Special situation investing aims to exploit specific corporate actions to capture profits with minimal risk. And unlike many investment strategies, this one can work relatively quickly and in just about any market environment, making it a fantastic complement to a traditional investment portfolio.

Finding Great Investment Opportunities Hiding in Plain Sight

John Paulson had a secret.

And in 2008 – during the worst of the Great Financial Crisis – the relatively unknown hedge-fund manager used it to make a literal fortune.

We don’t need to remind you that 2008 was the worst year for stocks since the Great Depression. The major U.S. market indexes plunged 40%. Virtually no one on Wall Street escaped unscathed.

Even hedge funds – which, as the name implies, tend to “hedge” their long positions with short sales designed to profit when stocks fall – performed terribly. According to data provider HFR, the average hedge fund lost more than 18% in 2008, by far the industry’s worst year on record.

Yet Paulson’s flagship fund returned a mind-boggling 38% that year, representing billions of dollars in profit… and that’s after accounting for the hefty “2 and 20” management fees (2% of assets and 20% of profits) hedge funds typically charge.

These results made Paulson a Wall Street legend. But what was behind his stellar returns?

Paulson was famously one of the few investors on Wall Street who saw the subprime-mortgage crisis coming. So, you might understandably assume it was his bearish bets on upside-down loans or troubled banks that drove his record results.

That wasn’t exactly the case. Those short positions certainly padded his returns. But it was actually a single long position – in an unassuming consumer stock – that was responsible for a huge portion of Paulson’s outsized returns that year.

The story starts in July 2008, when U.S. beer-maker Anheuser-Busch (BUD) agreed to be acquired by Belgian brewer InBev NV. The deal valued BUD at $52 billion ($70 per share), and was scheduled to be completed in November of that year.

Longtime readers of Porter’s work will no doubt remember that deal. He originally recommended shares of BUD in 2006 – even telling subscribers they could put up to 25% of their portfolios into this “no-risk” stock. Those who followed his advice ultimately made 80% returns when the deal closed that fall.

BUD shares initially moved higher on the InBev news, trading near the $70 offer price. However, they soon began to sell off – along with virtually every other stock – as the financial crisis intensified that summer.

By October, BUD shares were trading as though the deal had never been announced. The stock had fallen back to near $60 as analysts became increasingly concerned that InBev would be unable to secure the financing necessary to complete the purchase. And that’s when Paulson made his move.

You see, Paulson had spent his early years on Wall Street in mergers and acquisitions (“M&A”). He had worked on countless arrangements like the BUD acquisition, and was confident it would close as planned the following month. The economics of the deal still made sense despite the higher financing costs due to the crisis. And unlike many M&A deals, there were no obvious regulatory concerns.

That meant BUD shares were offering a rare, low-risk opportunity to make spectacular profits. As Paulson explained in his 2008 year-end letter, investors had the opportunity to earn nearly 100% annualized returns as shares eventually rose from their October lows near $60 to the $70 offer price in November…

“The spread in InBev’s $70-per-share, all-cash acquisition of Anheuser-Busch widened in October to over a 90% annualized rate. The market mispriced the risk of the transaction, creating a strong buying opportunity.

“We aggressively added to our position in October 2008 with our funds becoming the largest shareholder of Anheuser-Busch and Anheuser-Busch becoming our largest position.

“When the merger closed in November at the agreed $70 price, the gain represented the largest profit we ever earned on a spread deal in our history.”

The Magic of “Special Situations”

The strategy Paulson used to safely make billions during the worst financial crisis in generations – “merger arbitrage” in Wall Street parlance – is one of several that are collectively known as “special situation” investing.

This type of investing is slightly different than the high-quality, capital efficient approach we love here at Porter & Co.

Special situation investing aims to exploit specific corporate actions – like company liquidations, reorganizations, spin-offs, takeovers, and, yes, M&A – to capture profits with minimal risk. And unlike many investment strategies, this one can work relatively quickly and in just about any market environment, making it a fantastic complement to a traditional investment portfolio.

Special situations can take any number of forms, but at their core they generally involve a good company facing a problem of some kind.

