Issue #108, Volume #2

Berkshire Hathaway Is Too Big To Generate Outsized Returns

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

Editor’s note: Today, Porter turns the Journal over to Pieter Slegers… Pieter is founder of Compounding Quality, a Substack platform with more than 1.5 million readers. Among those readers are Amazon (AMZN) founder Jeff Bezos, NBA star LeBron James, real estate investor Jared Kushner, and Pershing Square Capital CEO Bill Ackman. On average, Pieter’s portfolio has returned 20% annually. But, he says, apply his investing strategy to small and micro-cap stocks, and the results skyrocket. He calls these investments Tiny Titans – and yesterday he sat down with Porter to discuss. To watch their conversation, click here.

| Warren Buffett is a humble man… Look at his house… Berkshire Hathaway is too big to make money… Buffett’s bold prediction… Why Wall Street avoids small caps… Treasury yields aren’t cooperating… |

Warren Buffett made a surprising, boastful remark.

Despite all his success, generally speaking, Warren Buffett remains remarkably humble. Just look at his house.

It’s a wonderful place, but for a man worth over $150 billion, it’s probably the most modest house ever… Warren bought his house in 1958 for $31,500 and called it one of his best investments ever.

Or look at his car: an 11-year-old, 2014 Cadillac. Not exactly what you’d expect from one of the richest people on Earth.

{kind=link}

But one time, Buffett said something that wasn’t humble at all. He said something you’d rather expect to hear from a naïve teenage investor who thinks he cracked the code.

He said this:

I think I could make you 50% a year on $1 million. No, I know I could do that.”

And honestly? I believe he is right. Let me explain why.

It’s very easy: size hurts performance. In his 2023 shareholder letter, Buffett wrote:

There remain only a handful of companies in this country capable of truly moving the needle at Berkshire, and they have been endlessly picked over by us and by others. Some we can value, some we can’t. And, if we can, they have to be attractively priced. Outside the U.S., there are essentially no candidates that are meaningful options for capital deployment at Berkshire. All in all, we have no possibility of eye-popping performance.”

It seems like Buffett is going against his own words. On the one hand, he claims he could earn 50% annual returns. On the other hand, Warren admits there’s no chance for “eye-popping performance” at Berkshire.

But it makes perfect sense. And it all comes down to one thing: size. He could earn 50% returns if he was running a small portfolio.

Berkshire has grown so large that Buffett simply can’t invest in the businesses that once delivered his highest returns. Berkshire Hathaway is so big that Warren Buffett can’t make any money with it.

