Issue #129, Volume #2

Social Security Will Collapse By 2030 – Here’s How to Prepare

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| The End Of America… The signs are here and now… Social Security is a Ponzi scheme… Lost our AAA credit rating… World is selling the dollar… Young people can’t buy homes… What you can do… |

About 15 years ago, I wrote The End of America.

It was a 77-minute documentary that explained how America – the world’s most successful and prosperous country – was destroying itself. I explained, in detail, how our underlying financial problems (never-ending government deficits and the money printing required to finance them) would begin to cause serious and escalating social problems. This was long before Black Lives Matter, Occupy Wall Street, or Antifa began to terrorize our cities.

I explained the link between inflation and the collapse of civil society. Inflation creates massive disincentives for hard work and savings. It makes it vastly more difficult to cooperate effectively. And, as more and more people see their standard of living collapse in ways they can’t understand, societies fall apart. I predicted we’d see soaring amounts of prostitution (Only Fans), gambling (online sports betting), and drug addiction (fentanyl).

I also explained that, at some point soon, the “hidden” costs of inflation would explode. And on that day, everything you take for granted and love about America would end.

I predicted we’d lose our AAA-credit rating – and we did.

I predicted that our trading partners would soon abandon the dollar. Central banks now hold more gold than U.S. Treasuries.

And I predicted that as the dollar lost its world-reserve currency status, our standard of living would collapse. America would spiral into radical politics, soaring violence… and… eventually… a civil war.

We are at that point, right now.

And I can tell you what the final trigger will be: the collapse of Social Security in 2029.

Social Security will collapse before the end of this decade.

I’ll show you the exact numbers below. But, beyond the economics, the legal structures, and the specifics, what I want you to remember is that virtually every American fully believes that Social Security is something they are owed. They do not understand that there are no actual accounts. There are no investments. And there is no way anyone is going to survive on Social Security.

Let’s dive in.

The original 1935 Social Security Act (Title II) promised to provide a small annuity to elderly workers who paid into the system. The benefits were extremely modest. They were limited to people who had contributed to the system. And these payments – roughly $20 a month – were only available for people who were genuinely old. At the time, average life expectancy was just over 60 for men and 65 for women. Only 5% of Americans were even that old in 1935.

When FDR signed the 1935 Social Security Administration bill into law he specifically warned that this system wasn’t designed to cover everyone against the hazards of life:

We can never insure one hundred percent of the population against one hundred percent of the hazards and vicissitudes of life.”

But that hasn’t stopped Congress from trying.

Congress has added benefit after benefit while expanding access to the programs. Today 22% of Americans are entitled to Social Security. The Social Security Administration is currently sending checks out to over 60 million people. And these checks aren’t small anymore.

In fact, more than 30 million Americans receive all or most of their incomes from OASI – the old-age and survivors insurance program administered by the Social Security Administration. Average payment: $2,000 a month. Another 8 million people rely on Social Security’s disability insurance. Average payment: $1,600 a month. And then there’s the Supplemental Security Income program, which gives additional payments to 7 million blind and disabled people.

Whether you think it’s a good idea to give voters a mechanism to vote themselves the Treasury or not, the simple fact is that while Congress has been eager to buy voters, it never created any sustainable funding mechanism for these expenses.

As a result, Social Security is now the world’s largest Ponzi scheme.

The entire system is financed as a “pay-as-you-go” redistribution scheme. The problem is: there are now far too many beneficiaries and not nearly enough workers. In 1950, there were 16 workers supporting one beneficiary. Today, that ratio is down to 2.8 to 1 – if you include the 23 million government workers in America as “productive.”

When you look closely at the real numbers, you discover the real ratio is about 1:1.

There are only 57.6 million households in the United States that paid more than $10,000 in federal income taxes in 2022 (the most recent data available).

In other words, for every American household that’s engaged in meaningfully productive work… there’s at least one other person who is mostly or fully dependent.

Here’s a critical warning: if that productive household is you, nobody is going to “thank you for your service.” In fact, your fellow Americans are going to blame you and threaten you when the system collapses.

If you’ve seen people threatening to riot and steal because their SNAP benefits (food stamps) aren’t being paid because of the government shutdown, you’re getting a tiny taste of what’s going to happen when Social Security checks aren’t mailed out.

And here’s what most people don’t understand.

Social Security benefits, by law, can only be paid from the Social Security Administration Trust Fund (Section 201 of the Social Security Act (42 U.S.C. § 401).

The Commissioner of Social Security shall pay from time to time from the Trust Funds… benefits and administrative expenses… but only to the extent that such payments are made from moneys appropriated to the Trust Funds.”

When the Trust runs out of money, payments automatically drop to match incoming revenue – payments will be cut, massively.

Simple question: when will that occur?

SSA surpluses peaked in 2007, just before baby boomers started retiring. That year SSA saw almost a $200 billion surplus. And cumulatively, reserves “earmarked” to the Trust Fund peaked in 2009 at almost $3 trillion. But… since 2010 costs have exceeded the system’s income and more than $1 trillion has been cashed out of the system.

The core problem to the scheme is demographics. But a close secondary problem is none of your “contributions” were ever invested.

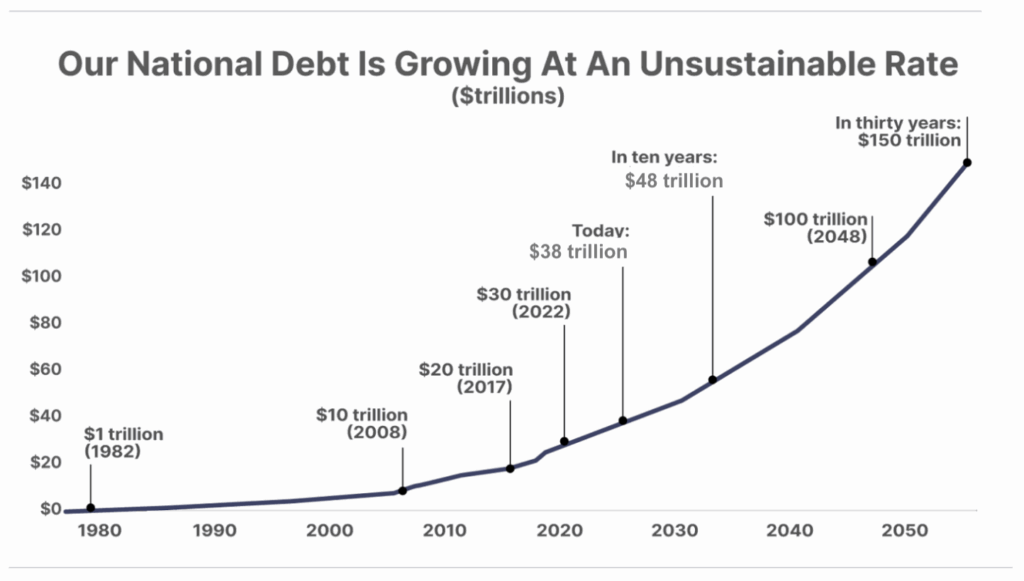

All the cash that’s been collected via payroll taxes was deposited into the Treasury’s general fund, where it has immediately gone out the door. All the Trust Fund’s “assets” are merely bookkeeping entries at the Treasury that “earn” a yield based on average Treasury rates. Last year that was about 2%. But the anemic returns aren’t the real problem. The real problem is the entity that’s promised trillions in future benefits is our government. And it is already $38 trillion in debt!

Today every dollar the Trust fund loses each year (about $200 billion last year) is a dollar that the Treasury must borrow in the credit markets. But where will the government find enough lenders as more and more central banks are selling Treasuries and buying gold?

By 2030, Social Security deficits will reach $500 billion a year. And the government’s other deficits will exceed $3 trillion – mostly because of soaring Medicare spending and interest costs. And then the Treasury has to find a way to refinance all of the existing government debts. When you do all that math, you get a total of around $40 trillion in financing needs over the next five years.

That’s $8 trillion a year, on average, that the government must borrow.

That’s 25% of GDP! Every year!

That’s not possible for the world’s largest economy. Keep in mind, the next largest debtor on that scale is Japan. Japan’s gross financing need is about 5% of GDP per year.

A huge reckoning is coming. And it’s going to happen a lot faster than anyone expects.

Last year’s Social Security Trustees report reveals current Trust Fund assets (earmarked at the Treasury) of $2.5 trillion. They currently expect systemwide deficits of “only” $250 billion next year. And they don’t see those deficits hitting $300 billion until 2029.

But these estimates are way off because they do not factor in the impact of rising inflation.

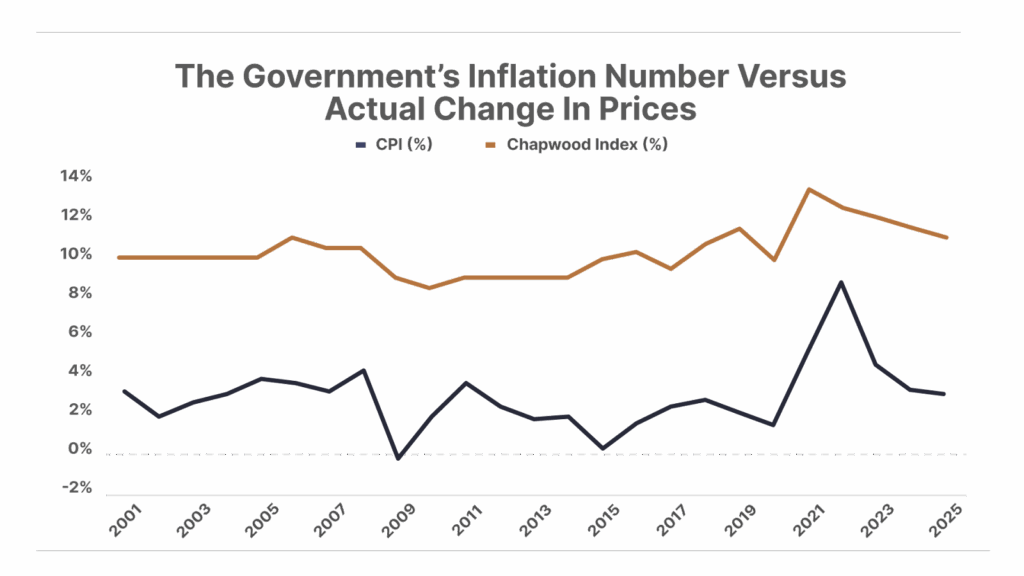

Maybe you’ve noticed that inflation isn’t going away. It’s nowhere near 2% that’s supposedly the target. Meanwhile, healthcare costs are soaring, which, along with tariffs (which will eventually cause much higher consumer prices), is going to drive CPI much higher than expected in 2026 and 2027. We already know from privately compiled data (see the Chapwood Index, for example), that actual inflation is running between 10% and 12% in most American cities.

As those kinds of numbers filter into SSA’s annual automatic cost of living adjustments, the system’s annual deficits are going to soar. If you assume 8% inflation, Social Security will run out of money by the end of 2030. And, if employment weakens, it will happen much faster.

What do you think will happen in 2029 when Social Security’s approximately 70 million recipients realize their benefits are about to be cut, automatically? And how will Congress provide more funding when it’s already having to print money to buy its own bonds every year because it cannot borrow 25% of GDP every year.

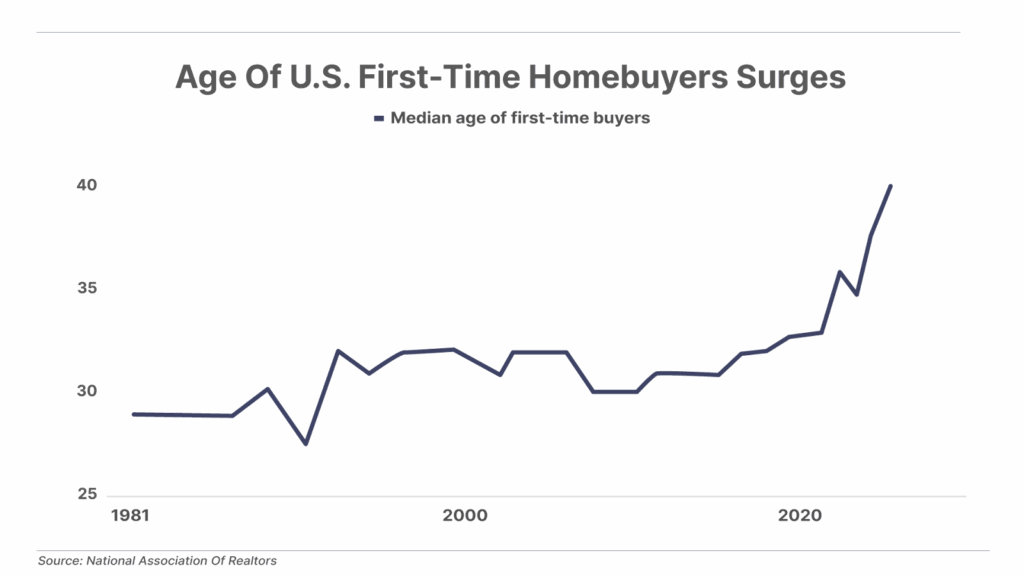

What do you think will happen over the long term as 25% of Americans try to vote themselves the paychecks of young people to make sure Social Security doesn’t collapse. Keep in mind, these are young people who can’t currently afford to buy a house.

There will be political violence like we’ve never seen in this country before.

New York City just elected a full communist mayor, mostly because college-educated people under 40 can’t afford to buy an apartment. Our economy is upside down because of out-of-control government spending and debt. And that means that life in America isn’t going to get better. It’s going to get a lot worse. And the collapse is going to happen a lot faster than anyone expects.

What’s the best way to protect yourself? Right now, I believe that’s by investing in energy. It’s cheap relative to technology and both demand from AI and inflation means that energy prices are inevitably going to move a lot higher.

If you don’t yet have exposure to our high-quality energy names – BWX Technologies (BWXT), EQT (EQT), Texas Pacific Land (TPL), Viper Energy (VNOM), Venture Global (VG), Core Natural Resources (CNR), I recommend you re-read those recommendations and consider how those businesses fit into your portfolio.

Pre-IPO Alert: The Next Tech Giant

Matt Milner just revealed how to grab a stake in the company behind ChatGPT before it hits the stock market.

He believes it’s racing toward a $1 trillion valuation — with explosive growth potential rivaling Google, Facebook, and Uber’s early investors.

⏳ Opportunities like this come once in a generation. Don’t miss out. Click here to watch Matt’s full reveal and learn how to position yourself today.

Three Things To Know Before We Go…

1. The debt spiral accelerates. U.S. national debt just surged past $38 trillion, two months after crossing $37 trillion and running a $5.1 trillion pace in new borrowing. The Congressional Budget Office projects total federal debt to reach $140 trillion by 2054, a level that would dwarf the productive capacity of the economy and the current M2 money global money supply today (roughly $100 trillion). The debt machine – and by extension the money printer – shows no sign of slowing; in fact, the pace is accelerating. Interest payments are consuming an ever-larger share of the federal budget, while bondholders are beginning to question the long-term sustainability of U.S. creditworthiness and the government’s ability to honor its obligations without perpetual monetization.

2. The Trump administration adds 10 new elements to the government’s list of “critical minerals.” The U.S. Department of the Interior has added uranium, copper, silver, metallurgical coal, and several other elements to the list of materials it deems critical to national security. Inclusion on the list increases the likelihood that these materials could be included in future tariff policies, and that related domestic projects may ultimately be in line to receive federal government support.

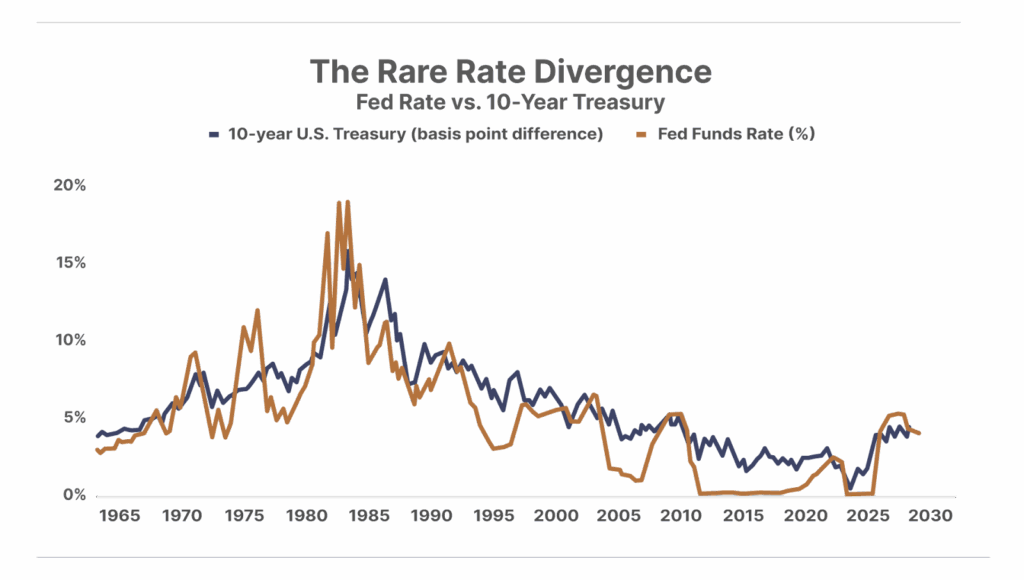

3. Diverging rates are unusual. The Fed cut interest rates by 25 basis points on October 29, and instead of also falling, as it almost always does, the rate on 10-year U.S.Treasuries rose 9 basis points that day… For context, the 10-year Treasury rate went down during the previous six phases of Fed rate-cutting. While the Fed controls short-term interest rates, longer-term bond yields are normally set by market forces. So this divergence of the 10-year rising while Fed rates fell is unusual. Longer-term bond yields’ opposite-way movement may reflect lingering fears of tariff-induced inflation. Also, the massive investments from overseas that President Donald Trump extracted in trade negotiations may create large demand for debt capital, exerting upward pressure on bond yields.

Tell us what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.