Issue #89, Volume #2

Take Care Of The Basics First

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| You deserve our best… Some companies are better at compounding capital… Find one high-quality company to buy and hold forever… Take care of the basics first… Tech companies driving all the earnings… For now… |

With Porter out this week, we’re sharing parts of an investment classic that Porter wrote more than a decade ago, at Stansberry Research. For years, readers cherished Porter’s musings in the Friday edition of the Stansberry Digest… and this was one of his best.

Here’s Porter in 2014…

For my entire career, I (Porter) have been working hard to give individual investors the strategies, information, and insight they need to compete with the pros on Wall Street.

And, today, I’m going to give you the one, big secret. It’s the only real, true secret of finance. And once you understand it, you won’t need us (or anyone else) ever again.

As longtime readers must be tired of hearing me say… I write the Friday Digest personally because I feel a huge responsibility to tell you what I would want to know if our roles were reversed. You’ve paid us to help you make decisions about investing your hard-earned savings. We aren’t fiduciaries. We don’t offer any personalized investment advice, nor do we manage anyone’s money. But this doesn’t absolve us of responsibility to you. You deserve our best. I’ve always tried my best to live up to that obligation.

So what’s the most important idea I’ve discovered in finance? What’s the one thing I’m going to teach my kids beyond the obvious stuff about saving, compounding, and risk management? What do I believe is the real secret to investment success? And… the biggest question of all… How do I invest my own money in securities?

Over the long sweep of your investing lifetime, strategies that only work extremely well in certain market situations are unlikely to play a dominant role. The big secret therefore is something you can use all of the time, for your entire life, as an investor. And here it is: Some companies are much better than others at compounding capital. Much better.

If your goal as an investor is to compound your savings over time, wouldn’t it be easier to simply figure out which companies will compound your capital at an acceptable rate, buy those firms (and only those firms) at reasonable prices, and then do something else with the rest of your time?

Here’s a simple, but powerful example. Well-run insurance companies can produce what’s called an “underwriting profit.” They are paid money in advance to manage your capital. And they get to keep not only the investment profits, but profits from the premiums, too. That’s like paying the bank to keep and use your money. No other business can compound capital so consistently.

Insurance companies have other fantastic advantages, too. They’re able to legally defer most of their taxes. They’re nearly immune from economic factors. They’re scalable. I could go on. They’re a focus for us because well-run insurance companies are legendary compounders of capital. Buy them at a reasonable price, and it’s impossible not to do well.

It’s not an accident that the greatest investor in history, Warren Buffett, has long focused on insurance stocks and other companies that are highly capital efficient. That is, companies that are natural wealth-compounders. Starting with his 1972 investment in See’s Candies, Buffett gradually over the years shifted the bulk of his wealth into a simple, long-term compounding strategy…

While Buffett didn’t abandon all other forms of investing, his largest allocations since 1972 have all used this compounding strategy. That famously includes his 1988 purchase of Coca-Cola (KO)… when Buffett put roughly 25% of Berkshire’s capital into a single stock! And it wasn’t a cheap stock, either. At the time, Coke was trading for 16x its annual earnings. Buffett had figured out the one, real secret of finance… the one secret to “rule them all.”

To use a long-term, compounding strategy effectively, you really only have to answer three questions.

- Is the company in question able to produce very high returns on its assets – in other words, is it a great business?

- Are these unusually high returns very likely to continue for decades, without requiring large and ongoing capital investments?

- Can the management of the company be trusted?

If the answer to these questions is “yes,” then all you have to do is simply not pay too much when you buy the stock.

Implicit in this is that these companies have a moat – because if they didn’t, competitors eager to beat them on price would enter the market, thereby killing margins.

Most of the companies that fit these criteria are branded consumer-products companies – stocks like McDonald’s (MCD), Coke (KO), Heinz (KHC), and The Hershey Company (HSY). Buffett explained in his 1983 shareholder letter how he thinks about these companies. The secret to their long-term earnings power is very simple: It’s their brand and the relatively unchanging nature of their products. These companies’ products are so well-known (and adored) by customers that these firms can constantly raise prices to keep pace with inflation.

Meanwhile, the brands – while requiring some advertising – aren’t like factories, gold mines, or drugs. They don’t require massive investments of new capital. There’s no new gold mine to find and build. There’s no patent that’s going to expire. And there’s not even any new product that must be created: Coke’s fans went crazy with anger when the company tried to change its product in a small way back in 1985.

