Issue #93, Volume #2

Hating On A Bond For All The Wrong Reasons

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Bonds are misunderstood… Shunned by non-distressed investors… Volatility plays a big role… Talen Energy’s merchant-power business… A 47% return in 12 months… Cooties on the playground… Bankruptcies are way, way up… S&P concentrations are staggering… |

Editor’s note: Porter has turned today’s Journal over to Distressed Investing senior analyst Marty Fridson.

Marty has a long background in trading, investing, and finance… Over a 25-year span with Wall Street firms including Salomon Brothers, Morgan Stanley, and Merrill Lynch, he became known for his innovative work in credit analysis and investment strategy.

Below, Marty shares some of the wisdom learned along the way. He offers up a case study of a distressed bond that most investors had shunned and written off for the default pile…

Marty offers up the details now…

Bonds are severely misunderstood.

Most investors think of bonds as unspectacular but steady performers whose role is to stabilize a portfolio that also contains the higher-octane asset class of common stocks. But subscribers to our Distressed Investing research know there’s another side to the story. They’ve seen returns like the following on some of our past recommendations:

- AMC Entertainment 5.75% bond maturing 6/15/2025: 42.64%

- Frontier Communications bond 5.875% maturing 11/1/2029: 43.87%

- Herbalife 4.25% bond maturing 6/15/2028: 35.32%

Stratospheric returns like those result partly from yields much higher than you see on the safe, secure bonds of investment-grade companies (rated BBB or higher). But it takes heroic capital gains to achieve percentage returns in the 30% and 40% range.

This is a different world from a stock that jumps 3% when quarterly earnings come in 10 cents higher than the analysts’ consensus. Rather than gauging the odds of the next quarter’s earnings per share exceeding guidance by a couple of percentage points, distressed investors often have to make a judgment on whether a company will default on the next coupon payment.

That event could be followed by a bankruptcy filing in which holders would recover less than half the face value of their bonds. In short, distressed investing is a high-stakes affair, but for that very reason the payoffs for being right can be phenomenal.

A Case Study That Demonstrates The Point

Talen Energy (TLN) competes in the merchant-power industry – these companies own electric power plants, but, unlike regulated utilities, they sell their electricity into the wholesale market. They don’t have long-term contracts, so they take a lot of price risk, with the possibility of earning high returns – or having to sell below cost.

On April 4, 2018, the Talen Energy 6.50% bond maturing 6/1/25 was priced at $645 – a steep discount to its $1,000 face value. That represented a 14.67% yield-to-maturity at a time when the average bond with the same B credit rating yielded 6.83%, less than half as much. The Talen yield exceeded the yield on comparable-maturity U.S. Treasury bonds by more than 10 percentage points, placing it in the distressed category by the convention I introduced some 35 years ago.

That valuation indicated a consensus among investors that Talen faced something like a one-in-four probability of defaulting within 12 months.

Not only did Talen not go belly-up in that span, but one year later, on April 4, 2019, the 6.50% bond’s price had jumped 36.82% to $880. Taking into account the interest earned over the period, an investor who owned the bond on April 4, 2018, achieved a one-year return of 46.90%.

So why was the price so depressed in April 2018 and what drove the price up so significantly in just one year?

Two fears were depressing the bond’s price in early 2018. Both were overblown.

The first fear involved Talen’s ownership at the time by a private equity firm, Riverstone Holdings. Bond investors have seen cases in which a private equity firm stripped assets from an acquired company, leaving it in a precarious financial position, leading to a default. Riverstone heightened fears of that dire scenario transpiring by extracting a $500 million dividend from Talen in December 2017 and subsequently suggesting that additional dividends might follow.

Those events were far from adding up to a looming financial crisis, however. Moody’s deemed the company’s liquidity position “adequate.” Furthermore, it’s unlikely that Riverstone would have extracted a dividend in December 2017 if Talen had truly been in serious financial straits. Riverstone’s managers knew that if Talen filed for bankruptcy in the next two years, Riverstone would have faced the possibility of being ordered by the federal bankruptcy court to return the $500 million dividend on the grounds that Talen Energy was insolvent at the time that the dividend was paid. (In technical terms, the dividend could have been ruled a fraudulent conveyance.)

