Issue #138, Volume #2

The Solution: A Business That Has Survived Both For 100 Years

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Tariffs are a tax… The spending will never stop… Look at the budget numbers… Largest tax increase of our lifetime… Hyperinflation and war are on the way… Build your family fortune… Jobs numbers grim again… Oracle loads up its debt… |

At our 2024 “Farmboree” – that’s the Porter & Co. Annual Conference at my farm in Maryland – I was roundly criticized for explaining:

-

Tariffs are taxes and, ultimately, consumers pay 100% of all taxes, whether they’re levied directly or indirectly

-

The spending will never stop – ever

Likewise, whenever I’ve written about these issues, many of our dear, paid-up subscribers have objected, mostly by parroting President Donald Trump’s talking points (which are economically illiterate).

Thank you for pissing off so many… I believe you’ll be completely wrong regarding tariffs and Trump’s ability to levy them. The people are learning and once they see the impact that they have far more money in their wallets they will never want to go back to a system that puts them in bondage. –Tom O.

Well, finally, the receipts are in. Trump’s first federal budget (passed by a Republican-controlled Congress) took effect on October 1. How does Trump’s budget reform the government, reduce waste, and eliminate the deficit?

Brace yourself. This one is a real shocker (sarcasm):

Trump’s budget has made our financial situation materially worse.

-

October 2025 federal spending was $689 billion (+18%)

-

October 2025 tax receipts were $404 billion (+24%)

-

October 2025 deficit was $284 billion (+10.5%)

– Comparison between October 2025 and October 2024. Source: Monthly Treasury Statement, November 25, 2025

Trump managed to both raise taxes substantially and grow the deficit at double-digit rates. That’s the worst possible outcome. Trump’s budget harms the economy (taxes are a cost of production) and doesn’t do anything to reduce the risk of a financial collapse – it makes it more likely!

These numbers don’t account for the total economic damage that’s being done by Trump’s taxes (aka tariffs) because they don’t show how many businesses shut down because they couldn’t pay the tariffs. But you are seeing that fallout in the jobs numbers.

Trump’s tariffs represent the largest tax increases of my lifetime.

They will have a major negative impact on capital investment, economic growth, and employment – just like all taxes do.

You’ll undoubtedly see or hear Trump crowing about the $31 billion in tariff revenue the government collected in October. It’s bizarre to hear Republicans (historically, the party of small government and low taxes) bragging about collecting billions in additional taxes! But beyond this oddity, it’s inane to brag about policies that are making our country’s financial crisis worse: our deficit was $105 billion more this October than last October.

If Americans genuinely want a healthy economy and a currency that won’t continue to spiral toward zero, then we must cut the cost of government substantially. This isn’t a political argument. It’s just math. And math doesn’t care about your feelings or who you voted for.

