Issue #24, Volume #2

How Braddock’s Secret Changed The World And Created $2 Trillion In Wealth

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

Editor’s note: If you’re interested, please respond today!… Porter is hosting a private dinner on Monday, March 3, at one of New York’s best and most exclusive restaurants in support of his longtime close friend, Whitney Tilson, who is running for mayor of New York City. Guests are asked to make a donation at this link to help support Tilson’s campaign to make New York City “safe and sane.” Porter, who keeps an apartment in New York, will be inviting a “who’s who” list of well-known NYC investors to the dinner. The location of the restaurant will come in response to the donation. Please RSVP before the end of business today, February 28, to join the group.

| How to beat the stock market, by a wide margin, using corporate bonds… Most people are going to lose money when they buy stocks… No one knows high-yield investing as well as Marty Fridson does… If you don’t want to get wealthy investing in bonds, tell me why in an email… |

I hope you’ll print this out.

This is, by far, the most valuable information we have ever published. This article will show you exactly how to beat the stock market, by a wide margin, by using corporate bonds.

Ironically, most people simply won’t buy bonds. Why not? Because there’s an entire industry that depends on you continuing to buy stocks. All the media you’ll ever see – all the advertising, all the books, all the movies, etc. – are always going to be about how you must buy stocks. No one will ever mention bonds. And after you read this, you’ll understand why.

Of course, we mostly sell research about buying stocks – so why did I write on Wednesday that most people shouldn’t buy stocks? And why am I now explaining the big secret about bonds to you?

I firmly believe my job is to give you the information I would most want if our roles were reversed. And, the truth is, as I told you on Wednesday: most people should not buy stocks.

Why?

Because most people (about 80%) are going to lose money when they invest in stocks. Even though the market seems like a fair game, it’s actually rigged to make sure that your emotions will betray you. Very few people (only about 20%) can overcome these hidden hurdles, but most people can’t. And they can’t learn to do so either. It’s hard wired.

Here’s a simple litmus test. If your average holding period across your investments is less than five years and if you make more than three or four investments each year (at most), the odds are overwhelmingly against you making money over time.

There’s virtually no chance that you’ll make money as an investor, even if you’re buying diversified ETFs or mutual funds.

Now, I don’t know you personally. I am not trying to insult you. But all studies of investor behavior show that the individuals who do the best, over time, are the investors who trade the least – and, thus, buy the fewest investments and hold them the longest.

The reason why is simply math: most stocks (about 53%) lose investors’ money over time.

So, even though the stock market is a winning game (on average, the value of all corporate equity increases by about 8% each year), there is no Mr. On Average. And the more stocks you buy, the worse your odds of winning become.

Though, on average, the market goes up, all of the value created by corporations ends up in the hands of about 20% of all investors. Most investors (roughly 80%) lose.

This phenomenon is called the Pareto Effect, and it’s found across all kinds of organic systems. It is a law of nature.

As any long-time subscriber will tell you, I am completely incapable of self-censorship. I call ’em as I see ‘em, whatever the consequences.

And I know, by telling you these hard truths, I am offending most of you. In fact, I am almost certainly costing my own company a lot of money. Hundreds – maybe thousands – of people will cancel their subscriptions simply because of this article. That’s no exaggeration.

In fact, a subscriber (David, from Texas) wrote to me on Thursday, saying this is exactly how he felt when I first explained these concepts back in 2015:

I remember you making this statement years ago, when I decided that I would meet your challenge and be the ONE person to prove you WRONG. Guess what. I was WRONG and you were RIGHT. To be honest when I first read YOUR statement, I thought you were kind of arrogant for even saying such a thing. But YOU won and proved me and my ego wrong. I believe that in all of us, we have such an ego that we believe we can beat the system or the market. WRONG. I am DONE with all this nonsense. I just should have taken your advice years ago. But I did not. So as the song goes, “Another one bites the dust.””

If it helps, my wife, who was trained as an engineer and has a completely analytical mindset about everything in life (except for me), is a much better investor than I am. Why? She is endlessly patient. And she doesn’t want to risk even a penny of capital unless she’s 100% sure she can’t lose money in an investment. I’m always too eager to move on to the next good idea.

But… there’s a solution!