Of course, most investors avoid investing in companies that have problems – particularly, serious problems – and rightly so. However, certain problems can create tremendous opportunities under the right circumstances.

Specifically, the best special situation investments tend to have a few key characteristics in common.

First, the company or stock should have a significant – yet solvable – problem. Examples include issues like bad management, inefficient operations, or poor strategic planning. Companies with more intractable problems – like obsolete products or unprofitable business models – are unlikely to qualify.

Second, the stock under consideration should be cheap, ideally on both an absolute basis and relative to its potential value if the company’s problem were solved. This dramatically reduces the investment risk.

Third, there should be a clear, identifiable solution to the company’s problem.

The Anheuser-Busch acquisition had all three of these characteristics.

The problem was clear… the financial meltdown had created serious (yet ultimately unfounded) doubt that the agreed-upon deal would close, which caused shares to fall significantly below the offer price.

Anheuser-Busch was otherwise a fantastic business trading at a reasonable valuation, giving investors like Paulson a margin of safety even if the deal somehow fell through.

And the solution to this problem was remarkably simple… All that was required to profit was the patience – and discipline – to hold on to shares until the deal was done.

Unfortunately, most special situations aren’t so straightforward. Often, concrete changes are required to solve the company’s problem and unlock its full value.

This might mean replacing an underperforming CEO, selling or spinning-off a portion of the company, or reorganizing the business entirely.

Such actions can free up significant gains for shareholders. However, companies rarely take these steps organically.

So the fourth – and arguably, most important – characteristic of a great special situation investment is a clear catalyst to put that action into motion.

Identifying companies with this combination of characteristics isn’t easy, but when you do find one, the results can be extraordinary.

