Issue #78, Volume #2

The Case For 100% Upside

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Getting Argentina to the negotiating table… To protect its booming energy business, it needs to settle this case… Oil company shares dropped when the judge forced it to hand over 51% stake… There are real costs that Argentina will feel immediately… The Trading Club members have already seen a nice bump in shares… Nvidia joins the $4 trillion market-cap club… |

On Monday, we previewed the bullish case for litigation financier Burford Capital (NYSE: BUR).

As a brief recap, the major upside catalyst for the business lies in its 38% stake in a $16.1 billion judgment awarded in the YPF case – involving Argentina’s nationalization of its largest oil company, YPF, which caused two hedge funds to lose billions of dollars.

The market has so far assigned low odds of Burford actually collecting on this payment because… well, it’s Argentina we’re talking about. But as we’ll explain today, the odds are stacking up in Burford’s favor toward forcing Argentina into a settlement agreement. The punchline: we believe Burford could be on the cusp of a multi-billion-dollar windfall that could send its shares higher by 100% or more.

If you haven’t yet read part I on Burford, we suggest starting with Monday’s Daily Journal to get caught up with the background on this case.

Let’s begin by laying out the appeal dynamics for this case.

Shortly after the September 2023 judgment that awarded Burford and its plaintiff group the $16.1 billion in the YPF case, Argentina filed an appeal with the Second Circuit of the U.S. Court of Appeals. The typical timeline for cases to move through the Second Circuit is roughly 18 to 24 months. Thus, we expect a ruling on this appeal by year-end, or early next year at the latest.

So far, Argentina has lost every major legal proceeding in this case since Burford launched the suit in 2015. Thus, while a successful appeal is the key risk for Burford, we assign low odds to this scenario. If Argentina loses the appeal, its last legal resort is a final appeal to the U.S. Supreme Court. Here again, this is a low likelihood given that the Supreme Court only accepts about 1% of the cases submitted. But should this scenario occur, it could result in another 12 to 18 months for the case to reach a final resolution.

But there’s a key dynamic at play that could bring Argentina to the negotiating table well before either of these scenarios plays out.

Argentina failed to post a bond as collateral for the $16.1 billion judgment following the September 2023 ruling. As a result, the presiding judge in this case – Judge Loretta Preska of the Southern District of New York (“SDNY”) – granted Burford the right to pursue collection on the judgment while the appeal is pending.

And that’s how Burford was able to get Judge Preska to grant its request for the Argentine government to hand over a 51% stake in YPF on June 30, as a means of partial payment on the $16.1 billion judgment. She gave Argentina only two weeks to comply with the request.

Now, we see low odds of Argentina actually complying with this request. Based on Argentina’s expropriation laws, it’s technically illegal for the country to transfer the YPF shares without a two-thirds vote from parliament.

Judge Preska acknowledged this legal hurdle in her June 30 ruling. But she didn’t consider this to be a big enough roadblock to prevent her from granting the order for Argentina to transfer its YPF shares. She noted that Argentina was obligated to find a way to make good on the ruling, through one of three avenues:

- Obtaining the necessary vote from parliament

- Changing the law

- Striking a settlement deal with Burford

Based on our read of the situation, options one and two are virtually impossible from a political perspective. The real impact here is that it massively boosted Burford’s leverage in bringing Argentina to the negotiating table to strike a settlement deal.

Why? Because this order has thrown into question the future ownership status of Argentina’s crown-jewel energy asset that promises to transform the country into an energy exporting powerhouse.

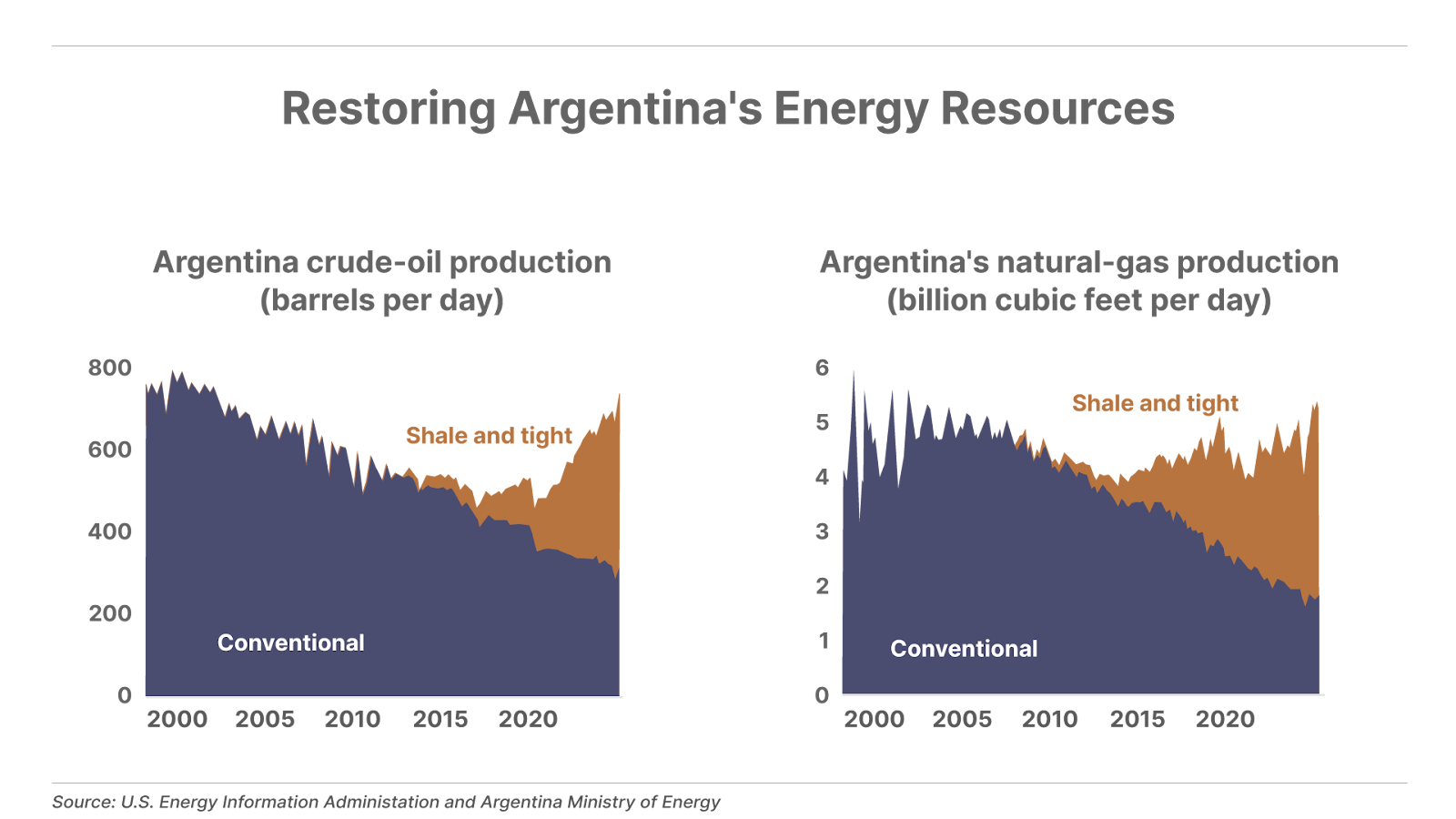

YPF Holds The Key To Argentina’s Shale Revolution

Argentina’s conventional oil and natural gas production has been in decline for decades. But starting in 2021, the country officially launched its own version of the shale revolution when it began developing the Vaca Muerta shale formation, located in the Neuquén Basin in northern Patagonia.

Vaca Muerta holds an estimated 16.2 billion barrels of oil reserves and 308 trillion cubic feet of natural gas. For context, that’s 34% more oil than the Permian Basin’s 12.1 billion barrels of reserves, and nearly 50% more natural gas than the Appalachian Basin’s 214 trillion cubic feet of reserves – the largest oil and natural gas basins in the U.S.

This makes Vaca Muerta one of the largest shale resources in the world. Best of all, this shale is ultra low-cost, with a break-even price of $40 per barrel – making it cheaper than the Permian basin.

And YPF owns the development rights to this ocean of cheap energy. The surge in shale production at Vaca Muerta has single-handedly reversed the decline in Argentina’s oil and gas production over the past few years:

Today, YPF makes up more than half of Argentina’s total oil production and over 70% of the country’s natural gas output.

