Surviving The Deepest And Longest Biotech Bear Market

Sharing One Of The Most Asymmetric Investments Ever

| This is Porter & Co.’s The Big Secret On Wall Street, our flagship publication that we publish every Thursday at 4 pm ET. Once a month, we provide to our paid-up subscribers a full report on a stock recommendation, and also a monthly extensive review of the current portfolio… You can go here to see the full Big Secret portfolio. Every week in The Big Secret, we provide analysis for non-paid subscribers. If you’re not yet a paid subscriber, to access the full paid issue, the portfolio, and all of our Big Secret insights and recommendations, please click here… At the end of this week’s issue, paid-up subscribers can find our Top 3 Best Buys, three current portfolio picks that are at an attractive buy price. Click here to learn how you can access them without paying the usual $1,425 annual subscription cost. |

We’re bringing Big Secret readers a special issue this week – a report from our colleague Erez Kalir, editor of Porter & Co.’s Biotech Frontiers.

If you’ve been with us for long, you’ve likely heard about the remarkable track record Erez has racked up over the past two years… he’s helped his Biotech Frontiers subscribers make a fortune with an incredible string of double- and triple-digit winners, including gains of 49%, 50%, 54%, 60%, 64%, 85%, 88%, 98%, 131%, 165%, and 237%, so far.

But what you may not realize is that Erez has accomplished this remarkable feat during the deepest, broadest, and longest biotech bear market in history. The average biotech stock has been crushed over this period, with many falling 70%, 80%, even 90%.

In this week’s issue, Erez explains why the biotech industry has been under such tremendous pressure… and, more importantly, why better days may finally be just around the corner.

Erez takes it from here…

In early 2024, I (Erez) emailed the CEO of a public biotech company who has been a long-standing friend. A doctor by training, he’s been in the world of life-sciences entrepreneurship for five decades now and has made his shareholders billions of dollars over that time. He is one of the biotech leaders I most admire – a brilliant scientist with a nose for making money and a strong ethical spine.

Over the prior year, his company’s stock price, like that of many other public biotech companies, had declined 80%. He’s the company’s largest shareholder with an 11% stake, so I knew he felt the financial pain personally. We hadn’t connected in months and I was writing simply to check in on him. Here is an excerpt from his reply:

“Dear Erez: Great to hear from you. It has been an unreal, even insane period. The industry has never seen interest rate increases anywhere near this magnitude. It has devastated development-stage biotech.”

It’s notable that my friend – one of the gray-haired wise men of the life-sciences industry – would begin his note to me by referencing interest rates. If you hope to invest successfully in life-sciences stocks, it’s crucial to understand why. Let me explain . . .

The Importance Of Interest Rates To Biotech Investments

Interest rates are like financial gravity. When interest rates are low, stocks float upward. When rates are high and gravity is strong, valuation multiples collapse – and stocks fall back to Earth.

But while physical gravity causes all objects to fall at the same constant rate (9.8 m/s2 ), financial gravity has a stronger effect on some kinds of stocks than others. And life-sciences stocks working to bring novel drugs and therapies to the world tend to be among the hardest hit.

To grasp why, it’s helpful to think of development-stage biotech stocks as long-duration equities… or the equity siblings to long-duration bonds – one whose maturity is far off in the future. As most investors know, these bonds are especially sensitive to changes in interest rates.

A long-duration equity is one whose free cash flows (“FCF”) are far off in the future. And this describes most development-stage biotechs. In the near future, they have to spend a lot of money up front – performing R&D, running clinical trials, paying lawyers to help them obtain regulatory approvals, and eventually launching their new product. All of this is money out the door – before any money comes in the door.

If they’re successful, their FCF tends to lie far out in the future. These FCFs can be astronomical for an effective new drug. But they have to be discounted back to the present. And as anyone who’s built a financial model knows, the more periods you have to discount your FCF back, the more sensitive the model is to changes in your discount rate – or in this case, to the U.S. interest rates that are the foundational benchmark for every discount rate in the world.

All of which brings us back to what the billionaire founder of Oak Tree Capital, Howard Marks, has called the sea change in our interest rate environment.