How “Catalysts” Kick New Life Into Struggling Companies

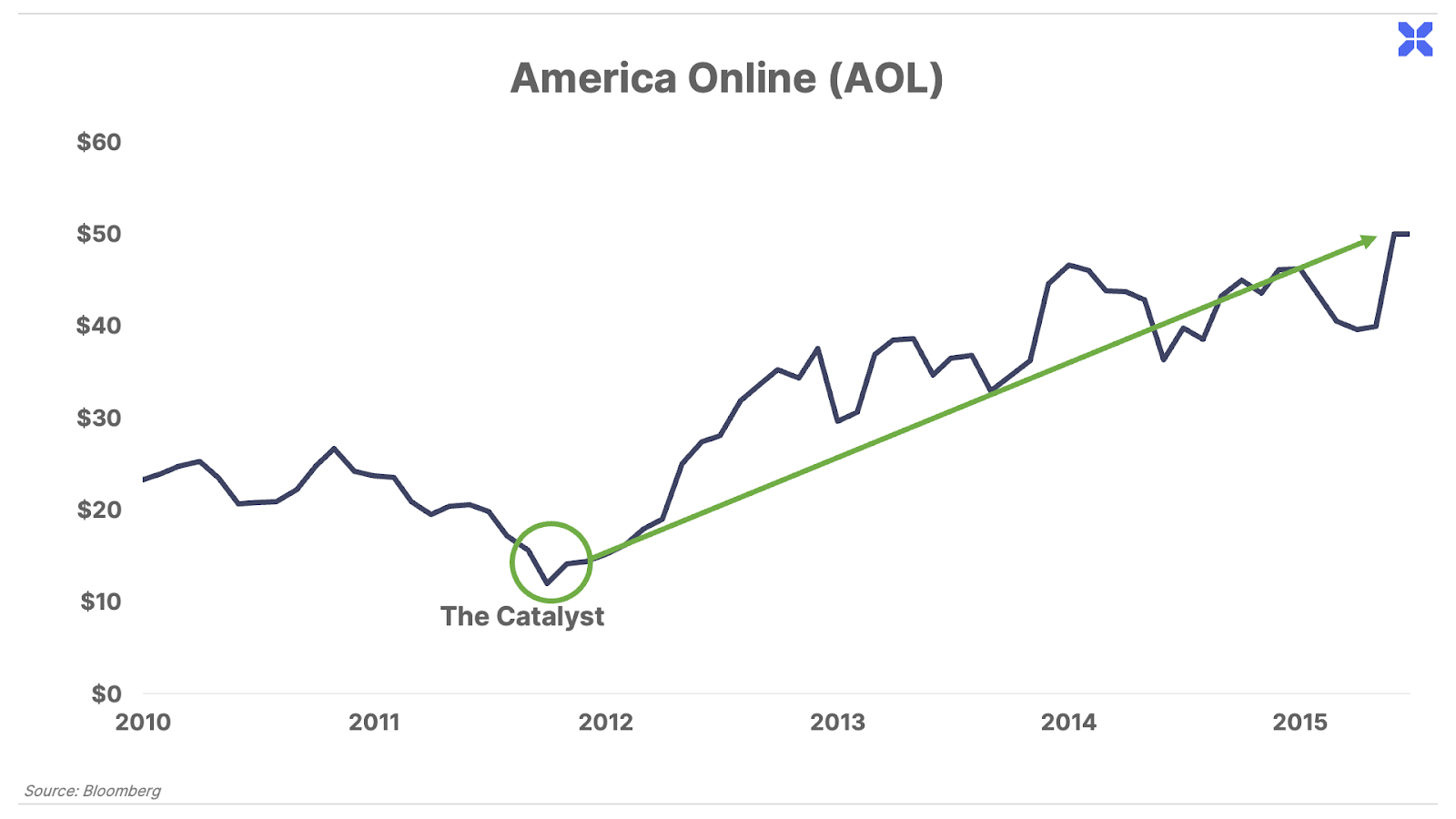

For example, online media company – and former dial-up internet-service provider – America Online (AOL) was left for dead following its spin-off from Time Warner in 2009.

But in late 2011, a catalyst kicked off a series of corporate actions that improved the company’s outlook. These included selling a cash-hemorrhaging local-news business called Patch, as well as returning nearly $1 billion – which the company had earned selling valuable patents to Microsoft – to shareholders.

AOL shares soared as much as 250% before Verizon bought it in 2015.

Around the same time, Netflix (NFLX) was facing significant problems of its own.

By the summer of 2012, shares had crashed more than 80% from their recent highs as the company struggled to find its footing in the rapidly changing video-rental industry.

But a catalyst that October set off a series of strategic initiatives – including going “all in” on its then-controversial shift to online streaming – that ultimately drove its stock 5,000% higher over the next several years.

