Issue #25, Volume #2

Readers Share Their Blunders… And Porter Responds

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Porter responds to readers’ three kinds of financial mistakes… Most financial advice out there is terrible… There is no substitute for buying high-quality businesses with track records of success… Porter’s offer to “Bill”… Trump’s crypto reserve announced… |

I spent my entire weekend replying to subscriber emails.

I’d wager that when I asked you to send me your stories about your biggest (financial) mistakes, you didn’t think I’d read all of them.

But I did!

In fact, I didn’t leave my house all weekend, except to go out to dinner on Saturday. I answered emails for more than 20 hours this weekend.

If you sent me an email, look for my reply – because I answered virtually everyone who wrote to me. (If you didn’t write yet, please take the time to do so. I read every email: [email protected])

The replies to my query came in three basic categories:

First, there were a lot of folks who said their biggest mistake was, more or less, me!

Some people took my sincere question about their biggest financial mistake and took the opportunity to mock me and/or to complain, loudly, about a stock they bought on our recommendation that has done poorly.

Also in this category were subscribers who complained that they’ve bought too many subscription research products, and/or that the research products they’ve bought from other publishers are not very good.

I’d put all these comments in a bucket labeled broadly as

#1: My biggest mistake was following bad advice or paying too much for bad advice.

I’ve been in financial publishing for 30 years.

And I’ll let you in on a little secret: most of the advice is terrible, especially if it sells well. And… even worse… many of the top-selling financial writers are crooks.

Michael Murphy, who wrote the best-selling tech letter in the late 1990s? Yep, he was a bank robber.

And Ken Roberts, who wrote some of the best-selling financial content of all time in the 1980s and 1990s? He told his unfortunate subscribers that trading commodities was the path to riches, describing commodities trading as the “perfect business.” I doubt if any of his subscribers ever made any money, but Ken sure did: his commodities brokerage featured some of the highest commissions in the industry! The Federal Trade Commission shut him down in the late 1990s.

And, you may not remember, but Wade Cook was the best-selling financial author in the world in the mid-1990s, which is when I started writing financial newsletters.

Cook’s firm had revenue in excess of $100 million a year, including a book that sold millions of copies annually called The Wall Street Money Machine. Mostly on the back of this one promotional book, he took his company (Wade Cook Financial Corp) public in 1997 when it was worth more than $200 million!

There was only one problem: Wade Cook was a taxi driver who didn’t actually know anything, at all, about finance. His “money machine” was selling covered calls. While this strategy can be used to generate income, the dynamics of the strategy make it very difficult (or impossible) to build lasting wealth because you’re long and short the same security.

Selling covered calls lets you keep all of the risk of owning a stock, while limiting your upside.

More risk, and less upside, is not the path to wealth.

Of course, much like Bernie Madoff, Cook made absurd promises about the riches you could create using this strategy. By 2000 he’d been sued by 14 different states for fraud. His company went bankrupt in 2003. And in 2007 he was sentenced to 88 months in prison for tax fraud. As far as I know, no one ever made any money using his “Wall Street money machine.”

Just as one of our subscribers actually recalled!

Gary D. wrote:

[My biggest financial mistake] goes back 35 years to a book I purchased called The Wall Street Money Machine. One chapter dealt with rolling stocks that regularly went from a low to higher price and then back down. After some research, I found such a stock that went from $15-$17 up to $23-$25 and then back down. Consequently, I bought 200 shares at around $17 and sold several months later at $24. I then waited for the stock to return to the teens to buy it again. Only problem was it never did. It was a stock you likely know of called AutoZone. If I would have just held it, it would now be worth $3,500/share and my 200 shares would be a cool $700,000.

When it comes to financial advisors, I’d recommend following the same strategy you should use in your investing: only buy the very best.

If you know that only about 7% of all stocks end up making all of the gains in the stock market, you should infer the same thing is going to be true with investment managers and investment advisors.

And just as I’d recommend never buying a stock (as a long-term investment) without a 20-year history and great results, I’d never recommend following any advisor (or any strategy) that can’t easily prove excellent results.

That’s why, starting in 2003, I was the first financial publisher to release a thorough, long-term track record of all of our products at Stansberry Research (the “Report Card”). That’s why, throughout my career, I’ve only published bona-fide experts with decades of experience in their fields.

