In many ways, the 2020s inflation scenario matches that of the 1970s.

Jerome Powell May Be Serving Up A “Great Inflation” Remix

| If you’re new here: Welcome! You’re reading “Something You Don’t Know,” Porter’s complimentary e-letter. It reveals a hidden market story, or dissects a largely misunderstood element of investing, every other Friday, at no charge. You can see our archive of earlier issues at this link. If you’d like to access Porter’s long-form analysis, you can sign up for The Big Secret on Wall Street here. |

President Lyndon B. Johnson – all towering 6’3” Texan of him – was pissed.

And his bespectacled Federal Reserve chairman, Bill Martin, was scared.

It was early December 1965, and Martin had been summoned to the president’s Texas ranch home to “talk things over.”

Visitors to Johnson’s ranch, known as the “Texas White House,” never knew what to expect. They might be whacked with a rolled-up newspaper or knocked off a motorcycle by the petulant president (a fate that famously befell Secret Service agents who refused to wash his car). Dogs – like one of the long-suffering First Beagles, Him – ran the risk of being lifted off the ground by the ears.

This time, Johnson chose violence again…

Hefty LBJ grabbed the bookish Fed Chair and shoved him against the wall. “You took advantage of me and I just want you to know that’s a despicable thing to do,” the president growled.

After taking over from John F. Kennedy in 1963, Johnson had ramped up the biggest extension of the American social safety net since the creation of Social Security in 1935. Medicare, Medicaid, and the War on Poverty marked the largest fiscal expansion since FDR’s New Deal.

And the money to pay for it had to come from somewhere…

LBJ’s explosive spending growth ended a 13-year streak of tame inflation that averaged 1.5% from 1952-1965, pushing inflation up to 4.5% in 1966.

Straight-laced Bill Martin (known as “the Happy Puritan”) wasn’t having it. Two days before the showdown at LBJ’s ranch, the Federal Reserve Board had begun raising rates, from 4% to 4.25%, in a bid to rein in inflation.

LBJ, however, wanted the cheap money to continue to flow. “Free” government money is a time-honored way to buy votes, after all. And economic growth – which comes a lot easier when interest rates aren’t rising – is electoral catnip.

The hawkish Martin stood in the way of the President’s ambitions. Hence the little “bully session” at the secluded 2,700-acre ranch.

Bill Martin left Texas with a lot on his mind. And after a few more modest rate increases to 5.75% in 1966, he caved into President Johnson’s wishes – and in 1967 began cutting rates.

LBJ’s aggressive fiscal expansion and Martin’s easy money policies pushed inflation to an 18-year high of 6.1% by the time Johnson left office in 1969.

But that was just the beginning.

As the Richmond Fed explains: “In retrospect, many scholars now believe that the roots of the 1970s inflationary spiral can be found in the 1960s.”

Why The U.S. Stock Market Went Nowhere for 16 Years

The unholy dream team of Bill Martin and LBJ set the stage for the “Great Inflation” of the ‘70s – an era of lengthy gas lines and obscene grocery prices that readers of a certain age may remember with horror.

Bill Martin felt it was his fault. “I’ve failed,” he told colleagues when he retired from the Fed in 1970.

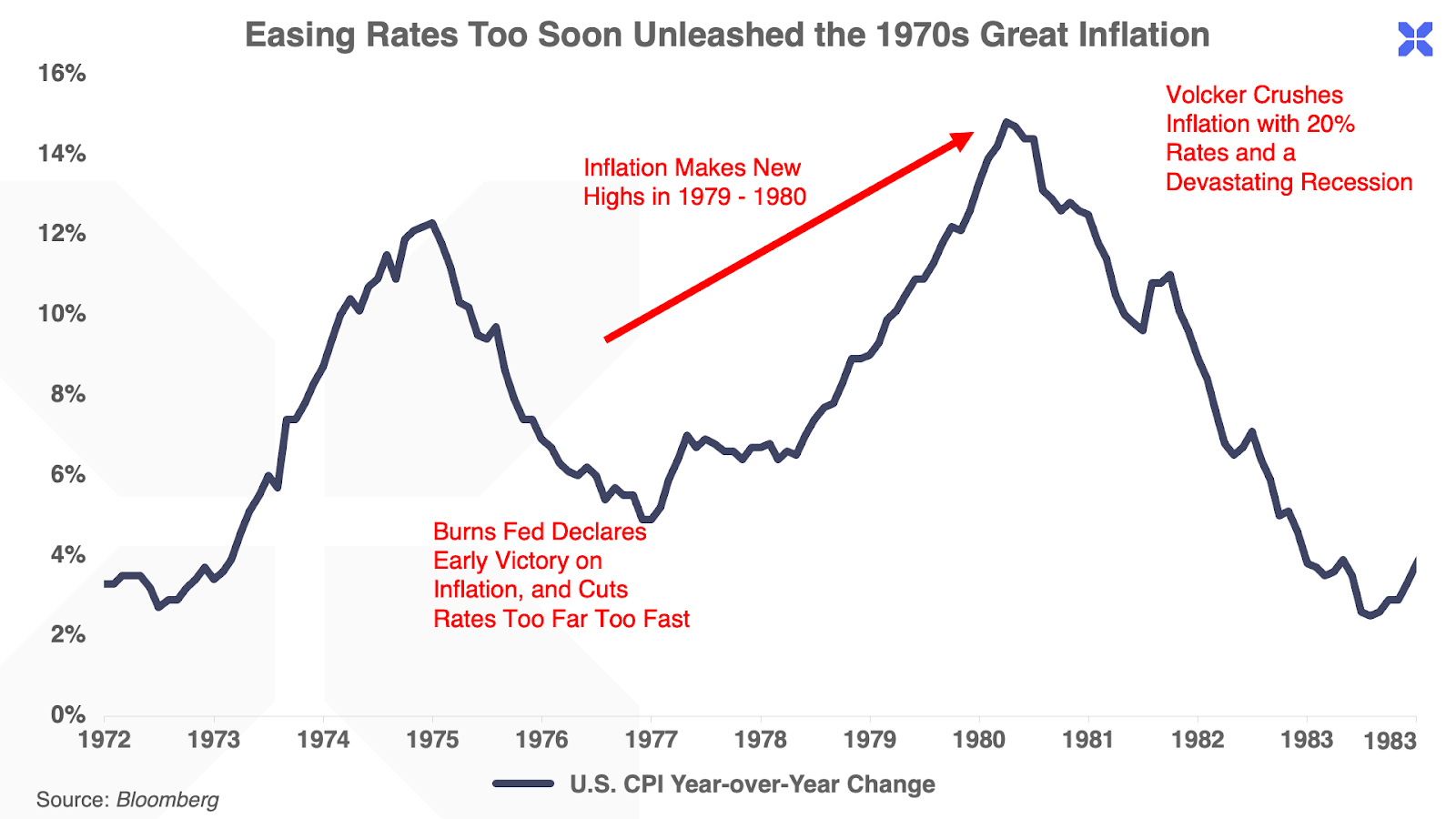

He shares the blame, though, with Arthur Burns, the next Fed chair. A Nixon appointee, Burns slashed interest rates from 9%, to 3.2% in 1972. And at the same time, President Richard Nixon applied bully tactics – no wall-slamming, though – to manage the U.S. economy.

“Tricky Dick” infamously welched on the gold-backed promise of the American dollar by closing the gold exchange window on August 13, 1971. Overnight, the U.S. currency was no longer backed by gold. And two days later, in a nationally televised speech, he announced, “I am today ordering a freeze on all prices and wages throughout the United States.”

When politicians wage war with the market, the market wins. Not only did Nixon’s price controls fail to contain rising prices, but – as Economics 101 suggests – they instead triggered crippling shortages throughout the economy. By 1974, inflation reached 12% – at the time, the highest in modern American history.

Higher interest rates pushed inflation down to 5% in 1977. But Burns declared victory too early, and cut rates too soon. And inflation soon came roaring back, to new highs of 15% by 1980.

What Burns failed to realize was that inflation expectations had become entrenched in the economy after 10 years of running hot. As consumers feared further price increases, they demanded ever-higher wages, creating a devastating wage-price spiral that turned high inflation in the early 1970s into the Great Inflation that spanned the entire decade.

As a result, Americans saw their real income fall as economic growth stagnated. And investors endured a lost decade of negative real returns.

Finally, take-no-prisoners Fed Chair Paul Volcker, who took the reins from Arthur Burns in 1979, did the fiscal equivalent of using a pickaxe to swat the big mosquito on the forehead of the American economy, by raising rates to an unheard-of 20%. Inflation sputtered to a halt – the mosquito was dead – but a devastating recession crushed the economy, along with asset prices.

Volcker’s strong medicine killed inflation, and set the stage for robust economic growth in the 1980s.

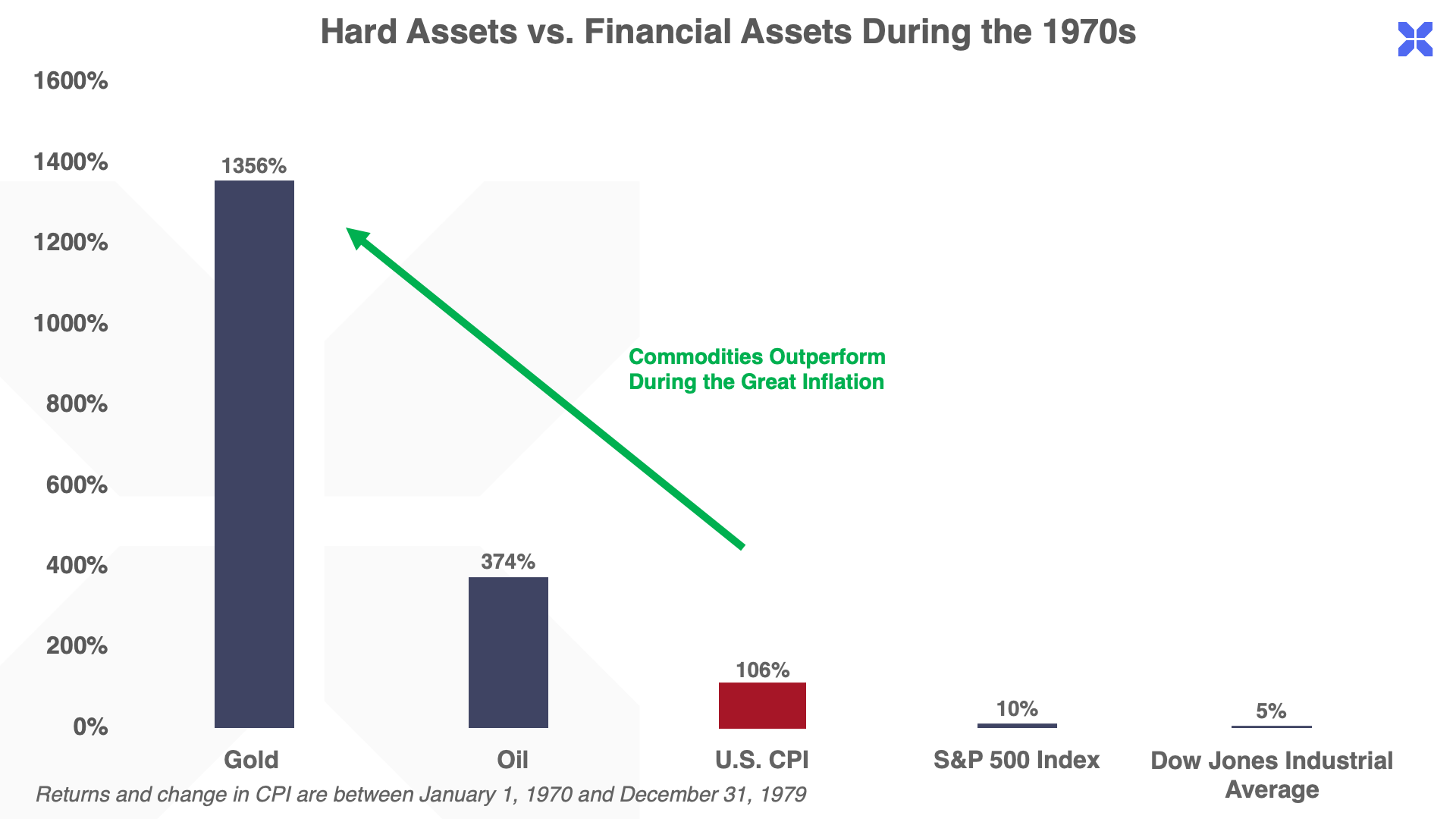

The damage to long-term wealth creation in markets was severe. Between 1965 – and LBJ’s manhandling of his bookish Fed chair – and the Volcker pickaxe, the U.S. stock market went approximately nowhere. The only winners in this environment were hard assets, including energy, copper, gold and other commodities.

The worst thing about this sorry tale: It’s happening again… to borrow from humorist Mark Twain, history is rhyming.

Powell’s Fed Risks a 1970s Redux

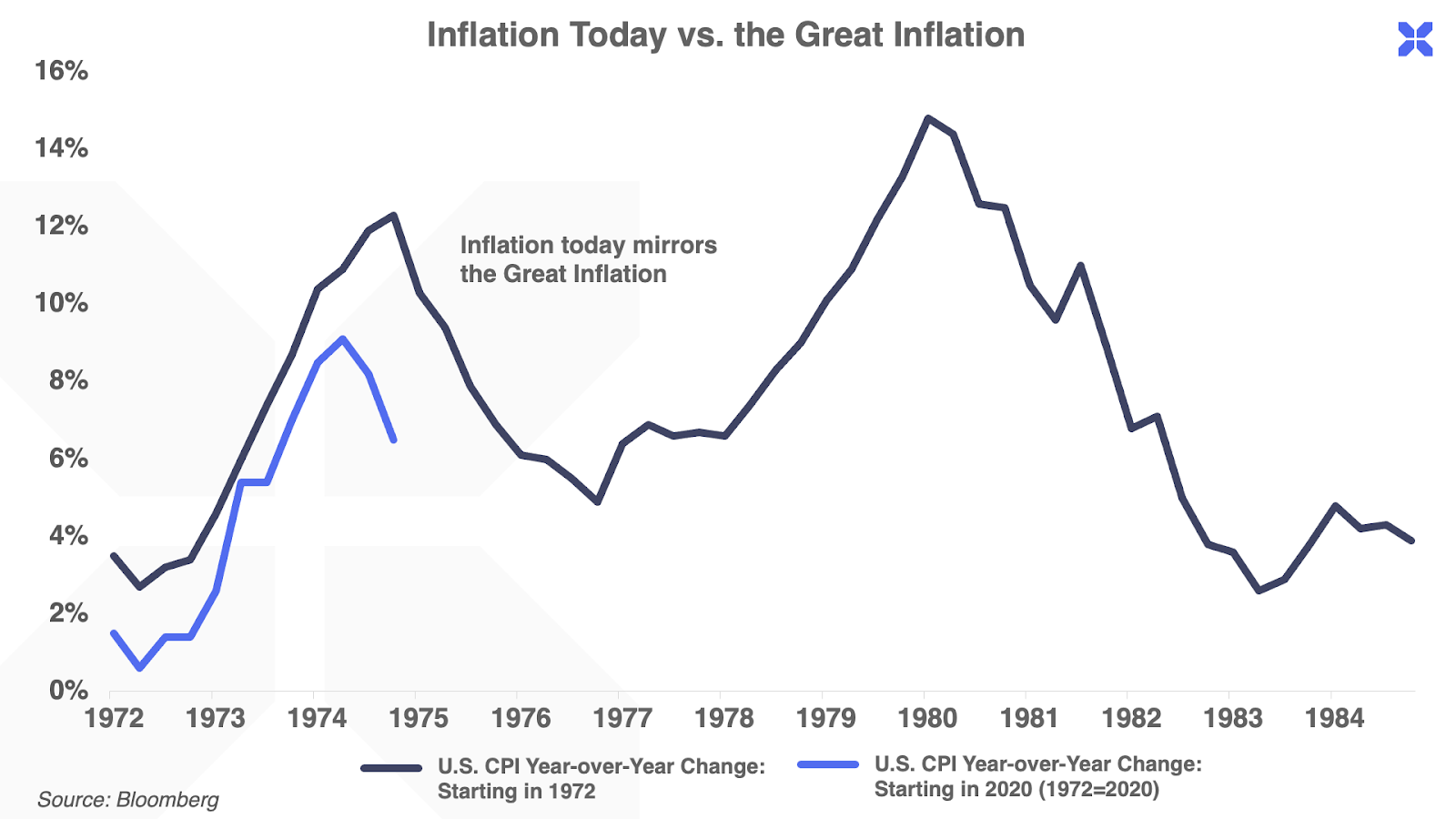

In many ways, the 2020s inflation scenario matches that of the 1970s.

For starters, 2022 was the worst year for the traditional 60/40 stock and bond portfolio of the last four decades… while commodities like energy have outperformed most other asset classes.

It’s not a scene-for-scene remake… but it’s easy to recognize some source material.

- COVID-era stimulus provided an influx of “free” government cash, much like LBJ’s earlier welfare schemes…

- “Happy Puritan” Bill Martin kept rates too low for too long… and so, more recently, did Jerome Powell…

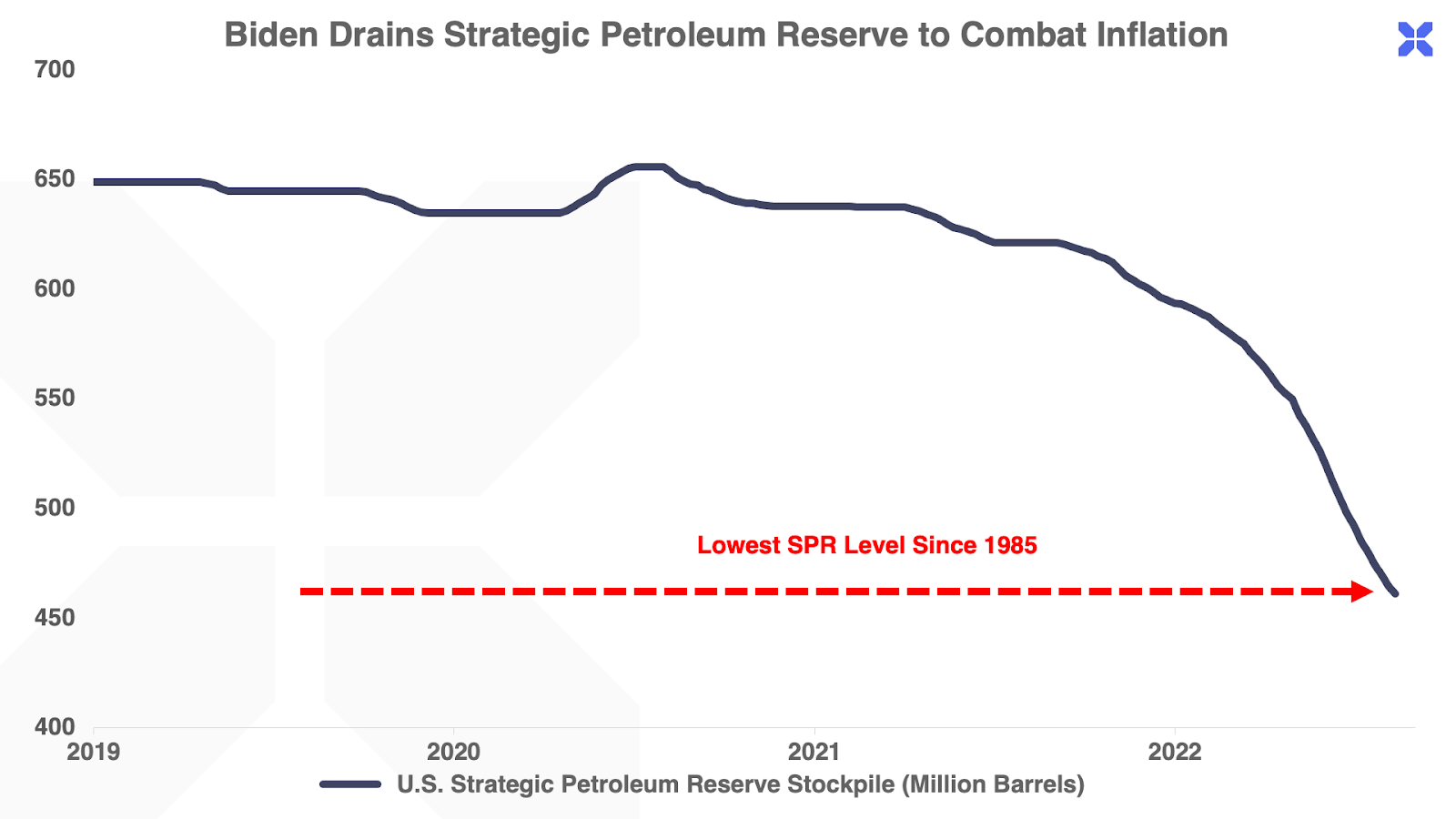

- And U.S. President Joe Biden – like Nixon in 1971 – has attempted to artificially suppress inflation, not with outright price controls, but rather by a record draining of the nation’s Strategic Petroleum Reserve to cap energy prices.

The problem with market manipulation that pressures prices in the short term is that it sets the stage for higher prices down the road (like Nixon’s price controls, which resulted in, for example, Americans paying the today-dollar equivalent of $9 for a gallon of milk).

Likewise, by dumping over 200 million barrels of oil onto global markets via the strategic petroleum reserves, the Biden administration has artificially lowered oil prices, to around $78/barrel today. And that’s undercut the incentive for desperately needed investment into new production.

For example, the number of oil drilling rigs deployed in the U.S. has now dropped to a new recent low of 771, or 304 less active drilling rigs than the pre-pandemic levels of 2019… setting the stage for an energy shortage soon. (And rather than invest, today energy producers are returning capital to shareholders, as in Chevron’s recently announced $75 billion share buyback program.)

In recent months Mother Nature has delivered a one-time “get out of jail free” card for global energy markets, with one of the warmest winters on record, both in Europe and the U.S. The historic draining of the SPR, coupled with extremely mild winter weather, has provided a brief respite for global energy prices… and a pause for global inflation.

Remember that temporary drop to 5% inflation in 1976, about midway through the Great Inflation? That’s where we are now.

After peaking at a 40-year high of 9.1% last summer, the U.S. consumer price index (CPI) retreated to a recent low of 6.4% in December 2022.

And that short-term drop has emboldened… and misled… the market.

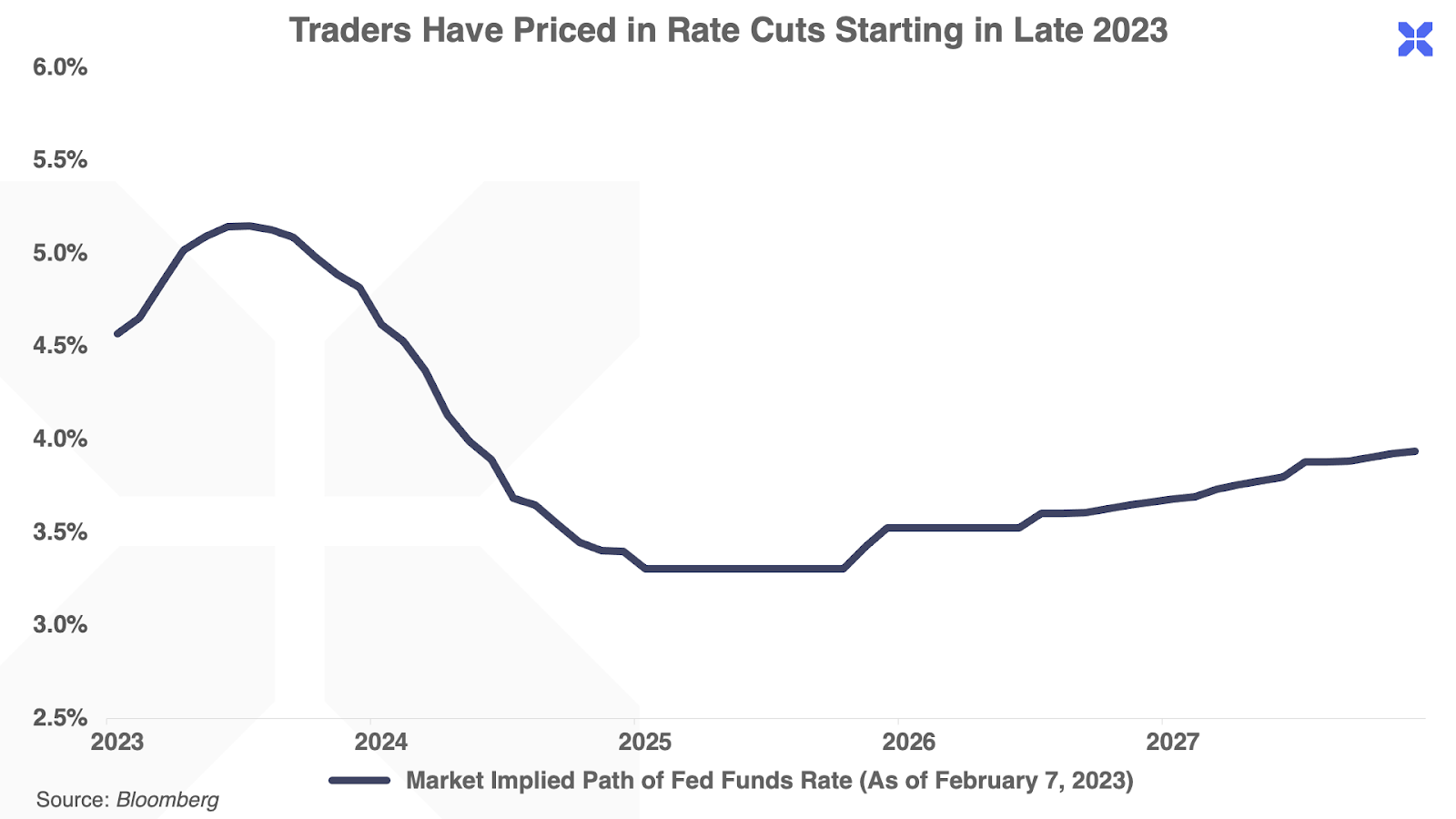

The consensus is that the so-called “Powell pivot,” towards rate cuts, is imminent. As shown in the chart below, the Fed Fund Futures are pricing in rate cuts starting in the second half of 2023, so that rates fall below 3% (from 4.25% now) by 2025:

Powell knows the way to avoid a repeat of the Great Inflation is a “higher for longer” interest rate policy. During a Cato Institute monetary policy conference last year, he noted that “We need to act now, forthrightly and strong” to avoid the mistakes of the 1970s. He explained that what happened then “followed several failed attempts to bring inflation under control,” which led to inflation expectations becoming entrenched in the economy.

Back in the 1970s, Arthur Burns hit 5% CPI and thought he had inflation tamed… but, as we’ve seen, he blinked too soon. It remains to be seen whether Powell makes the same mistake.

If Powell cuts rates like Burns, we get more inflation. If he drastically tightens (like Volcker), we get a sharp recession. Neither path is good for risk assets.

And there are a number of signs of recession, as we’ve written before.

America’s Economic Engine is Sputtering

The U.S. economy runs on credit. When America’s credit engine sputters, so does the economy.

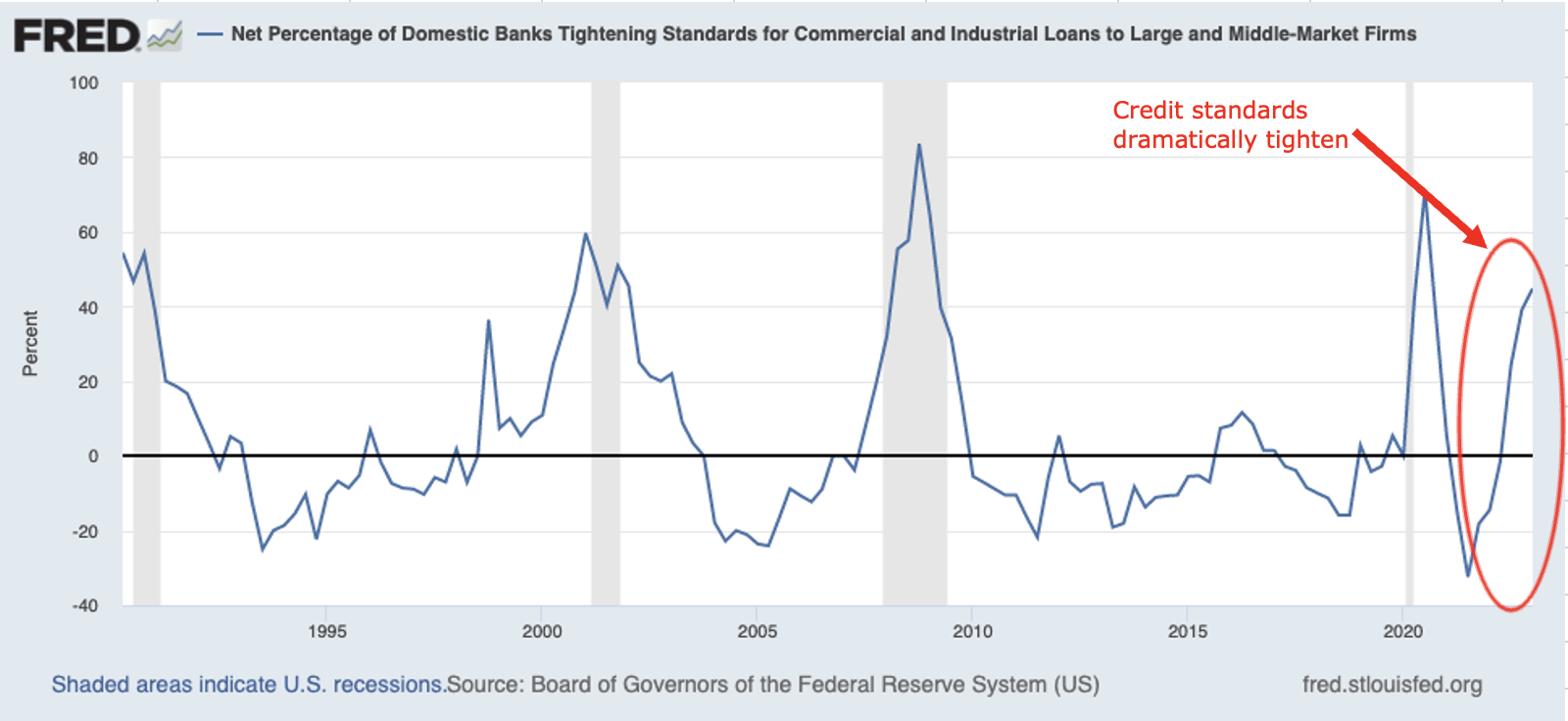

Bank lending standards have historically been a leading indicator of economic growth. Recent data shows a sharp increase in banks tightening lending for commercial and industrial loans. As the chart below shows, tightening lending standards has preceded every recession in the last three decades:

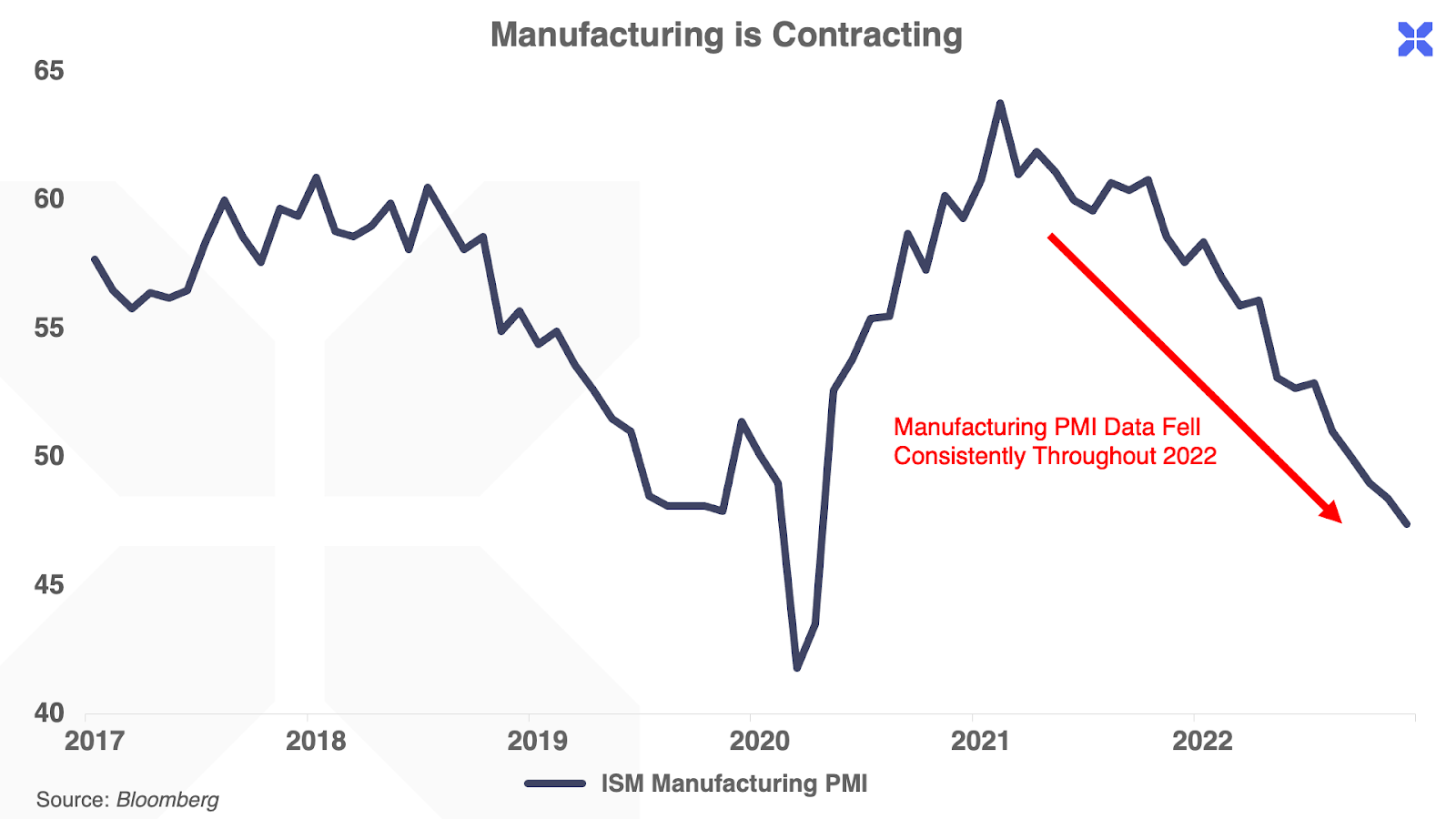

Tighter lending in the commercial and industrial sectors has translated into a sharp and persistent decline in manufacturing activity. This shows up in the purchasers’ manager index (PMI) – a survey of purchasing managers in the manufacturing sector that indicates whether their businesses are expanding or contracting:

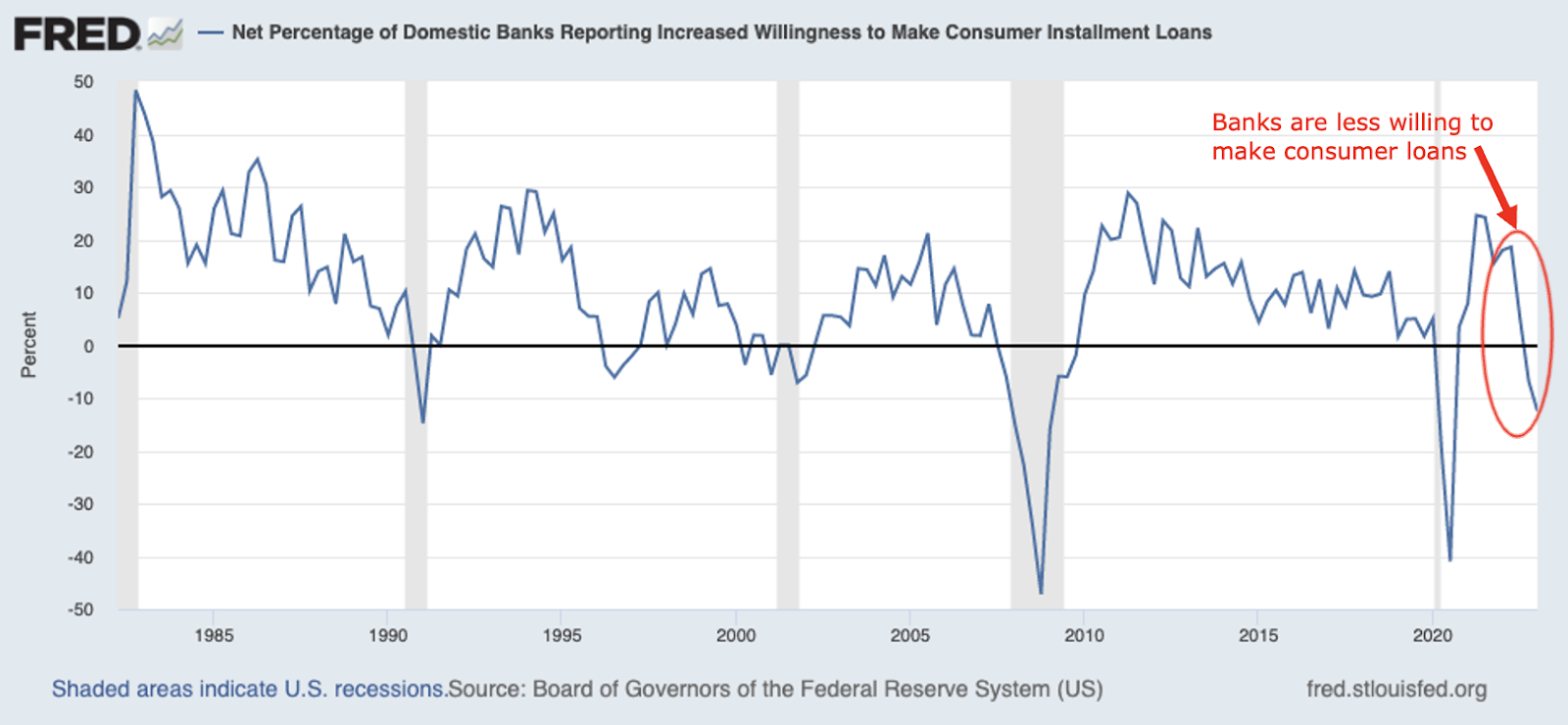

Meanwhile, banks are also tightening lending standards for consumer loans – another reliable leading indicator for an economic recession. Over the last twelve months, the percent of U.S. banks reporting an increased willingness to make new consumer loans has plunged deep into negative territory:

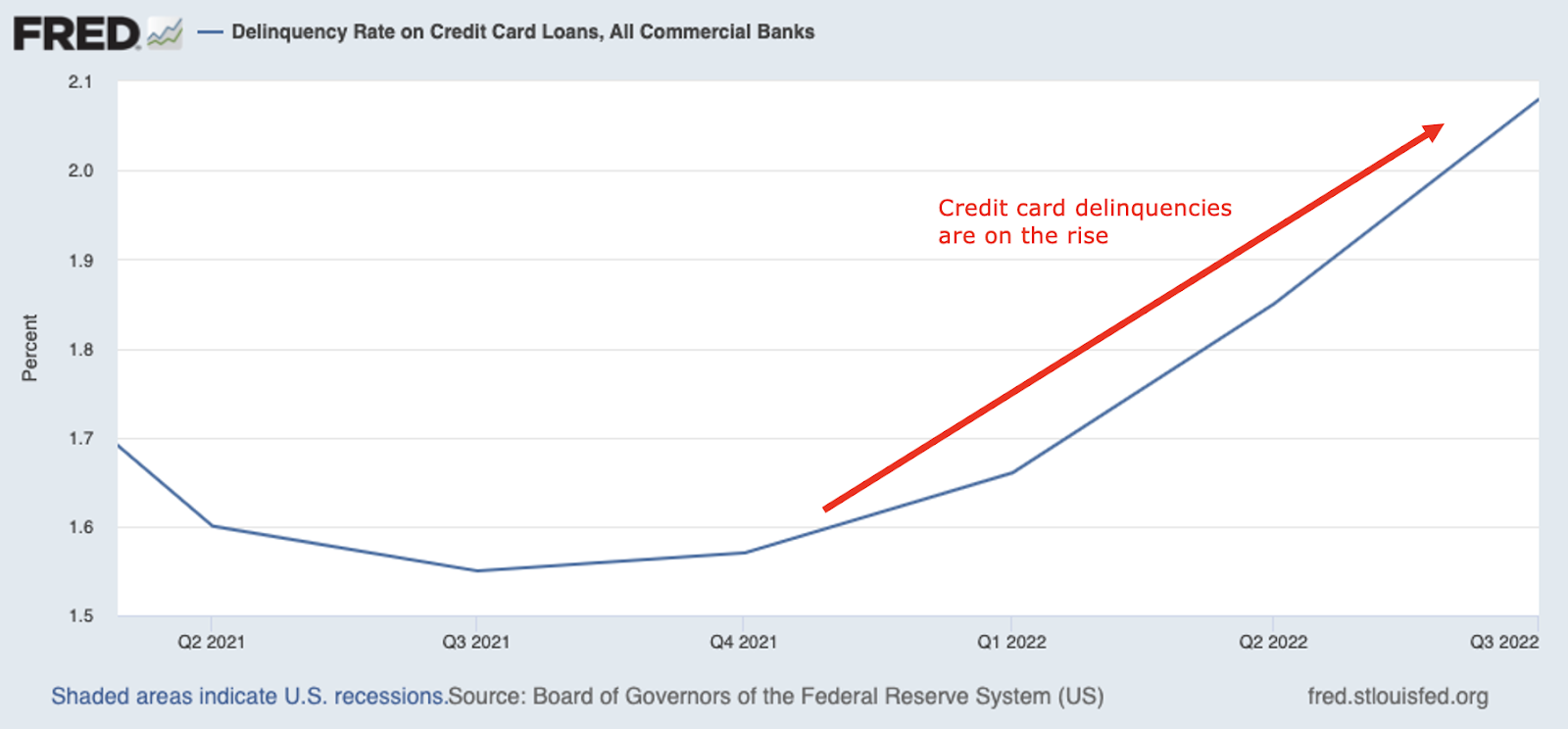

Banks are wary of making new loans right now because consumer defaults are on the rise. The chart below shows the recent acceleration in delinquency rates on credit card debt:

In the latest round of earnings calls, every major American bank reported a surge in credit provisions (capital set aside to cover future loan losses). For instance, J.P. Morgan reserved $2.3 billion for potential loan losses in Q4, a 49% increase from the prior quarter.

Here’s why this pullback in consumer lending is a big deal…

Over the past year, as inflation has eroded incomes, the consumer savings rate has plummeted to a record low of just 2.2%. In a recent survey, 64% of Americans reported that they are living paycheck to paycheck. As a result, they’ve turned to plastic, racking up a record $930 billion in total credit card debt, up by nearly $200 billion since 2020. (Not surprisingly, rising credit card use also played a significant role in the ‘70s recession.)

But with defaults on the rise and banks pulling back on lending, this source of spending is now drying up. Typically, American consumers take out roughly $20 billion to $30 billion in new credit card debt each month. In December, that figure fell to just $7.2 billion.

Fewer loans and fewer credit cards means less spending… and corporate America is feeling the pinch. S&P 500 companies are on track to post their first negative quarter of earnings-per-share growth since the COVID crash.

What’s more, the consensus estimates for the forward earnings of the S&P 500 just turned negative. This is a rare occurrence on permabull Wall Street – but when it happens, it usually precedes a steep drop in stock prices.

Despite the recent rally in stock prices, the key leading indicators of economic growth all point towards a sharp recession looming on the horizon. This includes rising default rates, tightening credit, and deteriorating corporate earnings.

The only question now is whether Jerome Powell will play the Volcker card and accept short-term economic pain to stamp out inflation for good. The alternative path of easing rates too soon risks a repeat of the Burns-era Fed, and a lost decade in economic growth and financial asset prices.

All things being equal, we’d rather deal with a sharp, one-time recession than another ten “lost years” of inflation. But the ball is in Powell’s court now.

How to Bulletproof Your Portfolio, No Matter Which Path Powell Takes

The Fed, like Mary Poppins, “never explains anything” – or, if it does, it’s always open to interpretation. As former chair Alan Greenspan once remarked: “If I seem unduly clear to you, you must have misunderstood what I said.”

Only Powell knows his own intentions. Meanwhile, investors need to focus on building a portfolio that can withstand a range of potential outcomes.

Focus on defensive names, like our capital-efficient “Battleship Stocks”. Find high-income securities like preferred stocks and REITs. And get broad exposure to commodities, and energy in particular.

High-quality energy companies can offer both offense and defense in a portfolio. In a recession, the current trend of underinvestment in fossil fuels should accelerate, boosting energy prices for many years. Conversely, in a 1970s replay, energy will provide one of the few safe havens during a high-inflation environment (just as it did in 2022).

The recent weakness in oil and gas prices has created an opportunity to buy some of the highest-quality energy companies in the market. Next week, for paid subscribers, we’ll introduce an energy royalty company poised to reap a windfall from the rise of America as a natural gas exporting superpower – a long-term trend that will support domestic gas prices regardless of the Fed, or the broader economic environment.

Finally, we’re also putting together a new team led by the “dean of high yield,” Martin Fridson – a true legend in the world of distressed debt. If the economy continues on its current path, we believe the stage is set for the “greatest legal transfer of wealth in history,” as default rates surge and high-quality debt trades down to pennies on the dollar.

Sign up here to get access to our existing portfolio, and the exciting new opportunities that are coming.

Porter & Co.

Stevenson, MD

P.S. If you’d like to learn more about the Porter & Co. team – all of whom are real humans, and many of whom have Twitter accounts – you can get acquainted with us here.