- HOW TO EARN 243% ON A BITCOIN BOND

- A GLOBAL “MINSKY MOMENT”

- THE BOND BULL DIES

- WHY WEALTH IS SHIFTING TO REAL ASSETS

No one had ever seen anything like it.

In the spring of 1928, a young stockbroker did something no one on Wall Street had ever done before. Or has since.

The broker told his clients to get out of debt – entirely.

At the time, that meant selling all their stocks. Back then, in the 1920s, virtually all investors in the stock market used margin loans. By looking out for his clients’ best interests – and telling them to get out of stocks – the stockbroker was essentially shutting his own business down.

And he didn’t stop there. He also warned his clients to completely avoid owning any corporation that was financed, in any way, with debt.

Here’s what he wrote:

We think you should know that, with few exceptions, all of the larger companies financed by us today have no funded debt. This situation is not the result of luck but of carefully considered plans on the part of the management and ourselves to place these companies in an impregnable position.

The advice we have given to important corporations can be followed to advantage by all classes of investors. We do not urge that you sell securities indiscriminately, but we do advise in no uncertain terms that you take advantage of present high prices and put your own financial house in order. We recommend that you sell enough securities to lighten your obligations or, better still, to pay them off entirely.

He repeated this advice month after month for more than a year, until the market crashed in the fall of 1929.

It saved the fortunes of his clients.

It also cemented his reputation as a wise and honest financier who cared deeply about the welfare of his clients – even more than his own firm’s profits.

The young broker’s name was Charles Merrill.

His reputation for excellent advice and selfless integrity created so much brand value that his firm, Merrill Lynch, went on to dominate the retail brokerage business for the next 70 years. The company’s network of brokers gave it unmatched stability on Wall Street, allowing it to grow into a leader in investment banking.

And eventually… even into mortgages.

In 2003, Stanley O’Neal, the firm’s first outside CEO and the only man to lead the firm who hadn’t started his career as a retail broker, led Merrill Lynch to invest heavily in subprime mortgages. A firm that was built upon a legendary reluctance to invest in indebted companies was destroyed by investing in the worst credits Wall Street ever created.

Ironically, it was Merrill Lynch’s reputation for caution, and its robust core business, that enabled it to borrow heavily and to invest billions in subprime mortgages.

It’s in this way that financial stability often leads to instability.

Bill Bonner, our long-time business partner and an underappreciated economic genius, explained the cycle to us this way:

Financial innovations always appear brilliant, at first. But they soon are taken to excess and become a farce. Eventually the farce leads to a tragedy.

We’ve seen many brilliant financial innovations become a farce.

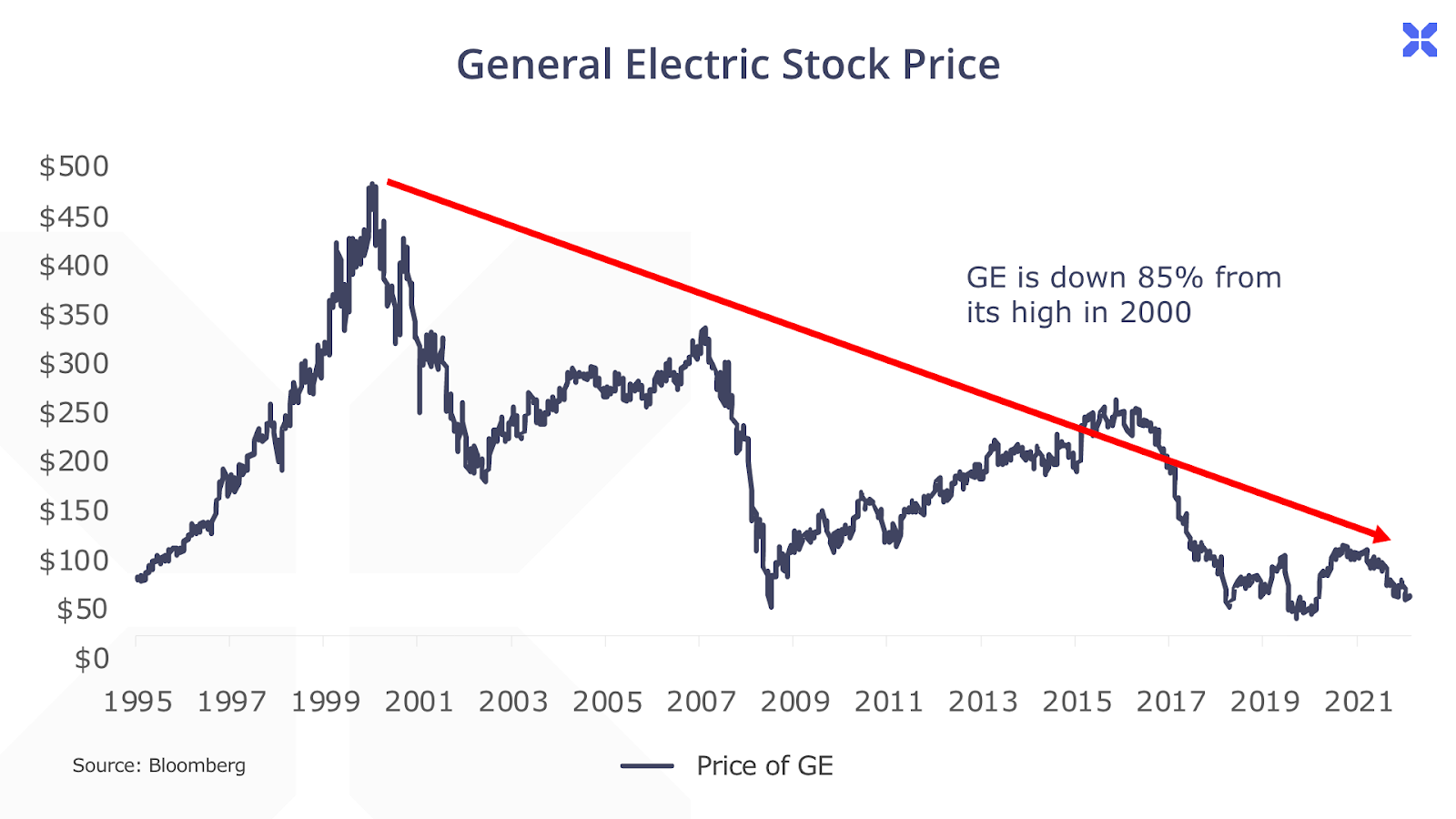

General Electric’s AAA credit rating – the highest possible and granted only to a small handful of governments and companies – allowed it to supply credit to millions of American consumers. It helped people buy their first electric appliances in the post-World War II baby (and building) boom. This was good for the consumer and great for GE’s bottom line, propelling it to become the largest publicly traded company in the world by 2000.