Today, at Porter & Co. there’s no question that we have the highest-quality analytical staff of all time in this industry. Our three leading analysts (Marty Fridson, Erez Kalir, and myself) have more than 100 years of combined experience in our fields and decades of proven results. We proudly publish all of our results – our complete track record, including our “hall of shame” – in every full issue.

Of course, even the best financial research won’t protect you from buying the wrong stock or putting too much money in any given investment. No investment analyst is perfect. But this is what I know from watching investors over the several decades: the investors who learn to avoid risk like the plague do a lot better than the investors who seek it out.

And that leads directly to the most common financial mistake of all:

#2: Taking a huge loss on a speculative investment.

I saw dozens and dozens of emails like this one:

Lee E. wrote:

In my 20s (1970s), investing some inheritance into a Colorado Ranch Recording Studio that was funding a ‘Mountain High’ cocaine party. Also in my 20s, investing some inheritance at the market top in a U.S. gold and minerals penny stock.

And James A. lost a fortune in one of the most notorious gold scams of all time, Bre-X:

Was sitting on a nice six figure profit in a small gold company, think the name was Bre-X. Geologist faked gold in core samples, committed suicide by jumping out the back of a helicopter. Stock dropped to zero or thereabouts in two days.

What’s one thing these experiences have in common? None of them involve high-quality businesses with a long history of success.

Here’s a good rule of thumb: never invest more money than you can afford to lose in a speculative investment.

And that doesn’t mean you shouldn’t ever invest in a new idea or a new business. It just means, when you do, you have to diversify – a lot.

Think about how many different companies venture capital groups fund and how few of these businesses (less than 10%) create all of the returns for the venture funds.

Benchmark Capital, for example, is probably the most selective venture firm in the U.S., and it has seeded almost 300 companies since 1995.

If you want to invest in high-risk opportunities, take some of your portfolio (not more than 20%) and divide by 300. That’s your position size per speculative investment. If you do that, you’d be surprised how well it works. Even a $1,000 investment in Amazon (AMZN) around the 2002 lows in the market would be worth more than $300,000 today. But… would you have really held this long? Maybe.

It seems easier to me to only buy proven winners. After all, an investment in Berkshire Hathaway (BRK) at the exact same time would be worth more than $10,000 today. That’s not a 300x return. But it’s still a 10x return. And that’s plenty. And you could have safely put 100% of your savings in Berkshire Hathaway and never had a sleepless night.

The lesson: you’re much more likely to do well as an investor if you only buy quality. And, if you’re going to speculate, keep your position sizes tiny so that you can withstand the volatility and hold for the long term.

And that leads to the final major mistake category…

#3: Selling way too soon.

One subscriber (he asked me not to publish his letter or name) told me about selling Berkshire Hathaway stock many years ago. He was a friend of Charlie Munger too, and Charlie told him not to sell. Ouch.

The first two stocks I ever bought in my life were Coke (1992) and Amazon (1997). I foolishly sold both in 1999. Had I not, those positions would have been worth more than $1 million today.

Mistakes like these have informed my mantra… Never sell a good business.

But, of course, we all make mistakes.

And, if you’re like me (over age 50), it can be a lot harder to recoup from big financial mistakes. Older investors are wiser and less likely to gamble – but we also don’t have as much time left to compound, so we can’t afford to make mistakes.

The most powerful letters I received were from people who’d made big mistakes, for a long time. And not just in their finances, but with their entire lives.

A long-time subscriber “Bill” told me (I’ve changed his name to protect his identity):

My greatest regret is spending 40 years as a drunken junkie. Since 2008, I’ve been trying to fix the mess I made of my life, but it’s very difficult with barely any funding. I miss great opportunities because I just don’t have the entry fees, and I’m running out of time at 68 years old. I work construction every day, but I can’t work as long as I should. I try to live on my meager earnings so I can invest a bit, but it’s pretty damn tough. I made the initial mistakes and blame no one but myself, but you asked. These “older years” are going to be awfully hard on me, I fear.

I loved that note. I loved it because “Bill” didn’t try to make excuses or blame anyone but himself. I’m going to offer “Bill” a complimentary Partner Pass membership and $100,000 in capital to use for free, but only if he’ll agree to use 100% of the money on Marty Fridson’s new Distressed Investing debt recommendations.

You see, I want “Bill” to have a second life.

And, I think the best way for older investors to build a second life is to focus on a little-known kind of investing that’s almost exclusively available to professional investors like Marty Fridson. But, with Marty’s help, I believe it’s possible for people like Bill to make 30%+ gains annually, by investing in a handful of these deals.