There are investments that you can make where the duration of the investment is fixed – and usually last four to seven years. If you sell, you’ll lose a lot of money, so you have a huge incentive to be patient.

Plus, in these investments, you’re legally guaranteed a fixed rate of return!

And, finally, the part that’s very hard to believe… you can use these assets to absolutely crush the stock market. No kidding.

I’m about to give you the single greatest wealth-building secret that’s ever been discovered.

It is a foolproof way to do what finance professors say can’t be done: routinely beat the market’s return with dramatically less risk.

And really, I mean no risk, none, no risk at all.

Legally, of course, I can’t say those words. Life is risk. But, as I know you’ll understand after reading this, you’ll see exactly why I believe this is a truly risk-free way to become extremely – no, I mean insanely – wealthy.

This approach only requires two things that, unfortunately, most people don’t have in great abundance: patience and brains.

Luckily, with our help, you can learn to be patient. And with Marty Fridson (our in-house expert) you have the best brains of all time regarding these assets. You’ve got no excuses (of course, that won’t prevent you from making them!)

But seriously, please print this out. Pour yourself an adult beverage (or whatever you like to imbibe to relax). Grab a pen. You’re about to become a very, very wealthy person.

I’m going to give you all of this – and every resource you need – for free.

I’m doing so because I hope you’ll immediately see how incredibly powerful this approach is, and I hope you’ll decide to follow it with at least most of your wealth.

And, if you do, then there’s no reason why you wouldn’t want Marty Fridson’s help. Our research product about these opportunities (Distressed) is a ridiculous bargain.

But, I’m asking for one thing in return for today’s information (which, as you know, is free!): If you decide not to follow this approach and you decide not to purchase a subscription to Marty’s work, then I’m asking you sincerely to please tell me why in an email.

You might have a very good reason, like not enough capital to invest in these markets. Or, who knows, maybe you know more than the world’s most acclaimed investor in this space.

Whatever the reason, no hard feelings. I’m asking you to actually write down the reason though, because often that’s the only way to get people to see what a terrible mistake they’re making. When you write your reason, you’re gonna think to yourself, well damn, that’s just stupid.

And maybe, just maybe, you’ll change your mind.

If you do, today will mark the best financial decision of your entire life. There is simply no better, no easier, or more foolproof way to become insanely wealthy.

Like I love to say: horse, meet water.

The World’s Only True Investment Secret

First, a bit of logic.

If there really was a foolproof path to market-beating investment returns without any risk then don’t you think someone would have already put this to use?

The market can’t be this inefficient, can it?

Yes, it can. And, as you’ll see, there is a simple structural reason for why this opportunity exists and has persisted for a long, long time.

But I don’t expect you to take my word for it.

This secret was discovered in the 1950s by Braddock Hickman, who published his findings in a landmark report, Corporate Bond Quality And Investor Experience.

Feel free to read the entire report, but I can summarize it very quickly for you.

Hickman found that from 1900-1943 (which was a full investment cycle, including the Great Depression), high-yield corporate bonds produced returns that were only slightly less than stocks, but were about half as risky. Thus, investors in bonds enjoyed a vastly superior expected return at initial purchase.

That, by itself, was a remarkable discovery.

But there was more.

Hickman also discovered that, during points of stress in the credit markets, it was actually lower-rated bonds (what today we could call “junk bonds” or non-investment-grade bonds) that performed the best. In fact, purchased during periods of distress, these high-yield bonds actually performed much, much better than stocks, with vastly less volatility.

And, yes, many people have put these ideas to work and made vast fortunes with them, most notably Michael Milken in the 1980s. Later Milken would be unjustly vilified by Rudy Giuliani, but Milken’s wealth wasn’t created by fraud or graft. He was simply the first investor to ever allocate huge amounts of capital into high-yield corporate bonds. And the amount of wealth he created was astronomical. More recently, Howard Marks (Oaktree Capital Management) has become a billionaire through the same strategy.

Today, the market for high-yield corporate bonds is over $2 trillion. And there continue to be periods where high-yield corporate bonds vastly outperform stocks – with much less volatility. (If you want to read a good primer on how high-yield bonds work and how they compare to stocks, Pimco has a good free white paper here:

When Bonds Vastly Outperform Stocks

The best time to buy junk bonds is in the midst of an economic crisis.