GE’s credit innovations were, at first, a brilliant asset for the company. These innovations were the foundation for the company’s incredibly stable earnings. For 80 quarters in a row the company met or beat its earnings forecast. The company’s CEO, Jack Welch, would become famous (and rich, with over $400 million of total compensation) thanks to GE’s remarkable growth.

But by the time Welch retired, the company’s accounting was a farce, as was revealed in subsequent SEC investigations. Likewise, most investors didn’t realize the company’s earnings were no longer powered by safe lending to homeowners. Instead, GE began to maximize the earnings power of its credit rating by borrowing huge sums of money (over $100 billion in overnight loans) to invest in high-yielding, risky credits – like private-label credit card debt and foreign mortgages. GE’s AAA rating was a farce.

By the early 2000s, as it piled into ever-riskier debts, like long-term care insurance, GE was well on its way to becoming a tragedy. The company would have certainly gone bankrupt in 2008 under the weight of its bad debts were it not for a $140 billion government-led bailout. With total debt of more than half a trillion dollars, GE, at its peak, was the 10th largest borrower in the world.

Even today, more than a dozen years after the crisis, the company limps along and continues to sell its best businesses to repay its enormous debts. (Editor’s note: Porter recommended shorting the company, saying it could never earn enough to finance its debts, over a decade ago, in July 2011.)

A Synchronized, Global “Minsky Moment”

Hyman Minsky was an academic economist who studied under Joseph Schumpeter at Harvard.

Schumpeter taught that capitalism’s dynamism was defined by “waves of creative destruction,” a description that profoundly influenced Minsky’s theory of credit.

Like Bill Bonner taught us, Minsky’s research showed how the financial system would trend from periods of stability, towards excess, and then instability. In short, there’s a process of creative destruction in banking too. New technology and other innovations enable more stability and therefore, more credit. But eventually the growth in credit surpasses its ability to be serviced reliably, and the so-called “Minsky Moment” occurs – a crisis strikes.

At these times, Minsky believed, the role of the central bank was paramount.

Ben Bernanke, the recent winner of the Nobel Prize in economics, and head of the U.S. central bank from 2006-2014, was a Minsky disciple. His studies of the Great Depression while the head of Princeton’s economics department convinced him that allowing banks to fail was the critical error after the crash of ‘29 that led to the decade-long Great Depression. The Nobel committee cited his work from the mid-1980s about the hidden costs of allowing banks to fail.

We are about to learn the hidden costs of not allowing banks to fail.

We believe that financial innovations and efforts to promote financial stability lead, inevitably, to more instability. Bailing out banks doesn’t eliminate Minsky Moments. It simply postpones them by allowing still-greater excesses to develop.

Therefore, we suspect that the central bank-led global economic stability that’s existed since around the introduction of the Euro, and which accelerated dramatically after the global financial crisis and the European sovereign debt crisis, is going to lead, eventually, to the biggest Minsky Moment in history.

And now, we are certainly well into the “farce” stage of the play.

Central banks have gone from supporting sovereign credit markets and mortgage markets, to buying junk bonds and equities. The size of their buying has gone to levels completely unimaginable before the global financial crisis, with the Federal Reserve’s balance sheet increasing 10-fold in just over a decade.

The scope of the central banks’ manipulations of the markets created something that should never exist in capitalism – negative interest rates.

The impact on the real economy has become a farce too. The past decade has seen income inequality soar as the money supply grew at much faster rates than productivity, sending asset values soaring relative to wages. Artificially low interest rates enabled both sovereign borrowers and corporate borrowers to afford vastly more credit.

Likewise, ultra-low interest rates led investors to take on far more risks, which in turn bolstered the number – and valuations – of speculative unprofitable firms to unprecedented and absurd levels. There were, at one time, more than 150 unprofitable “unicorns” worth more than $1 billion each.

Perhaps the most flagrant farce has been the creation of thousands of alternative “crypto-currencies” with little or zero utility that became worth billions overnight.

A Farce with Devastating Real-World Consequences…

The most dangerous impact on the real economy, though, has been the effect on resources and energy.

If unlimited amounts of capital are available, at virtually zero cost, then virtually any energy infrastructure project can be financed (at least on paper) – even projects that don’t work.

As a result, over the last decade $3.8 trillion has been spent on “renewable” energy infrastructure globally, in a quest to make our environment better. Meanwhile, the mix of fossil fuels in global energy consumption has declined by just 1%, from 82% to 81%.

What has increased, dramatically, is the carrying costs of our electrical grids. What has also increased, dramatically, is the instability of power grids, all around the world. This winter will reveal just how much time and money has been wasted on energy investments.

That’s going to cause a very significant rise in social and political unrest. People are going to die because of the instability of the power grids. And there’s going to be hell to pay.

And that’s not the only big problem.

