Issue #134, Volume #2

Target’s Earnings Continue To Decline; A Bankruptcy Filing By 2030-2031 Is Likely

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| My next big short… Target is the new Kmart… This is not a temporary dip… Target’s brand and business model are now permanently impaired… What happens next… A warning on the economy… Nvidia reports earnings tonight… |

On September 25, on X, I published a “short” thesis on one of America’s most popular retailers, Target Corporation (TGT).

I shared my view that Target has begun a terminal decline, much like I saw at Sears and J.C. Penney years ago. It has lost its core customer – affluent suburban “soccer moms.” The quality of Target’s merchandising and its staff has collapsed. You can see the result in its parking lots. They’ve become scary places around big cities.

Target is collapsing financially as a result: lower store traffic, lower same store sales, collapsing operating margins, all leading to far weaker free cash flows.

Target’s management has responded, so far, by cutting its capital expenditures (“capex”) – it’s building far fewer stores. But, eventually, to stave off a credit downgrade to “junk” it will have to cut its dividend. And, when that happens, it will truly be “good night Susie.”

As you might imagine, investors in Target didn’t take kindly to my skeptical view.

One poster predicted that my Target predictions would:

age like cat-shit wraped [sic] in dog-shit wrapped in chicken-shit like the rest of your ‘predictions.’”

Another helpfully reminded me that not all of my predictions come to pass in a timely manner:

Brother you’ve predicted 249 out of the last 5 market crashes and 876 out of the last 50 company bankruptcies can you stick to adverts in local news media instead of degrading the quality of my timeline?”

I got a chuckle out of that one.

I like to post my initial research into “hard to execute” ideas – investment ideas that are way out of consensus or where I have very little solid information – like shorting Target, on X. Why? Because millions of people frequently read my posts. And, more often than not, several of them will have critical insight into the opportunity. The jokes are also funny – if you’re not too thin-skinned. And, having lived the last 23 years of my life in a glass house with a Report Card waiting for me at the end of every year, my skin has gotten much thicker.

In Target’s case, connecting with store managers and other knowledgeable investors could give me a big edge. Then, when I’m certain I’ve got the story right, I will publish to our subscribers and put the idea in the Complete Investor portfolio. (If you want to see what I’m working on, please follow me on X: @porterstansb).

While it won’t grab the headlines like Nvidia surely will, Target also reported earnings today. And, sadly for its owners and employees, the results show a clear continuation of my short thesis: Target is the new Kmart.

In its most recent quarter, which ended November 1, Target posted revenue of $25.3 billion – a decline of 1.5% from the prior-year. That doesn’t seem too bad, but the declines were driven by continued substantial declines in same-store sales, which fell 2.7%. That’s the third consecutive quarterly drop. Omninously, in-store traffic specifically contracted by 2.2%.

This is not a temporary dip; it is customers deliberately rejecting Target’s physical locations in favor of other retailers. Most worrisome for Target, which again depends on affluent soccer moms, is the growing trend of this demographic to rely on delivery services, like DoorDash (DASH) and Instacart (CART). These services are robbing Target of the high-margin impulse buys these customers make inside the stores. And it is those sales that drive Target’s operating margins.

Today, Target reported GAAP (Generally Accepted Accounting Principles) earnings per share (“EPS”) of $1.51 for the third quarter, down a stark 18.4% year-over-year. And management knows this rate of decline is not going to change anytime soon. Their updated full-year guidance is depressing. They’re expecting continued same-stores declines, which will hurt results even more than in other quarters, because retailers make the lion’s share of their profits during the Christmas season. At the low end of the new guidance – $7.00 adjusted EPS – Target will deliver a 21% year-over-year collapse in earnings per share! That’s despite facing easier comparisons from last year, when they liquidated the worst of their post-COVID inventory glut.

These results suggest (at least to me) that Target’s brand and business model are now permanently impaired.

Since the fiscal 2022 peak, when annual revenue stood at $109 billion, cumulative revenue growth has been a pathetic 0.6% – essentially flat over three full years. Again, that doesn’t seem too bad. But inflation in this period has been substantial. Adjusted for the 8% to 10% annual retail inflation over this period, there’s been a 25%-plus decline in real (adjusted for inflation) revenue. If you doubt my inflation estimate, just look at what’s happened to Target’s margins: Operating income over the same span has plunged 38%, net income has dropped 41%, and diluted earnings per share has collapsed 37%.

And, where does the rubber really meet the road? Free cash flow, once a robust $6 billion a year, has eroded to roughly $4.5 billion on a trailing twelve-month basis. For the full year, I expect it will be slightly more than $4 billion.