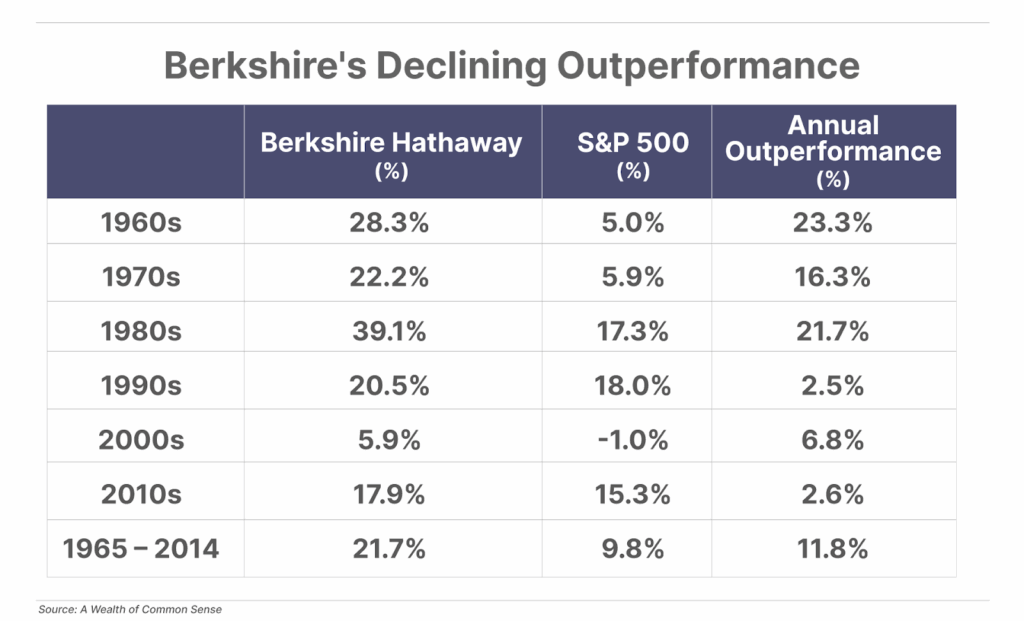

It’s the main reason for Buffett’s declining outperformance.

This has created a clear pattern over time: The bigger Berkshire got, the smaller the outperformance became.

Small Caps

You as a small, non-institutional investor have the main advantage over Warren Buffett… you can still invest in small companies.

And that’s a good thing, because small businesses can be excellent investments:

If you invested $1,000 in 1926 it would’ve turned into:

- Large caps: $8.7 million

- Small caps: $430 million

- Micro caps: $860 million

- High-quality micro and small caps: $1.26 billion

There are several reasons for this.

Low valuation levels

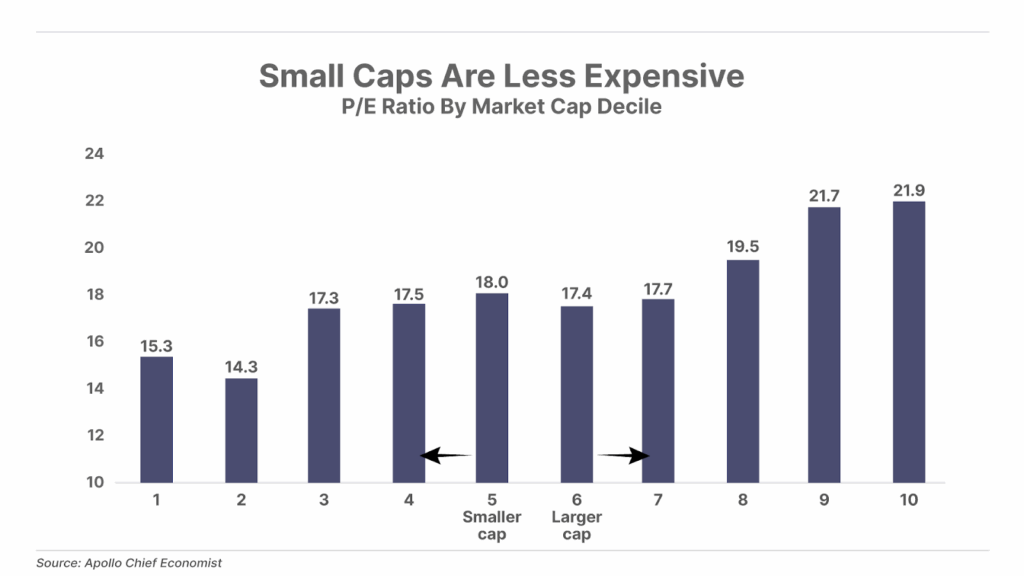

First, small-cap stocks typically trade at lower valuation levels than large-cap stocks.

That’s because professional investors can’t invest in small-cap stocks.

A few years ago, I was responsible for the daily operations of a fund with $200 million in assets under management (“AUM”).

While that might sound like a lot, it’s peanuts in the broader financial world.

But even our “small” fund couldn’t invest in stocks with a market cap under $10 billion.

This is a common limitation for funds, which means small caps are underfollowed by institutional investors.

As a rule of thumb, the smaller the stock, the less efficient the market. That’s why investing in small caps can be very interesting for investors like you. As Warren Buffett likes to say…

The secret of life is weak competition. If you want to outperform the market, go where competition is weak.”