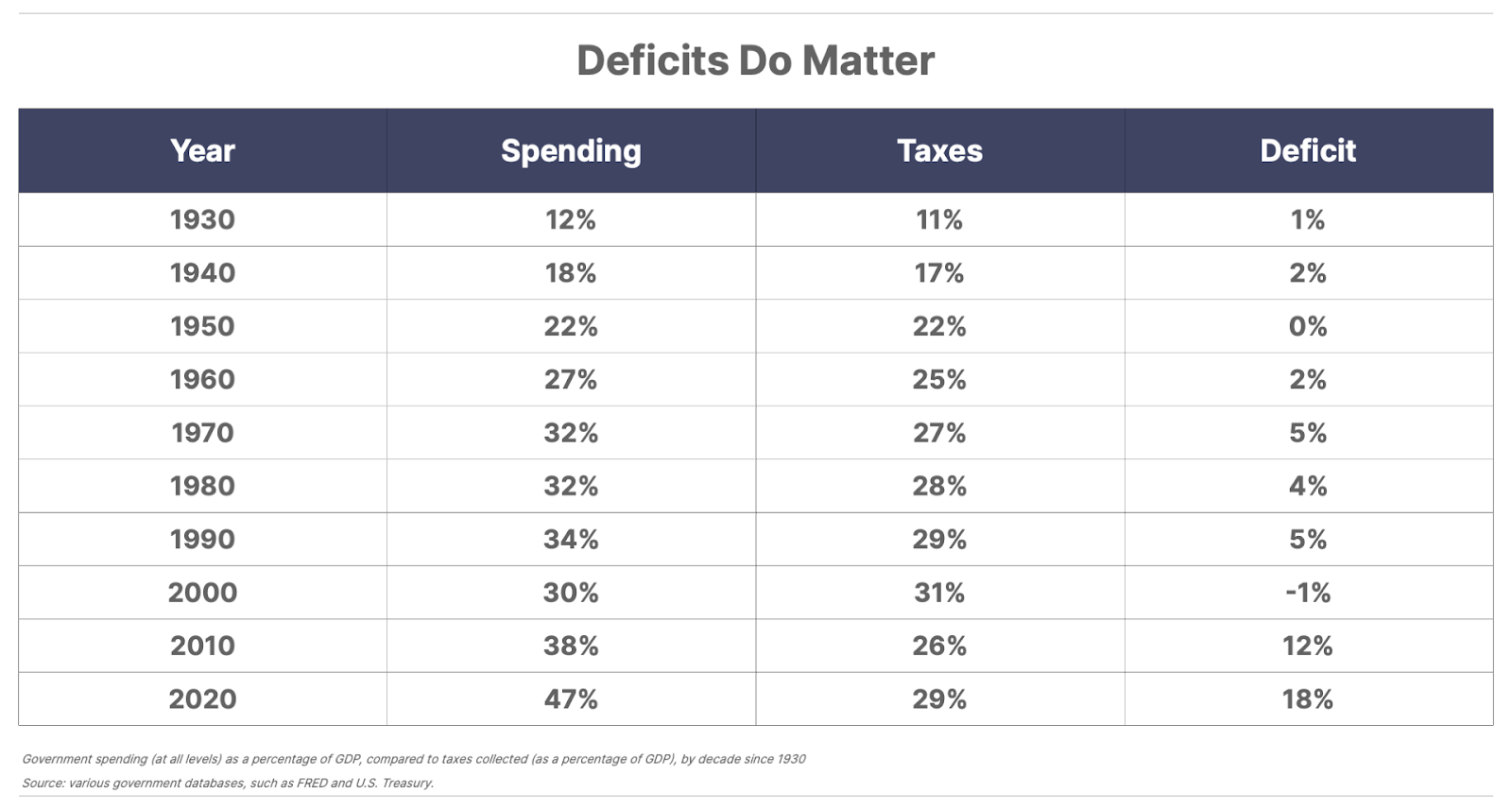

Government spending (state, local, federal) is now more than 40% of U.S. gross domestic product (“GDP”). History shows that governments cannot consistently collect more than about 20% to 30% of GDP in taxes, because beyond that level the costs (both direct and indirect) to collect the taxes exceeds the resulting revenue.

In other words: we have roughly twice as much government as we can afford. Tariffs won’t fix this. People will simply alter their behaviors to avoid the tariffs and that revenue will begin to fall, while the damage they’ve done to supply chains and trade will remain. Here’s a long-term look at these issues. Anything jump out at you?

Since the Global Financial Crisis of 2008-2009, when our government first began printing large amounts of money (“quantitative easing”) to bailout the world’s biggest banks, it has consistently run larger and larger deficits, in the false belief, as the late Dick Cheney said, that “deficits don’t matter.”

The average voter hasn’t figured out yet (and probably never will) the reason he can’t afford anything anymore isn’t because of greedy capitalists. It’s because the enormous size of the U.S. government makes everything unaffordable.

Unfortunately for all of us, the spending will never stop. “Nothing stops this train” is economist Lyn Alden’s succinct explanation. Neither party is economically literate – but that’s not the real problem.

The real problem is the incentives we’ve created in our extremely progressive tax code.

There are only 20 million U.S. households that pay more than $25,000 in income taxes, on a net basis (after factoring in all direct transfer payments and benefits). That’s only 15% of all households. These families pay for more than 85% of all income taxes raised. Most households – 125 million – pay nothing, or next to nothing.

[Editor’s note: Tax data is from the Congressional Budget Office (CBO) and the Tax Foundation, which provide the most comprehensive analysis of household tax payments. The latest detailed quintile-level data available is from 2019.]