And over the next five years, YPF plans to double its production volume, while also building out its energy-exporting infrastructure like pipelines and liquefied natural gas (“LNG”) terminals. Just like the shale revolution did for the U.S., the Vaca Muerta shale promises to transform Argentina from a net energy importer to a major global exporter of oil and LNG.

Here’s the challenge for Argentina: bringing all of that oil and gas to the surface will require substantial investment from international investors. YPF expects it will need to raise $10 billion in capital to fund its growth plans over the next five years. It also relies heavily on partnerships with veteran shale drillers like Chevron, ExxonMobil, and Shell – all of which have been instrumental in unleashing the potential at Vaca Muerta.

And if there’s one thing that all of these investors and partners hate, it’s uncertainty. The kind of uncertainty that was just unleashed by Judge Preska’s order for Argentina to surrender its 51% controlling stake of YPF to Burford.

On the day of Judge Preska’s June 30 ruling that ordered Argentina to transfer its 51% stake to Burford, YPF shares fell by 6% – the largest single-day decline since 2020. And with this new cloud of uncertainty over the future ownership of YPF, securing financing for YPF’s growth plans could become increasingly difficult.

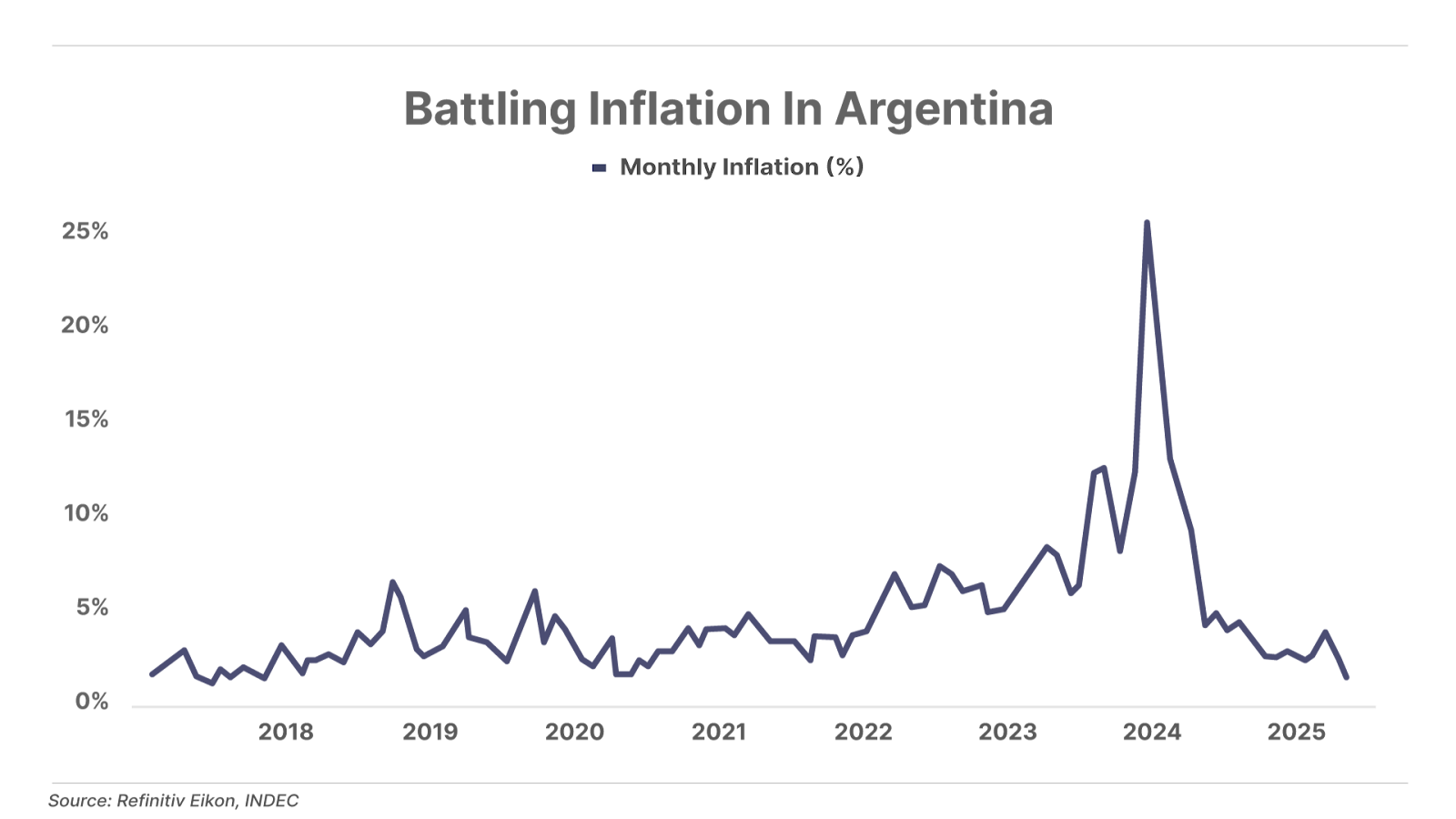

But the implications of the case go beyond YPF. The overhang of this case threatens to derail the masterful turnaround effort President Javier Milei has orchestrated for Argentina’s economy.

Within just a month of taking office in December 2023, Milei slashed government spending and eliminated Argentina’s fiscal deficit. His government has generated a budget surplus every month since January 2024, marking the longest streak in over a decade. And along with Milei’s free-market reforms that have opened up the economy and eliminated price controls, Argentina’s inflation rate has collapsed from a peak of over 25% per month when Milei took office down to a five-year low of just 1.5% by May 2025:

The next big step for Milei is to reopen the country to international investors, and refinance the country’s large debt burden at more attractive interest rates. Argentina’s Finance Secretary Pablo Quirno commented in June that the country is waiting for its government bond yields to fall below 10% to begin issuing more debt starting in 2026.

The country was well on the path to achieving this feat until the June 30 ruling that threatened Argentina’s ownership of its most valuable energy asset. The news sent Argentina’s five-year government bond yield higher by nearly 50 basis points. Meanwhile, the Argentina peso has lost 5% of its value against the U.S. dollar.