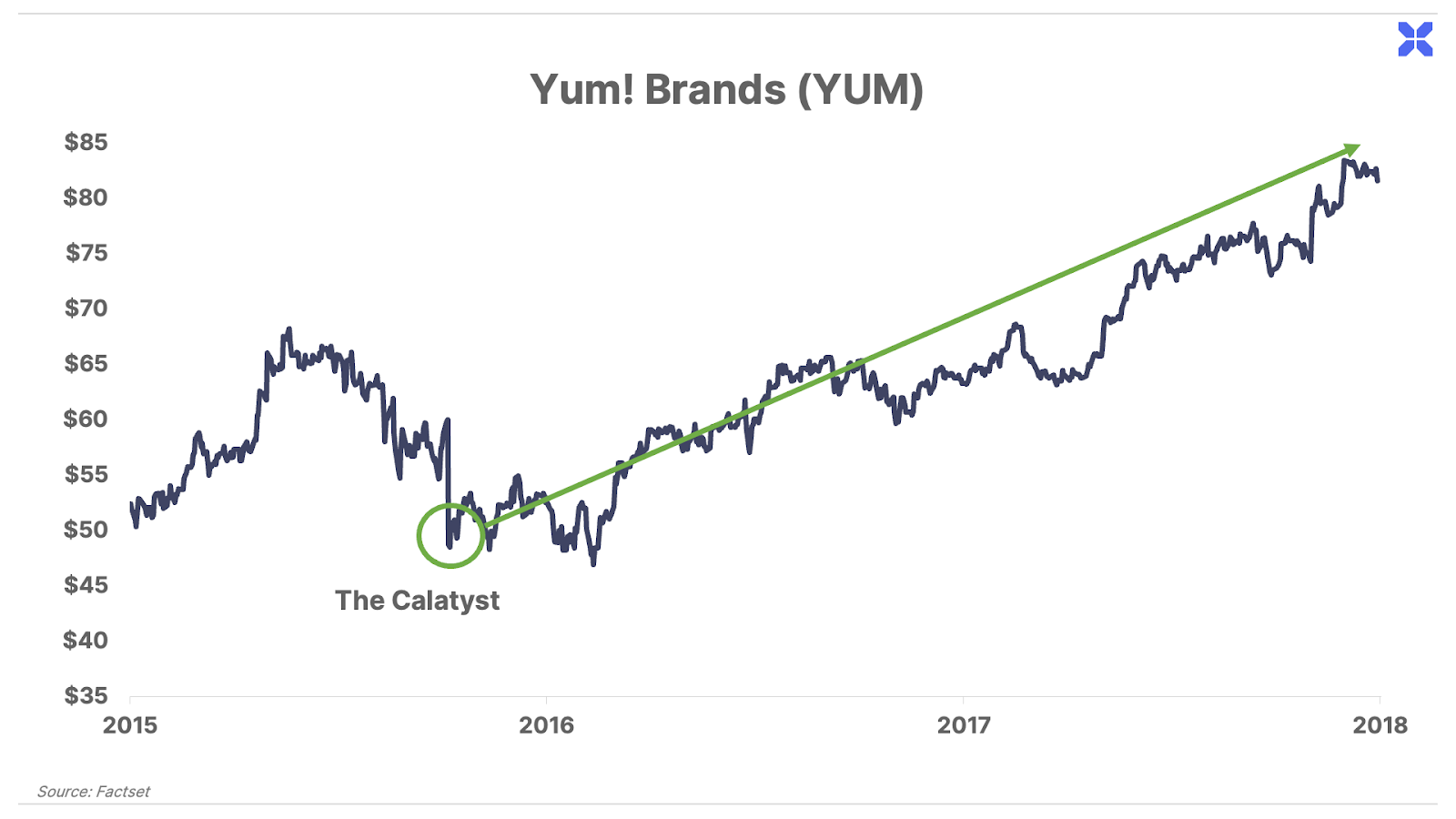

Shares of restaurant operator Yum! Brands (YUM) went nowhere for years following the 2008 financial crisis.

Much of the company’s struggles stemmed from problems in its China-based businesses. These problems were a significant distraction from the company’s larger U.S.-based operations, and likely dissuaded would-be investors who weren’t interested in international exposure, particularly to China.

But in 2015, a catalyst initiated a series of corporate actions, including spinning off its China-based businesses from the rest, making two new companies.

Yum China (YUMC) began trading as a separate entity in 2016 at $25 per share. Since then, shares have moved to $70. And together, shares of the two new companies are up nearly 250%, more than double the return of the S&P 500 over that time.

