Issue #88, Volume #2

The Insurance Company That’s Becoming An Elite Compounder Of Capital

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| What’s going on with our P&C stocks?… AXIS Capital found a replacement genius in Vince Tizzio… Loss ratios and expense ratios are down… BLS releases a grim jobs report… |

Editor’s note: Long-time subscribers know that I (Porter) take my summer vacation in August. Next week, I’m fishing with my two older sons (Traveler, 17, and Seaton, 14) in the world’s biggest fishing tournament, The White Marlin Open. The total purse should be around $7 million this year – wish us luck. The following week, I’m hosting some pro golfers and members of our Meadowdale Fellowship at my farm for the BMW Championship. And the third week of the month, I plan to fish in the other major marlin tournament, The MidAtlantic Billfish Tournament. So a busy and fun month is coming up for me. While I take a “break,” you’ll hear from Porter & Co.’s other leading analysts – Ross Hendrick, Martin Fridson, and Erez Kalir. I hope you’re enjoying the summer and I’ll see you in late August. (If you want to follow along for the fishing and the fun at the BMW Championship, please follow me on X.com. I’m @porterstansb)

As our paid-up subscribers know, we recently recommended another property and casualty insurance (“P&C”) company, AXIS Capital (NYSE: AXS).

As we proved last week in our first-ever Big Secret On Wall Street report card, our work on P&C is the most valuable research we produce – although I’m sure Marty Fridson (Distressed Investing) and Erez Kalir (Biotech Frontiers) would take exception to that claim.

But, let’s not get bogged down on which track record is actually the best (it’s Erez).

In P&C insurance, our average return has been 66% over the last three years, with an average holding period of about 18 months. That’s more than double the S&P 500’s returns over matching periods. And we had no losing positions.

Given these firms’ extremely low volatility and the security of their huge balance sheets, that’s an astounding investment performance. (In the background, just imagine Marty and Erez rolling their eyes…)

Our P&C research practice began back in 2012, while still at Stansberry Research. By 2014, we’d created our own proprietary industry model. Since then, using that model and buying the top 10 stocks as it ranks them has created 26% average annual returns. That’s an extraordinary, long-term track record – about twice the S&P 500.

(That model, by the way, is still in use at Stansberry Research, my former company. If you’re a Stansberry subscriber, you can access that model by looking under the “Tools” menu on the Stansberry homepage and selecting “Stansberry Monitors.” The “Insurance Value Monitor” contains the output of the industry model.)

I think we can beat the model at Porter & Co for two reasons.

First, the model’s rankings are based on 10 years of data. As a result, the model will miss new, high-performing companies, like Kinsale Capital (NYSE: KNSL), until they have 10 years’ worth of results to analyze. Likewise, it will also miss the rapidly improving results of an existing business going through a successful turnaround, like AXIS Capital, which is currently ranked number 20.

Second, the model does a poor job of recognizing the rare P&C company that can both deliver incredible underwriting and massive policy growth. That’s led the model to mis-rank Progressive (NYSE: PGR) for many years.

I’m not saying the model isn’t valuable – it is extraordinarily valuable. I’m saying that there will be some opportunities that the model misses. That’s why having a person who really knows the industry and who has followed it for decades can still add value.

Lately though, it sure doesn’t seem like I’m adding any!

Over the last month, AXIS has fallen almost 10%. While that’s not a huge move, it is a pretty big monthly drawdown for a company that has a beta of 0.82. (Beta is a measure of a stock’s monthly volatility, relative to the S&P 500, which has a benchmark beta of 1.0. AXIS is almost 20% less volatile than stocks in general.)

And, it’s not the only P&C stock that’s seen a pullback. The industry’s exchange-traded fund, Invesco KBW Property & Casualty ETF (KBWP), is off almost 6% over the last month. Kinsale, our top pick in the industry, is off 7%. And Progressive is down 9%.

So what’s going on? I’ll give you my thoughts below on what’s happening.

But, first, I want to update everyone on the turnaround at AXIS. This is a story worth telling.