You may believe this is “fair” or good public policy. And I’m sure I won’t change your mind. But I will point out that when seven families show up for dinner and only one family pays, the six families who aren’t paying have a huge incentive to order the most expensive stuff on the menu – and dessert.

Because most voters don’t pay any meaningful amount of taxes and so many are net direct beneficiaries of government spending, all the incentives in our current system of government are for more spending. And so that’s what is going to happen.

Our system is broken in the way all democracies inevitably break: voters looting the Treasury. And the only way this ends is the way these things always end: hyperinflation and, usually, war.

Americans believe that because the whole world accepts our paper money and owns our debt, that this won’t happen here. But they are dead wrong. Math doesn’t care about “exceptionalism.”

What should you do about this stark reality? Well, tomorrow, I’m giving all of our paid-up subscribers the ultimate solution.

This isn’t just another stock pick. It’s the perfect solution for what we face today with run-away government spending and the risk of a global war growing every day.

My newest recommendation is one of the few, genuinely elite businesses in the entire world. And not one of you has ever heard it – because it didn’t exist a year ago.

It’s also one of the most durable businesses the world has ever seen. Yes, I know that’s a contradiction – but when you read the new issue of Complete Investor you’ll understand how a century-old business can be less than a year old.

Sincerely, I urge you to please read this issue, above all others, carefully. It’s no exaggeration to say that what is in tomorrow’s Complete Investor could, all by itself, build a fortune for your family. A fortune that will last 100 years… or more.

In fact: I have no doubt this month’s recommendation will prove to be the best recommendation of my entire career – surpassing even Hershey, Microsoft, and W.R. Berkley.

I’ve been writing investment research since 1996 – 30 years next July. In my entire career I’ve never – not once – seen a better investment idea. Nothing else even comes close.

But, I know, most of you will dismiss this idea out of hand. The enormous value and potential of this situation isn’t obvious to most inexperienced investors. This opportunity doesn’t fit into any of the preconceived notions about investing that the media (CNBC) and Wall Street have sold you. You – virtually all of you – will say: “Oh, this isn’t for me. There’s not enough upside. I don’t have five years’ to wait. I need something that’s going to make me rich tomorrow.”

Meanwhile, this company will outperform almost every other business in the S&P 500 over the next 25 years. And longer. It is a very, very special business.

Complete Investor will be in paid-up subscribers’ email boxes tomorrow at 4 pm ET. I genuinely cannot wait for you to read it.

The Last Gold Bull Market

The last great gold bull market of our lifetime has already begun. Global debt is exploding, confidence in the dollar is cracking, and nations everywhere are turning back to gold. The Great Reset is really about gold’s return to the monetary system – a moment that will define the next decade… and those positioned early could reap generational wealth.

Click here to see why this is the last gold bull market that truly matters.