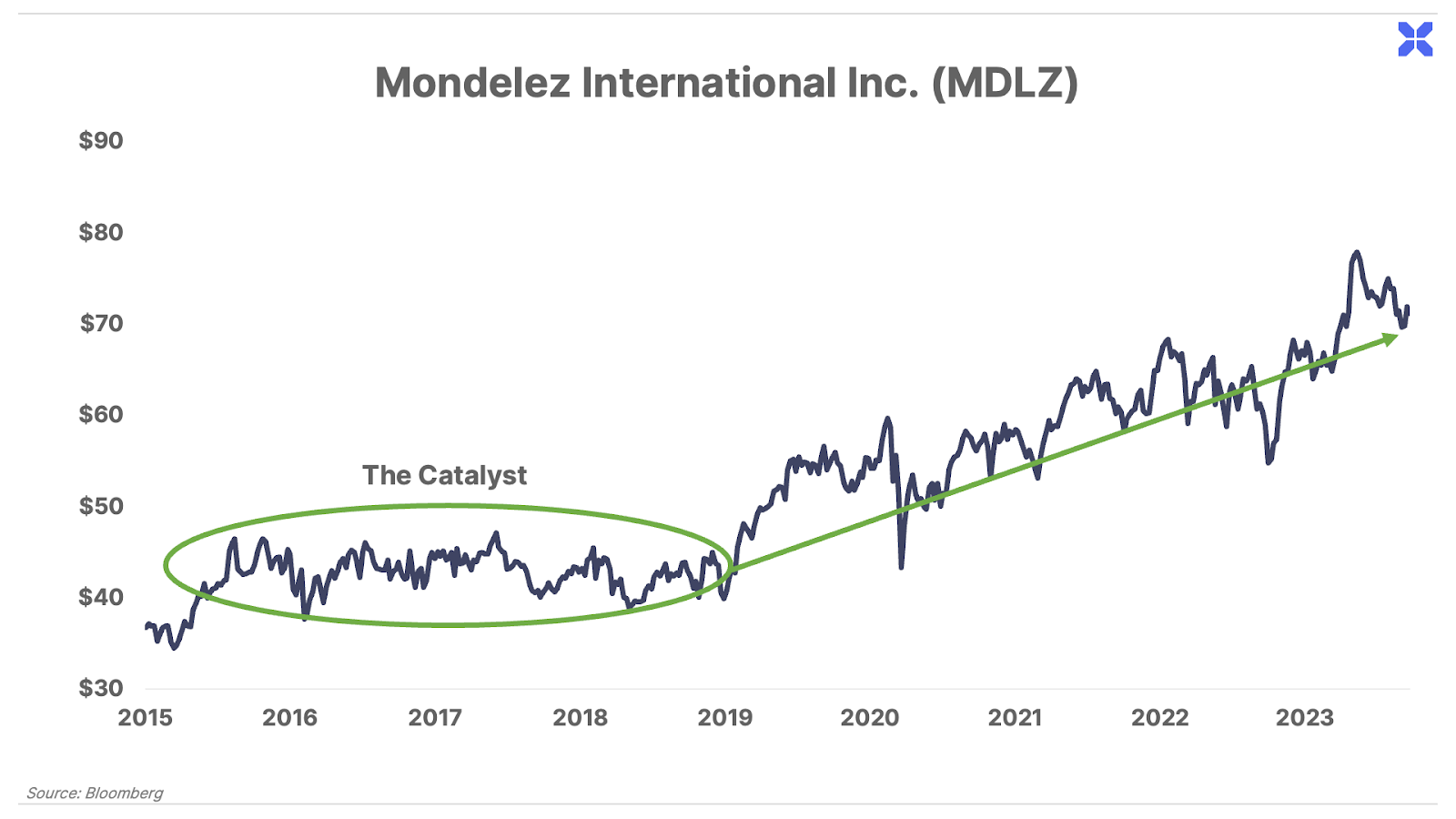

Shares of snack-food giant Mondelez International (MDLZ) were similarly stagnant for much of the 2010s as its business dramatically underperformed top competitors like Coca-Cola and The Hershey Company.

But beginning in late 2015, a catalyst kicked off a series of gradual corporate actions – focused primarily on cutting costs and improving the company’s operating margins – that has seen shares more than double over the past five years.