All these firms have to do is continue to deliver the same thing, year after year. And that means they can afford to return huge amounts of capital to shareholders. Merely buying and holding any of the stocks I mentioned above would have made you 15% a year annually if you’d just reinvested the dividends for the last 30 years. Even if all you did was invest $10,000 and then nothing else – not a penny more – you’d still end up with $575,000 at the end of 30 years. If you invested $10,000 annually, you’d end up with $4.3 million.

And the best part? Anyone can use this approach. The math is simple. And is it really that hard to realize that Heinz is the best sauce company… that Coke is the leading soft-drink business… or that McDonald’s makes the best hamburgers?

The No. 1 objection I get from readers when I talk about this strategy is: “That’s great, Porter. Wish I’d known about that when I was 25. But it’s too late for me now. I don’t have 30 years.”

That’s nonsense. Think about it this way… Buffett was born in 1930. He didn’t buy Coke until 1987. He was 57 years old. It has been one of the greatest investments of his life – bar none.

If that doesn’t convince you, just think about it this way. How often do you make more than 15% on your portfolio in a year? Whether you’ve got three decades to invest or only one, you should aim to produce the highest possible annual return without putting your capital at undue risk. There’s not a safer investment approach than this one, as your returns are being manufactured by great businesses. You don’t need a “greater fool” to pay too much for your shares to make a profit. In fact… The biggest risk you face is selling at all because that will trigger taxes (in most accounts).

These companies all produce something akin to financial antigravity: They earn more and more money, year after year. But most investors will never see it. It’s this seemingly invisible power that allows them to return massive amounts of capital to shareholders, a factor that sets them apart and greatly reduces investor reliance on capital gains. This is incredibly important over the long term.

Follow insurance stocks, for example… or consumer-products companies. Follow industries that have small capital requirements.

That’s the big secret… the one I will work hard to teach my children… and the secret that guides my personal investing. Each year, I try to find one high-quality, supremely capital efficient company to buy and hold forever. I can diversify this portfolio over time, adding only one stock each year. This will allow me to manage risk without having to sacrifice quality.

I believe this is the safest way to earn 15% or more on my portfolio, year after year. If you will adopt this strategy for at least a portion of your savings, it is overwhelmingly likely that you will succeed, too – assuming you refuse to pay too much for the stocks you buy.

I value the stocks I own the same way I value my own company – by the amount of cash it generates for its owners every year. I couldn’t care less about the market price, as long as I know that the company continues to gush cash from operations and as long as I can trust the managers. With that out of the way – with all of my fear removed – I can concentrate on capitalizing on the opportunities created by the market’s volatility.

Most investors will never have this advantage. And therefore… they will never be able to use the other profitable tools we also write about.

The lesson is simple: Take care of the basics first. Make sure your money is compounding at an acceptable rate. Once that’s covered, you’ll be in position to invest very successfully using other tactics.

Want to get access to monthly Big Secret On Wall Street recommendations? If you pay for just one year of The Big Secret… to celebrate our third anniversary, Porter is offering to cover the cost of your membership every single year after that… But you need to qualify. Click here to find out if you do.

Letting A Pro Invest Your Money

Presented by Stansberry Asset Management

Porter recently discussed this very concept with Stansberry Asset Management (“SAM”) Chief Investment Officer Austin Root.

SAM is an SEC-registered investment advisory firm with more than $1.1 billion in assets under management. SAM is separate and distinct from Porter & Co., and helps families and individuals across the country invest their wealth and achieve their long-term financial goals.

Austin has an investment pedigree grounded in real-world experience and a track record of delivering results. He ran a successful hedge fund with a strategic backing from Julian Roberston and Tiger Management… He was a portfolio manager for billionaire investor Steve Cohen… He was an investment banker for Blackstone… He has an MBA from Stanford… And before becoming CIO at SAM, he was the director of research for the former company I founded, Stansberry Research.

Porter has often said that if you have $1 million or more in investable assets, having a professional asset manager is a huge advantage. And that’s especially true if that asset manager has the skills and experience of the investment team at SAM.