The second fear factor that was weighing on investors’ minds on April 4, 2018, was a bankruptcy filing just four days earlier by another merchant-power company. FirstEnergy Solutions had been struggling to turn a profit on its coal and nuclear-power plants. But the decision to put FirstEnergy Solutions into bankruptcy was also connected to the desire of its parent company to exit the merchant-power business and transform itself into a fully regulated utility company. No such machinations affected Talen Energy.

Considering these facts, bond investors’ strong aversion to the Talen Energy bond was akin to children shunning a playmate because he has cooties. But money managers who don’t specialize in distressed debt like to be able to tell prospective clients that they’ve avoided most or all defaults in their investment universe.

In striving to maintain that kind of record, portfolio managers wind up dumping bonds with even a slight smell of possible default. Non-distressed managers’ tendency to err on the side of caution – and shun a bond for all the wrong reasons – creates sensational outcomes like the Talen bond’s 46.90% return for distressed specialists who can coolly make the risk-reward assessments free of any extraneous considerations.

To make this case study complete, let me note that Talen Energy did indeed file for bankruptcy on December 12, 2022, more than three years after the conclusion of the 12-month period I’ve been discussing. During 2022, natural-gas prices rose 160%. Talon’s margins and liquidity were severely squeezed as a result. Talon emerged from bankruptcy five months later.

Merchant power is a volatile, commodity-price-sensitive business. That was a key factor in Talen’s highly speculative B rating in 2018 and contributed to its highly elevated bond yield. If natural gas prices had skyrocketed then as they did in 2022, the 6.50% bond’s return would have been tragic rather than heroic. But a comprehensive weighting of the upside and downside led to the conclusion that the bond was trading way below its intrinsic value.

That’s not a rare occurrence in the distressed-debt market, as evidenced by the highly gratifying performance of Distressed Investing recommendations over the last few years.

Of the seven open bond positions in the Distressed Investing portfolio at the moment, six are in the green, for an average return of 21.5%. Marty and his team will be adding a new recommendation to the Distressed Investing portfolio in September… If you’re not already a subscriber, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on becoming a subscriber.

A Historic Gold Announcement

Is About to Rock Wall Street

For months, sharp-eyed analysts have watched the quiet buildup behind the scenes. Now, in just days, the floodgates are set to open. The greatest investor of all time is about to validate what Garrett Goggin has been saying for months: Gold is entering a once-in-a-generation mania. Front-running Buffett has never been more urgent – and four tiny miners could be your ticket to 100X gains.

Be ready before the historic gold move. Click here to get Garrett’s Top Four picks now.