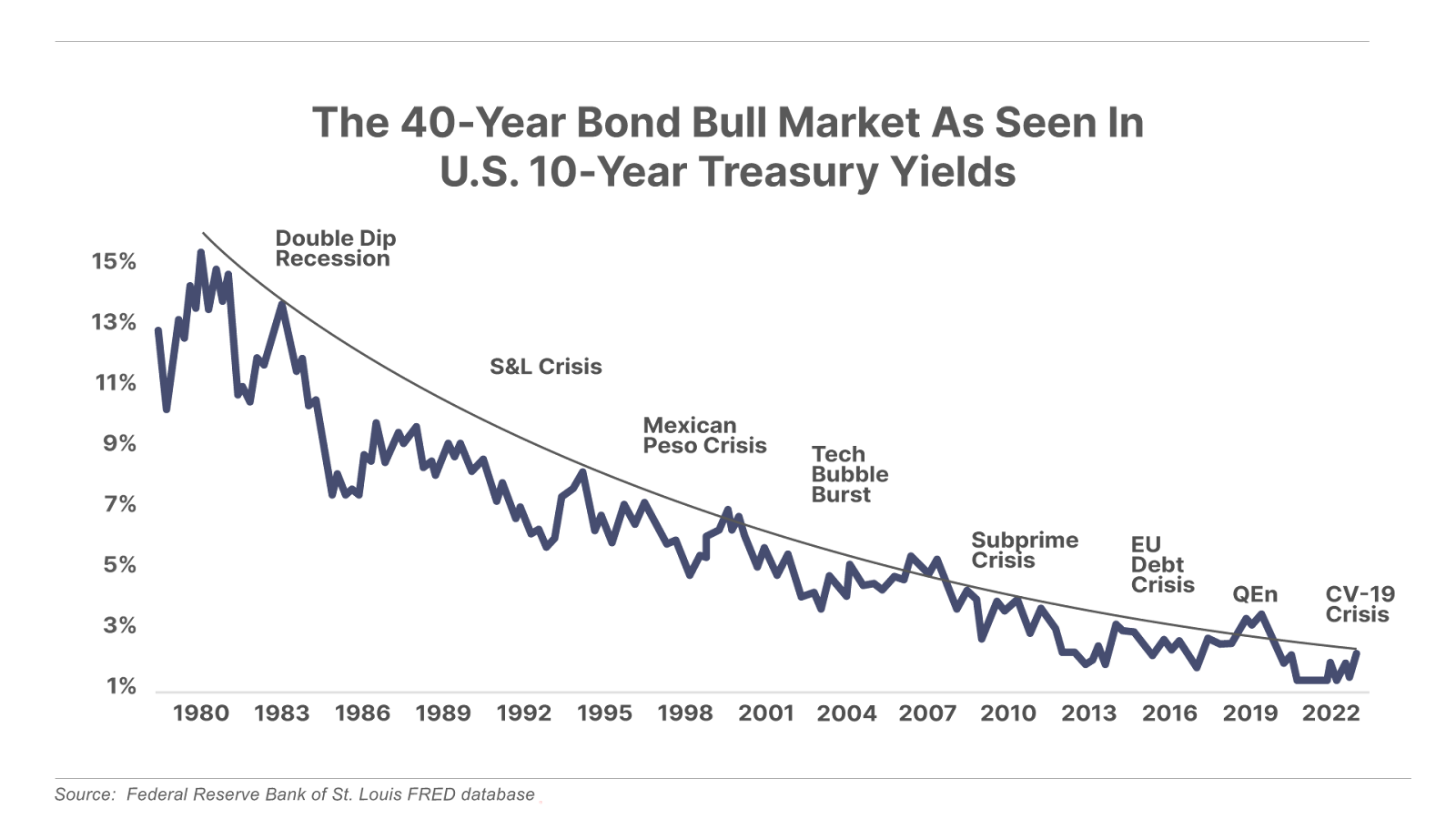

A History Of Modern Interest Rates In Five Minutes Or Less

For four decades – from 1982 to 2021 – U.S. interest rates mainly moved in one direction: down.

In the early 1980s Fed Chair Paul Volcker raised interest rates dramatically in a bid to slay inflation, which had haunted the U.S. economy for much of the 1970s. The Fed funds rate peaked at 20% in June 1981. And that did the trick: Volcker’s draconian interest rate medicine banished inflation.

Starting from the Volcker high of 20%, successive Fed chairs after Volcker… first, Alan Greenspan, then Ben Bernanke, then Janet Yellen, now Jerome Powell… have cut interest rates every time they’ve perceived the U.S. economy to encounter a problem. Bernanke, of course, cut rates all the way to zero during the Global Financial Crisis.

Believing that the U.S. needed an even more powerful stimulus, he then proceeded to print $4 trillion. But whereas Bernanke’s zero-percent rates and trillion-dollar printing press were advertised as “emergency measures” in response to the Global Financial Crisis, they ended up becoming business as usual for the Fed for the ensuing decade – long after our economy recovered from the mess of 2008.

Fed Chair Powell, faced with the COVID-pandemic shock to our economy in 2020, dusted off Bernanke’s playbook and printed $4 trillion in less than a quarter of the time it took the Bernanke Fed to do so.

But this time, the Fed’s money printing was accompanied by $2 trillion of the Biden administration’s fiscal stimulus, as well as supply shocks to both the U.S. labor force and global supply chains.

The result was a headline consumer price index (“CPI”) inflation rate of 9.1% in June 2022 – the highest rate since 1981.

Chair Powell may be many things, but he does not want to be remembered as the Fed chair on whose watch the inflation bogeyman returned to haunt America as it did during the 1970s. And so, faced with the highest CPI inflation rate in 40 years, Powell borrowed a page from Volcker. Powell proceeded to raise the Fed funds rate from 0% in March 2022 to 5.25% by the end of 2023, the steepest Fed rate hikes since the Volcker era.