The very best P&C companies have always been created and led by geniuses. Like Warren Buffett. And Bill Berkley of W.R. Berkley (WRB). These are a rare breed of men who understand all the odds… and then figure out how to beat them. They find new ways to underwrite risks like no one else can.

And there was no bigger, more swashbuckling insurance genius than AXIS Capital’s founder, John Charman.

Charman made his first fortune in the early 1990s, offering risk insurance on a 24-hour basis during the first Gulf War. He is a living legend. Inside the industry and in London’s business press, he’s known as the “King of the London Insurance Market.”

But he’s also something like Darth Vader. Employees loathe him because he forbids entertaining clients on the company dime and criticizes employees who take lunch breaks. He once had to settle with a female executive who brought a discrimination complaint. Charman had barred her from a meeting, saying, “We are discussing something we decided while you were having a baby.”

Today, Bermuda, where AXIS is headquartered, is the center of the P&C insurance industry. Bermuda-based insurance companies serve over 150 countries, with over $128 billion of premiums written yearly.

I need to digress a bit here, because AXIS wouldn’t exist today if it wasn’t for the man, Bob Clements, who created the entire Bermuda insurance hub.

In the early 1980s, Clements was the head of Marsh & McLennan – one of the world’s largest insurance brokers. He was looking for a jurisdiction that would treat insurance companies favorably and met with Bermuda’s regulators to create the perfect legal, tax, and regulatory environment. Then, in 1985, he created, from scratch, the world’s leading insurance company, ACE Limited. He’d later launch XL Capital, Mid Ocean Re, and Arch Capital. But ACE Limited was Clement’s biggest and best creation. It was backed by 34 corporate shareholders, including Marsh & McLennan (MMC) and JPMorgan Chase (JPM).

Although you’ve probably never heard of it, ACE Limited is still one of the world’s leading insurance companies. Why haven’t you heard of it? Because today it’s called Chubb. ACE Limited acquired Chubb in 2015 (for $28 billion) and kept its brand.

Buffett has been acquiring shares of Chubb (CB) consistently since the spring of 2023 and now (as of the most recent disclosures) owns about 27 million shares, or 6.7% of the company. I suspect that, sooner or later, Berkshire Hathaway will buy 100% of Chubb.

What does all of this have to do with AXIS Capital and John Charman? In the late 1990s, Charman was ready to sell his first insurance business, Tarquin. Guess who bought it? ACE Limited, in Bermuda, for more than $500 million. And what do you think happened when a rebellious genius – “the King of the London Insurance Market” – went to work for one of the largest insurance companies in the world, with its slew of corporate shareholders? Charman was fired in 2001.

The timing was fortuitous: 9/11 happened only months later. The destruction of so much of Manhattan created unprecedented insured losses. The claims rocked the Bermuda-based insurance industry. But it also created an incredible “hard market,” for property insurance. (A hard market occurs when premiums rise substantially because of perceived risks and weaker players exit.) Charman used the high premiums to launch AXIS in 2002 and it was immediately successful.

In its first full year in business, AXIS wrote $1.1 billion in premiums. By the next year, AXIS’ premiums more than doubled to $2.3 billion. And by 2015, AXIS had doubled again to annual premiums of $4.6 billion.

Writing premiums isn’t the hard part. Avoiding losses is much tougher. AXIS did both… at first.

Trouble arose from an unlikely source: Charman’s aggrieved spouse. Charman left his wife in 2003 after 28 years of marriage and moved to Bermuda. After offering his wife a $40 million settlement, he was famously outraged when instead of settling with him, she went to court and was awarded the largest divorce settlement of all time in London. To meet this obligation in full in 2007, Charman was forced to sell most of his AXIS shares (although he still owns about 3% of the company). No longer the controlling shareholder, he resigned the next year (2008).

What happens when a temperamental genius leaves his own company? (Ask me how I know…) AXIS’ profitability declined almost immediately. By 2015 its combined ratio (that’s its loss ratio + its expense ratio) was over 95% – which is far from elite. Its earnings growth stalled. And so did its share price.

What was the problem – what’s always the problem in insurance? Underwriting.