Three Things To Know Before We Go…

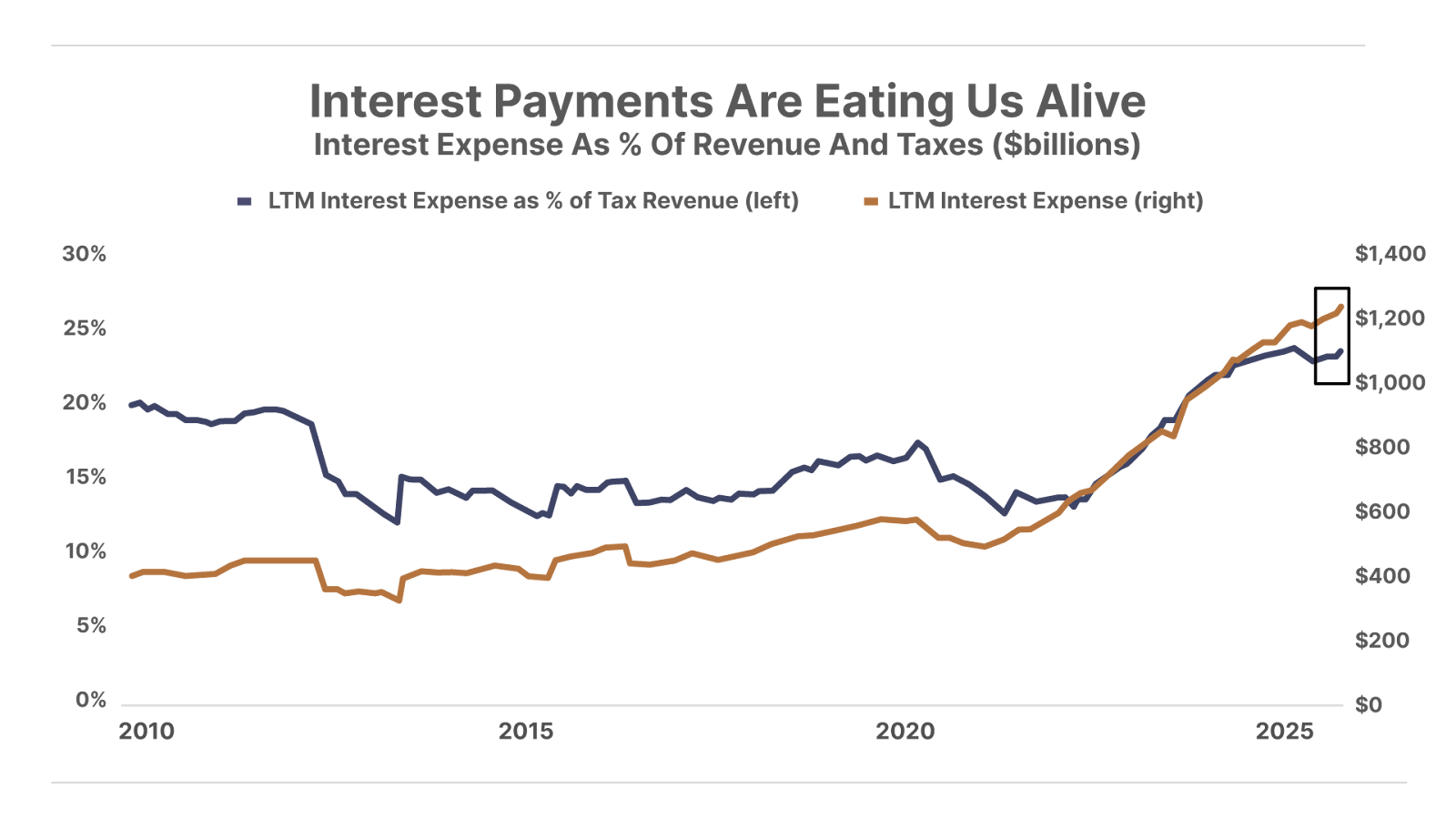

1. The U.S. government’s interest expense is surging. Adding some detail to what we outlined above… interest costs on federal debt reached a record $1.24 trillion over the last 12 months. Even more worrisome, interest expense as a percentage of government tax collections has doubled over the past four years to nearly 24% – meaning nearly 25 cents of every dollar the government collects in taxes is being spent on debt service alone. Interest is now the government’s second-largest expenditure, exceeding both defense and healthcare spending.