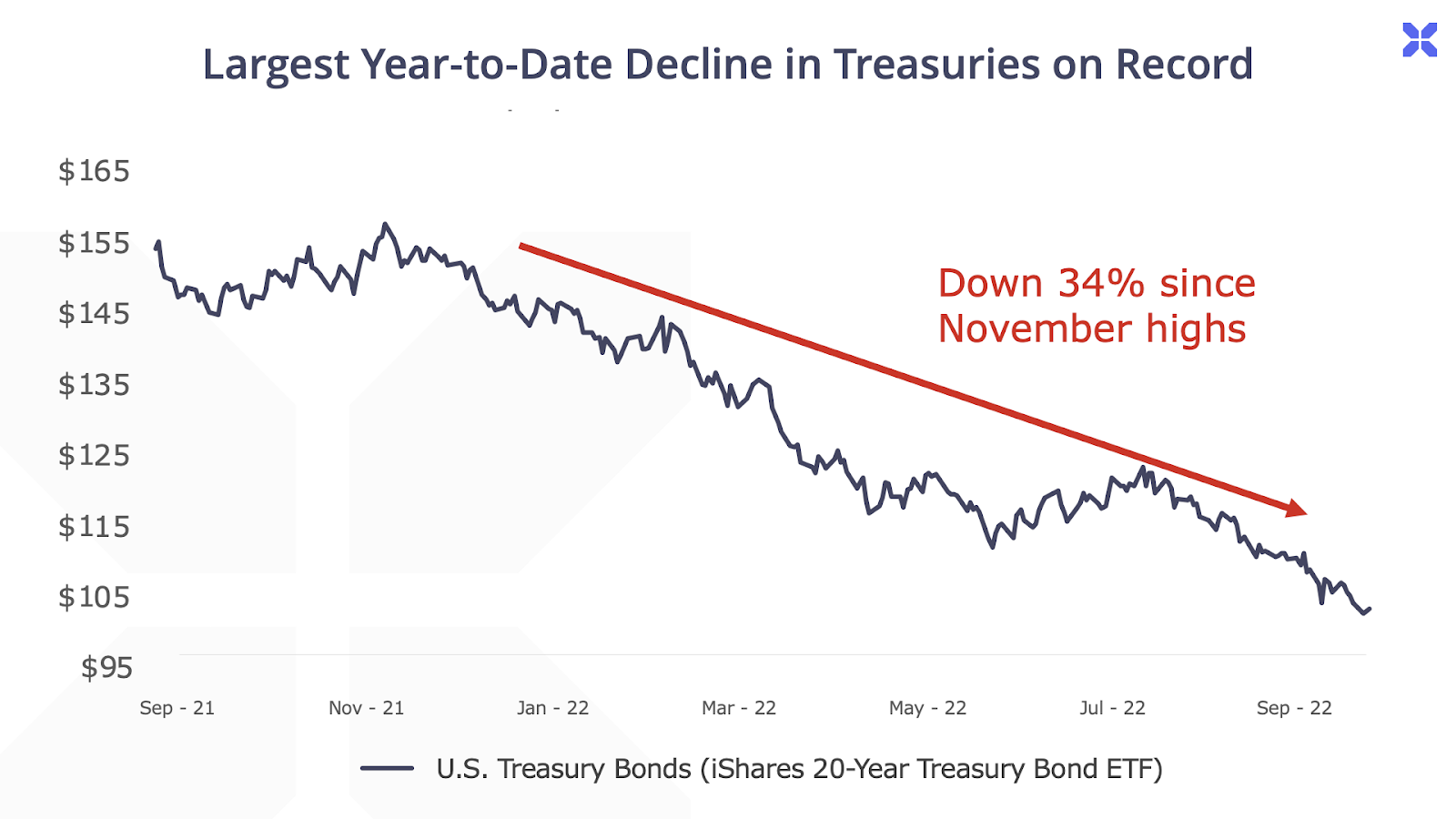

The ongoing collapse in long-dated British sovereign debt and the British pound is, we suspect, the first stage of the greatest financial tragedy in modern times. It will not be the only sovereign credit that’s destroyed this year. Constant maturity U.S. long bonds are down 35% from last November. That’s virtually unprecedented.

The losses in the world’s bond markets are going to wreck a lot of banks, a lot of pension funds, and a lot of insurance companies. The collapse in paper currencies is going to make it very difficult (read: impossible) to rein in inflation without wiping out trillions in equity valuations.

We face a global synchronized “Minsky Moment,” in which, because of soaring inflation (mostly related to soaring energy costs), the stabilizing impact of the world’s central banks is no longer available. The global economy now faces a complete reset of interest rates, sovereign debt loads, and corporate debt loads without the “cushion” of central bank largesse to soften the collapse.

What will happen? Michael Burry, of Big Short fame, says he thinks “the mother of all crashes” is en route.

Where to Put Your Money Ahead of the Debt Crisis

Our bet remains that, given a big enough panic, the world’s central banks will blink. We believe that, sooner or later, the only sustainable path for the developed world’s economies is a mixture of higher inflation rates, and massive social benefit restructuring.

In the U.S., for example, there is no legitimate way for our federal government to finance its $31 trillion (!) in debt.

The yield on 10-year government bonds in the U.S. has hit 4%. The last time it sustained that level of interest was in October 2008, before the global financial crisis. The total debt load then? Less than $10 trillion. Assuming inflation remains above 6% and the Fed Funds rate advances to that level, it will cost something like $2 trillion per year just to pay the interest on government debt.

In 2019, total federal tax receipts were $3.46 trillion. They’re currently estimated to be $3.7 trillion in 2020. Paying more than 50% of tax receipts in interest alone is completely untenable… never mind the trillions in unfunded liabilities of Social Security and Medicare.

These facts, more or less, are mirrored across the major economies of the developed world. Thus, like Michael Burry, we believe the scope of the coming crisis is far, far bigger than virtually anyone yet realizes.

That’s why we have written you this letter. Like Charlie Merrill in his time, we believe the world’s economy is on the precipice of a debt crisis unlike any that’s ever happened before. For at least the next 5-7 years, investors who flee debt and leverage, and who own high quality, unencumbered equity, and especially energy, will do best.

We also believe that investors will do well to divest themselves of the U.S. dollar and instead, make a long-term move towards alternative currency.

