Tom Sowanick noted that the U.S. now has the potential for three fives – a 5% unemployment rate, a 5% inflation rate, and a 5% yield on the benchmark 10-year Treasury. A combination of the first two, along with slow economic growth, could qualify the economy for what’s known as stagflation. That term, derived from a combination of “stagnation” and “inflation,” signifies a worst of all worlds in which inflation remains hot despite the widespread expectation that depressed demand in a sluggish economy will cool it down. Sowanick sees inflation potentially heating up as the dollar weakens and the new tariffs lead to price increases instead of being absorbed by exporters to the U.S.

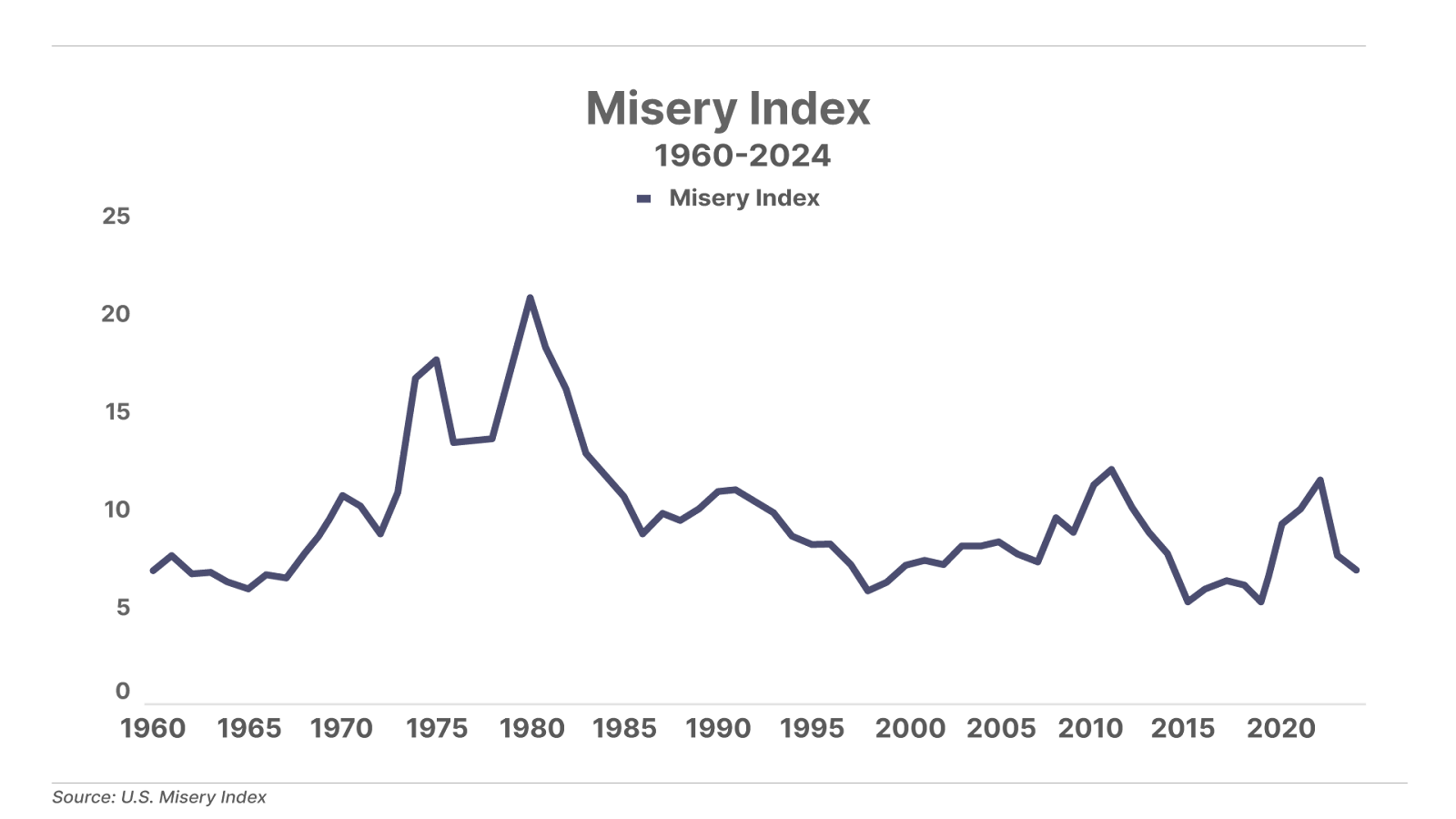

Stagflation entered the U.S. economic discussion during the economically troubled 1970s. Around the same time, economist Arthur Okun introduced a way to quantify stagflation known as the Misery Index. It’s the sum of the U-3 “official” unemployment rate and the consumer price index inflation rate. In the period from 1974 to 1982, the Misery Index ranged from 13.45% to 20.76%. In 2024, economic hardship was a less miserable 6.98%, but the “fives” envisioned by Sowanick would put it back into double digits.

The Misery Index is a people-oriented depiction of the economy at a given time: How likely are they to be out of work and how hard are their pocketbooks being hit by rising price levels? But that one-two punch forces consumers to tighten their belts, which is bad news for the business world. We can therefore expect that if the unemployment and inflation rates return to double-digit territory, the recent trend of rising financial distress will continue.

If the supply of distressed bonds increases, the prices of distressed bonds will likely decline. This suggests some bargains will become available for discerning, patient investors. In time, many genuinely viable companies within the distressed universe will repair their balance sheets and patch up their operations. We’ll be carefully looking over the distressed merchandise to generate profitable recommendations.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care Concierge, Lance James, at 888-610-8895.