It’s during these times that default rates increase, investors become nervous, and – most importantly – investment-grade bonds get downgraded.

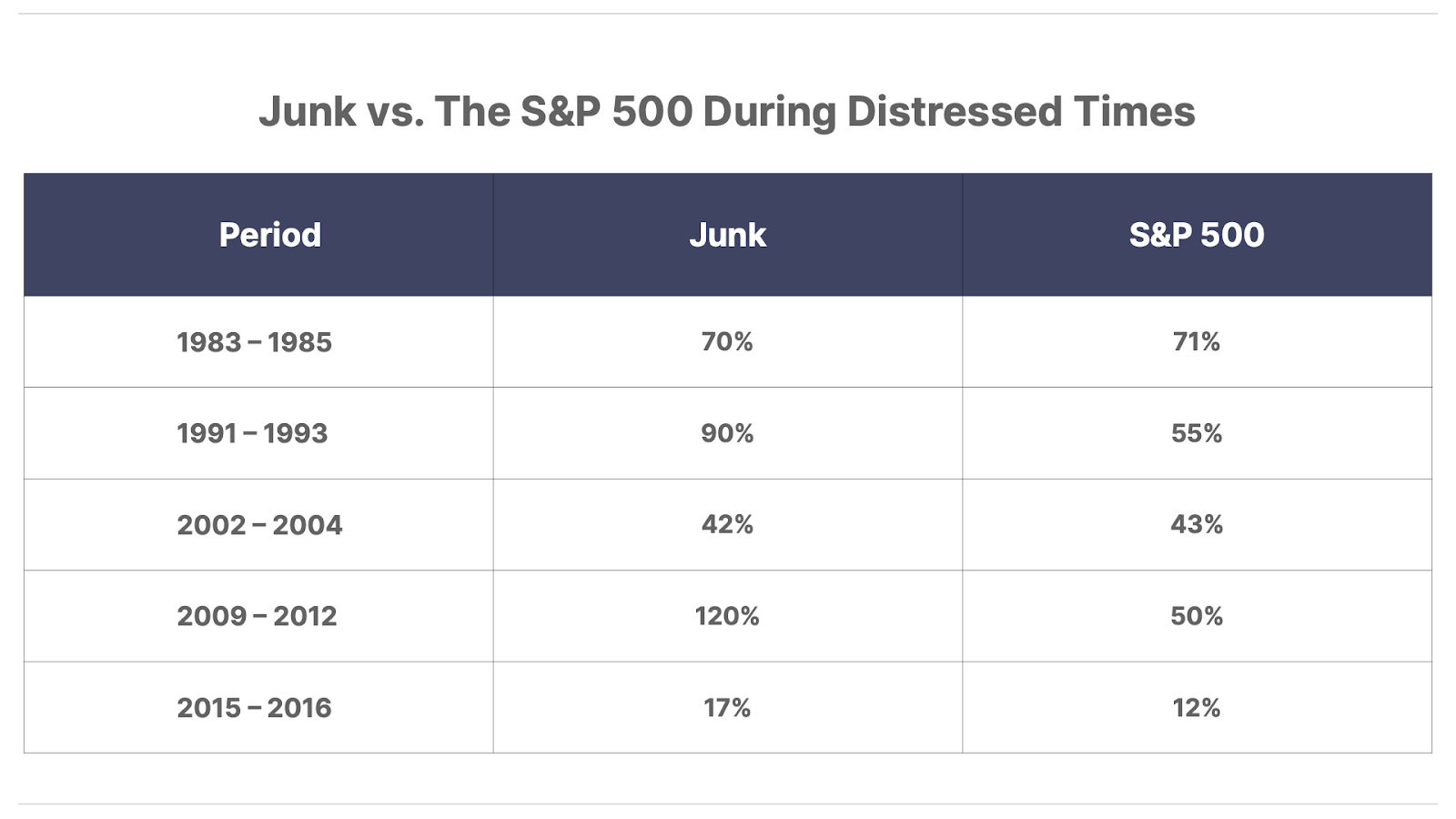

From 2009-2012 – the period coming out of the Global Financial Crisis – junk bonds returned 120% compared to 50% for stocks, based on index results.

