Issue #41, Volume #2

Lessons Learned From The 1973-1975 Recession

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Headlines now scream “stagflation”… Lessons learned from the 1973-75 recession… Nixon’s New Economic Policy antagonized adversaries and allies… There will be bargains… Tariff wars heat up – and cool down… The Mailbag: tariffs and the Orange Man… |

The stock market’s performance over the last week – at noon, the S&P 500 had dropped 12% since Wednesday – has rocked the economy, particularly given that the broad index had risen more than 20% in each of the last two years. Of course, it’s not the first time the market has fallen to this degree. To provide perspective on the market’s historical behavior, and to offer insights on what it means for equities, bonds, and the economy, Porter asked Distressed Investing senior analyst Marty Fridson to contribute to today’s Daily Journal.

Marty has seen it all… Investor’s Digest called him “the most well-known figure in the high-yield world.” Over a 25-year span with Wall Street firms including Salomon Brothers, Morgan Stanley, and Merrill Lynch, he became known for his innovative work in credit analysis and investment strategy.

Below, Marty describes the recession of 1973-1975, when high inflation, high unemployment, and slow economic growth merged to make stagflation a household word.

Here’s Marty…

One disconcerting aspect among many disconcerting aspects of the current market turbulence is the emergence of stagflation in economic commentary.

A mashup of “stagnation” and “inflation,” the term refers to a state of simultaneous low economic growth, high inflation, and high unemployment. JPMorgan CEO Jamie Dimon raised this possibility of it in his recent annual letter to shareholders:

The recent tariffs will likely increase inflation and are causing many to consider a greater probability of recession.”

As recently as May 28, 2024, the U.S. Chamber of Commerce headlined a report, “Stagflation Is Not A Looming Threat.” Yet on the morning of April 8, 2025, alone, the following headlines had all appeared within the last 24 hours:

- “Trump’s Tariffs Leave Economists Fixated On One Word: Stagflation” (Bloomberg)

- “Is The U.S. Economy Headed For Stagflation? Here’s What to Look For” (The Washington Post)

- “America May Be Headed For This Rare Type Of Economic Crisis – Stagflation Explained” (Vox)

- “Stagflation Is Now America’s Best-Case Scenario” (Bloomberg)

Such talk stirs up memories for those who were following economic events in the early 1970s. Stagflation struck fear in observers of the economic scene. Market watchers then were intellectually invested in the Phillips Curve, which states that the higher the unemployment rate, the lower the inflation rate – and vice versa. It had always been that when unemployment was high, workers had less money to spend, which decreased prices and inflation.

So high inflation coinciding with high unemployment? Couldn’t happen, many argued… until it did happen.