Rather than growing its business through “primary” insurance, which it could carefully underwrite, AXIS had been taking on more and more “reinsurance,” where other companies had done the primary underwriting work.

What’s the difference? Primary insurance in lines like excess & surplus (“E&S”) is virtually unregulated and typically bespoke. It’s much more profitable – when done right. Reinsurance is essentially a commodity business.

By the early 2020s, AXIS’ board wanted a complete restructuring of the business. It wanted to get out of reinsurance and to focus on high value specialty insurance.

To do that, they needed another genius. And they found one. They hired Vincent Tizzio as CEO in the spring of 2023. Tizzio was executive vice president and head of global specialty insurance at The Hartford (HIG), where he’d built a huge business in specialty insurance. He got that job because he’d previously served as CEO of Navigators Management for seven years, where he’d done the same thing – built a huge and profitable specialty insurance practice.

Under Tizzio’s leadership, E&S specialty insurance became AXIS’ primary focus. At AXIS, E&S means coverage for high-risk exposures that standard insurance carriers won’t cover. Globally, E&S was a $73 billion market in 2023. AXIS sees the market growing to $150 billion by 2030. That’s double-digit growth through the end of the decade.

AXIS only has a 2% market share in E&S currently. That gives it a long runway ahead. (This is, by the way, the same strategy that Kinsale was founded to pursue.)

When Tizzio took the helm, he saw that AXIS had under-reserved for future policy claims. AXIS took a $630 million reserve charge in 2023. And to further remove large, “long-tail” risks AXIS executed a loss portfolio transfer (“LPT”) deal with Enstar at the end of 2024. AXIS offloaded $2.1 billion of reinsurance reserves for policies written in 2021 or earlier.

Now Tizzio has a clean slate.

In 2015, AXIS’ business was roughly evenly split between the commoditized reinsurance segment and its primary insurance. But with its shift away from reinsurance in recent years, this segment now only makes up about 27% of premiums while primary insurance is the major revenue contributor at 73%. The result? Big improvement to underwriting profits.