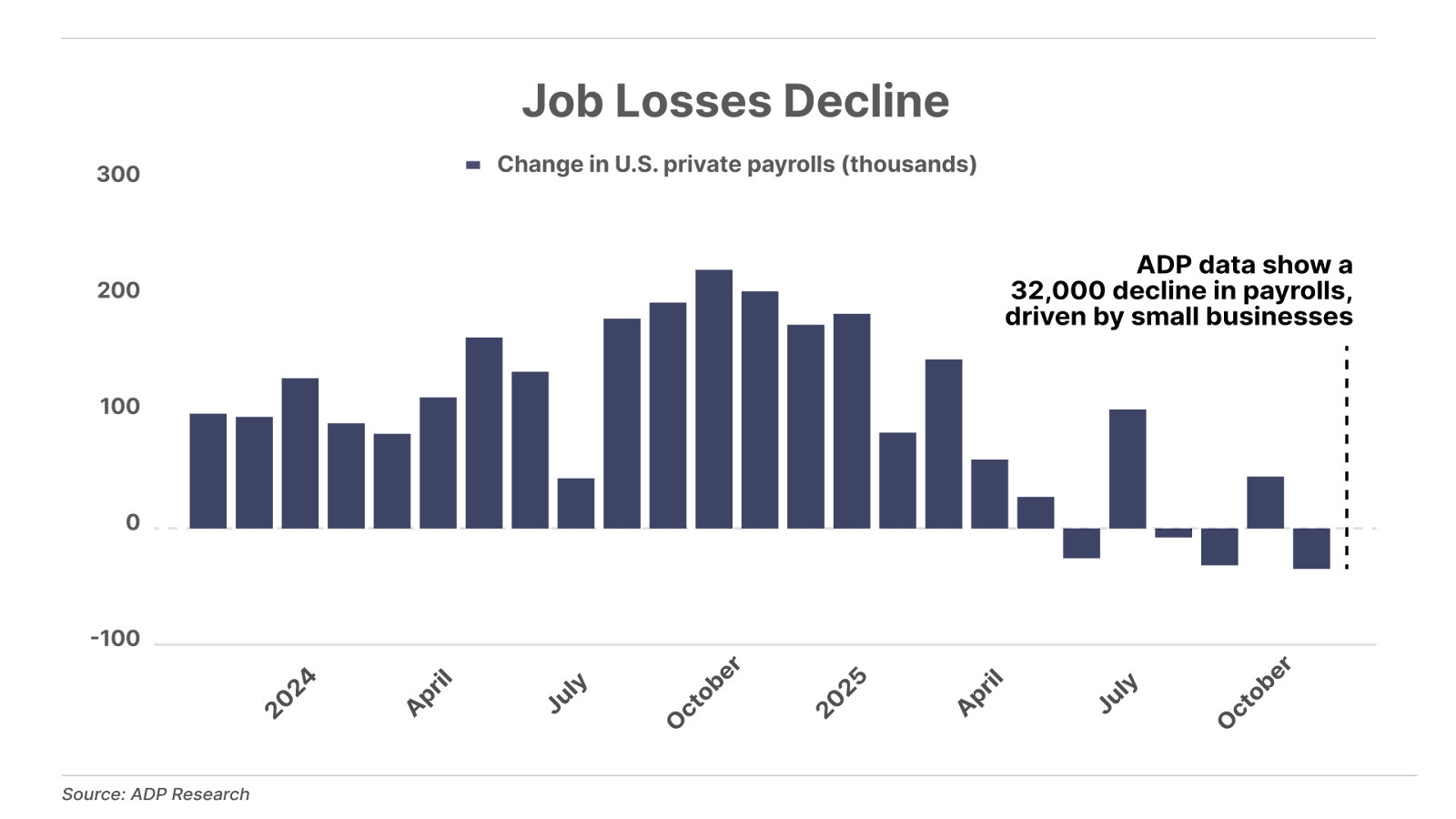

2. ADP warns of continued weakness in the labor market. This morning, payrolls processor Automatic Data Processing (ADP) reported private-sector payrolls decreased by 32,000 in November, the largest monthly decline since early 2023. Wall Street economists had expected a gain of 10,000 jobs. The decline was especially apparent among smaller companies – those with fewer than 50 employees shed 120,000 jobs, the largest monthly decline since the peak of the COVID lockdowns in May 2020. The probability of a December Federal Reserve interest rate cut is now 89% – up from 83% one week ago – according to the CME Group’s FedWatch tool.