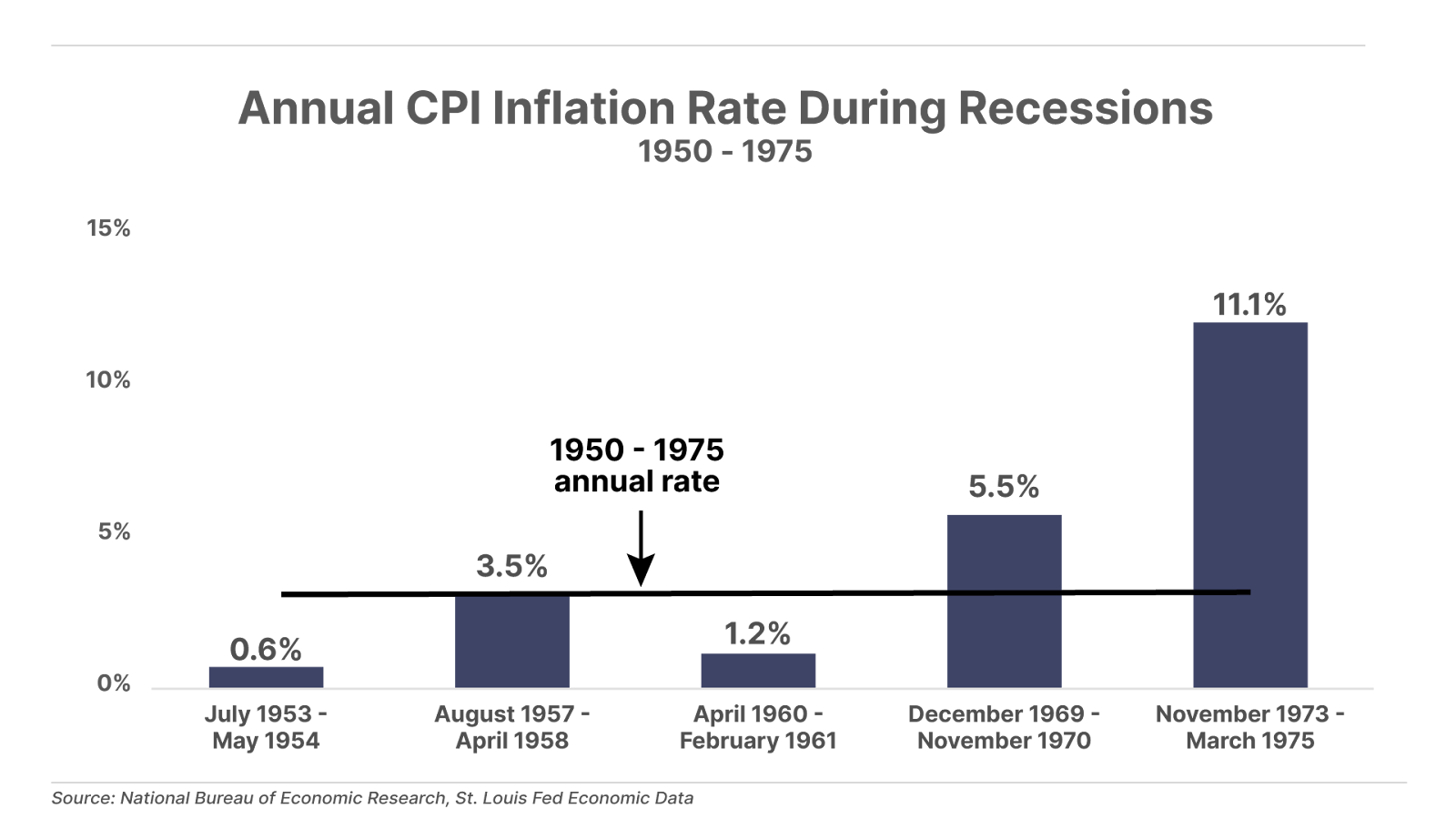

During the 1973-1975 recession, the monthly unemployment rate rose as high as 8.6%, compared with a 1950-1975 average of 4.9%. During that recession, inflation ran at a staggering 11.1% annual rate. The contrast was stark with the first three recessions shown in the graph below. In those episodes, inflation was either at or substantially below the full-period average of 3.5%. Only in the recession that began at the tail end of the 1960s did above-average inflation begin to appear in conjunction with economic contraction.

Parallels between the current period of resurging stagflation fears and the early 1970s extend beyond economic indicators. Just as President Donald Trump’s instigation of a tariff war has antagonized U.S. adversaries and allies, President Richard Nixon’s New Economic Policy, launched on August 15, 1971, did the same.

It wasn’t just because Nixon’s announcement pre-empted the hugely popular television show Bonanza. His economic program consisted of severing the dollar’s value from gold, instituting wage-and-price controls, and imposing a 10% tariff on all imports.

Domestically, the program was well received… at first. The day after he announced his program, the Dow Jones Industrial Average posted its biggest one-day gain ever (at that time). But prices in foreign stock markets fell sharply. And with the New Economic Policy arriving just a month after Nixon’s surprise announcement that he’d accepted Premier Zhou Enlai’s invitation to visit despised Communist China, the nation’s allies worried that America was going it alone in economic policy as well as foreign relations.

The rhetoric accompanying Trump’s trade policy strikes some of the same notes that accompanied the New Economic Policy. Nixon blamed his era’s U.S. trade deficit on other countries’ unfair practices. He complained about allies who didn’t “bear their fair share of the burden of defending freedom around the world.”