Once again, this doesn’t seem too bad, but look closer. Management has preserved free cash flow (and protected the dividend) by slashing capital investments by almost 50%. New store openings have been throttled (down to less than 20 per year). Remodeling programs were scaled back. And so, capex was gutted to defend cash flow.

Under the new CEO (Michael Fiddelke, who takes the helm next February), the next phase of cost cutting will be far more severe. Rumors say he’s planning to close 117 stores next year while canceling store remodeling entirely. That will cut capital spending by another 30%.

This is precisely the defensive shrinkage Kmart undertook from 2001 to 2003 before its forced merger-of-desperation with Sears and eventual oblivion.

Most investors won’t notice these material changes to the business’s performance. But they will notice when the dividend is cut.

The company’s $2 billion annual dividend payout (representing a yield of over 5% today) remains the foundation of the share price. Management will do anything it can to preserve the dividend payment, including cutting capex to virtually nothing and adding even more debt to the balance sheet. They can forestall the doom, but they won’t be able to stop it.

Free cash flow coverage has thinned to approximately 2.2x the dividend. And persistent traffic declines of more than 2% per quarter guarantee continued erosion of margins and cash flows. If the established trend holds – and the latest quarter proves it is accelerating – fiscal 2026 will bring a revenue contraction of 4% to 6%, driving operating margins below 4% and free cash flow under $3 billion. Dividend coverage will fall below 1.5x by early 2027.

At that point, the market will start pricing-in a dividend cut, even if the actual cut continues to be forestalled by actions that further impair intrinsic value (like more debt). At this point, you’ll hear management say, repeatedly, that they’re not going to cut the dividend – up to and including the night before they do!

This exact sequence – cutting capex and then the dividend to “preserve liquidity” – precipitated the final collapse of Sears in 2017 (dividend cut followed by bankruptcy filing within 18 months), Rite Aid in 2019 (dividend cut followed by bankruptcy in 2023), and Bed Bath & Beyond in 2020 (dividend cut followed by Chapter 11 in 2023).

On the credit front, Target currently maintains a solid investment-grade rating of A- from S&P Global Ratings and A2 from Moody’s Investors Service. However, with net debt-to-EBITDA already trending upward and interest coverage sliding, any further persistent traffic erosion will push leverage (debt-to-EBITDA) toward 3x by late 2027 and interest expense coverage below 5x.

Our distressed debt expert, Marty Fridson, can help us refine the timing of the likely credit downgrade sequence, but it will happen something like this:

- The first downgrade will be to the lowest investment-grade tier (BBB-/Baa3) at some point in 2027 or 2028.

- The catastrophic downgrade – a fall into junk territory (BB) – will happen by the end of 2029, once store closure charges of $1 to $2 billion hit the income statement.

- Target’s refinancing spreads will explode by 200 to 400 basis points – meaning it will cost the company a lot more to refinance its existing debts. And that will quickly lead to a death spiral.

This is the identical path J.C. Penney traveled from investment-grade in 2012 to junk in early 2020 to bankruptcy filing later that same year.

As far as confirmation of this thesis goes, I don’t think investors often get this kind of gigantic red flag: Ulta Beauty (ULTA) will withdraw, completely, from more than 600 shop-in-shop Target locations by August 2026. It’s hard to imagine a more complete repudiation of Target’s customer base, retail store value, and brand.

This is not a cycle. This is Kodak in the late 1990s, stubbornly clinging to film while digital cameras rendered it obsolete – a position I shorted profitably for several years, starting in the fall of 1998. It is Sears in the late 1990s, watching big-box category killers eviscerate the department-store model – another short I initiated profitably early in its decline.

Target is the new Kmart, being destroyed by the modern Wal-Marts – Walmart, Amazon, and Costco.

Target is repeating every fatal mistake of these predecessors, only with the added accelerant of digital disintermediation via Instacart and DoorDash.

The trajectory is locked. Once your retail brand loses status with high-value customers, it is virtually impossible to rebuild that franchise. Target has gone from the cool place to discount shop to a ghetto store where everything is locked up – but it continues to lose $1 billion a year to theft anyways!

Washington Buying Stocks As A Matter Of National Security

Presented by Digest Publishing

It’s unprecedented. The world’s richest entity – the U.S. government – is now using taxpayer funds to buy shares of select stocks… and sending them surging HUNDREDS of percent. And the legendary Rick Rule, alongside a very special guest, reveals on camera which companies could be next in line… and gives you a free stock pick for tuning in.