Junk-bond investors saw returns that were at least 140% higher than stocks, with about half of the risk: the junk bond ETFs (JNK, HYG) saw monthly volatility about half that of stocks (beta: 0.6).

And this extreme example isn’t the only one.

In fact, if you study every period of economic distress going back all the way back to 1900, you’ll find that junk bonds beat stocks every time – with higher total returns and less volatility.

I’ve got good data going back to 1980:

But wait, you’re probably thinking. These results don’t look like bonds killed stocks. Sure, maybe bonds are less volatile, but even in these optimal periods, stocks still outperformed a little in 1983-1985 and in 2002-2004.

No, they didn’t. Not really.

The indexes that we use to track bond performance (like Bloomberg’s) track changes to the market value of the bonds and assume investors reinvest the coupons back into the bonds, much like total-return stock indexes assume dividends are reinvested.

But tracking returns this way dramatically underestimates actual investor returns, when the bonds are bought at a large discount. To understand what’s really happening, you need to know how bonds work.

(For folks experienced with bonds, please pardon this basic explanation. I know that a lot of my readers have never bought a bond before.)

Bonds are a contractual obligation: they are a way for corporations to borrow money through a contract.

There are typically two parts to the contract.

First, companies must pay interest (typically twice a year) to the contract holder. These payments are known as coupons. And, second, the contract must be redeemed at the full face value, after a fixed amount of time.

A typical corporate bond has a face value of $1,000 and today coupons are usually between 8% and 12% annually.

Bonds are quoted using the date of their maturity and their coupon rate. So you might discuss with your broker “the IBM 6s of May 2030.” That means IBM owes the holder of that bond two payments each year of $30 (for a 6% coupon rate) and IBM must redeem that bond for $1,000 in May 2030.

But, during periods of economic distress, the market price of bonds – normally $1,000 – can fall dramatically.

If investors begin to fear that IBM won’t be able to redeem the bond or make the required coupon payments, the market price of the bond can fall – to any level.

But, no matter how far the bond price falls, its face value doesn’t change, nor do the coupon payments change, and the company’s legal obligation to redeem the bond at full face value doesn’t change either. Thus, during periods of economic stress, it’s possible to buy bonds with a market price that’s far below face value – say $500 instead of $1,000. And the lower cost means that the coupons are worth a lot more, as an ongoing yield. In this case, if that IBM bond’s market price was 50% below face value, then its yield would be 12% to the new buyer, not the initial coupon rate of 6%.

And, as you can see, as long as IBM makes these payments and redeems the bond (as it is legally required to do) an investor buying at half of face value is going to make an incredible return. There will be a 100% capital gain as the bond is paid off at face value in 2030, plus five years of 12% yield.

These kinds of opportunities emerge most often when a bond is downgraded from “investment grade” to “non-investment grade.”

Why Bonds Vastly Outperform Stocks

Remember when I said there was a structural explanation for these opportunities?

The credit rating system (and the way the regulators use it) creates a huge structural problem for the credit markets.

There’s a Grand Canyon of difference to financial institutions (and their regulators) between investment grade and non-investment grade. Thus, most big financial firms simply aren’t allowed to own non-investment grade debt. And, as a result, the market for non-investment grade debt isn’t as efficient. There can be huge mispricing in this market, especially during periods of economic stress, when default rates rise.

In fact, the entire non-investment grade debt market can become destabilized when large corporate bond issuers are downgraded to “junk” because there simply will not be enough buyers for these bonds. And, as these so-called “fallen angels” find buyers at much higher yields, junk-bond investors will sell previously issued junk bonds and “upgrade” their portfolios into the newly available fallen angels.

It’s during these periods where outrageous returns can be earned.

And the reason is simple to understand: the difference between the lowest tier of investment-grade debt and the highest tier of non-investment grade debt is almost entirely fiction, as Hickman first proved in his seminal paper. There just isn’t a big enough difference in actual default rates to justify the large premium in yields that are available in junk bonds.

But, rules are rules. And it’s the regulators’ rules that cause the big dislocations in the bond market. These rules aren’t going to change – in fact, they’ve gotten worse since the 2008-2009 crisis. And that’s why this market anomaly has persisted for decades.

Okay, but what does this have to do with the example above, about how stocks seemed to perform as well as bonds in some of those periods?