Best of all, this kind of investing automatically solves the most common mistakes investors make.

#1. These deals are rare, and they don’t come along every day. You won’t have too many deals to look at or to study. You won’t be overwhelmed.

#2. These deals are guaranteed by law. While it’s not technically impossible to lose money, it is extremely rare, if you know what you’re doing. I’d argue, if you’re being guided by Marty Fridson and you follow his advice, it’s virtually impossible to lose money.

#3. You can’t sell too soon. These investments have limited liquidity and, to garner the full return, you’ll have to hold until maturity, which happens on a specific day. That is typically two to five years, sometimes longer. And sometimes shorter. The point is, you’ll know exactly how long to invest: no more guessing.

Thanks so much for all of your notes this weekend.

I really appreciate you sharing and trusting me with your stories.

I hope you’ll watch this video that I’ve made about my biggest mistakes and my recent efforts to build a second life.

Three Things To Know Before We Go…

1. Tuesday is (maybe) tariff day. President Donald Trump’s tariffs on Mexico and Canada on more than $900 billion of imported goods annually are set to take effect on March 4. The tariffs could be lower than the 25% that Trump previously promised… and there’s a chance that – like when tariffs were set to go into effect on February 3 – they’ll be postponed. Think tank Tax Foundation estimates that, if the Trump administration moves forward with its plans, overall tariffs will rise to nearly 18%… and the last time tariffs were that high, they ushered in the Great Depression. Why would tariffs be a better idea now than they were then?