Thus, the YPF overhang not only threatens Argentina’s control of its crown jewel energy asset, but it could impose significant costs on the overall economy through higher government borrowing rates and downward pressure on its currency.

These are real costs that Argentina will feel immediately, even as it attempts to continue delaying payment through a lengthy appeal process.

Given all of these factors, we believe it will ultimately lie in Argentina’s best interest to make this problem go away. Based on previous precedent of similar cases, and the strength of Burford’s current negotiating position, we believe it’s reasonable to expect a settlement at roughly 50 cents on the dollar of the $16.1 billion judgment – a windfall of $3 billion to Burford, equal to the total current market cap of the entire company.

In that scenario, we see Burford’s shares rising to a $6 billion valuation, or approximately $28 per share. That would reflect a 20x earnings multiple, which we believe is a conservative estimate of the fair value of its shares.

And what about the downside risks? Say, if Burford loses the appeal, or Argentina simply defaults on the judgment and fails to pay? Well, YPF is just one of the assets in Burford’s $7.4 billion portfolio. It’s also worth noting that the company’s all-in investment is approximately $70 million, and it has already sold off a portion of its stake to other hedge funds for $236 million, securing a triple-digit return. So no matter what happens from here, Burford is playing with house money on YPF.

And therein lies the beauty of its business model. Burford’s management has proven to be extremely shrewd capital allocators, by taking calculated risks with limited downside and asymmetric upside. That’s how the company has achieved an average return on invested capital (“ROIC”) of 105% on concluded cases, with only a single losing year. And it’s how the business has compounded its book value at 15% annually since going public in 2009, while the share price has increased at 17% per year over that same time.

Even excluding YPF, Burford’s business model has never looked better. Last year, it generated $700 million in cash and reported a record $327 million of realized gains across its portfolio. Trading at a $3.2 billion market capitalization, Burford trades at less than 10x this year’s expected earnings and at 1.3x book value. Similar business models in the private equity world, like KKR Group (KKR) and the Carlyle Group (CG), tend to trade at 4x to 5x book value and anywhere from 15x to 25x earnings.