Those returns are the index returns – the gains to the market price of the bonds, plus reinvesting the coupons. But the indexes can’t measure the impact of vastly higher-than-market yields that actual investors will gain when they buy these bonds at a big discount to face value.

In other words, the actual returns are far better than the indexes suggest.

For example, let’s assume you bought an average non-investment grade bond during the market turmoil in 2009, with a four-year duration. (Most corporate bonds mature in seven years, so a four-year duration is very typical.) And let’s say you held until maturity in 2013.

Your returns as an actual investor would be far higher than the indexes, because you get the coupons at a huge discount to face value. Your total returns would have been 140%, with most of the return coming from your much higher than market coupon yield (19% annualized, 16% cash yield). That compares to 110% for the four-year return in stocks (16% annualized). Meanwhile, the junk index only captures the coupons being reinvested into the increasing face value of the bond, 90% (14% annualized).

Okay, so there’s a lot of complicated math there, but it’s not hard to understand that if you’re buying the right to $1,000 for less than $750 and you’re going to receive 16% a year in cash yield, it’s going to be very difficult for the stock market to beat your returns. The cash yield alone will beat the stock market.

Plus, these are legally binding contracts: the company must pay. Especially during periods of turmoil, when buying stocks is extremely difficult emotionally because of the huge price swings, having the certainty of a bond is a real-world advantage.

Alright… so… there’s just one problem. How do you know when it’s the right time to buy junk bonds?

When To Buy Bonds

Well, that’s the easiest part of all.

The way to judge the relative value of junk bonds is by comparing their current yields against the current yields of similar duration U.S. Treasury bonds (which are considered risk-free.)

By comparing the two yields, you can see what the “risk premium” is currently in junk bonds.

You want to buy when there’s at least a 750 basis point risk premium in junk bonds.

That means, you want to receive an extra 7.5% a year over U.S. Treasury yields.

Today, if you were going to buy a junk bond, you’d want to get at least an 11.5% yield. That’s based on five-year U.S. Treasury bonds, which are currently yielding around 4%.

There are, of course, lots of “nits” around this general advice. You might accept a lower yield if the company’s assets were of a particularly high quality (lower risk in the event of a default) or you might demand a lot more yield if you believe the default risk is higher than the market believes.

These kinds of opportunities exist all of the time, but, like the rest of the markets, they wax and wane. So how can you follow this market easily? That’s simple. Bank of America maintains a very handy index that looks across many different durations and produces a composite view of the entire high-yield-bond market, compared to U.S. Treasuries. It’s called the U.S. High Yield Option-Adjusted Spread Index.

If you select “Max” on that chart’s duration, you’ll see there are huge swings in the average spread between high-yield bonds and U.S. Treasuries. So, one way to approach this market is to simply try to lock in great long-term yields when, as seems to happen once every seven to eight years, the corporate bond market hits a speed bump and investors have the opportunity to lock in yields that are 8% to 15% above U.S. Treasury bonds.

Over the last 20 years or so, those kinds of opportunities have emerged in 2001-2002, 2008-2009, 2012, 2015, and 2020.

My dear paid-up subscribers love to bitch about how there’s nothing in high yield to buy right now. Always makes me chuckle. Look at those dates. The biggest gap between these opportunities is about seven years. And these bonds have seven-year durations!

If you’re wise, you’ll just buy these bonds the next time an opportunity emerges. Enjoy making 15% to 20% a year – without any risk.

And, just wait… as your bonds mature… another big opportunity will come along.

Remember: the market can’t make us do anything. We just have to be willing to provide capital when the market is willing to meet our demands. And, like manna from heaven, it rains often enough to keep us fat and happy.

The last such golden opportunity in bonds was in 2020 – and it was legendary. That was five years ago. And the largest gap between these opportunities is seven years.

What’s that tell you will happen soon?

Why You Should Only Buy Bonds – And Only Marty’s Bonds

Get ready, my friends. Your life is about to change – forever.

I’ve long known about how powerful the high-yield market is. But sharing it with my subscribers isn’t easy – at all! Corporate bonds are a “professionals” market. It’s like a closed club.

Nobody else is going to explain how it works or help you invest in it.

Why? Because if you had a golden goose, would you tell the world about it?