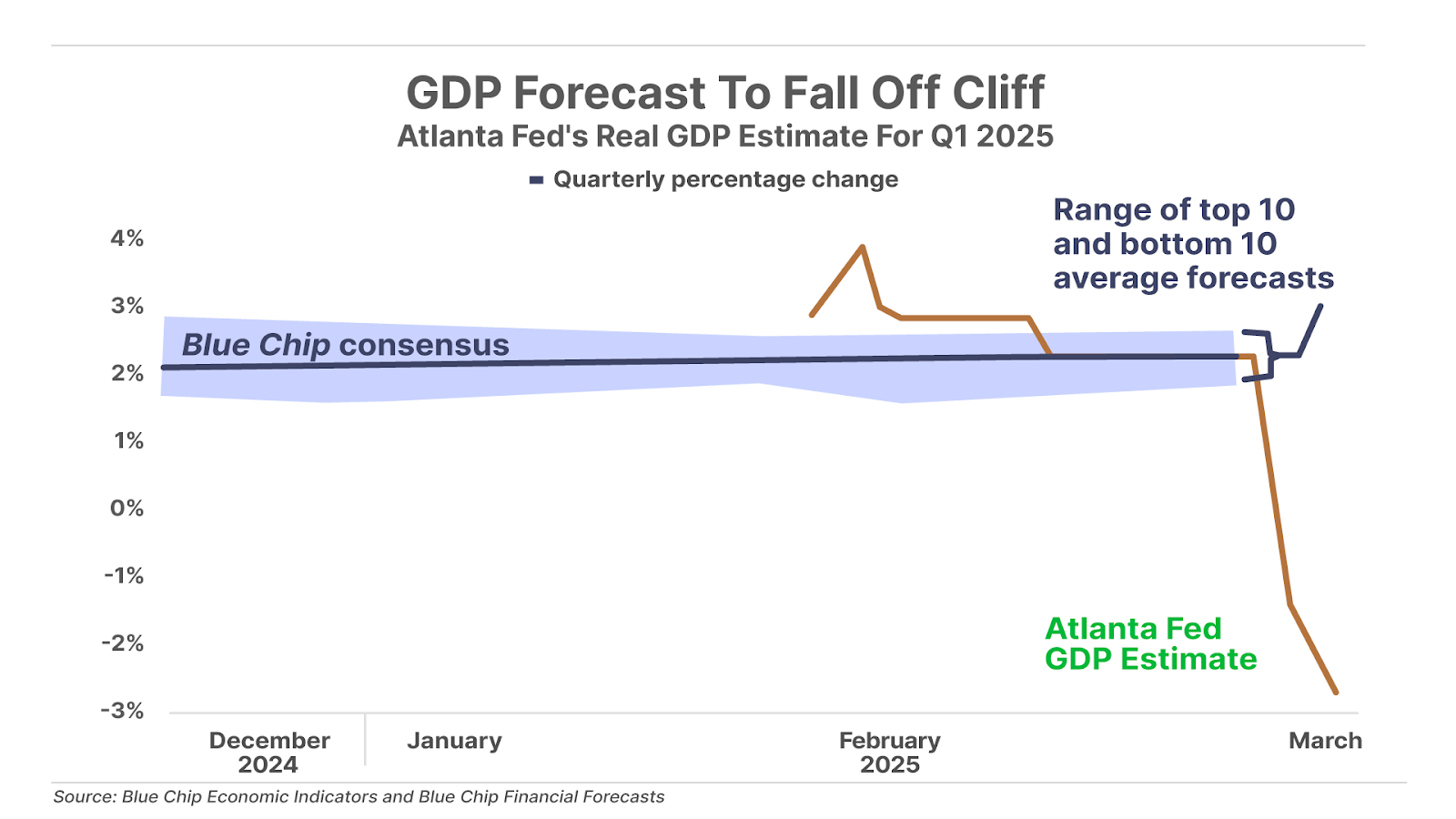

2. U.S. growth outlook plunges. The Atlanta Federal Reserve Bank’s real-time forecast for U.S. economic growth just took a major turn lower, with its Q1 GDP forecast plunging from a nearly 4% annual rate of growth last month… to negative 2.8% today. Most financial pundits have shrugged off the weak Q1 forecast as short-term noise from companies accumulating imported goods ahead of new tariffs – causing the trade deficit to balloon, and thus reducing GDP. However, a growing body of evidence indicates a more lasting economic slowdown, including the sharp drop in retail sales, home sales, and consumer confidence. All that will be compounded by higher inflation – which is in store this year.

