With gold trading above $3,400 per ounce and looking set to clear new record highs above $3,500, we want to add some precious metals exposure into the portfolio.

Specifically, we want to own gold royalty companies. We love the royalty model for its capital efficiency. Royalty companies don’t spend a dime digging through miles of earth to mine and process precious metals. They simply provide the financing for other gold companies to do the heavy lifting, and in exchange, they get a share of production.

Most mining companies funnel a big chunk of their profits right back into capital expenditures, leading to lackluster free cash flow margins in the single-digit range. Top-tier royalty companies, on the other hand, can turn over 50 cents of every dollar in revenue into free cash flow.

The company we’re recommending today is Triple Flag Precious Metals (NYSE: TFPM). Headquartered in Toronto, Canada, Triple Flag was founded in 2016 and has become one of the fastest-growing new entrants into the gold royalty business. In the last seven years, it has increased its revenue at a 36% compounded annual growth rate (“CAGR”). This year, it’s expected to generate $322 million in revenue and $182 million in free cash flow, for a stellar 56% free cash flow margin.

The company’s portfolio includes 235 royalty assets, with 23 producing mines and 203 in the development and exploration stage. Approximately 75% of Triple Flag’s royalty revenue comes from gold royalties, with the remaining split across silver, copper, nickel, lead, and zinc. The company largely focuses on politically stable, mining-friendly jurisdictions like Canada, Australia, the U.S., and South America.

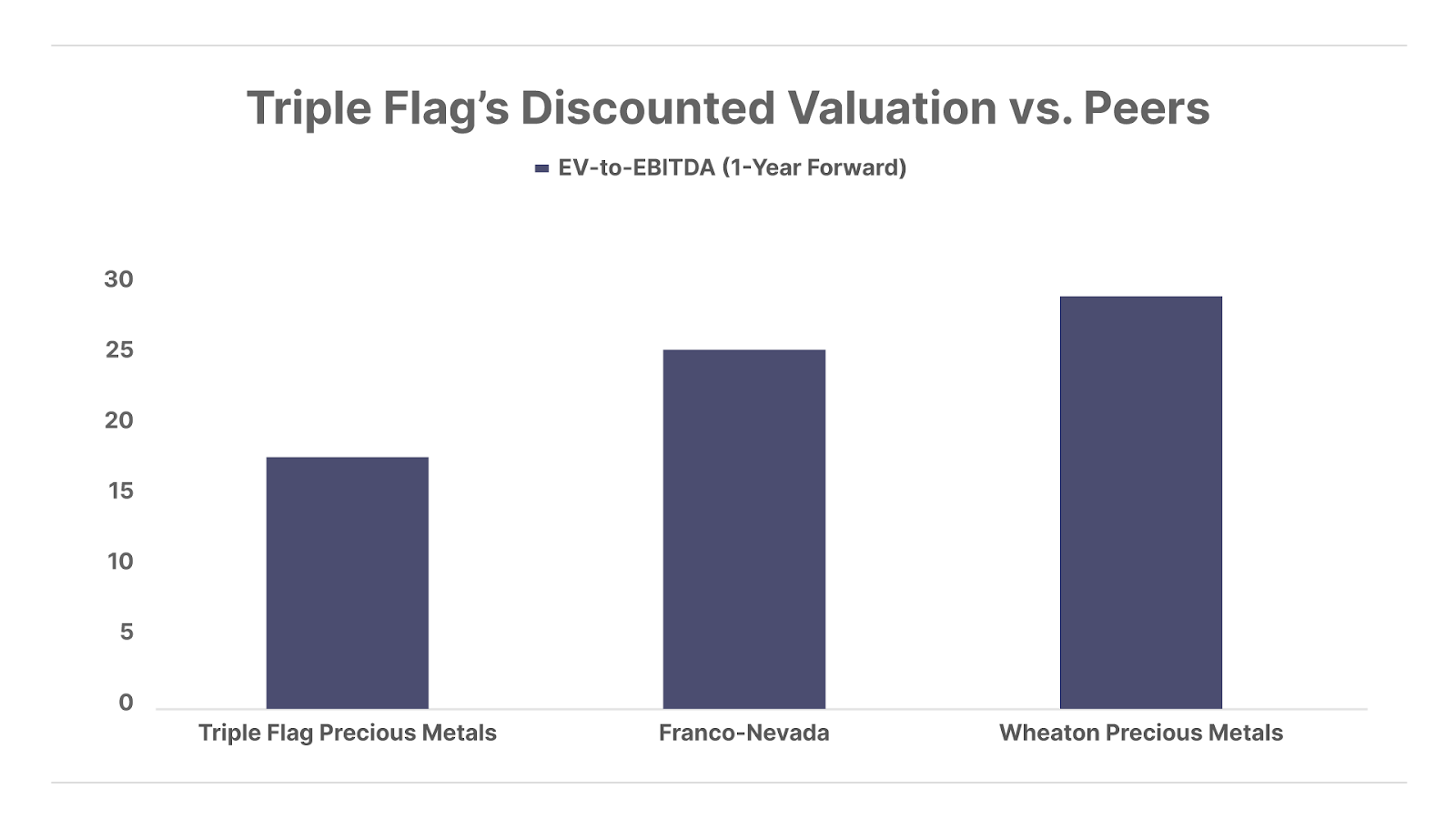

The shares have generated a CAGR of 19% since it became publicly traded on U.S. exchanges in 2021. Despite its impressive history of rapid growth and shareholder returns, the business is attractively priced at a one-year forward multiple of just 18x enterprise value-to-EBITDA (earnings before interest, taxes, depreciation, and amortization). That’s a 30% discount versus fellow gold royalty company Franco-Nevada (FNV), and a nearly 40% discount to Wheaton Precious Metals (WPM).

It’s also worth noting that legendary activist investor Paul Singer has placed a big investment in Triple Flag, through his asset management company Elliott Management. As of Q1 2025, Triple Flag is one of Elliott’s top positions, making up nearly 22% of the total portfolio.

This is a stock we want to own for the long run, and thus we plan to buy shares outright in this initial trade. In the future, we may trade around this position by selling puts or covered calls on Triple Flag, and will alert you to any future trades we make before we place them.

We’ll plan to acquire 200 shares at around $23 per share, for a total position size of around $4,600 or about 5% of total portfolio capital.

| Action to Take: Buy Triple Flag Precious Metals (NYSE: TFPM) up to $25 per share |

Good Investing,

Ross Hendricks