Tesla’s rivals have been investing heavily in their own EV production and are now, for the first time, challenging the company in quality, innovation, and performance. This means that Tesla is now staring down a threat unlike any it has seen before.

Elon Musk’s “Genius” May Need A Recharge

Editor’s Note:

We don’t recommend short positions at Porter & Co. But for sophisticated investors who can implement short-selling within a disciplined risk management framework, shorting can help hedge a portfolio.

Tesla suffers from declining margins, poor product quality, and heightened competition – making the stock’s stratospheric valuation even less defensible. We believe a short position in Tesla could offer protection against a coming bear market… as we explain below.

It was – supposedly – a “horrible, horrible accident.”

That’s what movie director Rian Johnson told Wired magazine.

But in truth, it’s pretty clear that the main character in Johnson’s latest Netflix hit whodunit, “Glass Onion,” is based on none other than Twitter and Tesla owner Elon Musk.

The Musk-like character in the film – self-absorbed tech billionaire Miles Bron, who lives in a futuristic glass castle on a private island and dabbles in space travel and science-fiction cars – is just a little too on-the-nose to be an “accidental” resemblance.

Tellingly, Bron is also really, really dumb – though he manages most of the time to come across as really, really smart.

The “whodunit” lightbulb (spoiler alert!) goes off when the detective in the flick, played by former James Bond Daniel Craig, realizes that Miles Bron is, in fact, not a genius at all…

“His dock doesn’t float. His wonder fuel is a disaster. His grasp of disruption theory is remedial at best. He didn’t design the puzzle boxes. He didn’t write the mystery. Et voila! It all adds up. The key to this entire case. And it was staring me right in the face.

Like everyone in the world, I assumed Miles Bron was a complicated genius. But why? Look into the clear center of this glass onion. Miles Bron is an idiot!”

The real Elon Musk may not be an idiot, but despite (or because of?) his brilliance, he’s definitely made some questionable decisions over the past few years.

And right now, the iconic company synonymous with his name, Tesla Inc. (TSLA), is taking the fall.

Warning! Battery Low!