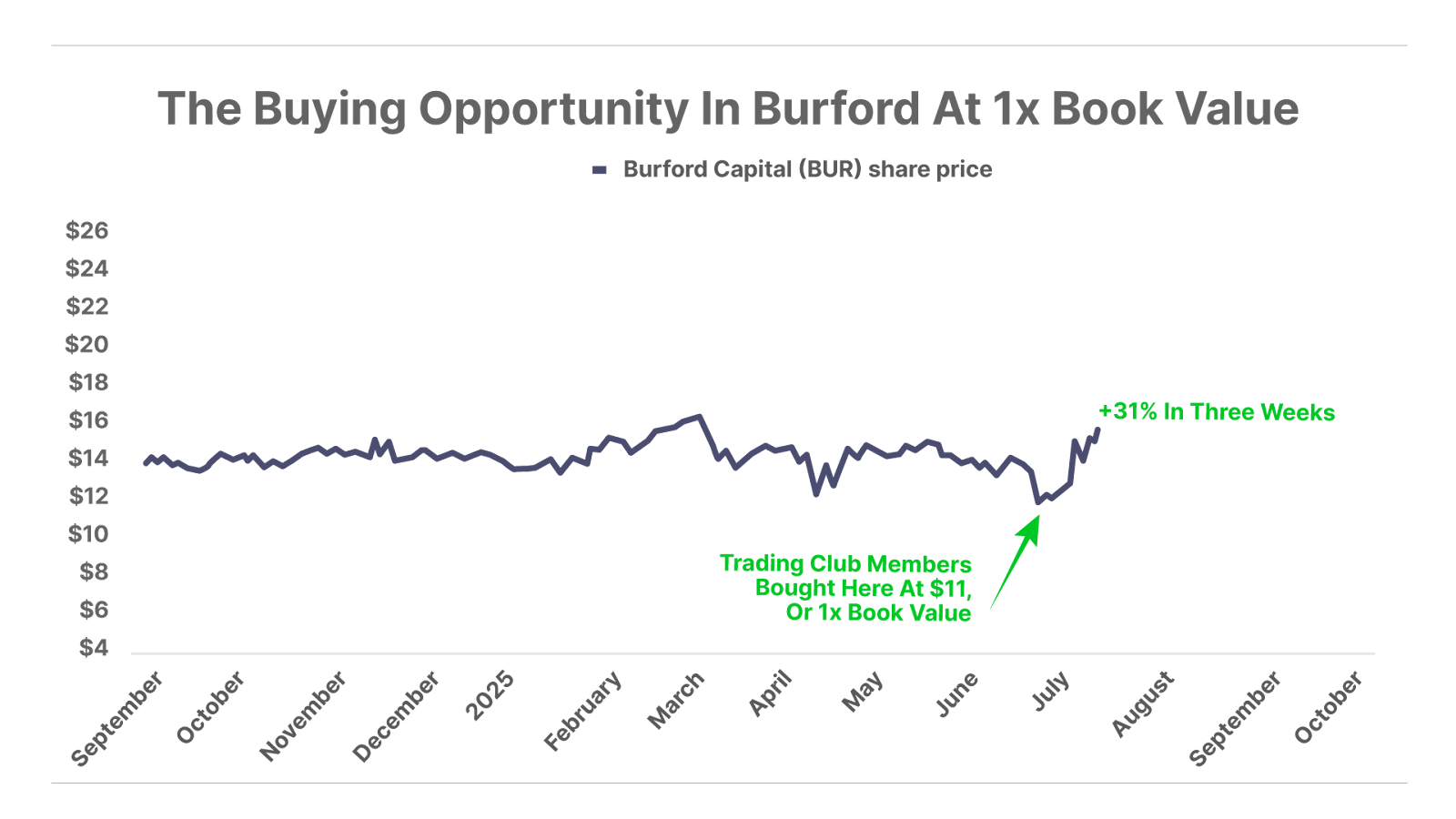

In a downside scenario, such as Argentina winning its appeal on YPF, we believe Burford will likely find a floor at around its current book value of $11 per share. Historically, Burford has rarely traded at or below book value – only 9% of the time since it went public in 2009. And investors who have bought at any of those points have enjoyed tremendous long-term gains, averaging 21% compounded annual growth rate (“CAGR”):