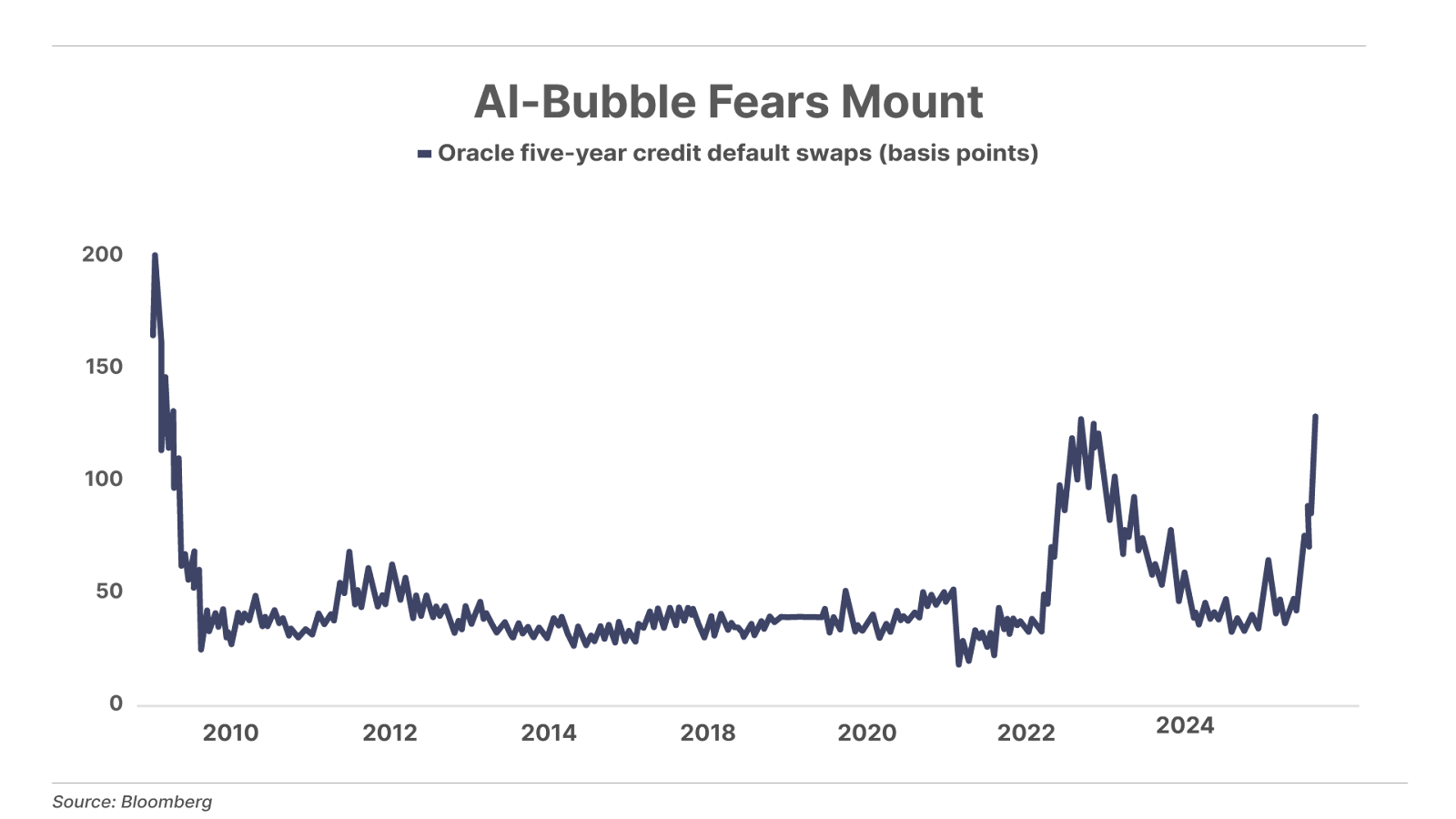

3. Oracle credit default swaps hit the highest levels since the Global Financial Crisis. The cost to insure against an Oracle (ORCL) default (measured through the company’s five-year credit default swaps) jumped to 128.1 basis points per year – a 16-year high. This spike comes after Oracle issued tens of billions of dollars in new debt this year to fuel its AI expansion – including $18 billion high-grade bond sale in September. Credit markets are beginning to question if these AI investments will generate the returns needed to justify the spending.

And One More Thing… The AI Bubble Watch

The concern over Oracle’s leveraged spending on AI capex is exactly what we warned in Monday’s Daily Journal:

An AI bubble and real tech innovation can co-exist… As the speculative frenzy builds, too much capital floods into an industry chasing increasingly marginal investments. The boom eventually gives way to a devastating bust.”

Oracle’s credit spreads widening is an early sign that institutional investors are beginning to doubt the economics of the AI-data-center arms race. When credit markets begin to price in financial stress for a leading hyperscaler, it means that the exuberant AI capex cycle is entering a riskier phase.

That’s why we recently shared with Trading Club members a strategic hedge designed to protect against a potential collapse in the AI boom – offering the potential for 10x or greater upside if the AI bubble bursts.

Tell us what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Porter Stansberry Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.