Three Things To Know Before We Go…

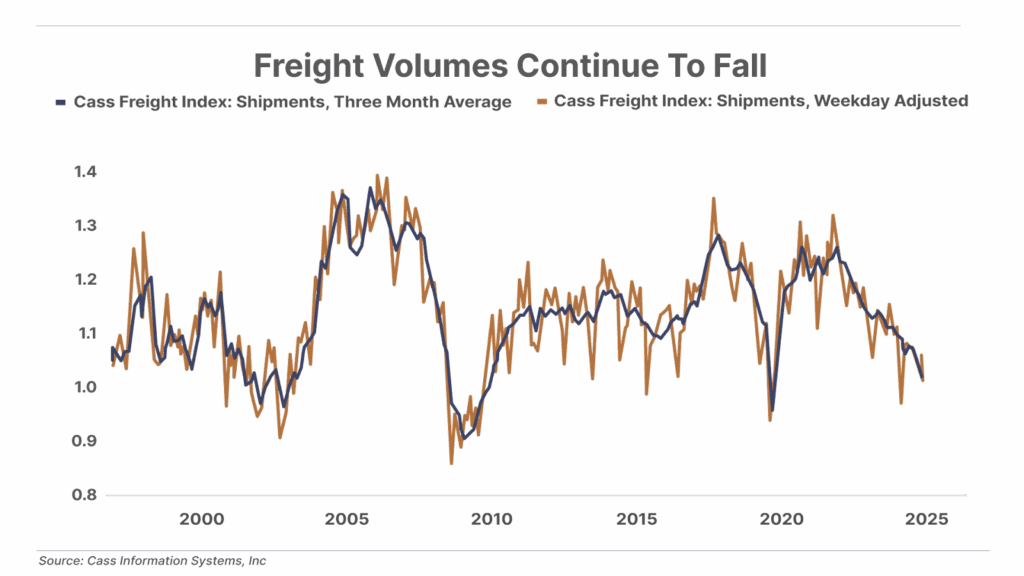

1. Freight data is flashing warning signs for the economy. The Cass Freight Index – North America’s benchmark measure of shipment volumes – fell again in October to its lowest level since the pandemic, signaling a contraction in the physical movement of goods. Trucks move the bulk of industrial inputs and manufactured products in this country, so when freight shipments decline, it’s a clear signal that economic activity is slowing. And unlike the recent weakness in the jobs market, the slowdown in shipping volumes can’t easily be blamed on artificial intelligence (“AI”) disruption.

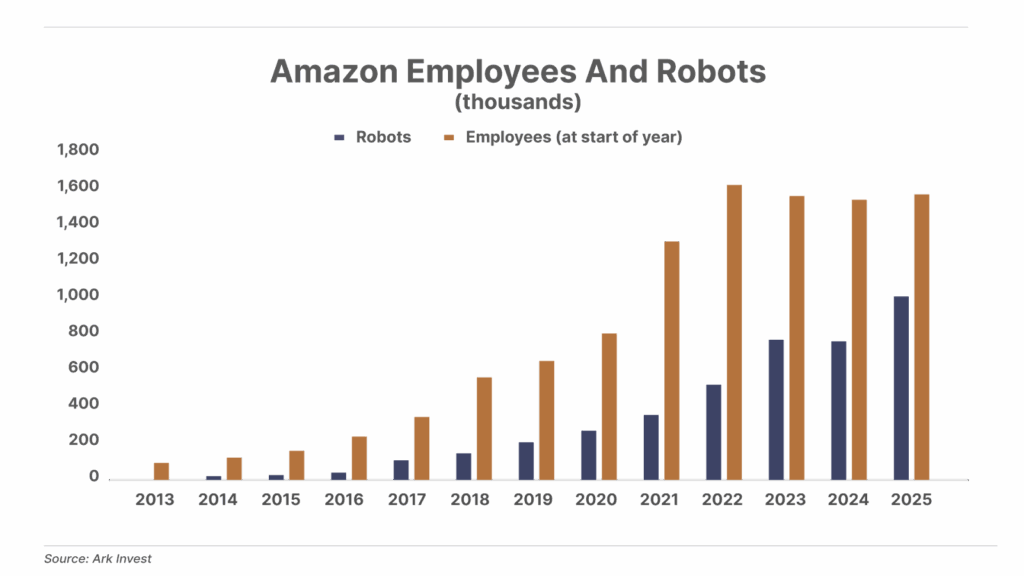

2. The robots are coming. Stunning data from Amazon (AMZN) shows workplace automation is quietly accelerating. Since 2022, the number of employees at the company is essentially unchanged at just under 1.6 million. Meanwhile, the company’s use of robots has nearly doubled from 520,000 to 1 million. If this trend continues, the company will likely employ more robots than humans by 2027.

3. Nvidia earnings on tap. Leading AI chipmaker Nvidia (NVDA) reports Q3 earnings after the market close today. Analysts expect another banner quarter of growth, including 57% year-on-year (“YOY”) revenue growth to $55.2 billion and a 56% YOY increase in earnings per share to $1.26. The key thing we’ll be watching for is any hint of guidance for the 2027 fiscal year (ending January 31, 2027). Based on current estimates, Nvidia is on track to earn $6.83 in FY 2027, which puts the forward valuation at a reasonable 27x earnings.

And One More Thing… The Energy Sector Is Incredibly Cheap

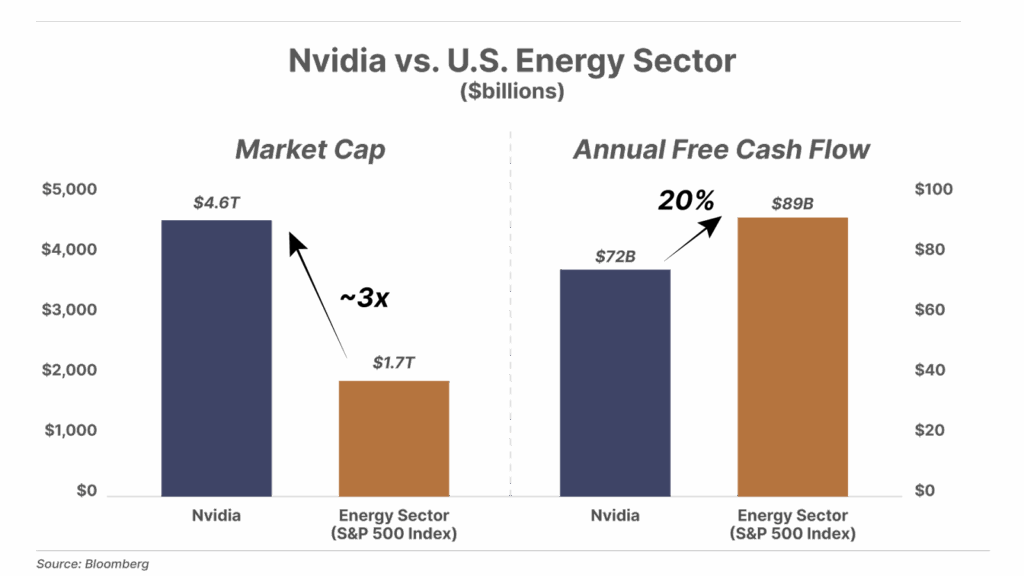

Nvidia is obviously critical to the Parallel Processing Revolution. However, we also need massive amounts of energy to power the huge AI data centers running Nvidia chips. And as the chart below highlights, the entire energy sector of the S&P 500 is currently valued at just one-third the market cap of Nvidia alone. Meanwhile, the combined free cash flow of the sector is 20% higher than Nvidia’s.

In short, energy companies are as cheap as ever today. But that won’t be the case forever. You can get immediate access to detailed research on all of our favorite energy stocks with a subscription to our flagship Complete Investor advisory. Click here to learn more.

Tell us what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

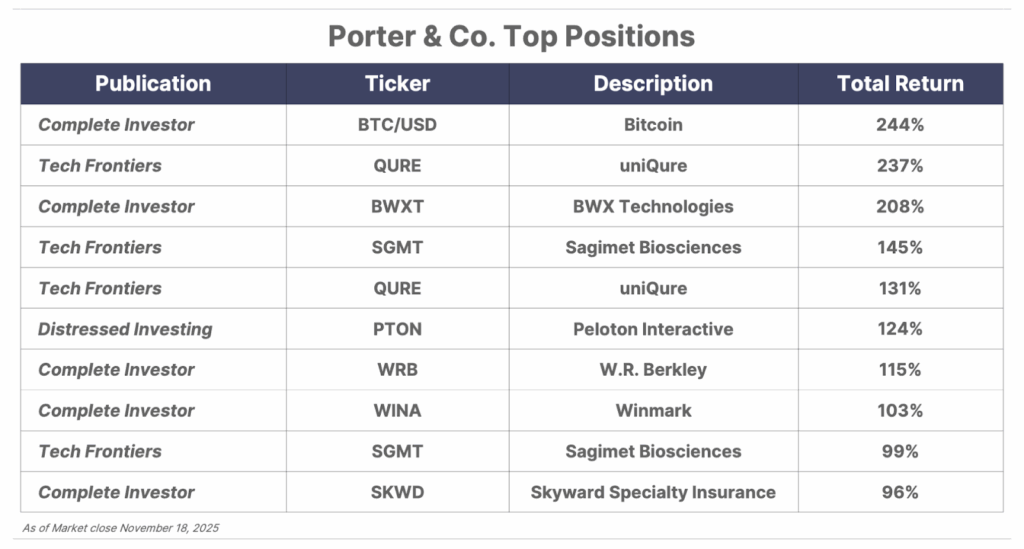

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.