If you try to do this investing on your own, you’re going to find it’s very difficult. You’ll have to read 700-page bond debentures – and really, you’ll need a lawyer to help you understand them. And, I have to warn you, if you don’t know what you’re doing, you’re going to royally screw up. There are often dozens of bonds for a single business and you have to buy the right one! This isn’t something you can realistically do on your own, unless you have many years of experience as a bond analyst or a securities attorney.

So to help us navigate these markets and master them, I recruited Martin Fridson.

You can Google him to learn more about his incredible career. Here’s the short version: he invented high-yield bond research on Wall Street.

He started his career at Wall Street’s most legendary bond firm, Salomon Brothers. He then built the best team on the Street at Morgan Stanley and Merrill Lynch. His 40+ year career on Wall Street is unmatched for accomplishment: there’s simply never been a better professional investor in these markets than Marty. No one else even comes close. He was named Institutional Investor’s top high-yield analyst nine times. (They basically retired the award with Marty.)

I’m sure that every financial newsletter publisher says the same thing about their analysts. But they don’t have anyone on their entire staff who compares to Marty. If you ask anyone who worked in fixed income on Wall Street between 1980 and 2010, they will all say the same thing: Martin is a living legend.

We launched Porter & Co’s Distressed Investing with Martin Fridson in the spring of 2023.

As you can tell from the Bank of America risk spread chart (aka the U.S. High Yield Option-Adjusted Spread Index), our timing was far from perfect. There were not many high-quality opportunities at that point in the cycle. No matter. Marty got to work.

Since we launched, he’s recommended 17 bonds. He’s made money more than 80% of the time. And his annualized return – in bonds alone – beats stocks: 13.6%.

But, we recognized it wasn’t a great time to recommend only bonds, so Marty has also been recommending a small number of stocks, investments he found out of studying corporate balance sheets. This unique approach led to his recommendation of Peloton, for example, a stock that’s now in our Top Positions list, in fourth place, with close to a 140% return.

Marty first recommended the company’s bonds when a new management team cut overhead. Marty was sure that the resulting increase to cash flows would more than cover the debts, making the bonds “money good.” Then, as cash flows kept increasing, Marty realized the market was badly mis-pricing the stock too. He’s a legend.

And, when we started Distressed Investing, I suggested starting with two stocks (Salesforce (CRM), which was in distress at the time) and Houlihan Lokey (HLI) (which is a restructuring firm that deals with distressed companies) as investments. When you put everything together, the results have been extraordinary. A nearly 80% win rate and total returns of 35.8% (26% annualized).

These numbers are mind-boggling. I do not believe it is possible to achieve better results – or even close to these results – in any other investment fund or investment newsletter that’s focused on low-risk investments.

I am very proud of what Marty has accomplished for our subscribers so far.

But these returns are nothing compared to what Marty will be able to do for us when the credit cycle turns and defaults start rising. That’s when the very best opportunities will emerge and when Marty’s skills will shine brightest.

In his latest issue (published yesterday), Marty wrote that cold winds are starting to blow in the corporate credit markets and we may soon see opportunities to lock in 15% to 20% yields – plus capital gains.

It’s time to change your life. You can become not just a good investor, but a great investor.

Marty will teach you everything you need to know about how to buy bonds (his intro guide is the best ever published, anywhere). And, with every single recommendation, he will walk you through exactly how to buy the bond he’s recommending, even down to exactly what to tell your broker, if you can’t buy the bond directly online.

There are three reasons why this is best investment decision you’ll ever make:

#1. This is the only truly proven way to beat the market, by a wide margin, using an entire asset class that has far less volatility than socks.

#2. These investments provide you with very high levels of income and are legally guaranteed, which greatly reduces the risk of capital loss.

#3. These investments have long durations (typically three to four years), which will help you to remain invested long enough to produce substantial returns.

And, Marty Fridson is the best research analyst in the entire history of this market. His track record is unmatched.

If you want to make the greatest investments of your life, I strongly suggest buying a subscription to Distressed Investing or joining us as a Partner Pass member…

Why Bonds Are At The Center Of My “Second Life”

There’s a lot more I have to share about investing in corporate bonds. But it’s very personal and you might not be interested.