Three Things To Know Before We Go…

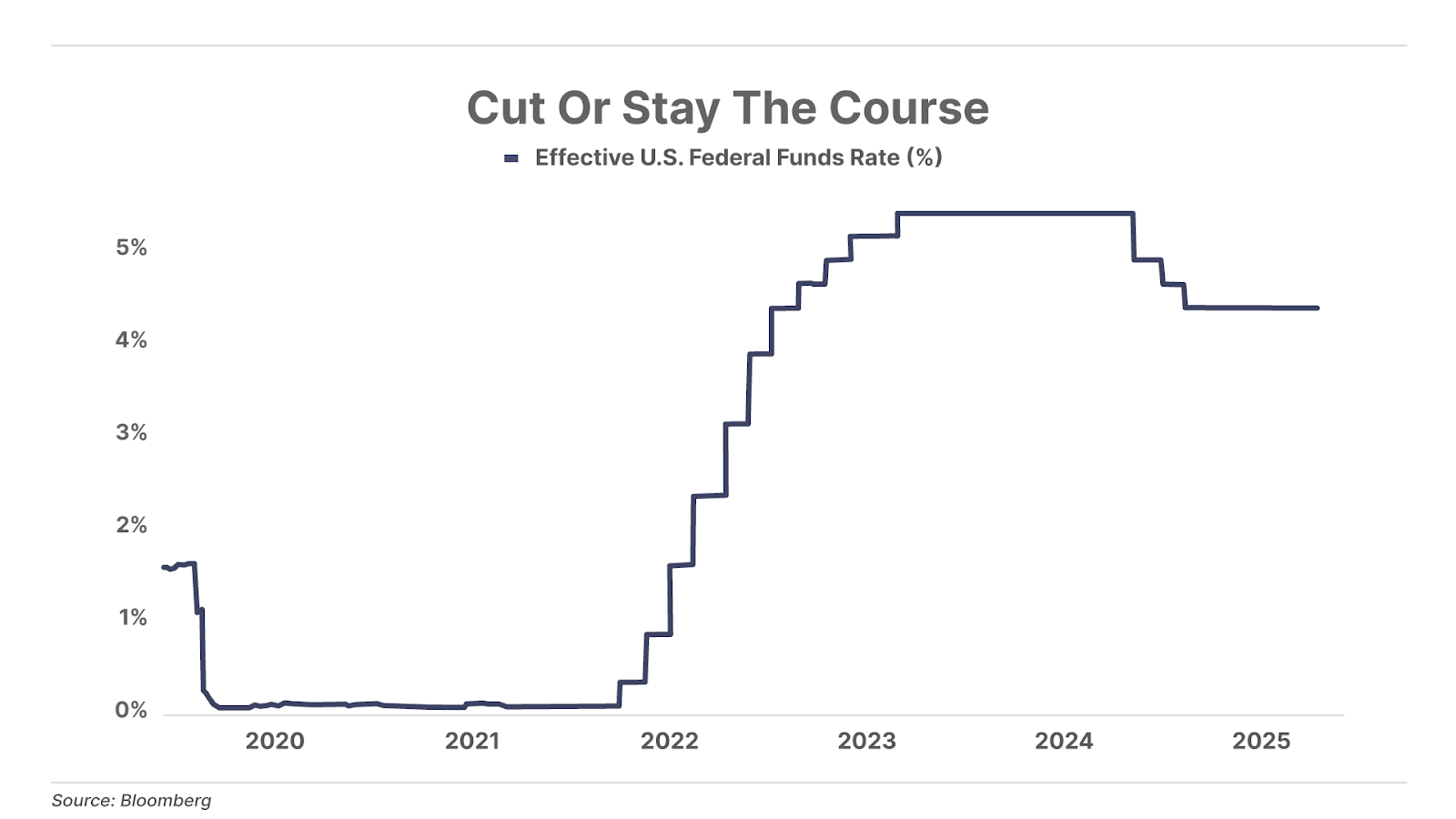

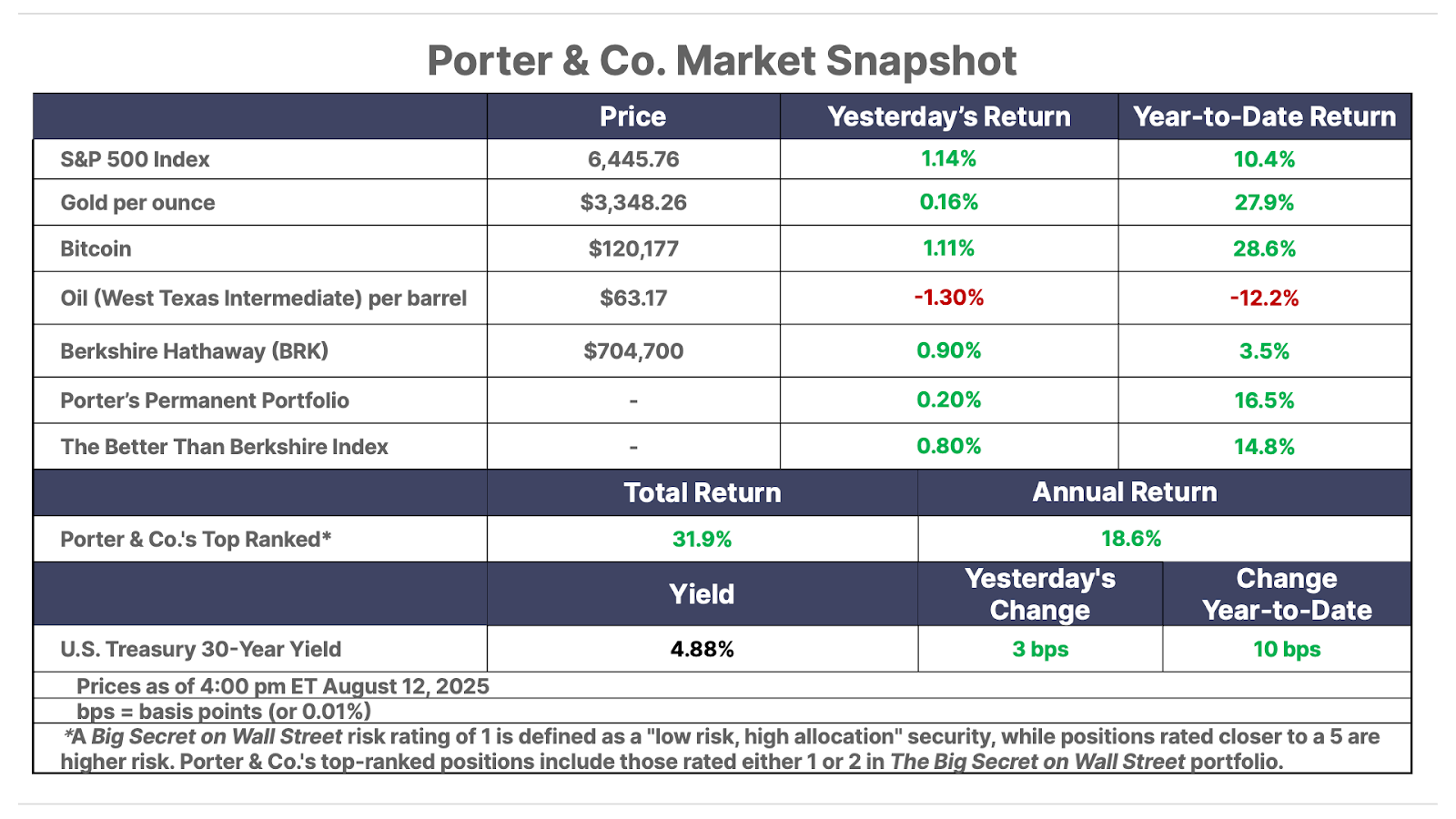

1. Lower inflation clears the way for a rate cut. July’s consumer price index (“CPI”) inflation slowed to 2.7%, below consensus forecasts of 2.8% yet still above the Federal Reserve board’s 2% target. Because of this news, Treasury Secretary Scott Bessent is now urging the Fed to cut interest rates by 150 basis points – from around 4.5% to 3%. Markets think some sized cut is inevitable… pricing in a 99.9% probability of a September cut. Fed Chair Jerome Powell and others will decide then whether to tap the gas and risk higher inflation or to stay the course and disappoint the market.