The law of large numbers

The law of large numbers states that the larger you get, the harder it is to grow at very high rates. It’s way easier for a company that earns $1 million to double in size compared to a company that earns $50 billion.

Let’s take Apple (AAPL) as an example. If Apple were to grow at a compound annual growth rate (“CAGR”) of 10% for the next 20 years, it would be worth roughly $20 trillion (current market cap: $3 trillion). To justify this market cap, every person on earth would have to own multiple iPhones!

That’s the challenge of scale: the bigger you are, the harder it becomes to grow.

Small caps don’t have this constraint.

Historical proof

Still not convinced? Look at the historical performance. Between 1926 and 2006, the smallest decile stocks compounded at a CAGR of 14.0% compared to 10.3% for the S&P 500.

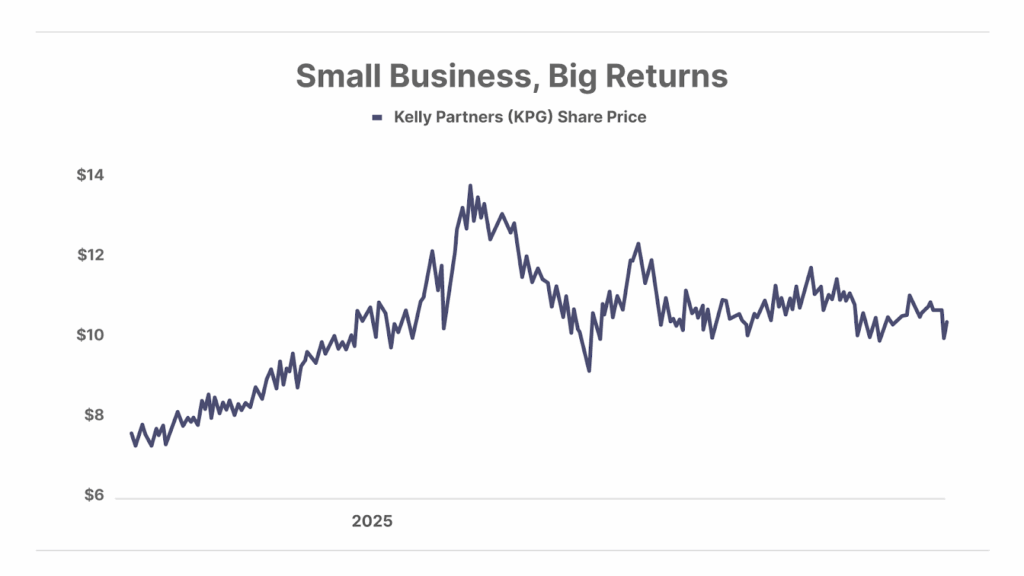

We see the same trend in our Compounding Quality portfolio: Our smallest business, Kelly Partners Group (KPG), has produced the strongest returns. It’s a company I pitched at Porter & Co.’s Annual Conference last year. The stock is up almost 40% since then:

Mini Buffett Stocks

So now the million-dollar question… Which stocks would Warren Buffett buy if he had only $1 million to invest?

He would look for these seven characteristics:

- Net debt / EBITDA less than 3… healthy balance sheet

- High insider ownership… skin in the game

- Net profit margin greater than 10%… high profitability

- Five-year average revenue growth greater than 9% per year… attractive growth

- Return on invested capital (“ROIC”) greater than 15%… great capital allocation skills