Global Currencies in a Race to the Bottom

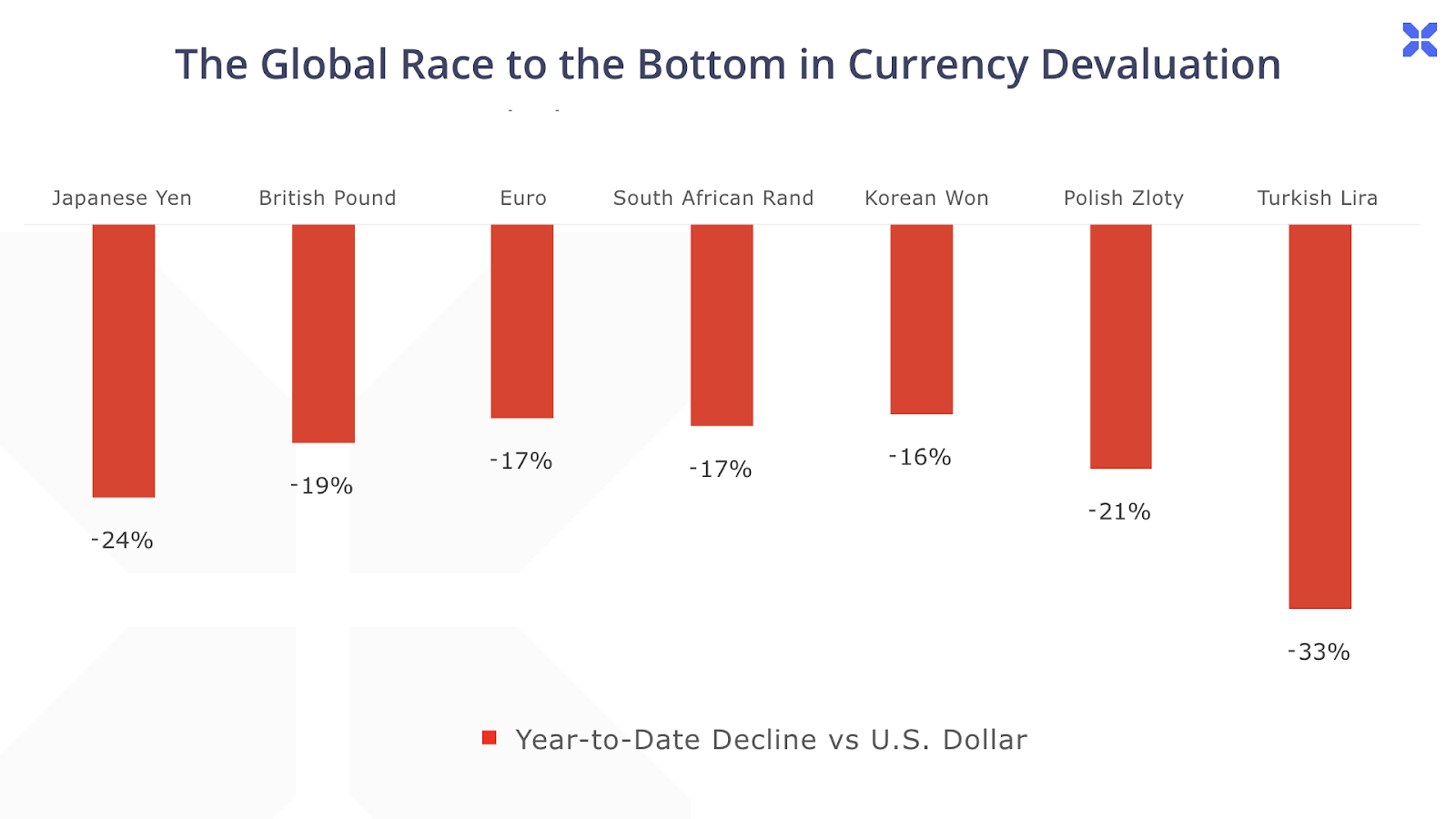

Given the unrelenting pressure on sovereign governments to finance unsustainable debts with inflation, all signs point towards widespread currency devaluation going forward.

Already this year, the Japanese yen has collapsed by 24%, the British pound has shed 19% of its value, and the Euro is down 17% against the U.S. dollar along with similar declines in currencies of other major economies, like South Korea, Poland and South Africa:

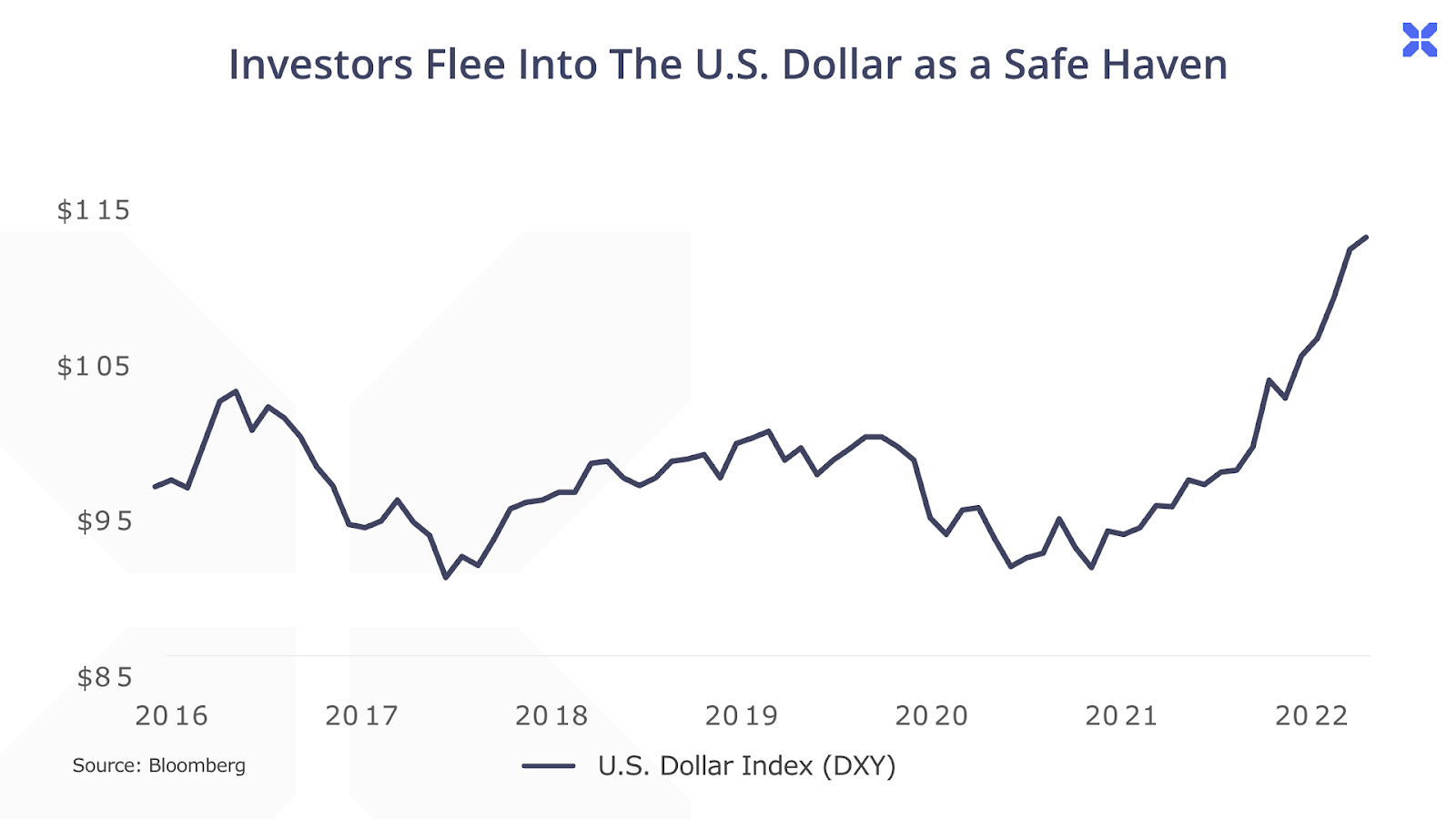

For now, the U.S. dollar reigns supreme. A big part of this divergence is due to the aggressive monetary tightening campaign by the U.S. Federal Reserve. Other factors include the global energy crisis that is spiking energy costs for economies with less energy security, like Europe and Japan.

Finally, there’s the U.S. Dollar’s role as global reserve currency – providing a safe haven that investors traditionally flee into amidst economic and financial distress.

These factors have all combined to temporarily prop up the U.S. dollar’s value on a relative basis. But zooming out beyond these short-term factors, the bigger picture is clear: the United States is the largest debtor nation in world history.

And thus, our future seems certain: paper money systems are unblemished by historical success. There are zero historical examples of any debtor nation with over 100% of GDP in debt that didn’t inflate away its obligations.

America’s history of printing away its obligations began in 1690, with our first colony, the Massachusetts Bay Colony. The most recent example was in 1971, when President Richard Nixon cheated our foreign trading partners and creditors. He repudiated the Bretton Woods agreement, which required the U.S. to settle its foreign debts in gold. Nixon, much like Sir William Phips, assured the public the measure was only “temporary.” Nixon also claimed, laughably, that the accompanying wage freeze and 10% import tariff would “increase jobs.”

The next decade saw the first substantial decline in real wages in American history. It was the beginning of the hollowing out of the middle class, as inflation sent asset prices higher, while the average standard of living fell.

And it is about to happen again.

There is no question in our minds that U.S. politicians will tap the printing press to paper over America’s unsustainable debt burdens. That’s why we believe investors should take advantage of the temporary strength in the U.S. dollar to diversify into alternative stores of value.

This includes sound money, like gold and silver, which will soar in value against rapidly depreciating fiat currency in the coming years. Other tangible assets, like commodities, will also appreciate for the simple fact that governments can’t print things like copper, as we explained in our previous issue.

One Asset Has the Most Upside from a Global Currency Devaluation

It’s more than just a store of value. This decentralized, digital monetary network allows seamless monetary transfers to anyone around the globe with the click of a button. It’s a peer-to-peer transfer mechanism, which means it exists outside the scope of governments and central banks, making it the most legitimate international, reserve currency.

If you think this sounds like Bitcoin, you’re right. We’re not in the business of hiding behind misleading descriptions here at Porter & Company.

Given the absurdity of many crypto “currencies” (we’re as fed up with “Dogecoin” as you are…) you may be surprised to see us recommending Bitcoin in this letter. We believe that Bitcoin is, at present, the best alternative to the U.S. dollar as a world reserve currency. And we think, more and more as this crisis builds, enormous amounts of value from around the world will seek to own it and mine it.

In our eyes, Bitcoin is the ultimate form of money. It’s a currency of pure energy.

But the investment we’re about to show you isn’t merely Bitcoin – it’s something better.

The New Global Money

Unlike fiat currencies, Bitcoin runs on software – not decrees from central bankers and governments.

Bitcoin was born in the wake of the last financial crisis, first defined in an anonymous whitepaper, published on October 31, 2008. The paper laid out the dire need for a globally available, decentralized and non-inflationary currency.

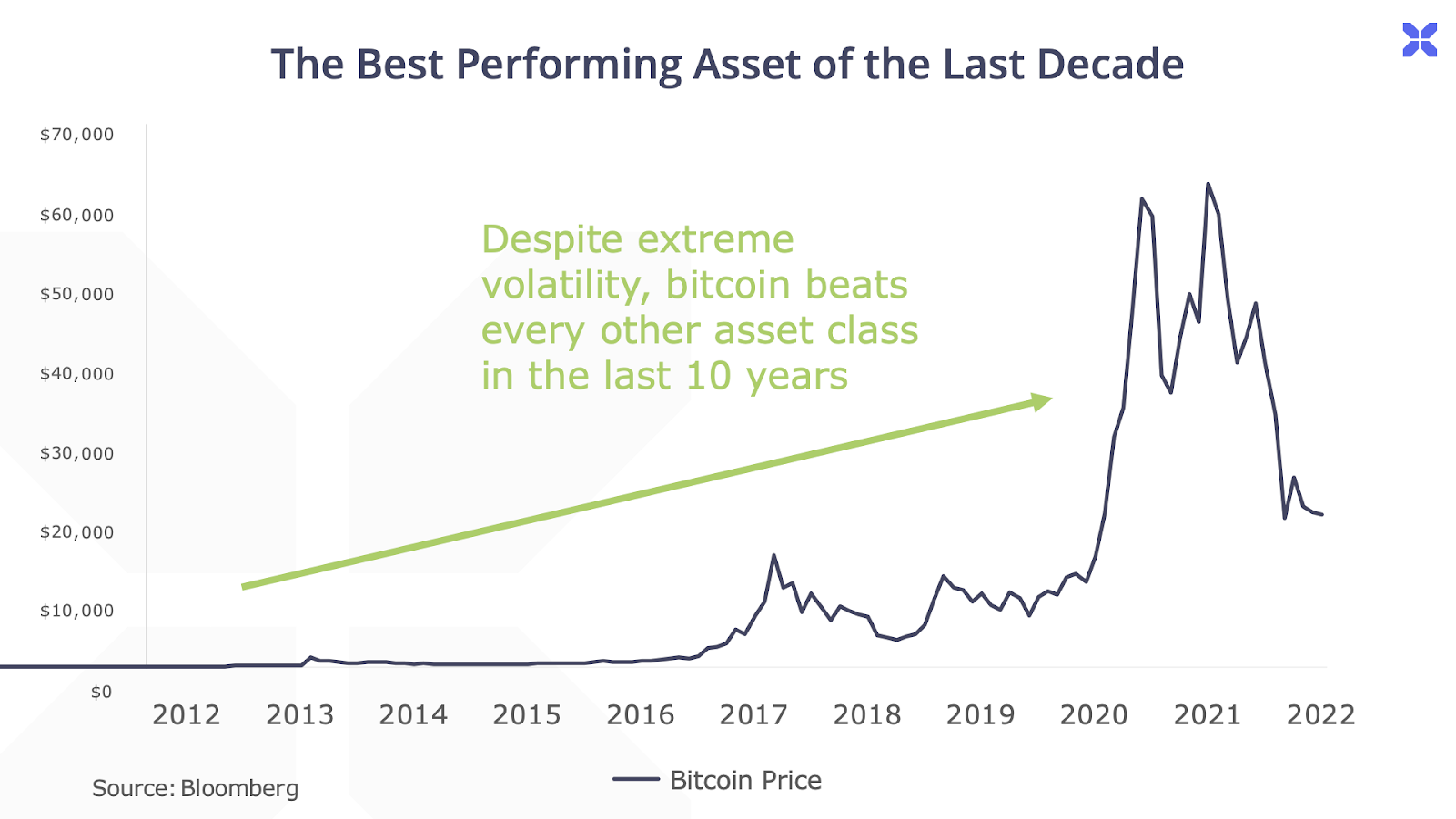

The solution came in the form of the Bitcoin network, which was launched as an open-source software protocol in 2009. Bitcoin registered its first series of transitions at pennies on the dollar, and went on to become the best performing asset class of all time – undoubtedly fueled by the record volumes of global monetary expansion during the last decade:

The Bitcoin protocol ensures that only 21 million coins will ever be created. That makes it immune from currency devaluation, and eliminates the silent theft of purchasing power through inflation that plagues sovereign currencies.

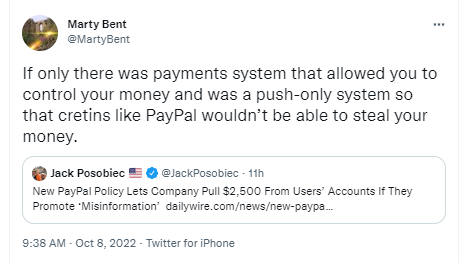

Beyond providing a source of stable money, Bitcoin also allows seamless, secure peer-to-peer transactions with anyone around the world at the click of a button. Often referred to as the “internet of money,” Bitcoin’s decentralized nature eliminates interference from governments, thereby eliminating the threat of censoring transactions and currency devaluation.

This censorship-free feature has never been more important in today’s world of “cancel culture” when financial institutions like Paypal threaten to financially punish those who engage in “thought crime”:

Bitcoin achieves all of these critical monetary features through its elegant software protocol that makes the network stable, self-regulating, and ultra-secure.

Here’s how it works…

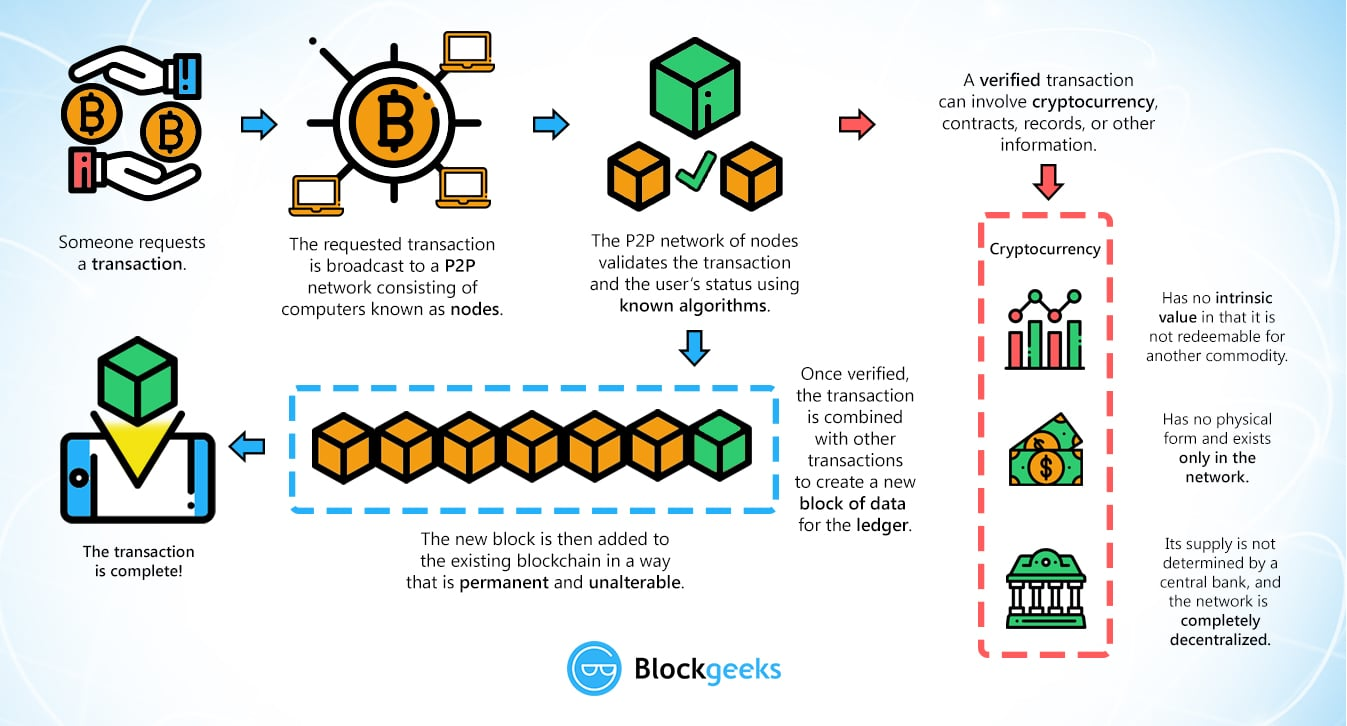

Every Bitcoin transaction is digitally encrypted onto a decentralized network, known as the blockchain. The blockchain is essentially a public ledger, maintained through a network of thousands of “nodes”. At each node, high-powered computers — known as miners — keep track of every Bitcoin transaction. These miners compile real-time Bitcoin transactions into data blocks.

When a given data block fills up, the miner adds it to the pre-existing block series. This process forms a chain of continuous transaction blocks, hence the name “blockchain”. Here’s a diagram showing how individual transactions get added to the Bitcoin blockchain:

The blockchain was designed as a self-regulating network, with built-in incentives for computers around the world to compile and keep track of every transaction. In exchange for lending their computing power to the Bitcoin network, miners are rewarded with entries into a lottery for each data block they create. The number of actual Bitcoins awarded in these lotteries declines over time, ensuring that the total number of Bitcoins approaches a hard limit at 21 million coins.

In this way, Bitcoin mimics the gold standard. Gold mining became progressively more difficult and expensive over time, as the industrial revolution and new discoveries eliminated many sources of gold. Today, as computing power radically increases through time according to Moore’s Law, Bitcoin is designed to become progressively more difficult to mine. Thus, Bitcoin is designed to match increases in computer power, in the same way that the earth’s natural geology caused gold’s relative scarcity.