You may have heard that I lost my wealth when my first company, MarketWise, collapsed. And that’s true. As the share price of MarketWise fell from $17 to $0.40, I was wiped out. I’d borrowed a lot of money to finance a divorce. And suddenly, after our IPO, years of deferred taxes came due. I lost almost everything. And, in the aftermath of those losses, a cardiac event nearly killed me in June of 2022.

As I slowly recovered my health in the summer of 2022, I made the decision to have a second life.

I don’t know if you’ve ever been through a moment like this in your life, but I didn’t just want everything back that I’d lost… I wanted to rebuild everything in a way that I couldn’t ever lose it again. I wanted to build a better business, where I’d always maintain firm control. I wanted a better marriage with someone I knew truly loves me, and I wanted to build a second fortune, using an approach where volatility would never again cause me to lose millions in assets.

And so, I’ve decided to make this kind of investing – in distressed corporate debt – the center of a new hedge fund I’m launching. I plan to make this approach the foundation of my wealth.

I’ve recently finished a new documentary about my Second Life. I hope you’ll watch it. And I hope it inspires you to make the most of this opportunity with Marty.

And, like I said earlier, if you’re not going to invest with Marty, then I want you to tell me why. Send me an email. Explain it to me… [email protected].

The only valid answer: “because I can make 26% a year in bonds all by myself.”

If that’s not true, then you’re choosing to be poor.

Just click here to watch My “Second Life”

SPONSORED BY ONEBLADE: A $10 Million Shave?

Ten years ago, a single shave cost Porter $10 million…

It all started in Rimini, a remote Italian village on the Adriatic coast. In a dusty, old barbershop that could’ve been a front for the mafia, Porter experienced what he calls the perfect shave. Ever since that shave, Porter became obsessed with getting the same shave at home. Ten years and $10 million later, he created OneBlade – the world’s finest safety razor. A razor that redefines shaving perfection. Today, you can try the OneBlade Genesis, use STANS15 for 15% off, exclusive for Porter & Co. readers.

Three Things To Know Before We Go…

1. No surprises in today’s inflation report. This morning, the Bureau of Labor Statistics reported the personal consumption expenditures (“PCE”) price index – the Federal Reserve’s preferred measure of consumer inflation – rose 0.3% in January (2.5% annualized), in line with analyst estimates. Core PCE – which excludes food and energy prices – also came in as expected, rising 0.3% (2.6% annualized). While the latter represents the lowest annual inflation rate since March 2021, it’s also worth noting that both headline and core PCE remain well above the Fed’s official 2% target… and recent data suggest inflation could begin to move higher in the months ahead.

2. Cash levels at U.S. mutual funds hit a record low 1.3% of total assets. While cash levels plummet, the latest (as of February 26) AAII Bearish sentiment survey shows that 61% of retail investors are bearish on the stock market over the next six months – up sharply from 41% just a week prior. When fund managers are nearly fully invested, the risk of forced liquidation – if fund shareholders sell – rises sharply, adding downside pressure to stocks. Meanwhile, Warren Buffett’s Berkshire Hathaway (BRK) is holding a record level of cash.

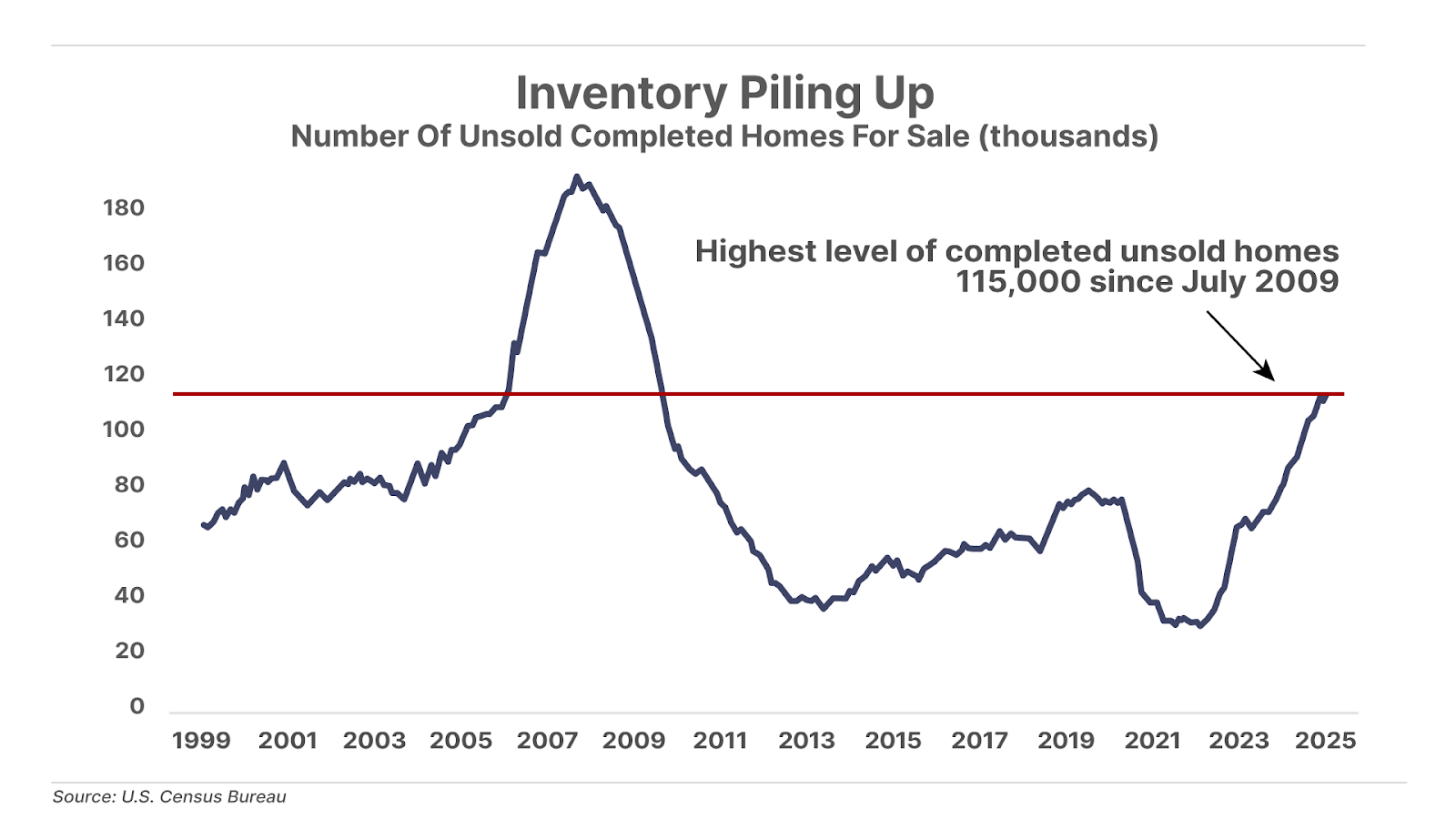

3. America’s housing market grinds to a halt. Record-high home prices and elevated mortgage rates continue weighing on U.S. home sales. The National Association of Realtors Pending Home Sales Index (a measure of expected home sales based on already-signed sales contracts) fell by 5.2% year-on-year in January to 70.6, reaching the lowest level on record going back to 2001. That means that as buyers are balking at today’s high prices and financing costs, inventories of unsold homes are piling up at an alarming rate. Unsold housing inventory increased by 17% in January to reach 115,000, the highest level since July 2009. Bloated inventories and sluggish sales will likely continue pressuring the shares of U.S. home builders… and doesn’t bode well for the economy broadly, either.

Good investing,

Porter Stansberry

Stevenson, MD

P.S. George Gilder has had an enormous impact on my life.

When I was in my early 20s and first learning the tools of investment analysis, George’s work helped shape my understanding of supply-side economics… the inherent morality of capitalism… and the dangers of collectivism.

He also helped lay many of the foundations for my first newsletter, as it was his research that opened my eyes to the inevitable dominance of the internet.

And over time, I came to fully appreciate how extraordinarily visionary George truly is. He’s predicted everything from the rise of the microchip to personal computers, iPhones, Netflix, cryptocurrencies, and more – often years before anyone else.

It’s difficult to describe the thrill when I was able to meet George Gilder for the first time… and when he came to my farm to speak at our Porter & Co. conferences.

I can count on one hand the number of analysts whose work I read all the time. And George is at the top of the list.

So when he recently released a presentation about a $59 billion medical revolution… I couldn’t wait to watch it.

I learned a lot. And I think you will too. You can watch it here.