- No extra shares issued in the past three years… we don’t like dilution

- Plenty of reinvestment opportunities

- P/E ratio less than 18… Attractive valuation

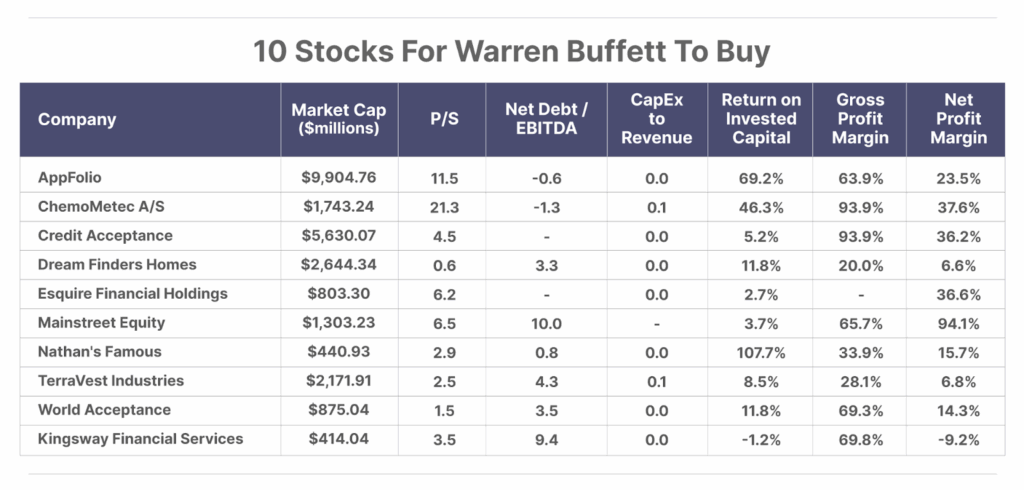

I created a watchlist of 94 companies I believe Buffett would be interested in (available at Tiny Titans).

Let’s pick out 10 for you… and for Warren:

I think they all have 10x potential from this valuation level. My favorite ones in this list? Esquire Financial Holdings (ESQ), Mainstreet Equity (MEQYF), and Kingsway Financial Services (KFS).

Pieter and Porter sat down yesterday to discuss Pieter’s Tiny Titans strategy and small-cap investing. In the conversation, Pieter points out seven “DNA markers” shared by companies that go from obscure small caps to global market leaders… and how to use them yourself to separate tomorrow’s winners from today’s hype.

To watch their conversation, click here now.

Is the World’s Greatest Investor

About to Shock Wall Street?

In just a few weeks, a move decades in the making could be revealed — and when it is, it could ignite the next great gold rush. Savvy insiders are quietly positioning now… before Buffett makes it official. Garrett Goggin has already pinpointed four tiny-gold-miners that could 100X once the announcement hits. It’s the perfect moment to be greedy — before the herd wakes up.

Click here to get Garrett’s Top Four gold picks now — before the world’s greatest investor pulls the trigger.

Three Things To Know Before We Go…

1. Intel and Nvidia make a deal. Yesterday, Nvidia (NVDA) announced the purchase of a $5 billion stake in Intel (INTC) as part of a new partnership between the two chip-making giants. The companies plan to co-develop “multiple generations” of chips for data centers and computers, including a customized x86 CPU designed for integration into Nvidia’s AI and data center platforms. After two decades of lagging behind its peers, Intel could be reaching a critical turning point.