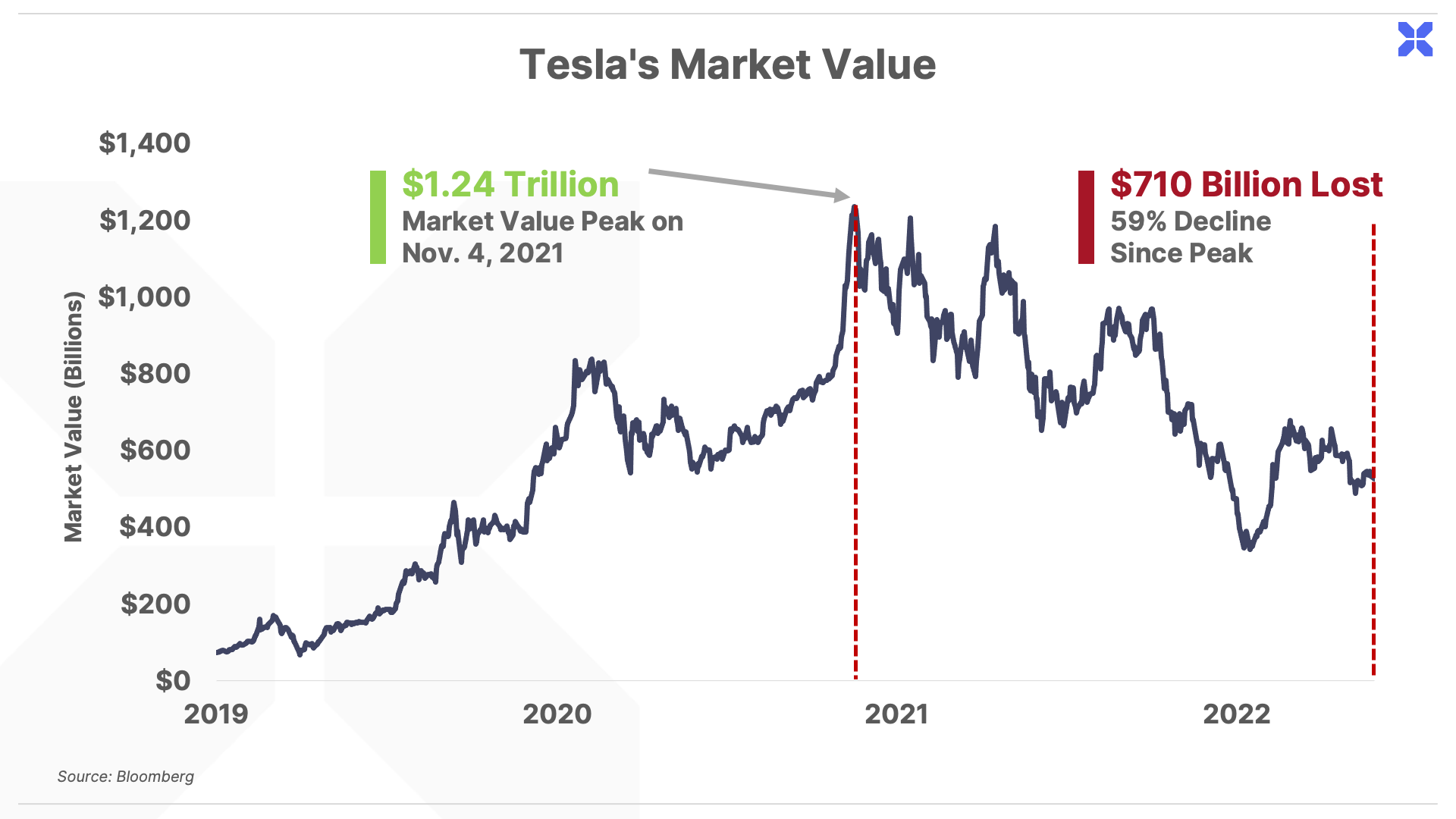

Tesla shares took off during the post-Great Financial Crisis bull market. Between its initial public offering (IPO) in June 2010 and the end of 2021, Tesla shares rose a mind-boggling 32,500% – the equivalent of a 60% annualized return for 11 consecutive years.

At its peak, Tesla’s market capitalization was over $1.2 trillion – one of just five public companies in U.S. markets ever to achieve this 13-figure feat – and Musk’s net worth was more than $300 billion, making him for a time the world’s wealthiest man, according to Forbes.

But Tesla’s fortunes have reversed since the bull market morphed into a bear. The shares have fallen roughly 60% from their November 2021 peak.

This decline has erased more than $700 billion from Tesla’s market value. It also earned Musk a dubious honor: His $182 billion drop in net worth officially set a Guinness world record for the largest loss of personal fortune in history. (Like everything else Musk does, go big or go home.)

Admittedly, this isn’t the first rough patch the company – or Musk – has experienced.

Over the past decade, Tesla has faced numerous challenges – production headaches, nearly running out of cash, Securities and Exchange Commission (SEC) investigations, and a chronic inability to turn a profit selling cars – but somehow come out stronger on the other side.

Throughout all of these previous speed bumps, though, Tesla enjoyed one key advantage – it was the only game in town.

Today, though, the electric vehicle (EV) market has become saturated by compelling offerings from legacy automakers. And Tesla now faces the most significant challenge since its inception – real competition.

Ford T-Bones Tesla

Tesla has a long and well-documented history of cutting corners in research and development in order to inflate its margins, which has led to frequent mechanical issues and recalls. (Just this week, Tesla recalled 1.1 million vehicles in China – virtually all the cars it’s sold in the country – due to a potentially severe braking defect.)

Still, for the better part of a decade, if you wanted an EV with a reasonable battery range and performance on par with (or better than) a vehicle with an internal combustion engine, Tesla was your only real choice.

