The Intersection Of Two Immense Forces Will Generate Extraordinary Wealth In The Years Ahead

Why Energy Is Our #1 Investment Theme for 2026

| This is Porter & Co.’s Complete Investor (formerly The Big Secret On Wall Street), our flagship publication that we publish every Thursday at 4 pm ET. We regularly provide to our paid-up subscribers a full report on a stock recommendation, and also an extensive review of the current portfolio… At the end of this week’s issue, paid-up subscribers can find our Top 3 Best Buys, three current portfolio picks that are at an attractive buy price. Every week in Complete Investor, we provide analysis for non-paid subscribers. If you’re not yet a paid subscriber, to access the full paid issue, the portfolio, and all of our Complete Investor insights and recommendations, please click here. |

It’s likely to be the single most important trend shaping the financial markets, the U.S. economy, and even the geopolitical landscape in the years ahead.

Yet few investors truly understand the implications today.

Wall Street and Main Street are too distracted, arguing over which company will “win” the artificial intelligence (“AI”) race (nobody knows)… whether tariffs are good or bad (they’re taxes, and they’re bad)… and whether stocks will soar or crash (it’s nuanced)…

Meanwhile, they’re ignoring one of the most powerful and inevitable investment trends in history… one that has the potential to deliver extraordinary returns over the long term for investors who are positioned correctly.

We’re referring to the convergence of AI and energy that is already well underway.

But to understand the magnitude of what’s coming – and why this is our top investment theme for 2026 – we first need to step back in time.

The Two Forces Driving Humanity

The long arc of human technological development has always been driven by these two forces: energy and intelligence.

Man’s discovery of fire and written language was the first epoch, leading to the emergence of civilization, innovation in tools and weapons, the development of religion, and to the establishment of centers of learning and memory, like at Alexandria.

Wood – to burn and build – fueled much of this growth. But by the 1600s, the English – one of the premier global powers of the time – were running out of trees. The English navy needed giant trees to make warships to defend their island nation. More directly, the scarcity of trees threatened human lives as the population grew and there wasn’t enough energy to cook food and heat homes.

So, the British developed coal mining. Beginning in 1600, shipments of coal into London grew exponentially from only 35,000 tons (when it was used by royalty to heat castles) to 467,000 tons in 1700 (up 1,234%) as it became London’s dominant fuel source.

The dramatic increase in coal production and usage in the 1600s was truly remarkable, and it made good economic sense: coal contains twice as much energy per pound as wood.

By 1800, following the introduction of the Newcomen steam engine in 1712 (to pump water out of coal mines), the United Kingdom was producing an astonishing 10 million tons of coal (+2,041% in 100 years) per year. Coal production would peak around 1900 at almost 300 million tons per year (+3,000% in 100 years). And with this energy, humanity flourished.

For almost a thousand years (between 100 AD and 1000 AD), London’s population remained around 50,000. It took another 500 years to double to 100,000 by 1500. It then doubled again in only 100 years, to 200,000, by 1600. But then, because of a lack of energy, the population collapsed.

Then came coal. And London’s population grew to 1 million by 1800, roughly four times more people than the city had previously been able to support at any point earlier. By 1900, 6.5 million people lived in London, making it the largest city in the world.

It’s remarkable that even now, 500 years later, coal is still the dominant source of energy in the world, and thus still the foundation of human life.

Over the last 22 years, more than 1.4 thousand gigawatts (“GW”) of new coal-fired capacity has come online, almost all of it in India or China. To put that in perspective, that’s more new coal-fired power in the last two decades than America’s total installed base of all forms of power generation (1.2 thousand GW).

Yet, despite all of this the world still doesn’t have enough energy. That’s because the demand for energy is endless.

Most people do not understand that the demand curve for energy and for intelligence do not follow classical economic models. There is never enough supply of either to satisfy demand.

All other commodities are disciplined by marginal utility. This is the idea that while one car, for example, can greatly increase your personal productivity, another car will not yield much, if any, increase to productivity and, therefore, isn’t worth as much to you.

But that simply isn’t true when it comes to energy or intelligence. Computer programmers, for example, discovered that no matter how much memory is built onto a chip, software designers will always use all of it – and still want more. Likewise, demand for electricity is simply endless. No matter how much electricity is produced, under peak demand, all of it will be used unless pricing restricts demand.

In short, when it comes to energy, demand always exceeds supply.