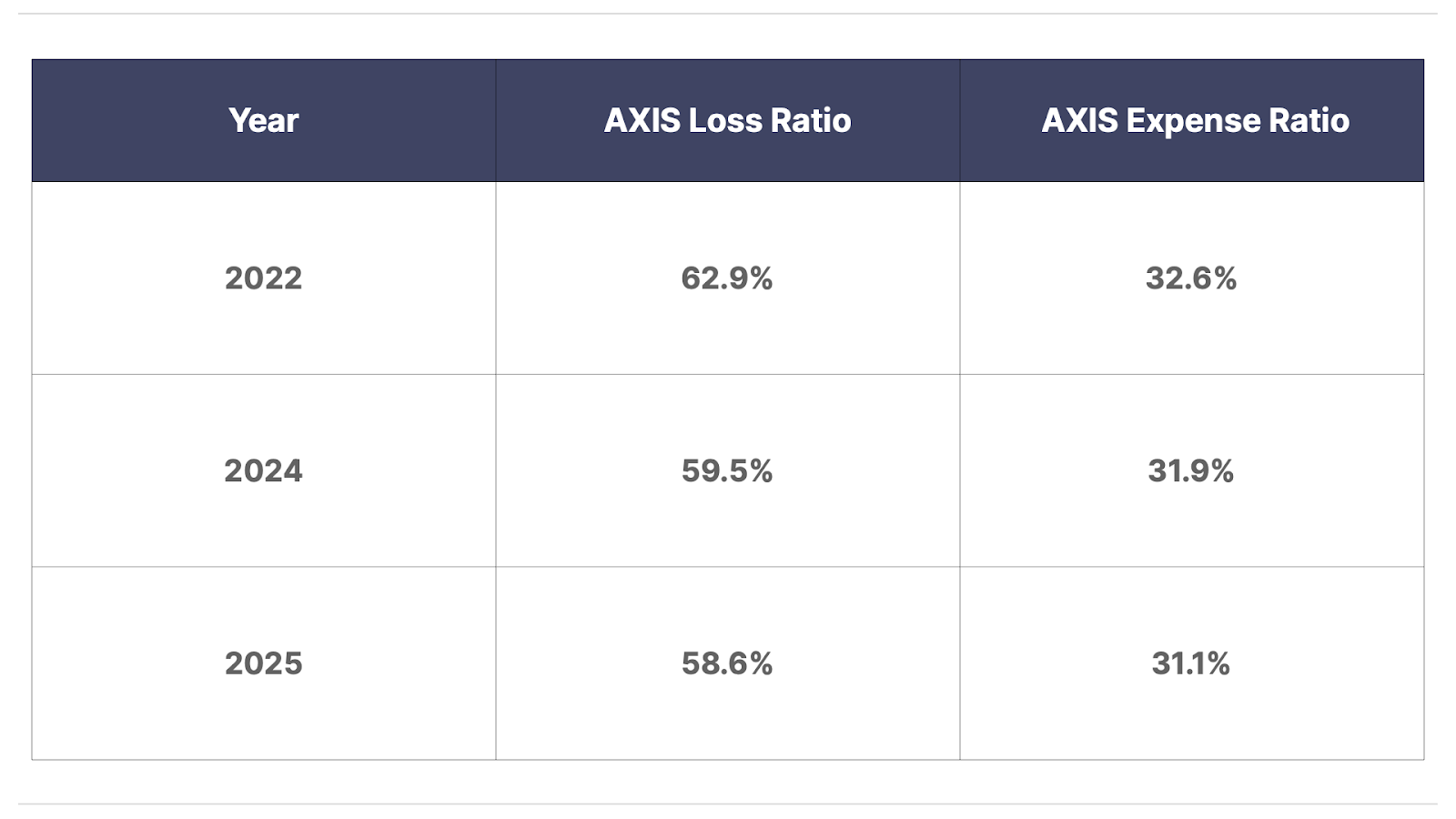

AXIS posted a loss ratio of 62.8% in 2022. But by 2024 its loss ratio was down significantly to 59.5%. And in Q1 of 2025 losses came down even further to 58.6%. With a smaller, but higher margin business, expenses should fall too. AXIS’ expense ratio was 32.6% in 2022. By 2024 the expense ratio was down to 31.9%. And in Q1 2025 it hit a new low of 31.1%.

AXIS released very good Q2 results on July 29.: the turnaround is on track and the company’s core results continue to improve. Its primary insurance segment posted an all-time high in premium volume ($1.9 billion) and an outstanding 85.3% combined ratio. Loss ratio continued to improve, at 55.9%. This is a dramatic turnaround that puts AXIS’ primary insurance unit into the range of elite insurance firms. (Kinsale’s Q2 loss ratio was 55.1%.)

Net income for the quarter was $216 million ($2.72 per share) up from $204 million ($2.40 per share) last year (up 13%).

I believe you’ll see AXIS’ stock “re-rated” higher over the next few quarters. Its current P/E is only 9. With a return on equity near 20%, it should trade at 15x or higher. And the AXIS board knows it: In February it authorized a $400 million share buyback. By June there was only $110 million in shares remaining under that authorization.

Since Tizzio took over, share buybacks have gone from $23 million in 2023, to $215 million in 2024, and – my estimate – $400 million in 2025. With about $150 million in cash dividend, that’s $550 million in capital return in 2025 (7.5% cap return yield).

I believe that AXIS is becoming an elite “compounder” that will continue to buy back substantial amounts of shares. Most of the market won’t recognize what’s happening for a while, but that won’t last for long. AXIS is a great stock for people who want market-beating returns and need an investment you can safely “set and forget.” I’d recommend selling puts at 5% to 10% below the market every month and just buying shares when you get put stock. It’s boring. But it works.

But wait, Porter, didn’t you just say that these stocks have all been selling off – why would we buy shares now?

Well, it’s my belief that buying great businesses when their shares are down is a good strategy. Makes sense, doesn’t it?

Right now there are two things that are plaguing these companies.