But that’s no longer the case.

Consumers now have dozens of new EV models to choose from, with more and more coming to market every year.

While Tesla is dealing with an endless series of problems ranging from brake and wheel failure to shoddy paint jobs to a tendency for its cars to burst into flames unexpectedly, companies like Ford are stepping into the breach.

The 120-year-old American institution has quietly made a name for itself in the EV market over the past several years…

Its first big offering was an electric take on its famous Ford Mustang in 2019: the Mustang Mach-E sport utility vehicle (SUV). Car and Driver just called the latest edition of the Mach-E “a great alternative” to Tesla’s Model Y SUV “thanks to its charming looks, luxury-level interior, and range as well as performance.”

Ford followed that up with an all-electric version of its popular F-150 truck in 2021. The F-150 “Lightning” was quickly named MotorTrend Truck of the Year and has already become the best-selling EV truck in the U.S.

Meanwhile, Tesla has been teasing (and repeatedly delaying) the release of its EV truck – the unusual-looking “Cybertruck” – for more than four years and counting.

Ford has also developed its own hands-free driving technology. Known as “BlueCruise,” Ford’s technology was named “the single best hands-free system for an EV” by Consumer Reports earlier this year.

That’s opposed to Tesla’s $15,000 “Full Self Driving” (FSD) system, which isn’t actually “hands-free” in any situation. In fact, FSD is currently subject to a National Highway Traffic Safety Administration recall whose filing is ominously titled “Full Self-Driving Software May Cause Crash.”

Tesla’s No Longer A Special Snowflake

Of course, Ford is just one of many competitors gunning for Tesla. And while Tesla is still the dominant leader in EV sales, its market share has been rapidly declining.

According to Experian’s Automotive Market Trends report, Tesla’s share of the U.S. EV market has fallen from around 80% in 2020 to just 64% at the end of 2022. Counterpoint Research’s Passenger EV Sales Tracker shows a similar trend globally, with Tesla’s share falling from nearly 20% in 2020 to just 12% last year.

This shift reflects a sharp slowdown in Tesla’s sales growth, from 71% in 2021 to 40% in 2022. That’s well below the company’s stated long-term projections of 50% annual growth.

Tesla has responded to increased competition by slashing prices, in the U.S. and in China. It’s cut costs across all of its models five times so far this year alone in a bid to spur additional sales. And that has already delivered a big blow to its profitability.

Tesla’s Q1 2023 net income fell by 24% from Q1 2022, from $3.3 billion to $2.5 billion. This drop in profitability came despite Tesla selling more cars and growing its revenues by 18%, to $20 billion, over the same period. In other words, Tesla is now being forced to compete on price and sacrifice profitability in order to keep the “growth story” alive – moving more units, but generating less income.

On Tesla’s Q1 earnings call, Musk guided for further price cuts, saying he could theoretically cut margins to zero. He also insisted price cuts had been positive for sales so far. (Though Tesla’s own reporting suggests otherwise. It shows “finished goods” inventory – completed cars it has not yet sold or delivered to customers – rose by $1.1 billion (32%) since the end of last year.)

In any case, cutting prices is likely to be a losing strategy.

First, in a prolonged price war, Tesla would be at a significant disadvantage. All its eggs are in the EV basket – while its competitors have other “legacy” vehicles to fall back on if EV sales slow.

But more importantly, if Tesla keeps cutting prices, it risks destroying its “brand power.” Consumers will eventually see it as just another mass-market vehicle like a Honda or Kia, which means it won’t be able to charge higher prices in future.

(It’s worth noting that Tesla has implemented a handful of modest price increases on some vehicles in the past couple of weeks. So perhaps the company has started to realize the folly of these prior moves.)

On the other hand, if Tesla instead acts to protect its margins with new offerings and a return to premium pricing, sales are likely to slow even further.