Societies that provision energy efficiently grow their wealth. Look at per-capita electricity production and you’ll find it is perfectly correlated to wealth – per-capita gross domestic product (“GDP”). Likewise, there is a very close relationship between electrical demand and computing per capita, too. And that relationship between electricity, computing power, and wealth is about to explode.

The AI Power Problem

In June 2024, Porter & Co. released a ground-breaking report entitled The Parallel Processing Revolution… Read it here if you have not already done so.

Now 18 months later, we believe this trend represents the most important shift since the invention of the computer itself. Instead of performing one task at a time, modern graphics processing units (“GPUs”) can perform millions of operations simultaneously, working in parallel… unlocking colossal computing power.

Parallel processing is what has made AI possible. It’s why computers can now recognize images, write code, drive vehicles, converse with humans, and simulate the physical world with startling accuracy.

But here’s the part everyone is missing… Parallel processing doesn’t just multiply intelligence. It also multiplies energy demand. Exponentially.

A single modern AI server rack can draw 10 to 20 times more power than a traditional data-center setup. That means a single GPU-driven data center – running up to hundreds of racks at once – can consume as much electricity as 50,000 homes. Multiply that across hundreds of data centers, across dozens of states… and you begin to see the massive problem barreling down on us. And the more powerful these chips become, the worse it gets.

Because remember: “intelligence” is not constrained by diminishing marginal utility. The more compute power available, the more we will use, and the more we will demand. This means energy demand will continue to rise.

The energy demand from parallel processing is already unlike anything we’ve ever seen before.

There are currently more than 500 new GPU-driven data centers planned across the U.S. When complete, these facilities could consume nearly 9% of total U.S. power capacity.

In short, we are facing a massive electrical power crunch over the next several years.

Where Will All This Electricity Come From?

There’s lots of talk and investment into solar panels and wind turbines, but they simply cannot meet this challenge. At least not alone, and not in time.

Despite $10 trillion invested globally in alternative energy, neither wind nor solar provide even 2%of global energy production. Hydrocarbons – oil and gas, the dreaded fossil fuels – still supply more than 80% of the world’s energy – roughly the same percentage as 30 years ago.

The fundamental problem is intermittency. Wind and solar are weather-dependent. As U.S. Secretary of Energy Chris Wright put it in a recent interview, relying on wind and solar for baseload power is like ordering “an Uber that you don’t know when it will show up, or where it will drop you off.” No consumer would pay for such a service. Yet the U.S. grid currently pays a premium for it.

Data centers cannot tolerate this uncertainty. They require 99.999%-plus reliability – 24 hours a day, seven days a week, 365 days a year. Solar panels don’t work at night. Wind turbines don’t spin when the air is still. And battery storage at the scale required remains economically prohibitive.

Daniel Yergin, Vice Chairman of S&P Global and one of the world’s foremost energy experts, recently explained that what we’re experiencing is not an “energy transition” but rather an “energy addition.” Yergin also notes that energy transitions historically take a century, not years or decades. And previous shifts – from wood to coal, from coal to oil – never fully replaced the old source.

Renewable energies are a blip at the moment – they may slowly increase their contribution over time, but for now they are a sideshow, even a distraction.

The reality is clear: the Parallel Processing Revolution can’t proceed without hydrocarbons. The only question is which ones, and for how long.

Natural Gas Is Likely To Be the Biggest Winner

If you want to understand where the smart money is flowing, consider this: Ken Griffin’s Citadel made a $1.2 billion investment into natural gas last year.

Griffin is arguably the smartest investor of the last 40 years. He started doing quantitative trading in his Harvard dorm room in 1987, turned $250,000 into $13 million by graduation, and has since produced 20% annualized returns while generating more than $125 billion in profit for his investors.

Griffin’s Citadel employs over 300 PhDs in computer science and data analytics. Their securities trading business handles about 40% of all retail investor trades, giving them unmatched real-time market intelligence. When Citadel makes a move this significant, it’s worth paying attention.

And their models are telling them what we’ve been saying for years now: demand for American natural gas is going to soar.

Here’s why.

In 2024, of all the fossil fuels, natural gas saw the strongest demand growth at 2.7% – an increase of 115 billion cubic meters versus an annual average of about 75 billion cubic meters. This wasn’t a one-time spike. It’s the beginning of a structural shift.

And look where that demand is coming from – natural gas currently provides more than 40% of data center electricity. That percentage is growing rapidly….And unlike heating demand, data centers never turn off. There’s zero seasonal flexibility.