Members of The Trading Club capitalized on the most recent opportunity to buy Burford at book value on Wednesday, June 18. The day earlier, Burford’s shares dropped 14% on news that a tax clause was introduced in the Senate version of President Donald Trump’s “Big Beautiful Bill,” which proposed a higher tax rate on litigation-finance transactions. In our June 18 buy recommendation, we gave three reasons why the share price was an over-reaction, including our number-one reason:

There’s no guarantee that this clause gets ratified into the official budget bill. The original version of the bill that passed through the U.S. House of Representatives contained no reference to the new litigation finance tax rate, and thus the clause will need to survive the reconciliation process.”

As it turned out, the clause got struck down during the reconciliation process on Monday, June 30. Then, just hours later on that same day, Judge Preska ordered Argentina to transfer its 51% stake in YPF to Burford, sending shares soaring.

Was there a little luck involved with that timing? Sure. But as we explained in our June 18 recommendation, the calculus for buying was simple:

The bottom line: we see tremendous value in shares of Burford after yesterday’s decline.”

In the three weeks since that recommendation, we’re up 31% in Burford shares in our live tracking portfolio for The Trading Club.

This is just one of 10 winning open trades in The Trading Club portfolio since we launched the publication on May 30. Our live $100,000 tracking portfolio is up 3.8% as of yesterday’s close.

The Trading Club is an opportunistic service designed to capitalize on both bull and bear markets – acting on high-conviction trading ideas from our team of analysts, including options trades on forever stocks, distressed debt, and biotech. Each trade is tracked in a live, real-money account providing a fully transparent track record.

We’re releasing our next series of trades at the end of this month.

If you’re interested in joining us and receiving the next trading ideas, click here to join the waiting list.

LIMITED TIME ONLY: FREE Ticker Symbol Revealed to Get Pre-IPO Exposure to SpaceX

A rare window of wealth has opened.

Discover how you can get exposure to Elon’s SpaceX, pre-IPO.

Reuters calls SpaceX “a better $1 trillion bet than Tesla”

Everything is revealed, for free, in this special presentation. No strings. No BS. Click here to see.

Three Things To Know Before We Go…

1. Tariff turbulence continues. On Monday, we noted that President Donald Trump had pushed back his July 9 tariff deadline until August 1 to give U.S. Treasury Secretary Scott Bessent additional time to work on trade deals. Since that announcement, the president has ramped up pressure on trading partners, issuing formal letters to 21 countries (so far) indicating they would face new – and in most cases, steeper – tariff rates, ranging from 20% to 40%, if they don’t reach a deal prior to the new deadline. Many of these new rates are close to what Trump had initially imposed as part of his “Liberation Day” announcement on April 2. The markets, for now, are taking the latest news in stride, with the major indexes trading modestly higher today.

2. An early sign of consumer weakness. Amazon’s (AMZN) Prime Day sales fell almost 14% during the first four hours of this year’s annual July sales event compared to last year, according to e-commerce agency Momentum Commerce, perhaps pointing to a slowdown in consumer spending. However, it’s also worth noting that this year’s event is four days rather than the usual two, so consumers may be holding off on purchases in the hope of better deals later this week. Other retailers are also increasingly offering big discounts of their own during this event, which could be diluting Amazon’s share of Prime Day sales. We’ll be watching this month’s retail sales data for further confirmation.