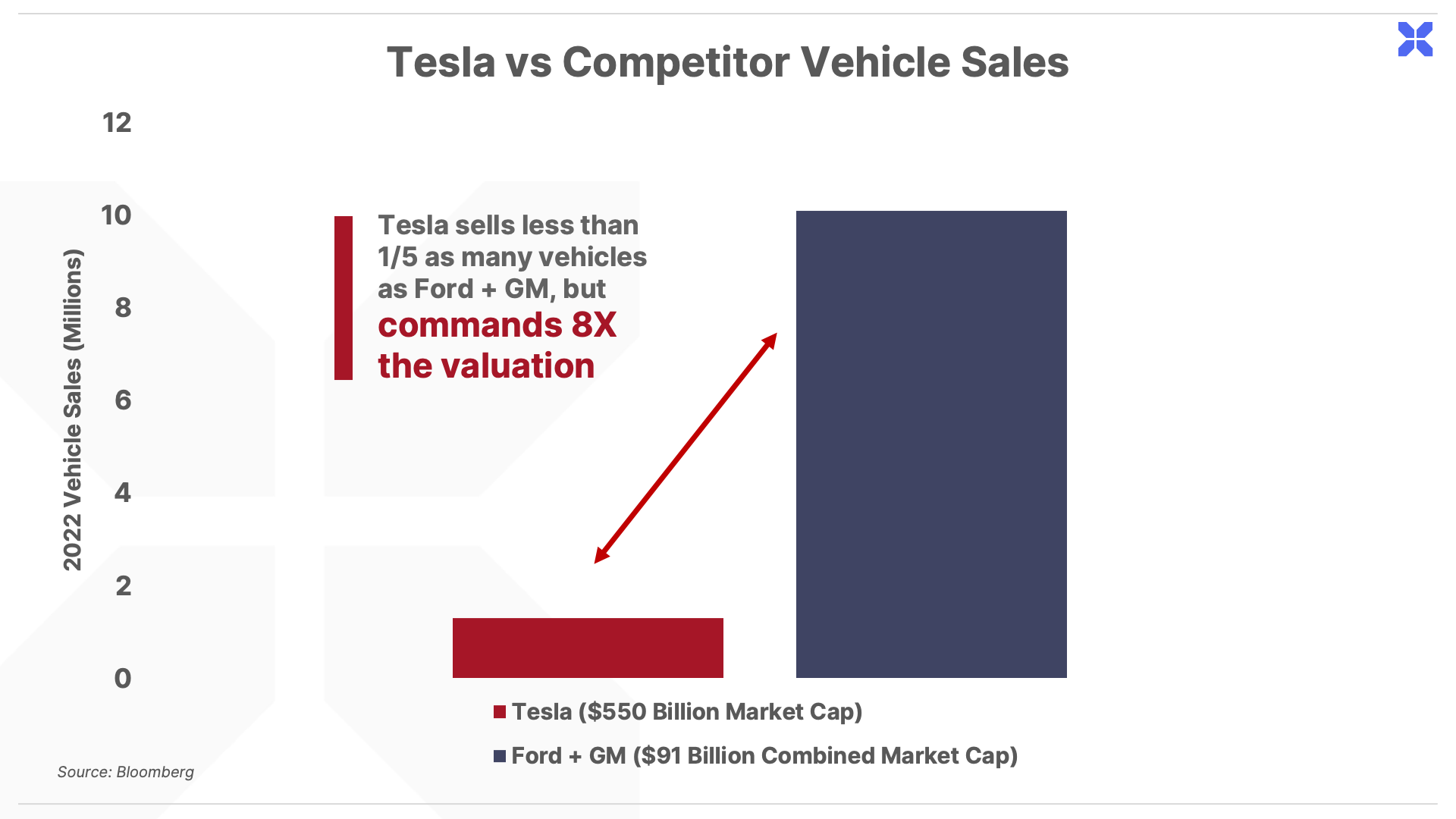

Despite the sharp decline in Tesla shares last year, the company is still trading at a market cap of more than $500 billion. For context, Tesla sold 1.3 million vehicles last year. General Motors and Ford combined sold 10.1 million cars, and together, they trade for a combined market capitalization of just $91 billion. In other words, despite Tesla selling 85% less vehicles than Ford and GM, it commands a valuation of eight times Ford and GM combined:

And therein lies a key risk to the Tesla thesis. Most automakers trade for a deep discount to the broader stock market, including GM’s 5x earnings multiple and Ford’s 6x earnings multiple (compared with a 19x earnings multiple for the S&P 500).