Three Things To Know Before We Go…

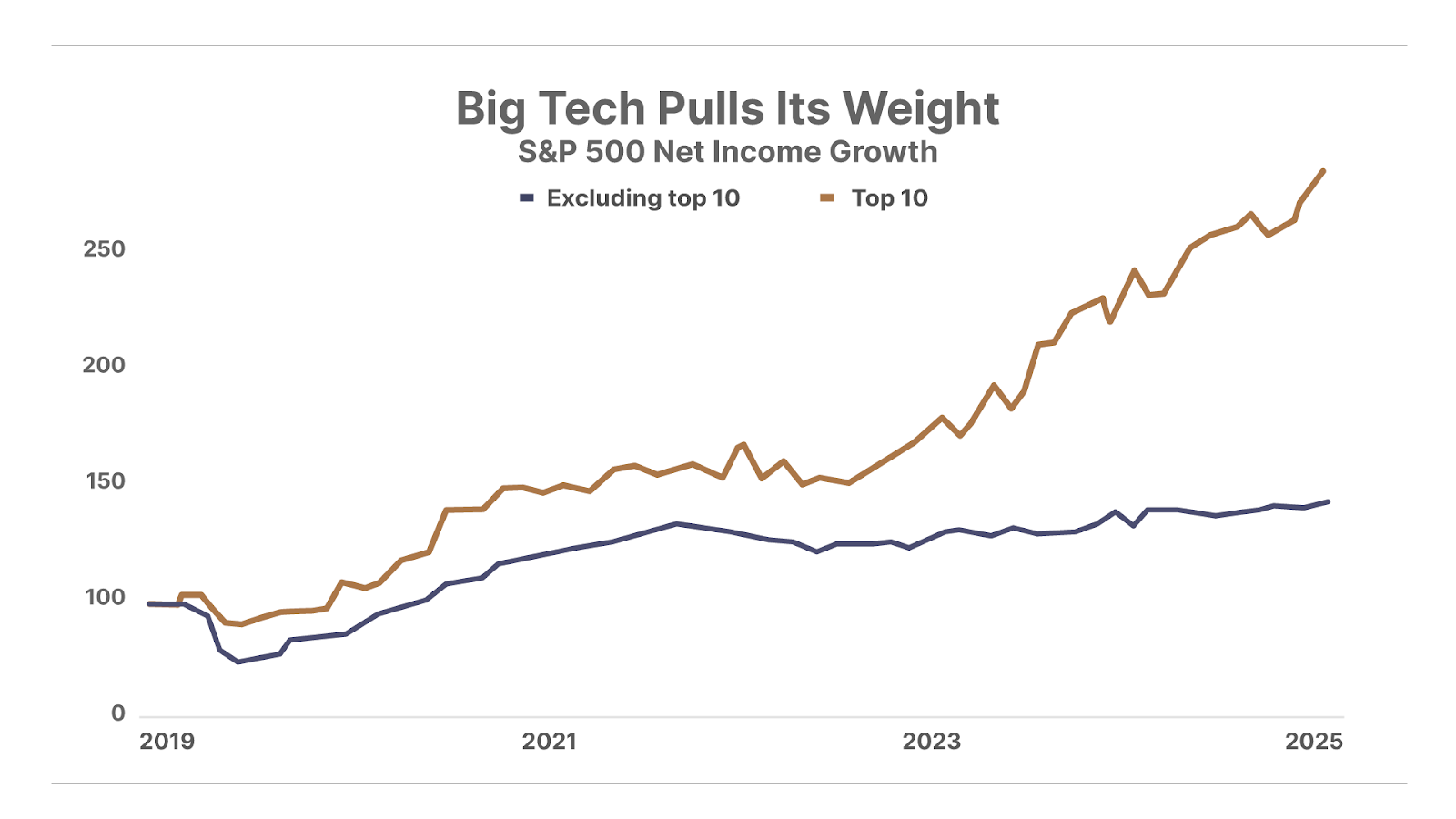

1. Big tech outperforms the rest of the market. Virtually all of the earnings growth in the S&P 500 since 2022 has come from the index’s top 10 largest companies. Meanwhile, the bottom 490 companies have collectively generated flat earnings over the same period. The market is increasingly dominated by a handful of tech companies benefitting from the artificial intelligence (“AI”) boom. But there’s just one problem…