The demand picture gets even more dramatic when you factor in liquified natural gas (“LNG”) exports.

In 2024, LNG exports totaled 11.9 billion cubic feet per day (“Bcf/d”) and consumed 11.5% of total U.S. production.

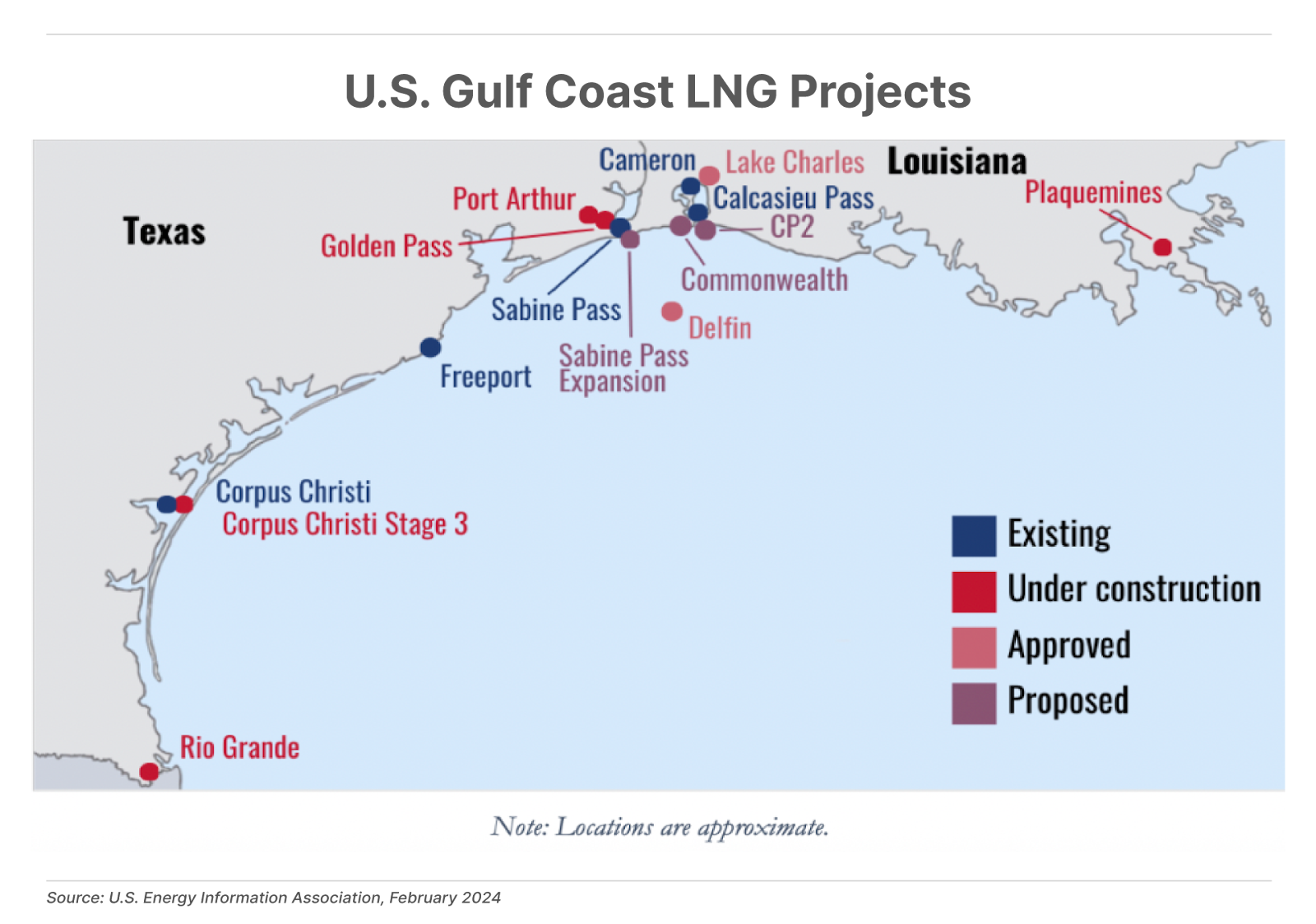

There are currently seven major LNG construction projects near completion or underway in the U.S: ExxonQatar’s Golden Pass (Texas), Venture Global’s Plaquemines (Louisiana), Cheniere’s Corpus Christi Stage 3 (Texas), NextDecade’s Rio Grande (Texas), Sempra’s Port Arthur (Texas), Venture Global’s CP2 (Louisiana), and Energy Transfer’s Lake Charles (Louisiana).