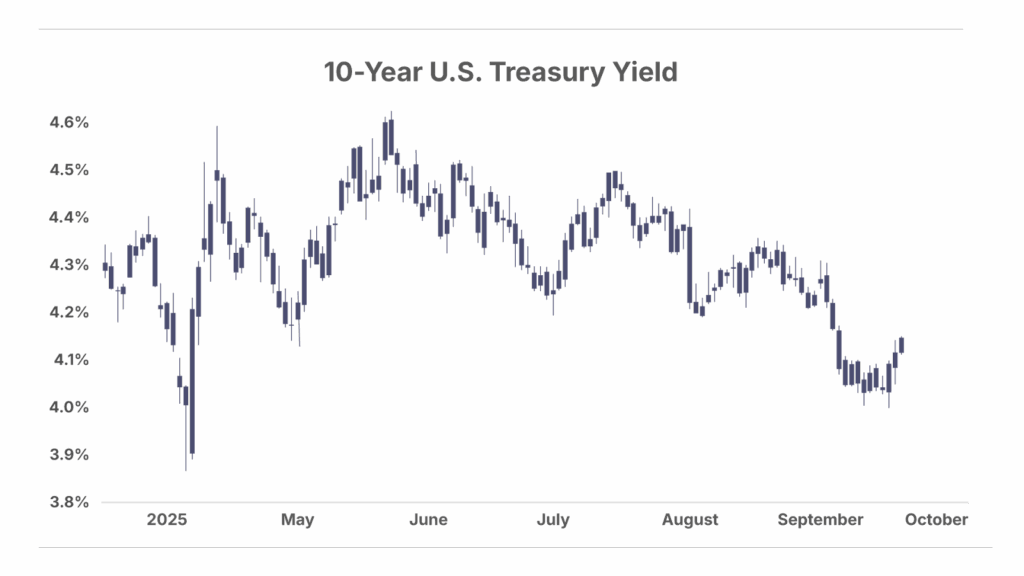

2. Treasury yields aren’t cooperating. A big part of the rationale behind President Donald Trump’s calls for the Federal Reserve to cut interest rates is to ease the cost of consumer credit, particularly mortgages. However, while some consumer credit rates are tied to the Fed’s short-term rate, the most common mortgage – the 30-year fixed-rate – is tied to the yield on the 10-year U.S. Treasury note. And, unfortunately, this yield has been rising since the Fed cut rates on Wednesday, from 4.00% to 4.14% today. Of course, three days does not make a trend, but this is certainly not the reaction the Trump administration was hoping for so far.

3. U.S. stock buybacks hit $1.6 trillion and are only expected to grow. JPMorgan projects repurchases could climb at this record pace to reach another $600 billion in the year ahead. The trend isn’t only in the U.S. – pointing to a 38% global increase in buybacks through August. Buybacks continue to help fuel the equity rally, injecting liquidity and supporting higher prices.

Tell me what you think: [email protected]

Mailbag

Porter received a number of emails about Wednesday’s Journal – which discussed the real reason behind the U.S. Civil War and how economic and social conditions today are ripe for another civil war. One thing he mentioned in that essay is this:

“The important thing to understand: Congress created an automatic annual increase in benefits, to match the government’s CPI-U index, but it never changed the funding mechanism. And that means Social Security is going to run out of money.”

Bravo, Porter! “The Real Lesson of Antietam” was a great read and super insightful. I fear Trump tariffs are setting America up for absolute disaster. Social Insecurity insolvency doesn’t help.

Ugly days are ahead.

All the best!

Matt G.”

Excellent summary on the true cause of the Civil War (all wars?). And although what you say is coming for the U.S. is hard to read (and believe), the facts are clear and let’s not forget it is not just happening in the U.S., it is happening everywhere, especially Europe. I flew international for my last 10 years at American Airlines. Since I flew mostly in the European Theater, I saw the decay of sovereignty of the individual countries and more importantly, their cultures due to Muslim immigration. Europe is toast and it will likely happen there first, the next civil war you portend.

Jorge”

Lifetime long-armer and Twitter follower. Been reading your recent epic posts. Bravo!

I’ve been pondering if the wealth division and the growing separation between the haves and have-nots is intentional. By design.

What better way to foment civil war than to create a super wealthy class on the back of everyone else? Do it, dramatize it, assassinate our heroes, and keep playing with matches near the powder keg until it explodes.

Once we tear each other apart, Soros & Co. get to swoop in and remake America in their image.

Thanks for helping us long-armers survive this thing.

Matt V.”

I love the history lesson. I was a history minor and always loved learning about “the War of Northern Aggression,” but have never heard of this perspective.

Brian F.”

I always enjoy reading your thoughts, but your column today is fear mongering, provocative nonsense. Social Security is the easiest of our major problems to fix and it will be done, because there is no alternative. Some combination of increased revenue, higher retirement age, and use of a lower inflation index is all that it will take. You do great harm by fear mongering Social Security into a bigger issue than it is.

Tim M.”

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care Team at 888-610-8895 or internationally at +1 443-815-4447.