First, there’s a general concern that lower short-term interest rates are coming. Insurance companies hold huge bond portfolios. Their investment results are, for the most part, tied to relatively short-term (usually three-to-five-year) interest rates. Whether lower rates actually materialize or not, this isn’t a big concern for me because the firms are great bond investors and will manage around the yield curve to continue to produce good earnings.

The second issue is more substitutive.

Steve Eisman (the short seller who was featured in the Michael Lewis book and movie The Big Short) recently featured Brad Safalow on his podcast. Eisman is widely followed by hedge funds and family offices, which can bring a lot of attention to his content. Safalow, who is an advisor to hedge funds, has a short thesis on Kinsale. He’s been recommending investors short Kinsale since last fall – at $440 per share. And after Kinsale’s fantastic earnings report last week, being short KNSL shares has become a lot more painful. So he’s making the rounds trying to convince people that Kinsale’s results aren’t sustainable.

The crux of his argument is that the market for E&S premiums is going to “soften” and that, sooner or later, there’s going to be another “earthquake” that wrecks the industry. He thinks Kinsale, as an insurer of “last resort” for risky policies, will face margin compression when rates fall and claims rise. As evidence, he points to Kinsale’s declining growth rate.

Kinsale’s premium growth has indeed slowed from 50%+ in 2021-2023 to around 20% in H1 2025. And, yes, of course, the market for insurance premiums is somewhat cyclical. E&S is softening with 5% to 10% rate discounts and increased competition according to industry reports (Burns & Wilcox). And, with an industry-leading P/E ratio (26x), Kinsale does trade at a wide premium to its peers.

But none of this is new. You could have made all of these same arguments at any point in Kinsale’s decade-long ascension to the top of the industry. Why is Kinsale one of most expensive P&C stocks? Because along with Progressive it’s the best. In the most recent quarter it crushed estimates: gross premiums up 22.2% (+8.2% beat), combined ratio 75.8% (much better than 77.7% expected), and its annualized return on equity (“ROE”) was 32.5%, which is roughly twice the other top companies in the industry.

These stocks are always at risk for a 20% to 30% decline because of catastrophic events, like California’s wildfires. But, once again, this is why quality matters so much in this sector. Arch Capital lost $500 million. How much did Kinsale lose? $22 million. AXIS lost $32 million.

Horse, meet water.

Have you done well with our P&C insurance-company recommendations? Please take a minute to let me know. It really makes a difference to us, knowing that people have benefited from our work. And, if you haven’t, please let us know what happened so that we can figure out better ways to serve you. Either way, let us know. It only takes a minute: [email protected]

Trump To Open ‘Phase II’ Of The American Birthright?

Presented by Paradigm Press

President Trump has made a move to permanently open the floodgates of America’s mineral dominance, unleashing Phase II of the American Birthright. Historically, Phase II has been the most lucrative investing window across resource booms. The last time this happened, investors could’ve seen rare peak returns of 7,500%… 20,183%… even 140,000% in the span of three years. Trump is just days away from opening a new Phase II window. To know exactly what to do, get the complete Phase II strategy immediately HERE

Three Things To Know Before We Go…

1. Big slowdown in jobs. This morning, the Bureau of Labor Statistics reported the U.S. economy added just 73,000 jobs in July, well below expectations of 106,000. More concerning, the May and June jobs reports were revised down by a massive 258,000 to just 19,000 and 14,000, respectively – representing the largest two-month downward revision since 1979 (outside of the COVID lockdowns). The unemployment rate also ticked higher to 4.2% from 4.1% last month.

2. The odds rise for a September rate cut. The Federal Reserve held rates steady for the fifth consecutive time on Wednesday, with Chair Jerome Powell reaffirming that the central bank remains in “wait and see” mode. However, following this morning’s weak jobs report, the odds that the Fed will cut interest rates at its next meeting rose to 79% from just 38% yesterday, according to the CME Group’s FedWatch tool. With signs of a slowing economy and with two Fed members voting for cuts this week, the market clearly believes a September cut is more likely than not.