When completed, these facilities will add another 18 Bcf/d of export capacity, taking total export capacity to 30 Bcf/d – or roughly 3x current levels. That’s more than the entire U.S. electrical generation sector uses today.

Thus, by 2030, LNG exports plus AI compute energy demand will consume over 50 Bcf/d of natural gas – roughly half of total U.S. production. Supply is expected to grow, at most, by 10%.

Given these factors, we’ll likely see natural gas trading above $10 per MMBtu (million British thermal units) by 2030 – it’s currently less than $4. And when there are significant demand spikes in the winter, we could easily see prices temporarily jump to as high as $50 per MMBtu.

Coal Is Making A Comeback

Coal’s share of U.S. electricity generation has fallen from 51% in 2001 to about 16% today – and that decline is unlikely to reverse anytime soon.

But here’s what is happening: the planned retirement of coal plants is increasingly being delayed or halted entirely.

The U.S. currently has approximately 190 GW of operational coal-fired capacity. According to S&P Global, since the start of 2023, plans to retire nearly 40 GW of coal capacity – roughly one-third of all previously announced coal retirement capacity – have either been delayed or avoided through planned conversions to gas-fired generation.

Meanwhile, the Trump administration has invoked emergency powers to keep some coal plants running. Speaking at an event last September, Energy Secretary Wright said the administration had been in contact with many utilities across the U.S. and expects that the majority of coal-fired plants slated for retirement over the next few years will delay closure.

The logic is straightforward. Retired coal plants offer something that no new construction can match: immediate, cost-effective infrastructure. They already have heavy-duty transmission lines, substations, pre-zoned industrial land, and community familiarity with large-scale operations. Building equivalent infrastructure from scratch would cost hundreds of millions and delay projects by years.

This is why Amazon (AMZN), Alphabet (GOOG), and Microsoft (MSFT) are all investing in sites previously occupied by coal facilities.

There’s also potential to temporarily expand coal-powered production significantly in the near-term if needed. According to James Grech, CEO of coal-miner Peabody Energy (BTU), U.S. coal plants are currently using only about 42% of their maximum capacity, compared to a historical average of 72%.

As Secretary Wright put it:

If we want to grow America’s electricity production meaningfully over the next five or 10 years, we’ve got to stop closing coal plants.”

Oil: The Overlooked Beneficiary

While crude oil plays a negligible role in direct electrical generation in the U.S., it is still likely to benefit from the acceleration of the Parallel Processing Revolution. That’s because petroleum is woven through every layer of AI’s infrastructure.

Start with the hardware itself. Petrochemicals derived from crude oil are essential inputs for the plastics, resins, lubricants, and coolants used in AI systems. Every circuit board, GPU casing, server rack, and cooling system contains oil-based materials. Without petroleum-derived feedstocks, the global rollout of AI infrastructure would be impossible.

Then there are logistics. Semiconductors manufactured in Asia, servers assembled across multiple regions, and data-center materials shipped worldwide all depend on oil-fueled ships, aircraft, and trucks. The supply chain that makes AI possible runs on diesel and jet fuel.

And here’s something most people don’t realize: data centers rely heavily on diesel backup generators to ensure uninterrupted operations. These generators are critical for guaranteeing near-perfect reliability. Though they run only occasionally, their scale across thousands of facilities translates into meaningful oil consumption.

In addition, in some parts of the world – including the Middle East, Africa, and small island nations – oil-fired power plants remain central to electricity generation for data centers. And even here in the United States, “peaker” plants – oil-fueled plants that were traditionally only used to supplement baseload power during periods of peak demand – are increasingly being pressed into service to meet surging AI demand.

A recent Reuters analysis found that about 60% of the power plants slated for retirement in the PJM Interconnection – the largest Regional Transmission Organization (“RTO”) in the U.S., which operates the electrical grid for 13 states and Washington, D.C. – postponed or cancelled those plans in 2025. And most of the plants averting shutdowns were peaker units run on oil.

Again Energy Secretary Wright sees this as just the beginning:

There are a ton of peaker plants that could operate more. The biggest targets are spare capacity on the grid today.”

While peaker plants currently contribute about 3% of the country’s power, they have the total capacity to produce 19%.