These discounted valuations reflect the fact that car-making is generally a bad business. It’s a highly competitive industry that requires huge sums of capital to constantly introduce new vehicles each year (or risk losing market share, as Tesla is finding out the hard way). It’s also a low-margin and highly cyclical business, where razor-thin profit margins can quickly turn into buckets of red ink when the economy turns and auto demand drops.

Tesla’s monstrous $550 billion valuation reflects a roughly 50x earnings multiple. This is based on the narrative that the business can continue growing sales at 50% per year while also maintaining its historically thick margins. This lofty valuation also implies that Tesla can continue growing regardless of the ups and downs in the economy.

But this narrative is falling apart in real time. In order to keep the growth story alive, Tesla must now begin investing huge sums of money to introduce new vehicle models to keep up with the competition. Otherwise, it will be forced to continue slashing prices to move volume.

In either case, the glory days of a long runway of high-margin growth are now in the past. With legacy automakers now heavily in the EV game, Tesla is just like any other car company, and deserves to be valued like one.

How Tesla Shares Can Help Hedge Against a Bear Market

Our recommendation to most investors is to simply avoid investing in Tesla. But for more sophisticated investors, shorting shares may offer an attractive hedge against a portfolio of long positions. Short selling involves borrowing shares, selling at the current market price, with the aim of buying those shares back at lower prices, thereby profiting from a decline in the share price.

Short selling can offer protection in a bear market, by providing profits from short positions that offset losses from long positions elsewhere in the portfolio. The best short-selling candidates come from weak companies with the potential to fall further and faster than the long positions in a portfolio.

We believe Tesla meets these criteria, given the elevated risks to its business model, and its recent trading history.

From the start of the bear market in the S&P 500 in January 2022, Tesla shares have fallen by 51% compared with a 13% loss in the S&P 500. A pairs trade involving a long position in the S&P 500 and an offsetting short position in Tesla would have yielded a net profit of 38% since January 2022 – not only insulating against the bear market, but creating a net profit, despite the overall declines in the broader market.

But this strategy comes with risks. The potential losses from short selling are unlimited – the more prices go up, the bigger the short position becomes, and losses can quickly escalate.

That’s why position sizing and risk management are critical. A properly constructed portfolio would involve a diversified basket of long and short positions, so that no single idea can deliver a fatal blow to an investor’s capital.

A stop-loss is also essential for short positions – a predefined level where an investor automatically closes the position to prevent further losses.

In the case of Tesla, we would recommend placing a stop loss on a short position at 50% above Tesla’s recent trading price of $173 per share, or $260 per share.

We recently recommended the bonds of one of Tesla’s key EV competitors in Porter & Co. Distressed Investing. In comparison to Tesla’s margin collapse in Q1 2023, this company enjoyed a substantial uplift in its profit margins. And it trades for a much more compelling valuation of just 6x earnings, versus Tesla’s 50x earnings multiple.

Best of all, the security we recommended is a convertible bond – which offers additional downside protection versus owning shares, while still retaining upside from share price appreciation.

Distressed Investing recommendations are only available to Partner Pass members. If you’re not a Partner Pass member, learn more about Partnering with us here.

Porter & Co.

Stevenson, MD

P.S. If you’d like to learn more about the Porter & Co. team – all of whom are real humans, and many of whom have Twitter accounts – you can get acquainted with us here – or email our “Mailbag” address at any time: [email protected].