It’s said that an ounce of gold has always been worth a fine men’s suit. That was true 2,000 years ago and it’s true today, despite massive increases in productivity. That’s because gold became relatively more scarce as humans figured out how to mine it ever more efficiently throughout the scientific and the industrial revolution.

The same is true with Bitcoin – but with one very important difference. Bitcoin’s “productivity curve” isn’t predicated by industrial (mining) technologies, but instead by the incredible, almost miraculous, advances seen in digital technologies. Bitcoin is a currency that’s designed to be stable relative to advances in computing. And that means its value has soared relative to other currencies.

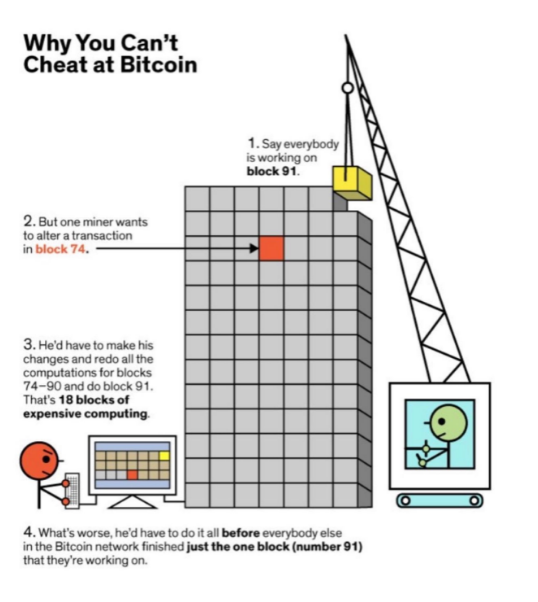

The Bitcoin protocol uses several mechanisms to ensure security and integrity of the blockchain. This includes the fact that 50% of the network nodes must approve each data block before adding it onto the blockchain. This prevents a bad actor from creating false transactions in real-time.

That’s because in order to create a “false” version of the Bitcoin ledger, a bad actor would need to rewrite the entire blockchain history with the new false version, as explained in the following graphic:

The end result is a secure self-regulating decentralized network, governed by a series of rules that eliminates the need of any central authority. That’s what makes Bitcoin the ultimate candidate for global reserve currency – a neutral asset that exists outside the realm of sovereign governments and banking cartels.

Bitcoin is the people’s money. And more people are using it each day.

So far this year, more than 17 million transactions have been settled in Bitcoin. But we’re still very early in its adoption, and therein lies the big upside case to much higher prices…

Bitcoin’s Unlimited Upside Potential from Growing Global Adoption

Over the last decade, Bitcoin has transformed from a fringe speculative vehicle into a mainstream financial asset. Today, big banks like Goldman Sachs, Citi and JP Morgan are now dealing in Bitcoin. And Fidelity — one of the world’s largest asset managers with $12 trillion in assets — now offers Bitcoin investments in its 401k retirement plans.

This growing adoption is how Bitcoin went from a standing start in 2009 to a more than $1 trillion asset at its peak last year. And yet, we’re still in the early innings of this story. Remember that the ultimate bull case for Bitcoin is its ascendance to become a global reserve currency.

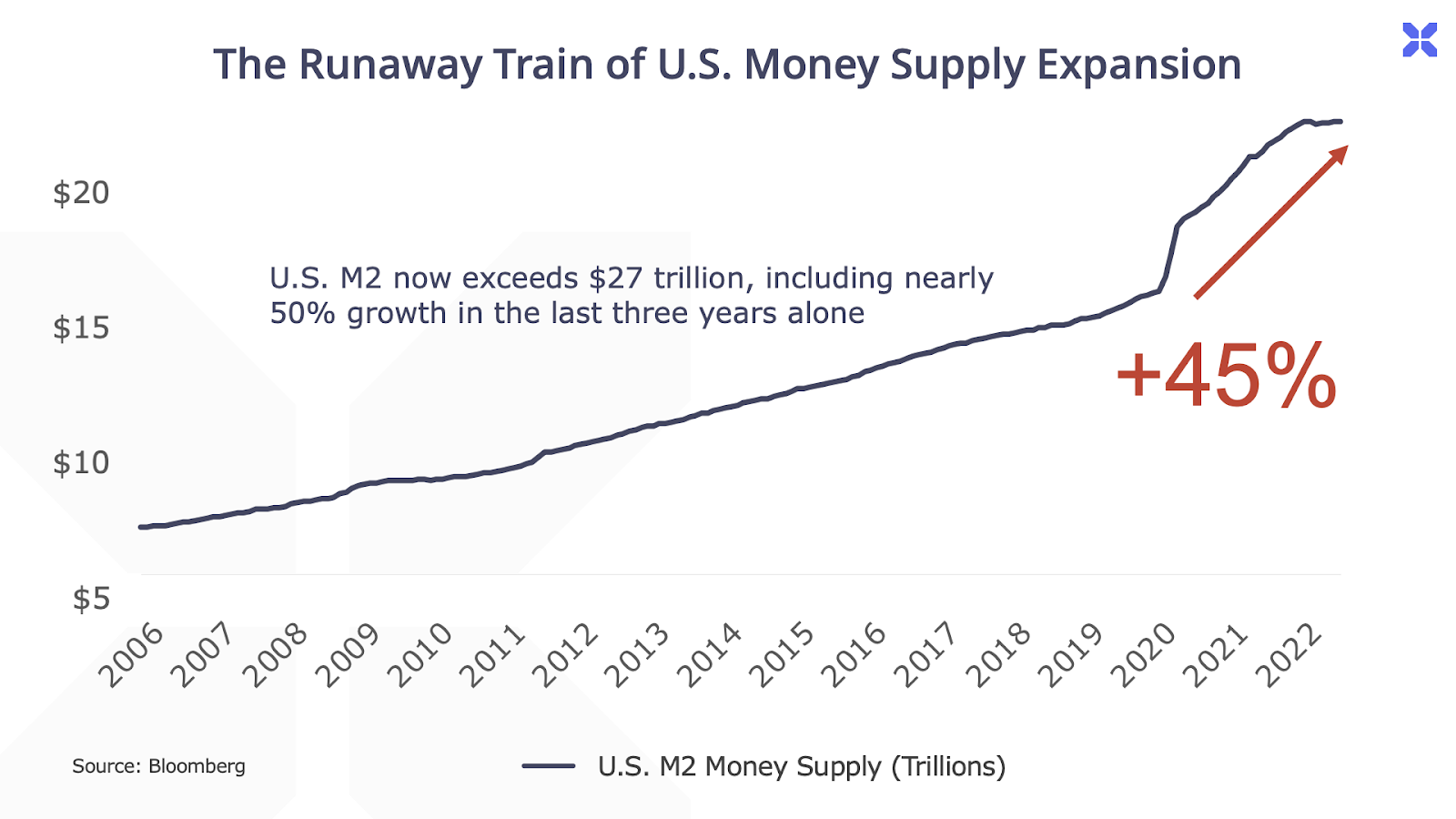

In that context, the potential addressable market for Bitcoin is the global M2 money supply, defined as currency in circulation plus overnight deposits, savings deposits, and money market funds. These are all sources of currency that could flow into Bitcoin if investors lose confidence in fiat currency and begin looking to Bitcoin as an alternative store of value.