Altogether, in 2025, AI-related oil consumption – including oil-fired electricity, diesel backup, petrochemical feedstocks, and logistics – accounted for approximately 1.4 million barrels per day (“bpd”), or about 1.4% of global demand.. By 2030, projections suggest this figure could rise to nearly 5 million bpd – equivalent to as much as 5% of worldwide consumption. At an assumed oil price of $80 per barrel, AI-related oil spending could reach nearly $150 billion by 2030.

This doesn’t make oil a primary beneficiary of the AI boom. Natural gas and coal will capture the lion’s share of new power demand in the near-term. But oil deserves a place in the conversation – not as a growth story, but as yet another “old economy” sector that’s being pulled back into relevance by the insatiable energy demand of AI.

Nuclear: The Long-Term Solution

But while natural gas and coal will bridge the immediate gap, the ultimate solution for powering the AI revolution is nuclear energy.

The energy density is simply unmatched. A 10-gram uranium pellet – about the weight of a peanut – releases as much energy as burning 4,350 gallons of oil, 22 tons of coal, or 590,000 cubic feet of natural gas. Nuclear fuel contains 1.5 million to 2.5 million times more energy per unit of mass than fossil fuels.

For data centers, nuclear offers the perfect profile: reliable baseload power, operating 24/7 regardless of weather conditions, with capacity factors exceeding 92.5%. Nuclear plants can run 18 to 24 months between refuelings, with planned outages lasting only a few weeks. Some advanced reactor designs aim to operate 10 years without refueling.

The tech giants have already noticed – and acted. In 2024, global private investment in advanced nuclear companies surpassed the combined value of such deals over the previous 15 years.

Microsoft signed a 20-year power purchase agreement with Constellation Energy to restart Three Mile Island Unit 1 – a $1.6 billion project set to generate 835 megawatts (“MW”) of carbon-free electricity exclusively for Microsoft’s data centers by 2028.

Google has announced partnerships aimed at bringing gigawatts of nuclear capacity online by 2030.

Amazon purchased a Pennsylvania data center that draws power directly from an adjacent nuclear plant and is investing heavily in small modular reactor (“SMR”) technology.

The U.S. Department of Energy (“DOE”) is also supporting restarts of the Palisades plant in Michigan and Duane Arnold in Iowa. Restarting an existing nuclear plant costs approximately $1 billion to $2 billion for nearly 1 GW of capacity – far cheaper than the $37 billion required for a new plant of similar capacity.

There’s also significant potential in converting retired coal plants to nuclear power. According to Deloitte, 128 to 174 GW of nuclear capacity could be retrofitted at operating and retired coal plants, with capital expenditure savings of 15% to 34%. At least 11 states have publicly expressed interest in this approach.

But SMRs represent the next frontier. With capacity up to 300 MWs, they offer greater flexibility and can be deployed on smaller sites. Their modular construction and standardized components help reduce costs and shorten timelines.

But here’s the crucial caveat: widespread commercial deployment of advanced reactors is likely to arrive no earlier than the 2030s at best. Licensing, demonstrating, and deploying new designs takes years, so the industry will have no choice but to rely on “dirty” energy in the interim.

Our #1 Theme For 2026

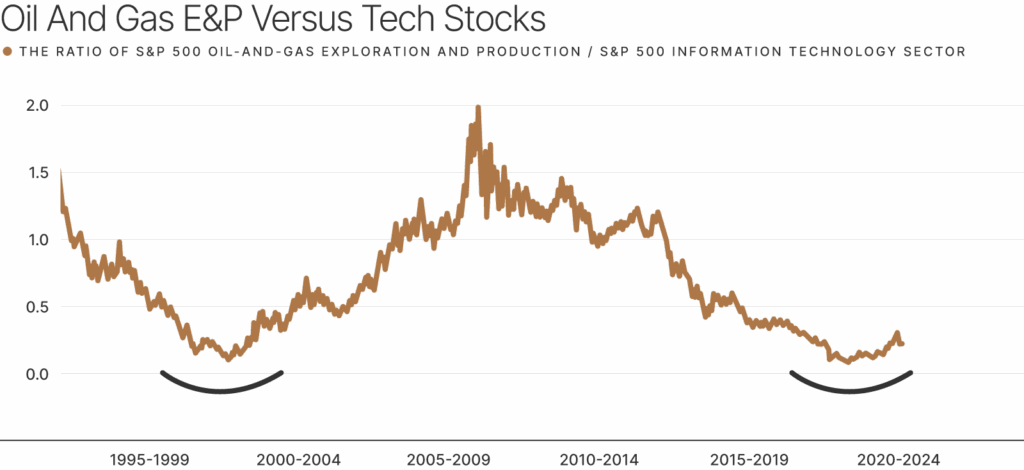

The last time the setup for energy looked this compelling was the late 1990s. As Wall Street chased internet stocks, it ignored “old economy” sectors like energy. By the peak of the dot-com bubble, the energy sector was historically cheap – the direct inverse of the overvaluation in the tech sector.