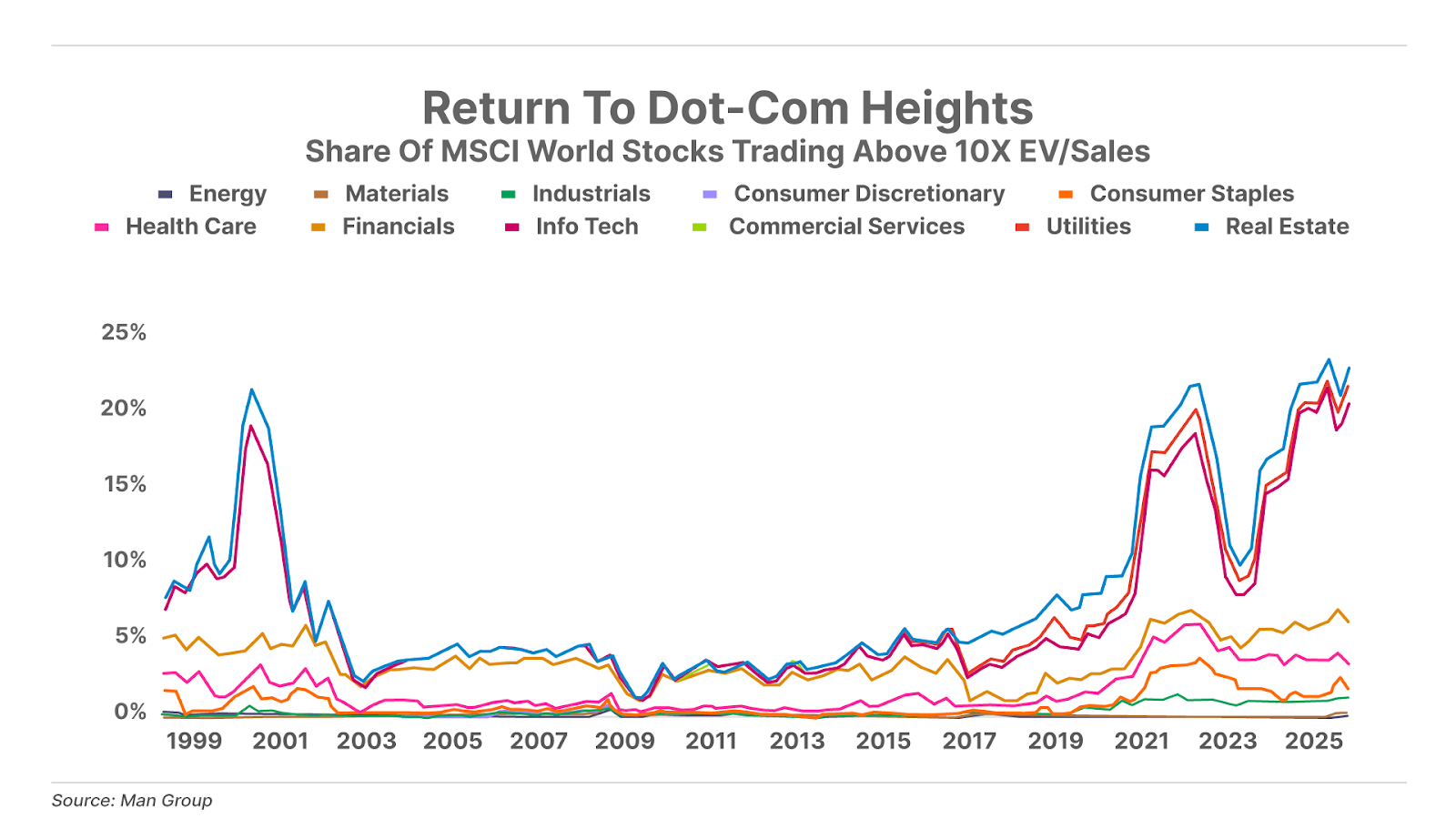

3. Investors buy stock like it’s 1999. With more than 20% of global stocks trading at valuations exceeding a high 10x enterprise value-to-sales ratio, this is the most expensive stock market in history – surpassing the previous records set at the peak of the dot-com bubble in 1999 and the 2021 meme-stock frenzy. What could go wrong?

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland