Issue #139, Volume #2

Why A Global Financial Crisis Is Now Certain

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

|

The Blackwater 61 crash… This is not political… Most people don’t pay taxes… International financial crisis is coming soon… Worse than the UK after WWII… AI debt is scaring Wall Street… Inflation softens a bit… |

A box canyon, if it’s steep enough and narrow enough, can cause catastrophic plane crashes.

A plane enters the box canyon (a narrow gorge with steep, cliff-like walls) and before the pilot recognizes the danger he flies too close to the soaring end wall. There’s not enough room to pull up and fly over. And the sides are too narrow to turn around.

That’s what happened to Blackwater 61, the call sign of a CASA 212 turboprop plane carrying six Blackwater private security contractors on November 27, 2004, in the mountains West of Bagram airbase in Afghanistan. Everyone on board died.

It’s the perfect metaphor for the U.S. government’s fiscal problems. The “plane” seems to be flying normally. And even though everyone can see the “canyon,” nobody understands yet that we don’t have the ability to pull up before there’s going to be a devastating crisis.

I introduced you to some of these ideas earlier this week. And, as I expected, lots of people didn’t seem to read (or understand) the facts that I laid out. Instead, they saw my warning as merely a criticism of the President. So, before we continue, I want to make it explicitly clear, once again, that these problems are not political. The problem is our system (our plane) can’t possibly handle our existing debt load.

At some point soon – very soon – the bond market is going to piece this together. And there will be the largest financial crisis the world has ever seen, because our government’s debts are the foundation of the entire world’s system of trade, banking, and finance.

The numbers I showed you on Wednesday (which only became public last week) are the cleanest real-time proof I’ve seen yet that my box-canyon hypothesis is correct. Tax receipts were up a staggering 24% year-over-year yet the deficit still widened by 10.5%!

Please think about that for a second: even a once-in-a-decade revenue windfall (tariffs, capital gains, strong wage growth) was completely swallowed by the autopilot growth in interest expenses, Social Security COLAs (cost of living adjustments), and Medicare. That’s the structural trap – the box canyon – in one data point.

Everyone still believes that “we can grow our way out” of our debt problem. But data now say otherwise. It’s not just a mountain of debt – it’s a box canyon.

In the U.S., total government taxation – federal plus state plus local – was equal to 27.7% of U.S. GDP in 2022 (latest comprehensive OECD numbers). It’s likely much higher now, because of the tariffs. But, as you’ll see, the U.S. is already at or slightly above the level where the behavioral responses make collecting more tax revenue both impractical and self-defeating.

People will work less if taxed more. They will move their businesses (and themselves) offshore. They will alter their behaviors in ways that harm our economy and reduce tax collection overall.

To support this claim, the opposite always occurs: when the government sharply cuts tax rates, like President John Kennedy did in 1961 and Ronald Reagan did in 1981, revenue actually increases, while falling as a percentage of GDP.

Both state and federal income taxes are extremely progressive, with about 15% of all households paying for more than 85% of all taxes. As a result, marginal rates in high-income and high-tax states like California and New York are well over 50%. How can you raise taxes in those states? There are already huge incentives for highly skilled people like doctors, lawyers, engineers, artists, and good tradesmen to simply stop working. Or take payments under the table, in Bitcoin. Or move… And they will.

In other words, the plane can’t pull up fast enough. We can’t raise more revenue without seriously hurting the economy.

One big reason: there’s roughly a 1-to-1 dependency ratio between people who are completely dependent on the government and people who pay a meaningful amount of income tax.

Another reason: interest on the debt. We’re spending over $1 trillion on interest now. For context, the federal government collected $2.4 billion via income taxes last year. We’re spending 41% of income taxes on interest.

This is a box canyon, not merely a mountain of debt.

You’re probably familiar with Great Britain’s fiscal crisis following last century’s global wars. After WWII, the UK’s national debt-to-GDP ratio peaked at an astonishing 270%. Debts of this magnitude can’t be legitimately financed. So the government chose a path of financial repression rather than outright default. Most economists and investors assume we’ll get out of our box canyon in the same way.

The strategy involved the Bank of England (“BoE”) systematically keeping interest rates (yield-curve control), resulting in negative real interest rates. Over decades, inflation slowly but surely eroded the real value of the outstanding, low-interest Consol bonds that were used to finance the wars. Bondholders were repaid their nominal principal “in full,” but with currency that had significantly less purchasing power – like 99% less. This was effectively a slow, managed theft of wealth from creditors via currency debasement.