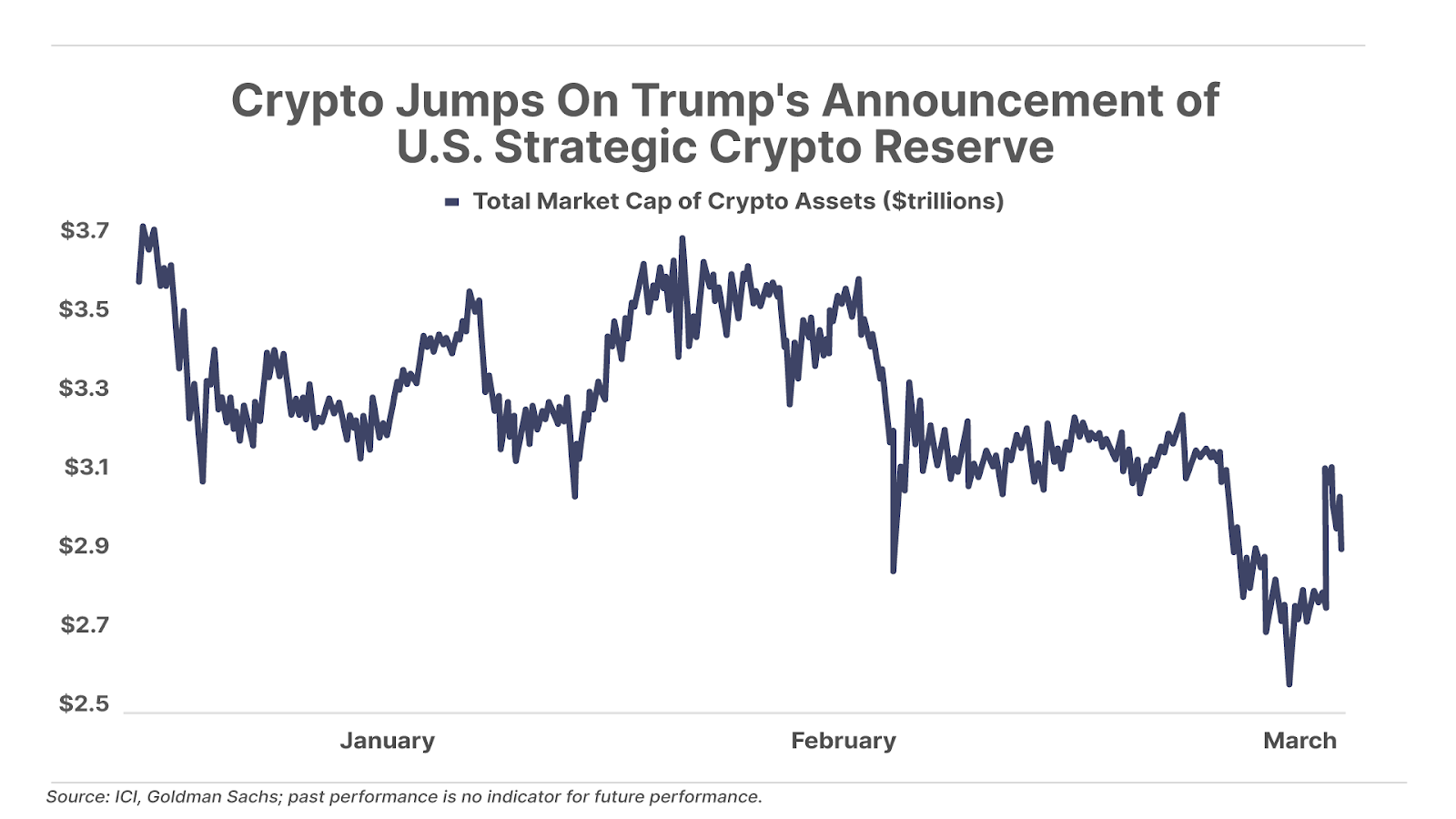

3. Crypto rallies on Trump’s announcement of a crypto reserve. Over the weekend, President Trump said that the U.S. will establish a strategic crypto reserve. Similar to the nation’s gold and oil reserves, a crypto reserve would serve as a hedge against the dollar in times of crisis. Bitcoin is trading 13% higher at around $90,250 following the news. Investing in hard assets like Bitcoin and gold helps avoid the debasement of government currency. That’s why Porter’s Permanent Portfolio (available to subscribers to The Big Secret On Wall Street) is heavily exposed to Bitcoin, and to hard assets.

And one more thing… Reader Poll

Today, Porter answered readers’ comments about their worst investing mistakes. He replied to “Bill,” who had said, “I’ve been trying to fix the mess I made of my life, but it’s very difficult with barely any funding,” with an offer of a complimentary Partner Pass membership and $100,000 in capital that can only be invested in new Distressed Investing recommendations. So the question is…

Coming Up This Week…

Wednesday’s PMI (purchasing managers’ index) data is expected to show a slowdown in services sector activity for the month of February due to uncertainty around Trump’s economic policies. And on Friday, the February jobs report is expected to show the addition of 185,000 new jobs, up from 143,000 in January.

In Case You Missed It…

On Monday in the Daily Journal, Porter explored Warren Buffett’s worst investment, which has destroyed capital – and his best one, which has returned 40% annually for 25 years.

In The Big Secret On Wall Street market update on Thursday, we explained how international opportunities are increasingly attractive compared to the U.S. stock market… and paid-up subscribers received an extensive portfolio update.

Also on Thursday, in an update for Porter & Co.’s Distressed Investing, senior analyst Marty Fridson explained that the Distress Ratio rose in February but is still well below its historical average. The upward trend will continue, Marty says: “It all adds up to a likelihood that distressed-debt investors will have a significantly wider array of bonds to choose from before very long.”

And on Friday in the Daily Journal… Porter made the case for distressed bonds – an asset class that is safer, more predictable, and less volatile than stocks. He called it the best-kept secret in the world of finance… As Porter wrote: “If you want to make the greatest investments of your life, I strongly suggest buying a subscription to Distressed Investing or joining us as a Partner Pass member… Go here to learn more and to make yourself part of this great opportunity to build immense wealth.”

And over the weekend, the Saturday Stock Screen explored opportunities across the pond, using the Modified Munger Screen as the filter… We shared for Partners a review of an Israel-based data provider that helps companies understand and optimize their digital footprints.

Finally, Sunday Investment Chronicles highlighted the best of what we read last week, including the data showing that investors have become unbelievably bearish on stocks.

Please, tell us what you think – good, bad, or indifferent: [email protected]

Porter Stansberry

Stevenson, MD

“Un-Surgery” and a $59 billion medical revolution

Presented by George Gilder

Have you heard of the new “Un-Surgery” treatments replacing many of today’s hospital operating rooms?They’re part of a booming $59 billion medical revolution sweeping the globe today…Giving doctors the ability to regenerate joints with just a few injections… or spines… or even heart muscles. And I’ve found one “under $5 stock” that’s in the thick of it all. Click here now to see the details.