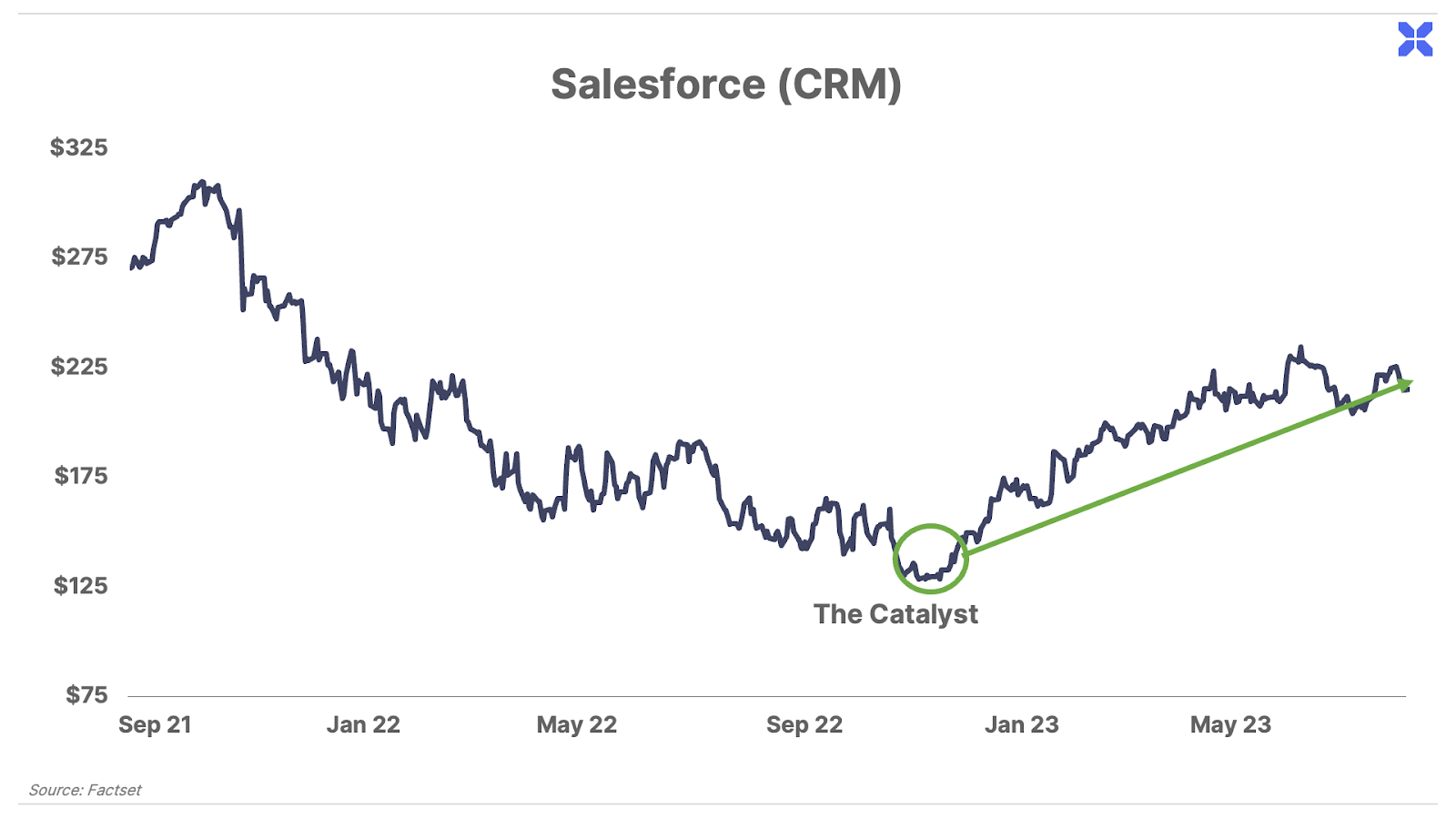

And just last year, Salesforce (CRM) – the world’s leading customer-relationship-management software firm – was struggling. The company’s once-impressive margins had flatlined as its operating expenses soared, causing its share price to crater more than 50% in the course of a year.

But in December, a catalyst emerged that triggered a series of corporate actions – including a review of expenses that led to cost reductions to various aspects of its operations – that are already paying off. Porter & Co. Distressed Investing subscribers, who bought CRM shares in March of this year, have seen 24% gains since our recommendation. (The stock is up 50% year to date.)

Not Everyone Sees the Low-Hanging Fruit

Of course, these are just a handful of the many special situations that any public-market investor could’ve taken advantage of over the past decade alone… Undervalued companies with a serious – yet solvable – problem, a clear solution to that problem, and most importantly, a catalyst to put that solution into motion.

But… We have to ask…

How many of these low-risk, high-potential-return opportunities did you personally invest in?

We’re betting your answer rounds down to zero. In fact, if you’re like most folks, you probably didn’t realize many of these opportunities even existed.

That’s because while identifying these opportunities is simple, it’s not easy. In fact, the in-depth research required has historically been out of reach for all but the most sophisticated professional investors. But not anymore…

Porter & Co. is launching an all-new, first-of-its-kind service dedicated to identifying the most lucrative special situation investments for individual investors. We can’t wait to share it with you.

Porter & Co.

Stevenson, MD

P.S. If you’d like to learn more about the Porter & Co. team – all of whom are real humans, and many of whom have X accounts (formerly Twitter) – you can get acquainted with us here. You can follow me (Porter) here: @porterstansb.