In the U.S. alone, the M2 money supply is over $20 trillion and growing – including nearly 50% growth since 2020 alone:

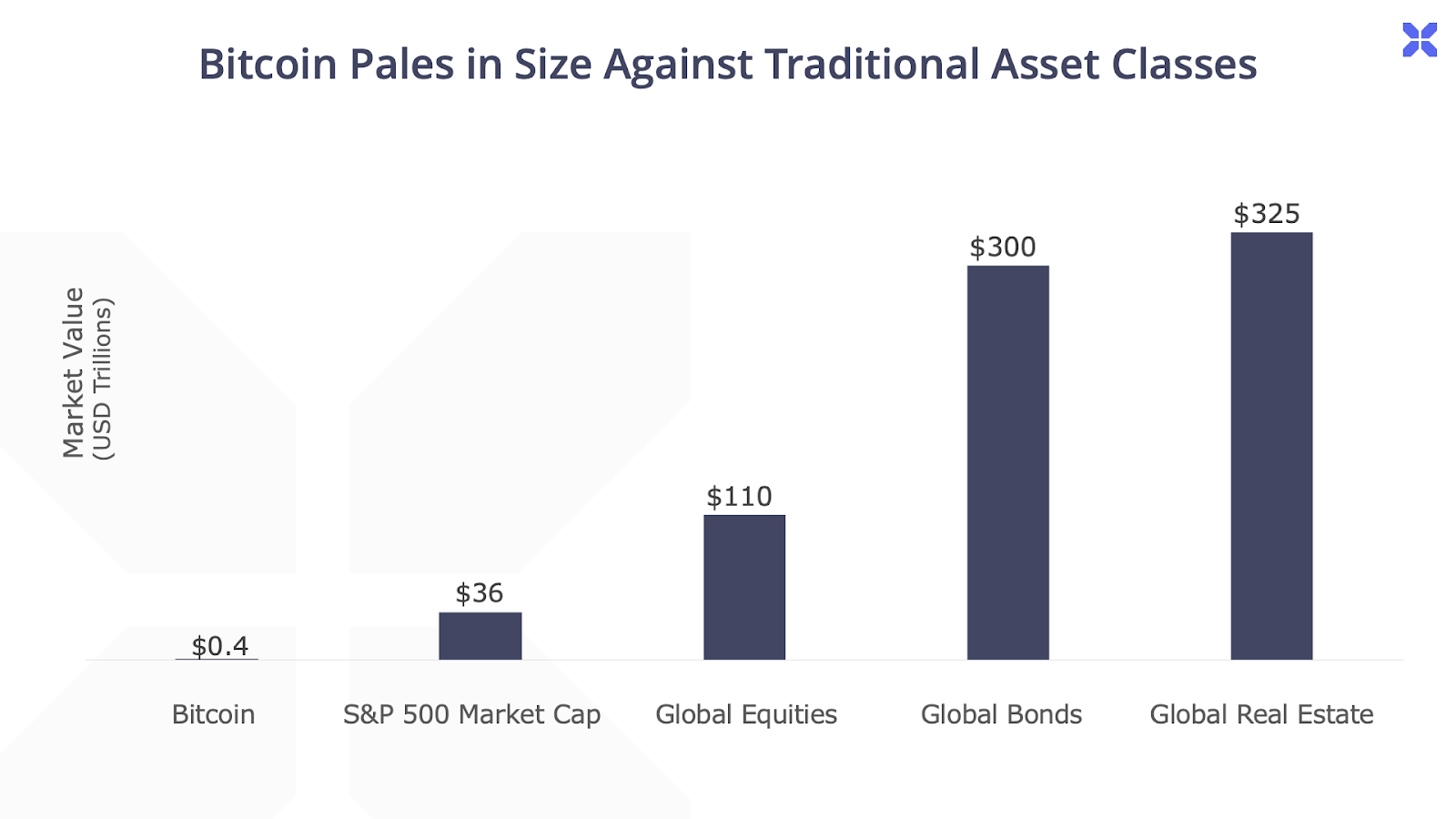

Globally, the M2 money supply is nearly $100 trillion. Meanwhile, the total size of traditional asset classes is in the hundreds of trillions of dollars.

Today, this wealth is mostly concentrated in stocks, bonds, and real estate. Bitcoin’s current $400 billion market capitalization is a rounding error compared with these traditional stores of wealth:

When you consider the ramifications of just 1-2% of global money supply or total wealth finding its way into Bitcoin, it’s conceivable that the market could soar from its current $400 billion into the tens of trillions, pushing the price of Bitcoin from $20,000 to millions of dollars per coin.

The bottom line: in a world where overly-indebted governments around the globe issue endless new supply of fiat currency to inflate away their obligations, more and more of those currency units will flow into alternative stores of value, like Bitcoin. And if the global investment community begins diversifying even a small portion of their wealth away from traditional investments into Bitcoin, there’s simply not enough supply to meet demand at today’s prices.

Given Bitcoin’s hard supply cap at 21 million coins, a scenario where trillions of dollars flow into the asset class, the conclusion is clear — much, much higher prices. As global central banks, including the Fed, return to their familiar playbook of cutting interest rates and expanding the money supply to deal with unsustainable global debt burdens, we see Bitcoin reaching new all-time highs and hitting $100,000… and that could be just the beginning of the next leg higher.

With Bitcoin prices recently falling from a high of $65,000 to around $20,000 today, we believe now is the time to get ahead of this trend. But instead of simply buying Bitcoin, we’ve identified a unique investment vehicle that will offer exposure to higher prices, while also providing protection against a downside scenario where Bitcoin prices fall in half from here.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.