The Biotech Bear Market

Let’s return to my CEO friend’s note with which we began our discussion of interest rates: “It has been an unreal, even insane period. The biotech industry has never seen interest rate increases anywhere near this magnitude.”

My friend is not exaggerating. The biotech industry didn’t exist in the early 1980s. Genentech, the granddaddy of modern biotechnology companies, IPO’d in October 1980 – and at the time it had no direct competitors. So the severe Fed interest rate hikes of 2022-2023 truly were a first for the biotech sector.

And because we’ve now understood how biotech stocks are long-duration equities – similar to long-duration bonds in their sensitivity to interest rates – we can also appreciate the punchline of my friend’s note: those interest rate hikes have “devastated” biotech.

The bear market in biotech that we’re in the midst of today is the longest, biggest, and most punishing bear market in the history of biotech. While the Nasdaq Biotech Index (NBI) is down 15% from its peak in September 2021, small-cap biotech stocks in the Russell 3000 are down 45%, and biotech stocks removed from the Russell 3000 because they no longer meet its inclusion criteria are down significantly more. Large-cap biotech has underperformed the S&P 500 by 66% since 2023.

Approximately 60% of the global biotech sector now trades with an enterprise value (“EV”) of $100 million or less. The number of biotech IPOs, and the amount raised in these IPOs, is down over 80% from their 2021 peaks. Measured in length, the current bear market has stretched over 1,600 days – almost four times longer than the average duration of prior biotech bears, and the longest biotech bear market on record.

But the most startling statistic may be this: Of the public biotech companies trading in U.S. markets today, roughly 40% (or almost 300 companies) trade with a negative EV.

A company’s EV is defined as its market capitalization less net cash. So a negative EV means there’s more net cash on the company’s balance sheet than the entire market capitalization of the company.

Over my two decades in investing, it’s been exceptionally rare to come across any meaningful swath of public companies trading with negative EVs. Why? Because a negative EV implies that if you could buy the whole company at once, you could shut it down, take the cash on its balance sheet, and come out ahead – i.e., you could get paid that net cash for shutting the company down.

Finding a stock market sector with a meaningful number of negative-EV companies can only mean one thing – that sector is the subject of the most extreme fear and loathing by investors. In fact, investors are so repelled by the sector, they’re ascribing negative value to many of its companies.

Which is a perfect opportunity for us.

Self-made billionaire and legendary investor Shelby Collum Davis once remarked, “You make most of your money during a bear market. You just don’t realize it at the time.”

In Biotech Frontiers, we’ve been leaning into Davis’ maxim while we can. And while I’m incredibly proud of what we’ve achieved so far, I believe we could do even better in the months ahead.

That’s because the Federal Reserve is likely to start cutting interest rates next month. And just as high interest rates gutted the biotech industry, lower rates will likely usher in a new biotech bull market.

In a real bull market, the small biotech stocks we cover are going to absolutely soar. Which means as great as we’ve done in Biotech Frontiers to date, the best is yet to come.

Editor’s note: The potential for a new biotech bull market means there has never been a better time to become a Biotech Frontiers subscriber. But that’s not the only reason to consider joining Erez’s service today…

As we mentioned upfront, since Erez launched Biotech Frontiers, he’s found great opportunities that most of the investing world has missed. Many of these recommendations have soared 100% or more… But Erez isn’t just a biotech expert.

Living in the San Francisco Bay area, the tech capital of the world, Erez has also immersed himself in the growing fields of artificial intelligence, blockchain, and computing… And he is finding lots of opportunities that he’d like to recommend to readers, but until now he has been limited, for the most part, to biotech.

But not anymore.

After meeting with Erez this August, Porter has decided to expand Biotech Frontiers into, well, new frontiers. To that end, we are renaming the advisory Tech Frontiers.

As part of that new frontier, Erez has uncovered a massive, under-the-radar opportunity for his subscribers – one that he’s calling one of the most asymmetric opportunities of his career.

It’s a multi-billion-dollar asset hiding inside a boring blue-chip company that has been completely mispriced by Wall Street. But with five imminent catalysts approaching, he believes this asset is on the verge of a major re-valuation… one that could happen any day now, and send this little-known stock up hundreds of percent.

As you’ll see, there is no one more qualified than Erez to share this story. He recently sat down with Porter to explain more about this opportunity. Get all the details here.

New to The Big Secret Portfolio? Start With Our Top 3 Best Buys Today

Our goal at Porter & Co. is to bring you world-class investment research, focused on “inevitable” businesses that you can buy and hold forever. This is the surest and safest path to building permanent wealth.

While we don’t believe in timing the market, we do keep a constant eye out for bargains. In each edition of The Big Secret, we highlight three current portfolio picks that are at an attractive buy point. We suggest you focus on these.

Since we began compiling and tracking the performance of the Best Buys in February 2023, the companies on the list have generated a 40.4% return, while the overall market, measured with the S&P 500, has produced a 31.1% return.

To see our latest Best Buys, click here to learn how to subscribe.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.