It wiped out the middle class and triggered the growth of socialism in Great Britain as most people believed that capitalism had failed them. And what are we seeing now in America? The same thing. And it will get much, much worse.

But, again, our situation isn’t merely a mountain of debt that can be “melted” away over decades with inflation. We’re facing a box canyon.

Very important difference: The UK’s debt was financed by perpetual bonds – extremely long-term debt. The U.S. debt crisis is structural. It’s driven by inflation-protected, off-balance-sheet commitments that dwarf the currently issued debt. These can’t be printed away.

Here’s the current breakdown:

-

Outstanding Publicly Held Debt: $30 trillion (approximately 95% to 100% of GDP)

-

Total Implicit Obligations (SSA & Medicare): The net present value (“NPV”) of unfunded liabilities for Social Security and Medicare over the next 75 years is estimated to be over $75 trillion (!)

-

Combined Indebtedness: When combining explicit debt with implicit entitlement liabilities, the total federal indebtedness is estimated to be over 340% of current GDP, making the total challenge significantly larger than the UK’s 270% post-war burden.

The second poorly understood difference is that the UK relied heavily on non-callable, perpetual war bonds (Consols), which gave its Treasury the flexibility and time to devalue those obligations with inflation over four decades.

The average maturity of the current U.S. Treasury market is currently 71 months. And 33% of all the publicly held debt will come due within 12 months. This vastly increases the risk of a funding crisis or a panic. As short-term debt must be continually rolled over, any sudden spike in market-driven interest rates will immediately translate into dramatically higher government interest payments, accelerating deficit spending, and requiring even more borrowing – a doom loop.

That’s the box canyon’s wall soaring up to meet us.

By the time the UK government went broke in 1946, it had already ceded its status as the center of global trade and finance to New York. But today, America very much remains the foundation and the center of the world’s markets. U.S. Treasury securities act as the risk-free benchmark for all U.S. domestic and global private sector financing. They are the foundation of global financial liquidity and serve as collateral for a vast network of global transactions.

The Federal Reserve has been forced to intervene previously (e.g., March 2020) to prevent a freeze in the Treasury market, highlighting its structural fragility. However, a crisis driven by a loss of fiscal credibility (a long-term insolvency concern) rather than a short-term liquidity shock is fundamentally different. If global investors (including foreign central banks, who are major holders of U.S. Treasuries) perceive the U.S. government as unwilling or unable to service its debt – either by raising taxes or cutting spending – they will demand substantially higher yields.

This rapid rise in the cost of capital would cause a synchronized, complete freeze in global lending, a massive flight from the dollar, and the potential disintegration of the existing dollar-based global financial order.

The world has no historical precedent for a crisis involving a reserve currency of this magnitude, making the outcome impossible to model.

But, I know this. It won’t be good – for anyone.

Next week, I’ll discuss three simple solutions – all politically impossible. And that’s why I am, more than ever, convinced that “winter is coming.” An unprecedented crisis. And war.

The Flight to Stability Has Begun. Most Investors Miss it.

Presented by Jared Dillian Money

When a handful of Big Tech names drive the market, history says it doesn’t end well.

In early 2000, the dot-com bubble popped, the S&P was cut in half, and money rushed into a corner of the market nobody expected.

Former Lehman trader Jared Dillian – one of Porter Stansberry’s top three favorite newsletter writers – sees the same setup now.

Money rotating out of growth and cash-rich, overlooked companies CNBC ignores.

Click here to get the details.

Three Things To Know Before We Go…

1. Inflation surprises to the downside. This morning, data from the Bureau of Economic Analysis showed the Federal Reserve’s preferred measure of inflation – known as the core personal consumption expenditures (“PCE”) price index – rose 2.8% year-over-year in September (the latest month of data available due to the government shutdown). Wall Street economists had expected a rise of 2.9%. While price inflation remains well above the Fed’s official 2% target, this morning’s report of a reduced inflation level likely keeps the central bank on track to cut rates again when it meets next week.

2. President Donald Trump proposed U.S. “tiny car” production. For a country that loves its trucks, SUVs, and oversized everything, the shift to smaller cars says less about consumer preference and more about the financial struggles consumers face. With the average new car now costing more than $50,000, the market for larger vehicles is slipping out of reach for many households – a troubling sign. Tiny cars – popular in Japan and European markets – would require regulatory changes to be built in the U.S.