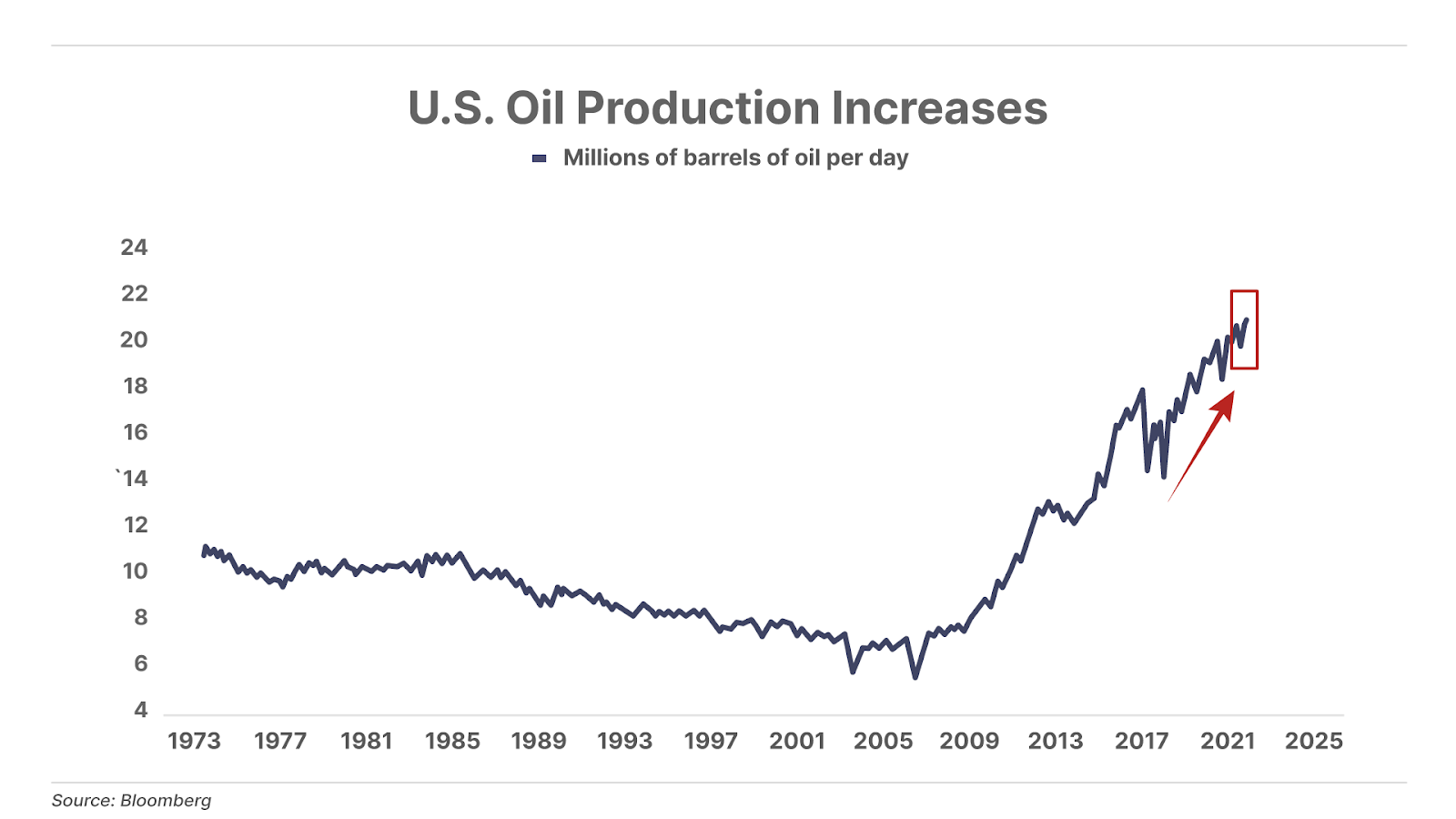

2. “Drill, baby, drill.” U.S. oil production is booming – hitting a record 21 million barrels per day in May. This production growth is occurring despite the number of active drilling rigs and fracking crews falling to four- and five-year lows, respectively. U.S. shale companies are the big producers and continue to become more and more efficient.

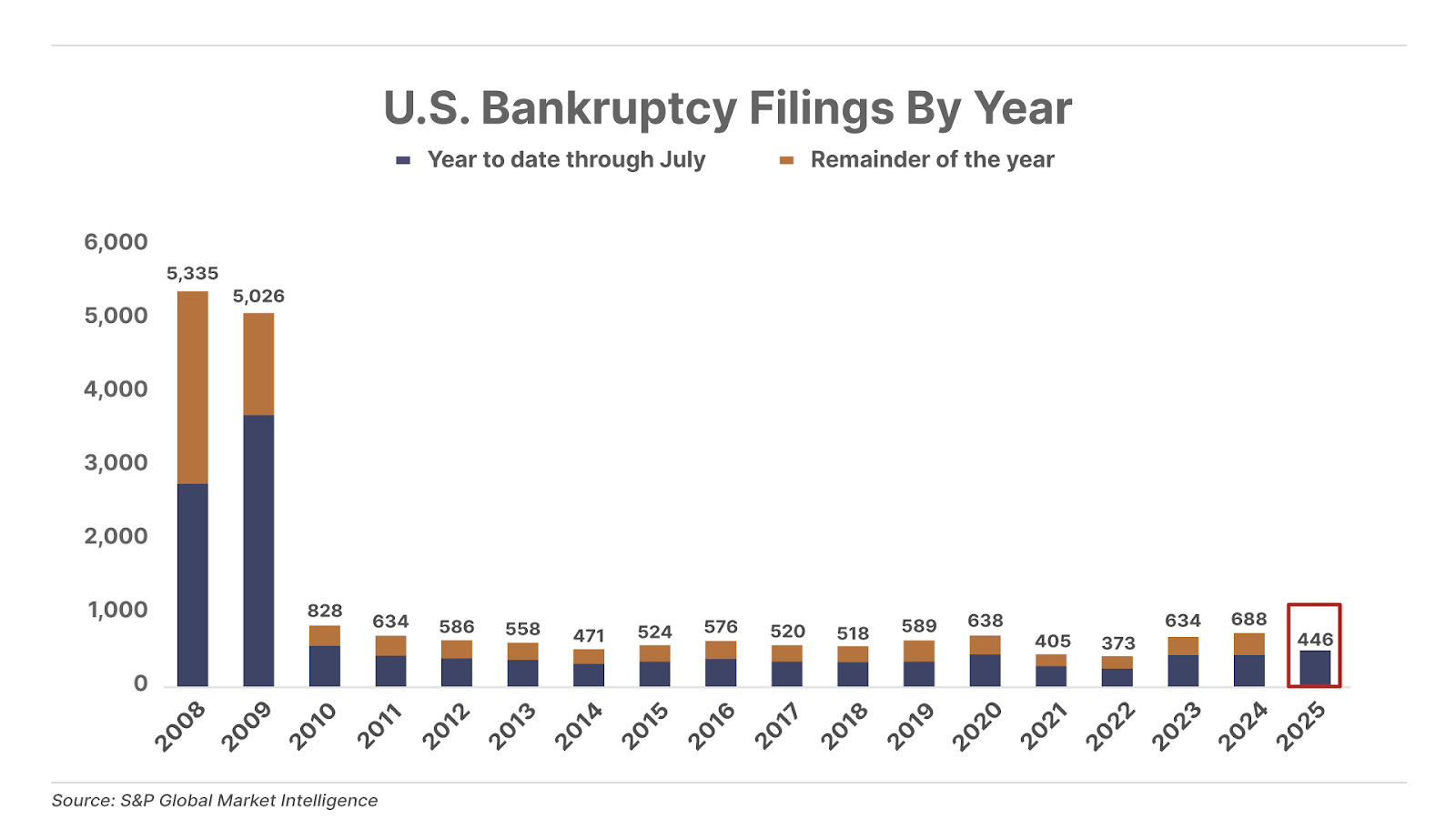

3. A bull market in bankruptcy. So far this year, 446 large U.S. corporations (those with over $50 million in assets) have filed for bankruptcy. That’s the highest year-to-date total since 2009, during the depths of the Global Financial Crisis. While the Magnificent 7 technology stocks continue leading the market to new highs on the back of the boom in artificial intelligence, average consumers and businesses continue to struggle in an otherwise lackluster economy.

And One More Thing… Market Concentration Madness

Nvidia (NVDA) and Microsoft (MSFT) now account for a record 15.4% of the overall valuation of the S&P 500 – the highest concentration ever for just two companies. This growing dominance could be masking a struggling broader index, and a stumble by either could weigh heavily on the overall market.