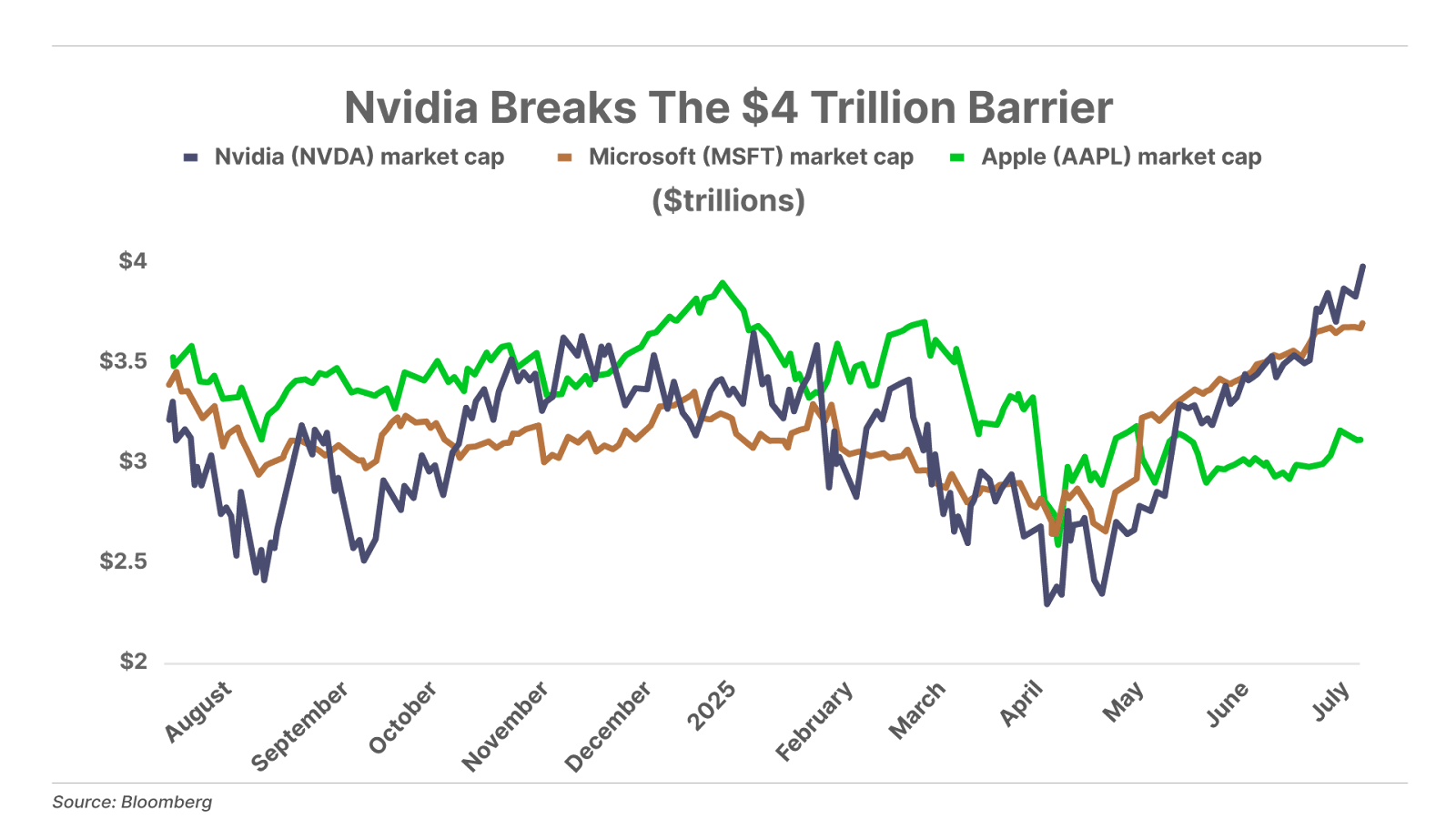

3. Nvidia hits $4 trillion milestone. Nvidia (NVDA) is the first company ever to reach a $4 trillion market capitalization. Shares of Nvidia are up 20% year to date and have soared over 1,000% since 2023, now making up 7.5% of the S&P 500 Index. The unprecedented milestone reflects the company’s dominant position in artificial intelligence (“AI”), where it is leading the parallel-processing revolution. Cloud infrastructure giants are projected to spend $350 billion on capital expenditures (much of that on Nvidia GPU chips) over the next year – up from $310 billion. Porter noted in the May 28 Daily Journal, “Nvidia is going to become vastly more valuable in the years ahead” – the meteoric rise underscores why it is currently the most valuable business in the world.

If you haven’t read our special report, The Parallel-Processing Revolution, you really should. It goes into far more detail and explains all of the different businesses that are partnering with Nvidia to create this entire new computer ecosystem.

Tell us what you think about this asymmetric opportunity: [email protected]

Good investing,

Ross Hendricks

Houston, Texas

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.