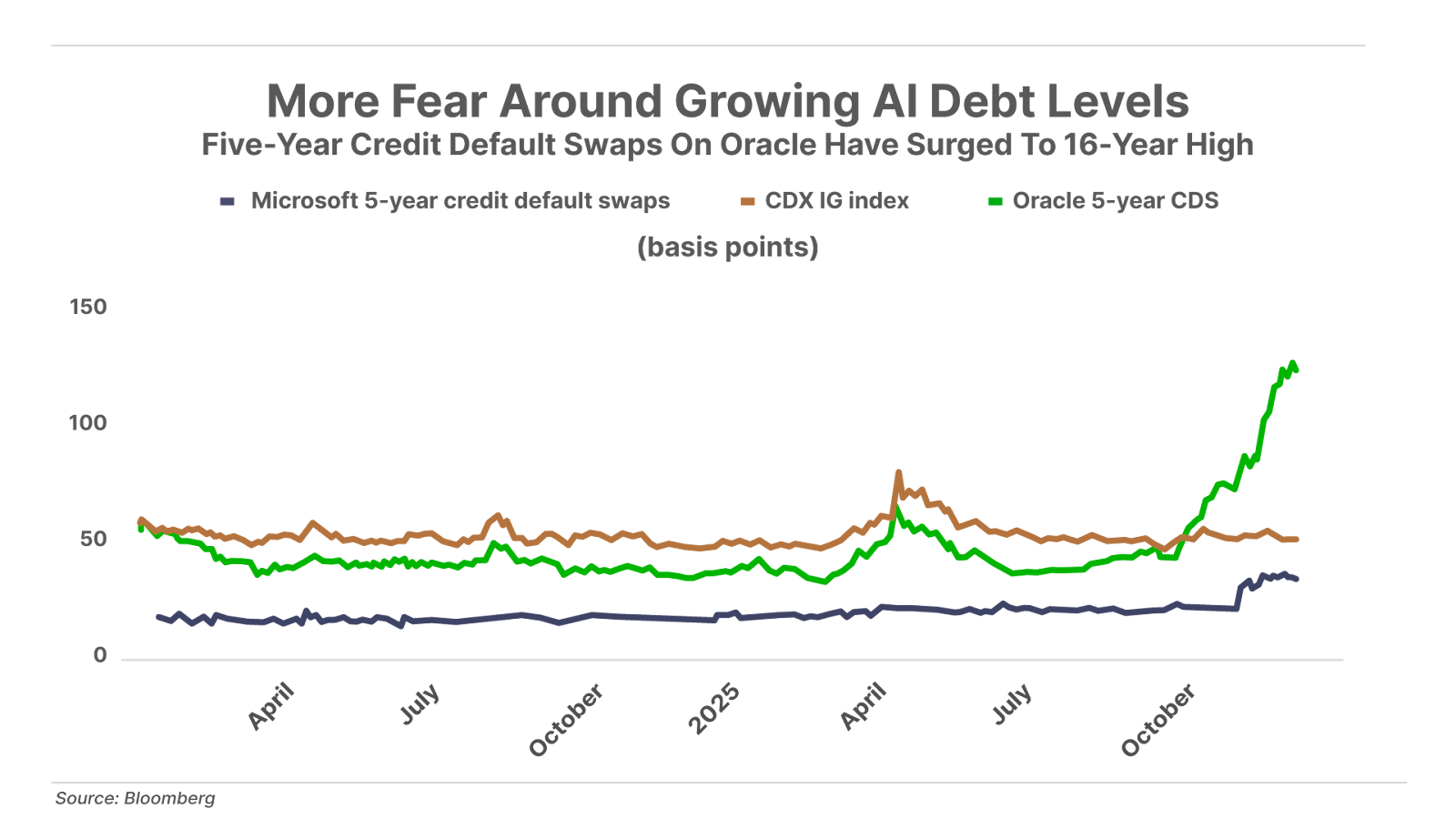

3. Wall Street shies away from the AI borrowing boom. As we reported on Wednesday, credit default swaps for data-management giant Oracle (ORCL) have surged to a 16-year high, and they aren’t alone – Microsoft’s (MSFT) credit default swaps are also rising. Hyperscalers and other artificial-intelligence-focused companies are expected to spend some $5 trillion building data centers and related infrastructure over the coming years. More of them have been tapping the debt markets – rather than their own cash flows – to fund this spending spree. Oracle, Meta (META), Alphabet (GOOG), and others have helped push global bond issuance to $6.5 trillion this year. Lenders are now hedging their exposure – essentially covering their tails – in case the enormous AI buildout fails to deliver the profits and returns investors are banking on.

Lead analyst Ross Hendricks recently shared with Trading Club members a strategic hedge designed to protect against a potential collapse in the AI boom – offering the potential for 10x or greater upside if the AI bubble bursts.

Tell me what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.