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

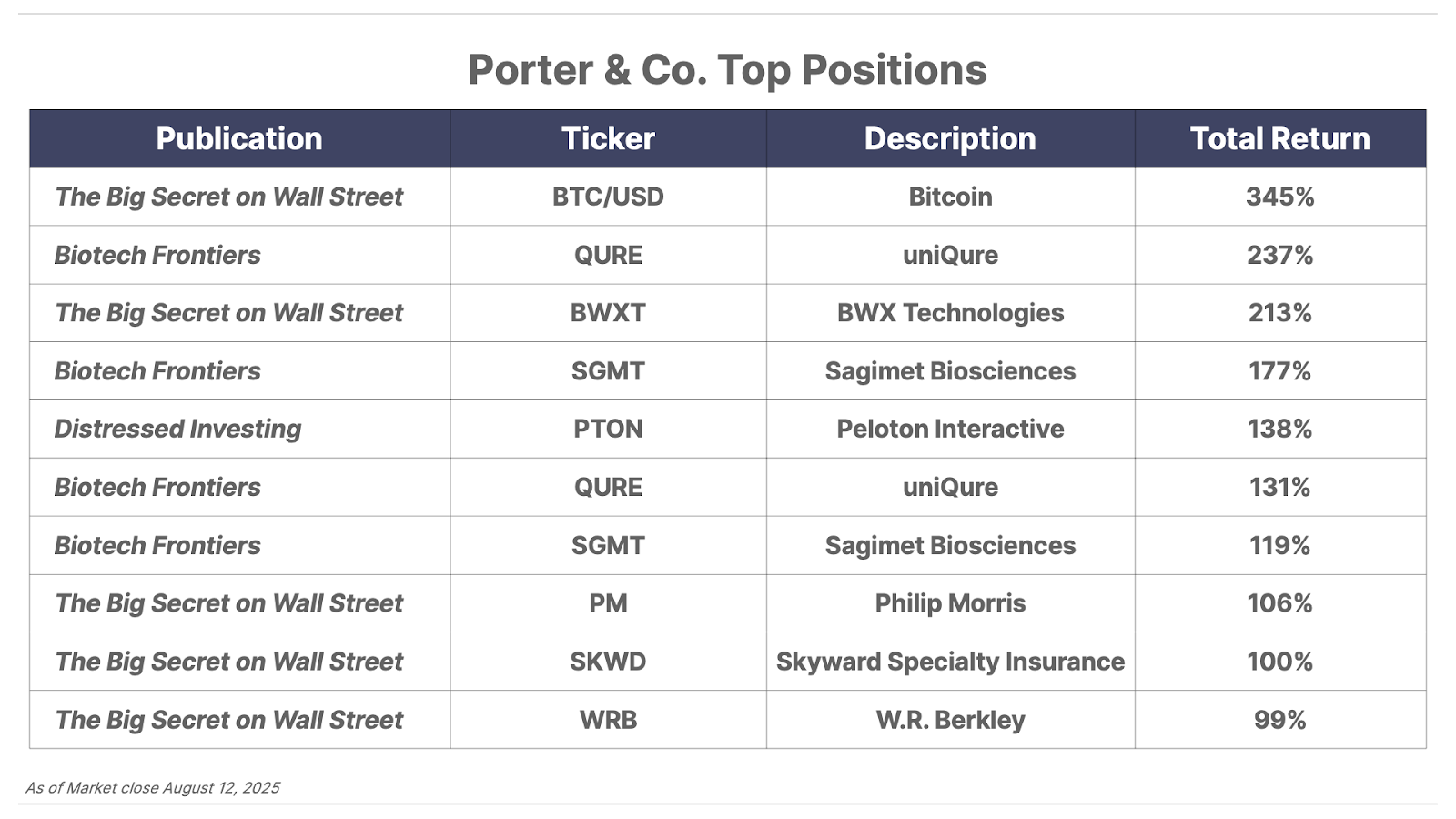

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.