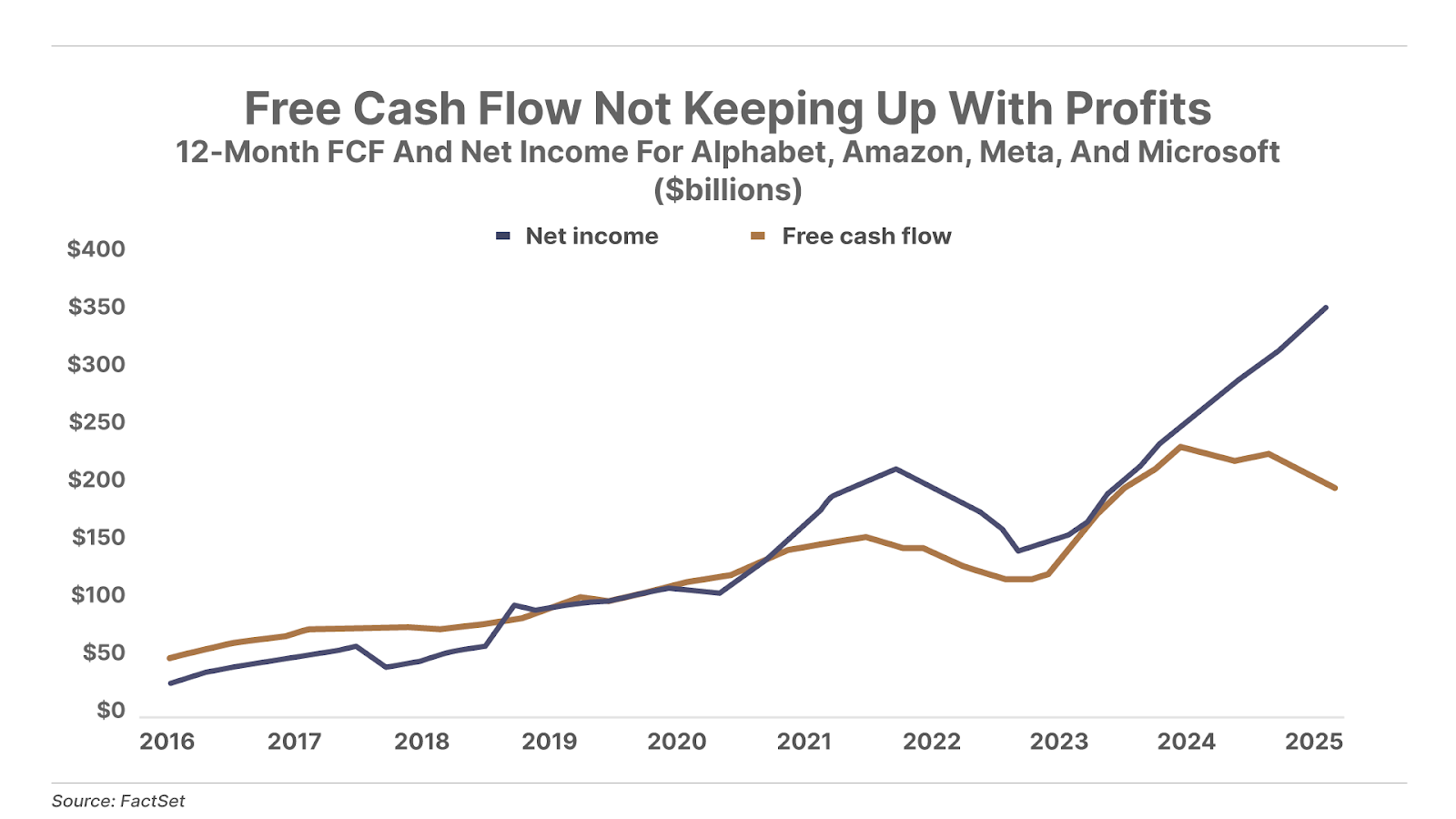

2. Big tech cash flows are falling short. Up until the AI boom kicked off with the launch of ChatGPT in late 2022, big tech’s free cash flow generally tracked their earnings growth. But since 2023, these companies have been sinking earnings into capex for data centers and other AI infrastructure. As a result, free cash flows are falling even as reported earnings are rising. This sets up a key risk for tech stocks and the overall market if the AI capex boom doesn’t eventually lead to free cash flow growth.

3. Trump fires BLS exec following weak jobs report. On Friday afternoon, President Donald Trump fired Bureau of Labor Statistics (“BLS”) commissioner Erika McEntarfer – a Biden appointee – following a weaker-than-expected jobs report and massive downward revisions of May and June data. While monthly revisions are common due to how employment data is collected – the BLS operates under the Department of Labor, which is led by a Trump appointee – the president accused the commissioner of “rigging” the report. In a Truth Social post, Trump said the “big adjustments were made to cover up, and level out, the FAKE numbers that were CONCOCTED in order to make a great Republican Success look less stellar,” and said his administration would pick an “exceptional replacement.”

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland