Issue #64, Volume #2

The Fool-Proof Way To Protect Yourself From Monetary Chaos

The “End Of America” began on November 25, 2008.

On that day, the Federal Reserve began buying mortgage-backed securities (“MBS”) and “agency debt” – the obligations of bankrupt Fannie Mae and Freddie Mac, two government-sponsored agencies that back most U.S. mortgages.

Through March 2010, the Federal Reserve purchased an astounding $1.25 trillion in MBS, $175 billion in agency debt, and, for good measure, $300 billion in long-term U.S. Treasuries.

Legally, only the U.S. Congress has the power to levy a tax. But because these securities were purchased with a modern-day printing press, Congress never approved these expenditures. Instead, these obligations were foisted on to the American people (about $5,000 per person) through an expansion of the money supply. Nevermind that the Fed’s own charter forbids it to buy mortgages.

Like a banana republic, America was monetizing the federal government’s debts and doing the same for private obligations (mortgages), too.

These events prompted me to write a documentary, The End Of America.

In that documentary, I predicted that this counterfeiting would lead to some obvious problems, like inflation. But, far worse, this sea-change in our monetary policy would lead to dozens of insidious cultural problems as the declining quality and reliability of our money would be revealed in a matching decline in our institutions, in civil society, and in our cultural cohesiveness.

In short, a debauched currency leads to a debauched society.

I predicted that America would lose its AAA-credit rating, as Fed asset purchases would continue, leading to never-before-seen debt levels in the U.S. I predicted that America would see an unprecedented increase in political violence. I predicted that America would see a huge increase in drug addiction, prostitution, and gambling. I predicted that the government would, eventually, take draconian and never-before-seen measures to change everything about how we live, how we work – even how we travel.

Our response to COVID wasn’t driven by any medical evidence or logic. It was driven by the idea that our government is all-powerful, a notion that was created by the printing press.

There hasn’t been a problem of any kind that hasn’t led to still more money printing ever since we started in 2010.

In 2012, in response to Europe’s sovereign debt crisis (why is that our problem…?), we launched yet another round of large-scale “asset purchases” – money printing. The Fed purchased $800 billion in Treasury securities and $800 billion in agency debt.

In 2019, there was a “hiccup” in the repo market. So, the Fed bought hundreds of billions in securities.

And, then, during COVID from 2020 through 2021, the Fed bought more than $7 trillion (!) worth of Treasuries and mortgages.

The printing and the spending and the borrowing will not stop – until eventually the entire system will collapse, most likely because of a civil war.

Or perhaps because of massive emigration.

Yes, really: productive people will leave the country when they can no longer build a reasonable life in America.

Most Americans still don’t understand. What we’ve been living through since 2010 isn’t merely a cultural evolution. We are watching the destruction of our entire society.

- There are now 1.4 million young women prostituting themselves daily on OnlyFans, which generates close to $10 billion a year

- Almost 25% of all American men between the ages of 18 and 49 have active online gambling accounts… generating over $100 billion in revenue – up more than 10-fold since 2018

- Since 2010, drug-overdose deaths increased from 12.4 per 100,000 to 27.8 per 100,000

- The homicide rate among African-Americans in 2010 was 17.7 per 100,000, and by 2020, it was almost 25 per 100,000

- There were virtually zero “transgender” people in the U.S. in 2010; today there are over 1 million (1 in 250) and the percentage of women who are actively homosexual has more than doubled (3.5% to 7.6%)

Why have all of these things happened?

It’s very simple: a sound currency rewards hard work, education, savings, productivity – the virtues of the bourgeoisie. A debauched currency incentivizes profligacy and destroys the middle class and its value system.

Inflation renders the American ideal impossible. Chaos follows.

Today, the median age of a first-time homebuyer is 38 years old.

We’re also living through a period of unprecedented corruption. President Joe Biden was a flat-out gangster. How many Americans back in 2010 would have ever dreamed of a U.S. president pardoning 4,245 people – including his own family?

Today, our sitting president is selling his own crypto coin, the most blatant influence peddling I have ever seen.

Remember: the Federal Reserve has never been audited. The American people still have no idea which specific mortgage bonds were purchased, from whom, or at what price. Nor will we be told the next time the Fed begins buying private assets. That’s virtually unlimited power. And we know what unlimited power does: it corrupts.

Today, the End Of America continues. Our government’s interest expenses on its debt have increased more than 5x since 2010, from under $200 billion per year to over $1 trillion.

And it’s not just the government.

Debasing the currency rewards borrowers over savers. There’s a huge incentive to borrow money when you know it’s going to be devalued over time. As a result, Americans have never borrowed more money. Collectively, we owe more than 400% of GDP in debt – public and private.

In total we will spend over $4 trillion on interest this year, about 11% of GDP.

This is obviously unsustainable. Likewise, it’s impossible for the existing Social Security and Medicare promises to be financed. Forget all of the huge numbers: there’s no way only three workers can support one retiree.

These problems are not someday-down-the-road issues. They are here, right now: in the next decade there will be at least a $10 trillion shortfall in these programs. There is no way we can afford those promises.

There’s no question that America is going to default.

And, finally, I am not the only person warning about these things. Both Bridgewater Associates’ Ray Dalio and JPMorgan Chase CEO Jamie Dimon have recently said in public things that for decades they would only say privately: America is approaching a default.

Seems like this would be simple to fix, doesn’t it? Economists understand there is no way for the government to spend more than 20% of GDP without causing huge deficits. So we simply have to cut spending. What’s so hard about that?

Well, watch what happens to anyone who tries!

Elon Musk is about to be destroyed. He’ll probably end up in jail, like a Russian oligarch.

America isn’t the nation you remember. Our government has become entirely captured by the Deep State. And the Deep State is undefeated. The spending will never stop because it’s the spending that sustains the Leviathan.

So… what should you do about all of this?

Well, the good news is, there’s a simple solution.

I outlined it for you last fall. It’s called the Permanent Portfolio. It was invented by my mentor, the legendary libertarian economist Harry Browne. It’s a way of structuring your savings – 25% in stocks, 25% in bonds, 25% in gold, and 25% in short-term fixed income (cash) – so that you’re protected from the wild asset price volatility that’s common to all big inflations.

And, you may recall, this is the strategy Ray Dalio used to build Bridgewater, creating the world’s largest hedge fund.

I made a few simple changes to the formula to capitalize on innovations (like Bitcoin) and to minimize the risk of investing in bonds.

Rather than owning bonds directly, I recommend owning them via investments in insurance companies, which can actively manage the duration risk in their bond portfolios. I unveiled an entirely allocated Permanent Portfolio last fall (with a fully diversified equity portfolio), and we’ve tracked its performance since. Porter’s Permanent Portfolio is up about 20%, with virtually zero volatility.

But it can be even easier!

You really don’t need to have 20+ positions. You just need to own: 1. A great consumer brand business. 2. A disciplined underwriter and bond investor (property & casualty insurance) 3. Gold and Bitcoin. 4. Cash.

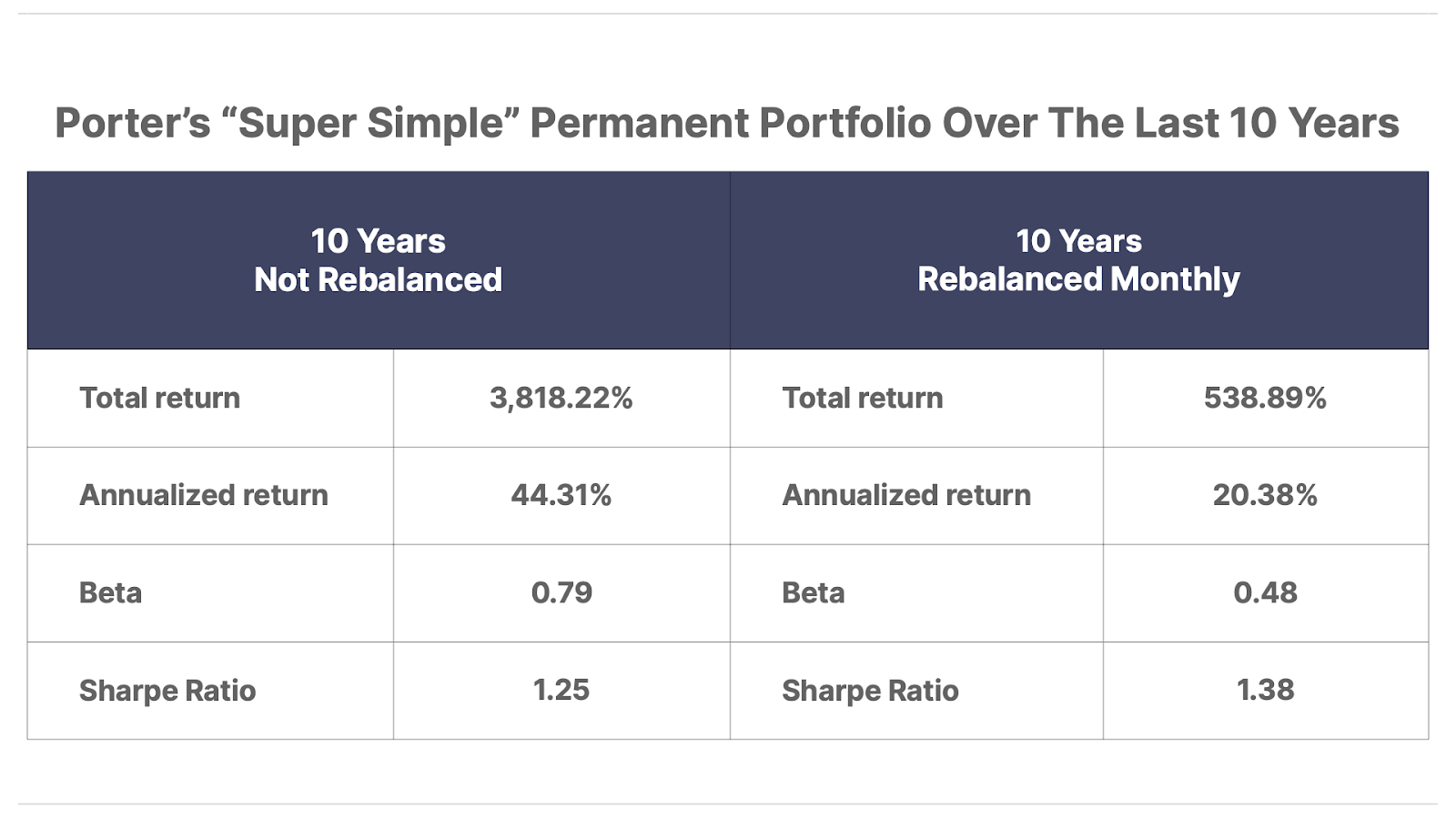

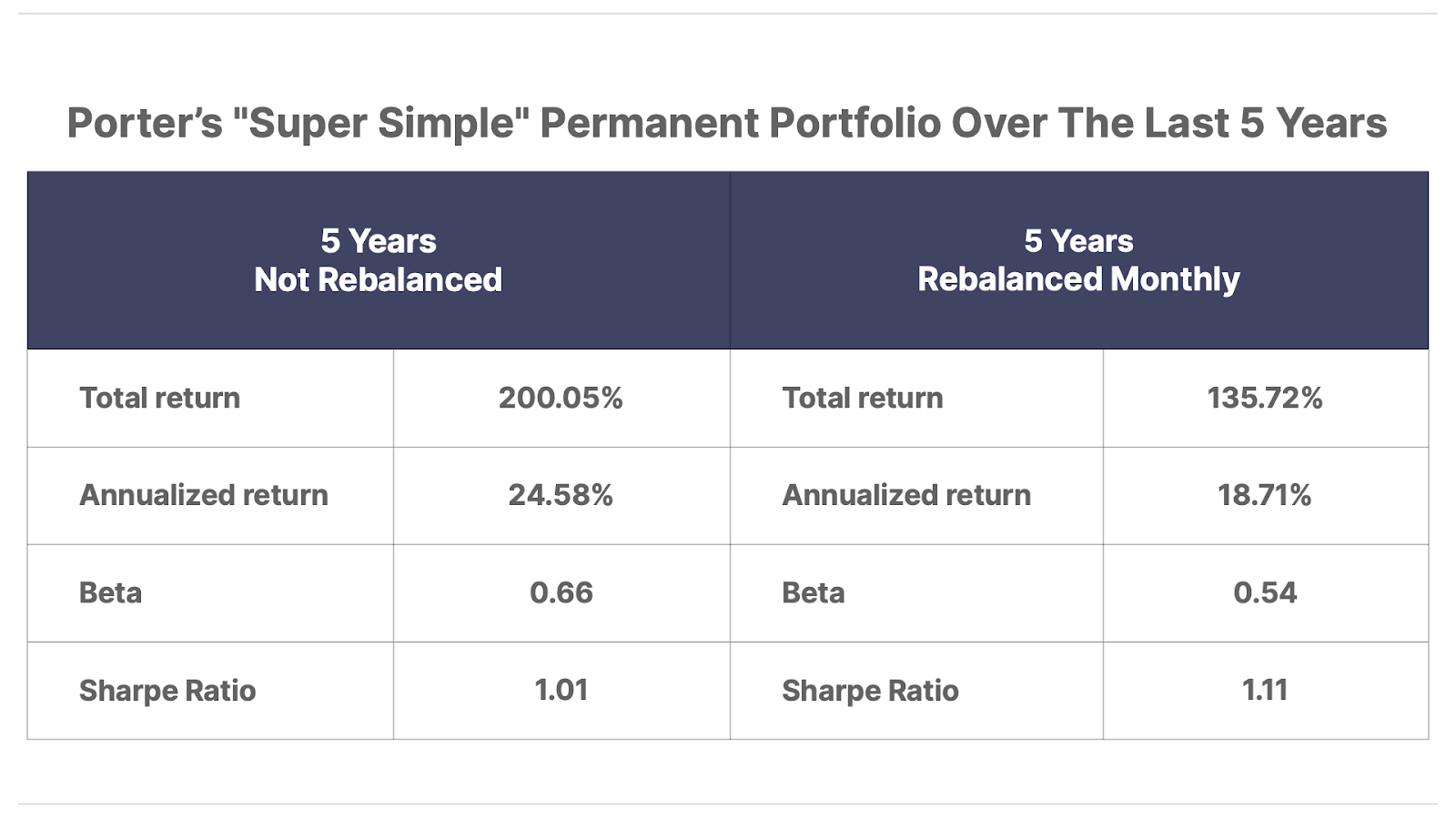

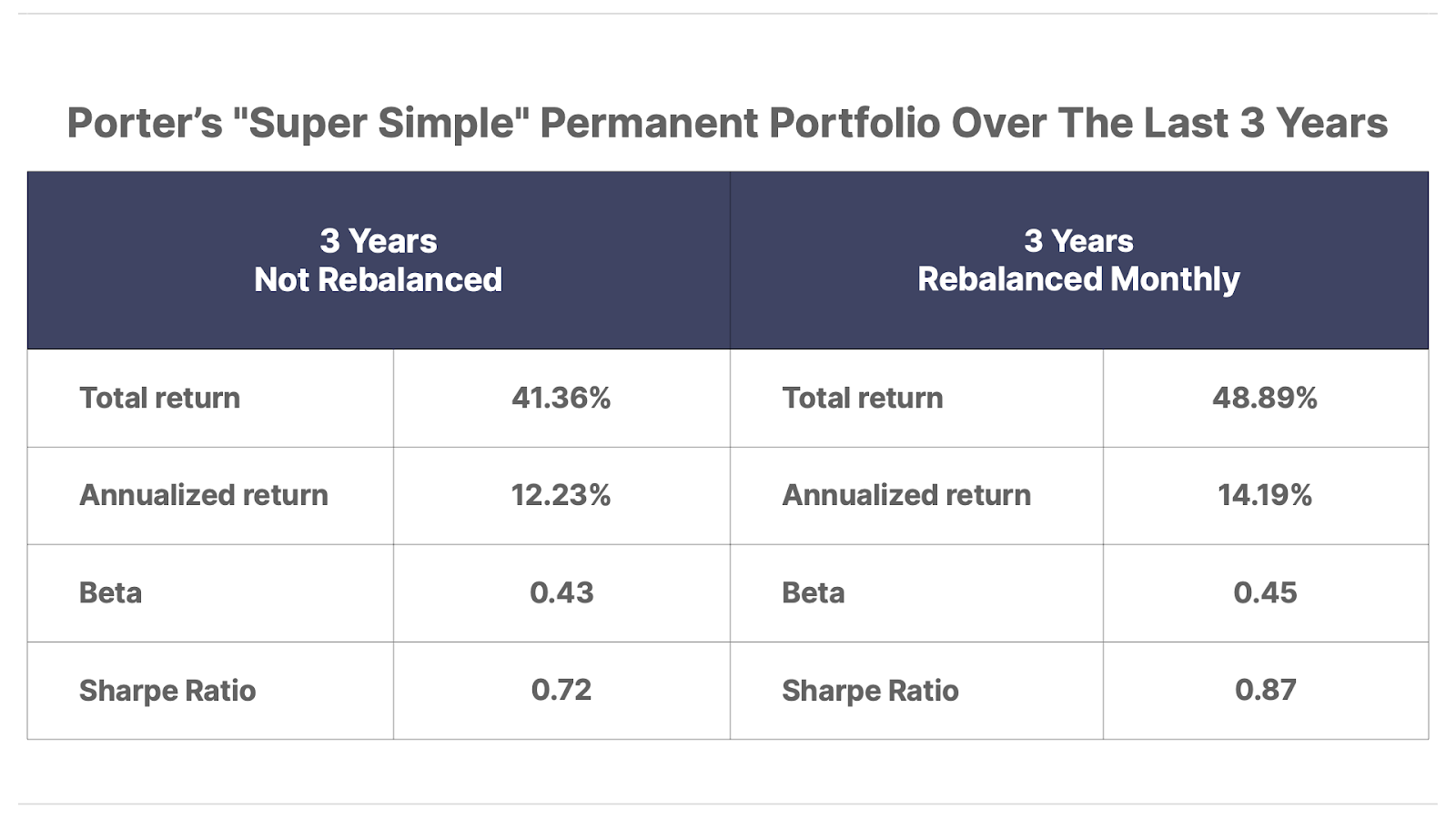

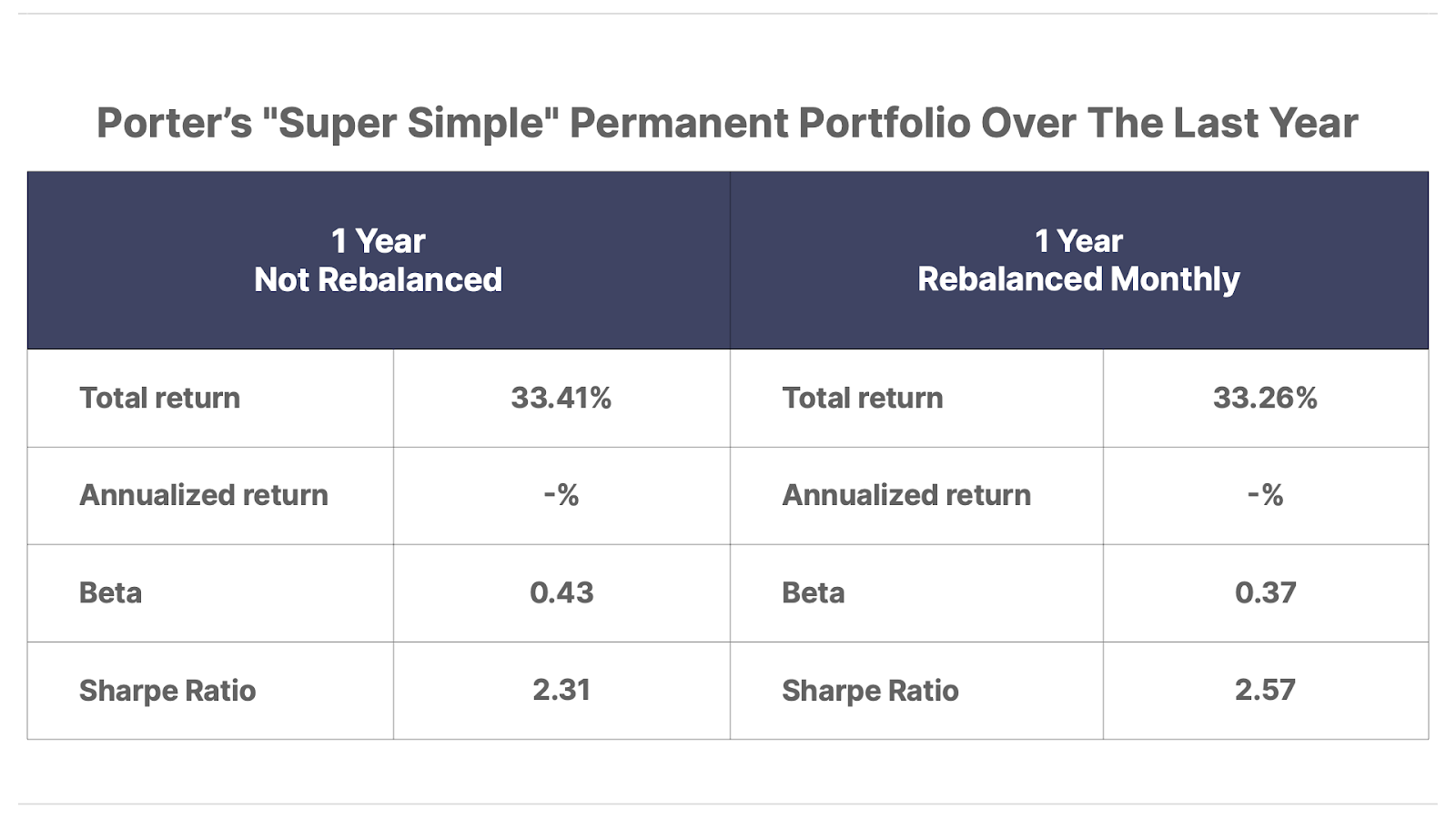

I asked our research team at Porter & Co. to run a simple simulation, to see how a scaled-down, super simple version of Porter’s Permanent Portfolio would have performed over the last decade.

I’ve written – for years – that Philip Morris International (PM) is the best consumer products company of all time. I’ve written – for years – that W.R. Berkley (WRB) is the best property & casualty insurance company in America. I’ve written for years that Franco-Nevada (FNV) is the best way to own gold. So what if you only owned these securities, along with Bitcoin and cash?

What if your permanent portfolio was just:

1. 25% in Philip Morris (PM) and Altria* (MO)

2. 25% in W.R. Berkley (WRB)

3. 25% in Franco-Nevada (FNV) and Bitcoin

4. 25% in cash

* Altria (MO) was spun out of Philip Morris in 2008. It is the U.S. product portfolio. To recreate the entire Philip Morris franchise, you should own both stocks.

If you held those investments for the last decade and you rebalanced the portfolio every month, you would have produced annual returns of just over 20% with a beta of less than half (0.48) the stock market, producing a Sharpe Ratio of 1.4.

You can see the result of this strategy below, for various time frames.

We’ve also compared monthly rebalancing to simply buying and holding these positions (not rebalancing). Not rebalancing will increase your returns but produces a worse Sharpe ratio as volatility increases (though it is generally still less volatile than the overall market).

What matters to me is this: Whether you rebalance monthly or yearly or not at all, this approach beats the market handily – despite allocating half of your assets to fixed income (via cash holdings and insurance companies).

That’s an astounding result.

There’s absolutely no better way to invest – nothing else comes close.

There’s no professional investor who’s capable of beating these numbers.

Thanks to inflation, this strategy is a one-way bet.

Horse, meet water.

P.S. If you’ve been following Erez Kalir’s work in our Biotech Frontiers, then I hope you noticed the huge move higher in Erez’s number-one conviction recommendation last night. It’s now up 84% since his most recent re-recommendation (full-position size) from last September. It seems likely that this will be the third time Erez has captured a 100% gain from this company since his first recommendation of this business in January 2024. I’ve never seen anything like this before in all of my years as an investor. Congratulations, Erez. You’re the best in the world at this kind of investing.

If you’re not already a subscriber to Biotech Frontiers, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on becoming a subscriber.

This Is NOT A Drill

For a limited time you can learn how to get pre-IPO exposure as Elon Musk commences his next trillion-dollar venture. And you can do it with any brokerage account.

Get the details completely free. But this video goes “dark” any moment now.

For the best shot at big gains, you have to get in ASAP — before it goes public.

Three Things To Know Before We Go…

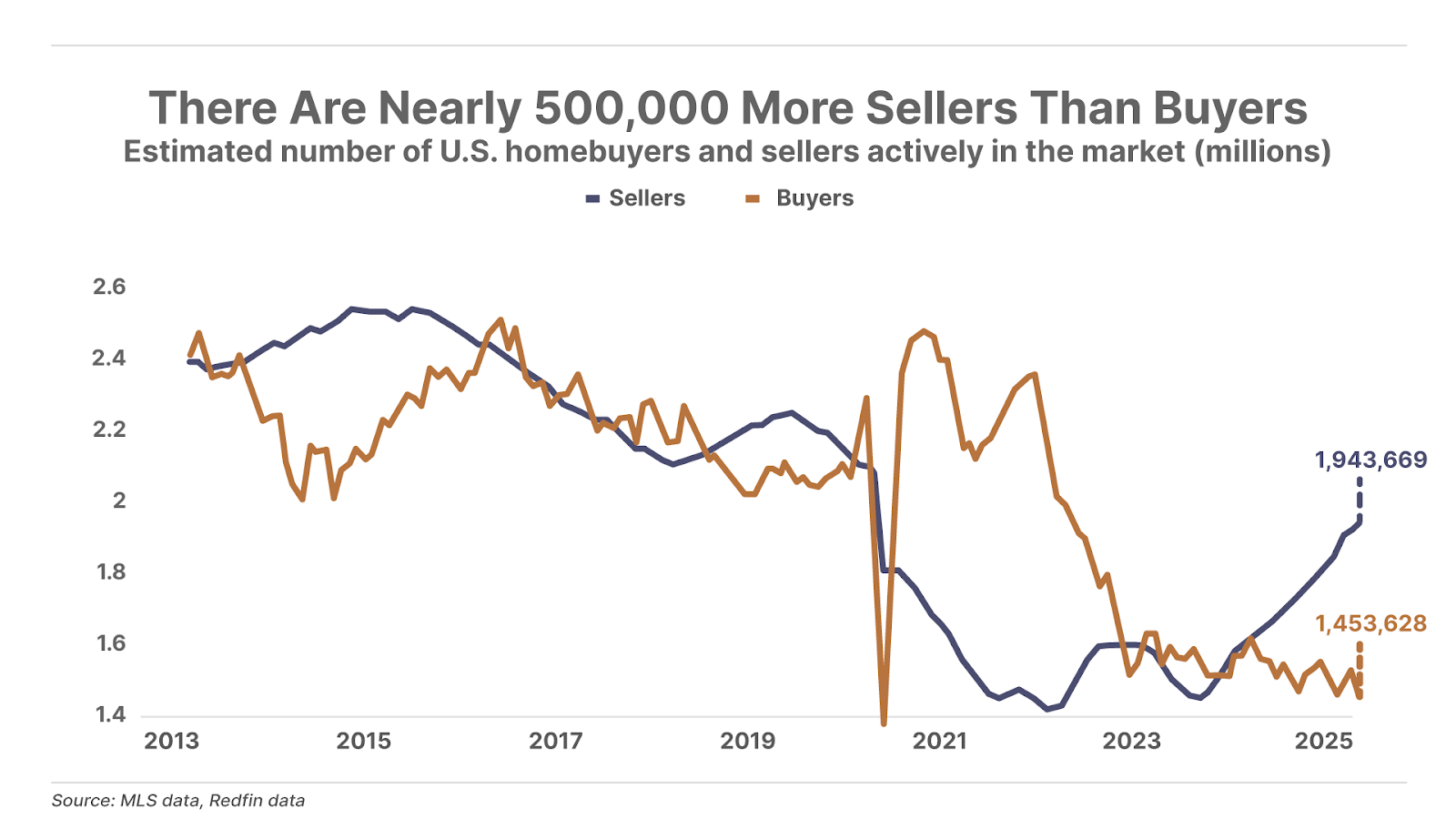

1. It’s a stagnant U.S. housing market. Sellers outnumber buyers by 34% in the U.S. housing market, according to data from Redfin. This is the widest gap between sellers and buyers since the online real estate brokerage firm began compiling the data in 2013. As a result, America’s housing market remains frozen as high borrowing costs (mortgage rates remain around 7%) and record high home prices keep buyers sidelined.

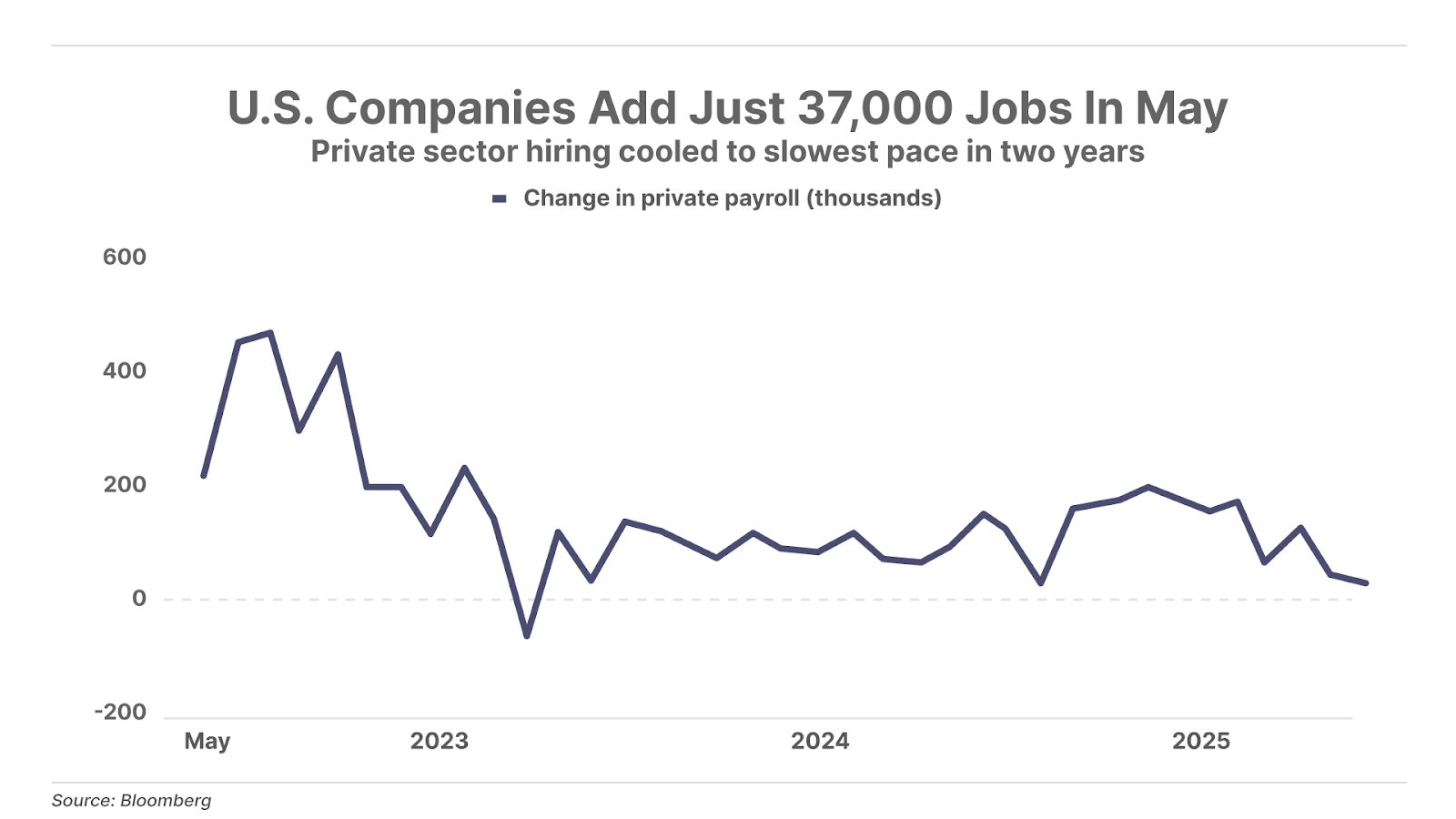

2. U.S. job growth slows to a two-year low. ADP private payrolls rose by just 37,000 in May – the weakest reading since March 2023 and well below Bloomberg’s consensus estimate of 114,000. In March, private payrolls rose by 147,000. That figure has dropped 75% in the two months since as companies scale back hiring amid growing uncertainty over President Donald Trump’s shifting tariff policies. Adding to concerns, all of May’s gains came from the travel and hospitality sector – which added 38,000 jobs – but those are largely seasonal hires ahead of summer. The broader trend is clear: U.S. job growth is losing steam fast.

3. Has Elon been reading the Daily Journal? Tesla (TSLA) and SpaceX CEO Elon Musk is suddenly sounding a lot like us. In a series of X posts yesterday, the (former?) head of the Department of Government Efficiency (“DOGE”) called President Donald Trump’s “Big Beautiful Bill” an “outrageous, pork-filled… disgusting abomination,” adding that it will “massively increase the already-gigantic budget deficit to $2.5 trillion (!!!) and burden America [sic] citizens with crushingly unsustainable debt.” Like us, he also pointed out that interest payments currently account for 25% of all government spending, and noted that if the government’s runaway spending continues, interest payments alone will eventually consume 100% of federal tax revenue. Repeat after us: the spending will never stop.

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.