When the bubble finally burst, there was a massive mean reversion that resulted in many energy stocks exploding in value.

Over the following decade – as shown in the chart above – these stocks not only beat tech stocks by a wide margin, but also outperformed the broader market. And contrarian investors who defied the “herd” and bought energy stocks at their historically low valuations made an absolute killing.

Big, blue-chip stocks like ExxonMobil (XOM), Chevron (CVX), and ConocoPhillips (COP) gained well over 1,000%, while many smaller energy companies soared even more.

We believe the stage is now set for a similar opportunity. Except this time, the potential returns could be even greater.

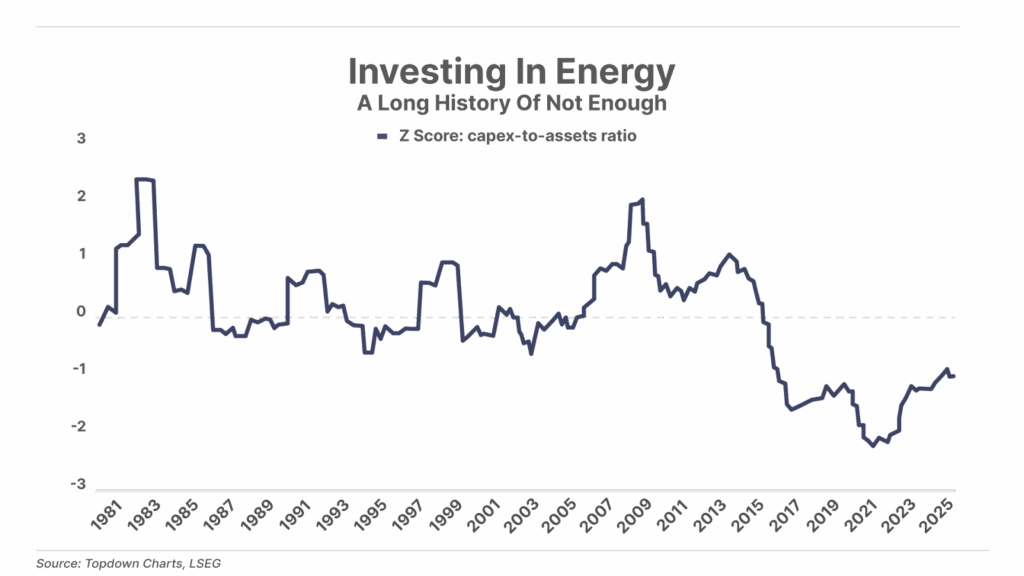

Not only has the energy sector been suppressed for years due to anti-fossil-fuel rhetoric and political pressure, but investment in new facilities, new exploration, and new drilling was massively suppressed by environmentalists.

And though energy capex has rebounded from its 2022 lows, it still remains historically low. In fact, as the chart below highlights, on average, energy companies still aren’t even investing enough to maintain their current production, let alone grow it.

And again, this is happening at a time when the world is demanding more energy than ever before.

This structural supply and demand imbalance suggests energy prices must move higher – and potentially much higher – from here.

Yet, as tech stocks trade at unsustainable, nosebleed valuations, energy stocks are still downright cheap… the broad energy sector is trading 40% below its 10-year average price-to-earnings (“P/E”) ratio.

We don’t expect this to last… As the impact of the supply-demand imbalance becomes clear – and the world begins to understand that the Parallel Processing Revolution is here to stay and thus requires more cheaper energy – we expect the under-valued energy sector will soar.

Fortunately, Compete Investor subscribers are in a perfect position to benefit from this trend.

If you are not yet a fully paid-up subscriber to Porter Stansberry’s Complete Investor, click here to learn how to become one… providing access to new recommendations, past issues, the full portfolio, the latest Best Buys, the editorial Roundtable, and more.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.