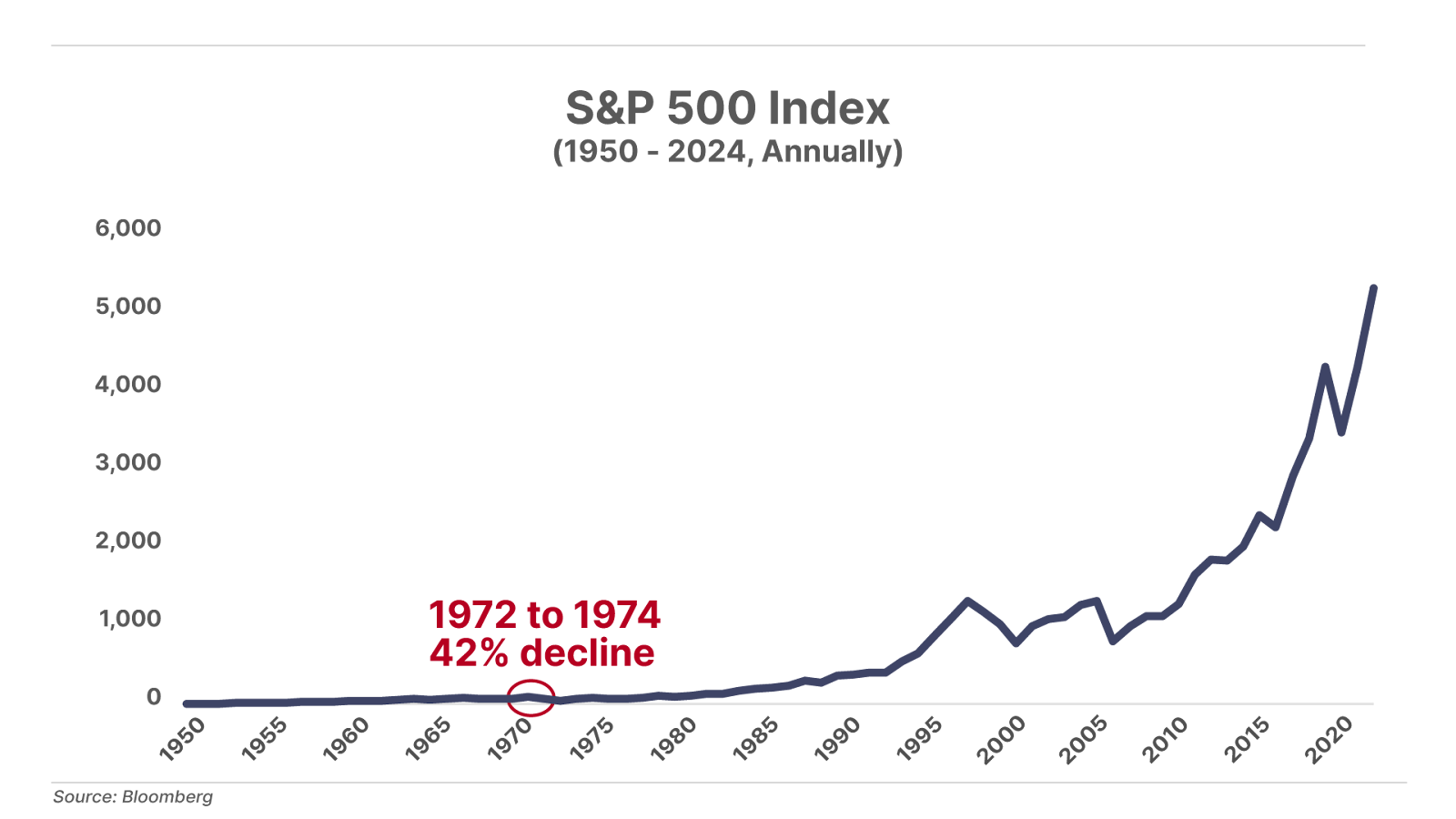

Despite the financial market’s initial favorable response to Nixon’s New Economic Policy’s introduction, it wasn’t long before investor sentiment soured. As the economy slumped and inflation soared, the S&P 500 dropped 42% from 1972 to 1974.

The graph below documents one saving grace, however. Stagflation didn’t become entrenched, and the blow to wealth that it inflicted barely registers as a blip on the long-term performance of the market. The S&P rose 31.5% in 1975. Embedded in that average were much bigger gains on many stocks of good companies that had become screaming bargains in the two-year downturn. For example, shares of Coca-Cola (KO) gained 175% in just three months following its October 4, 1974, low.

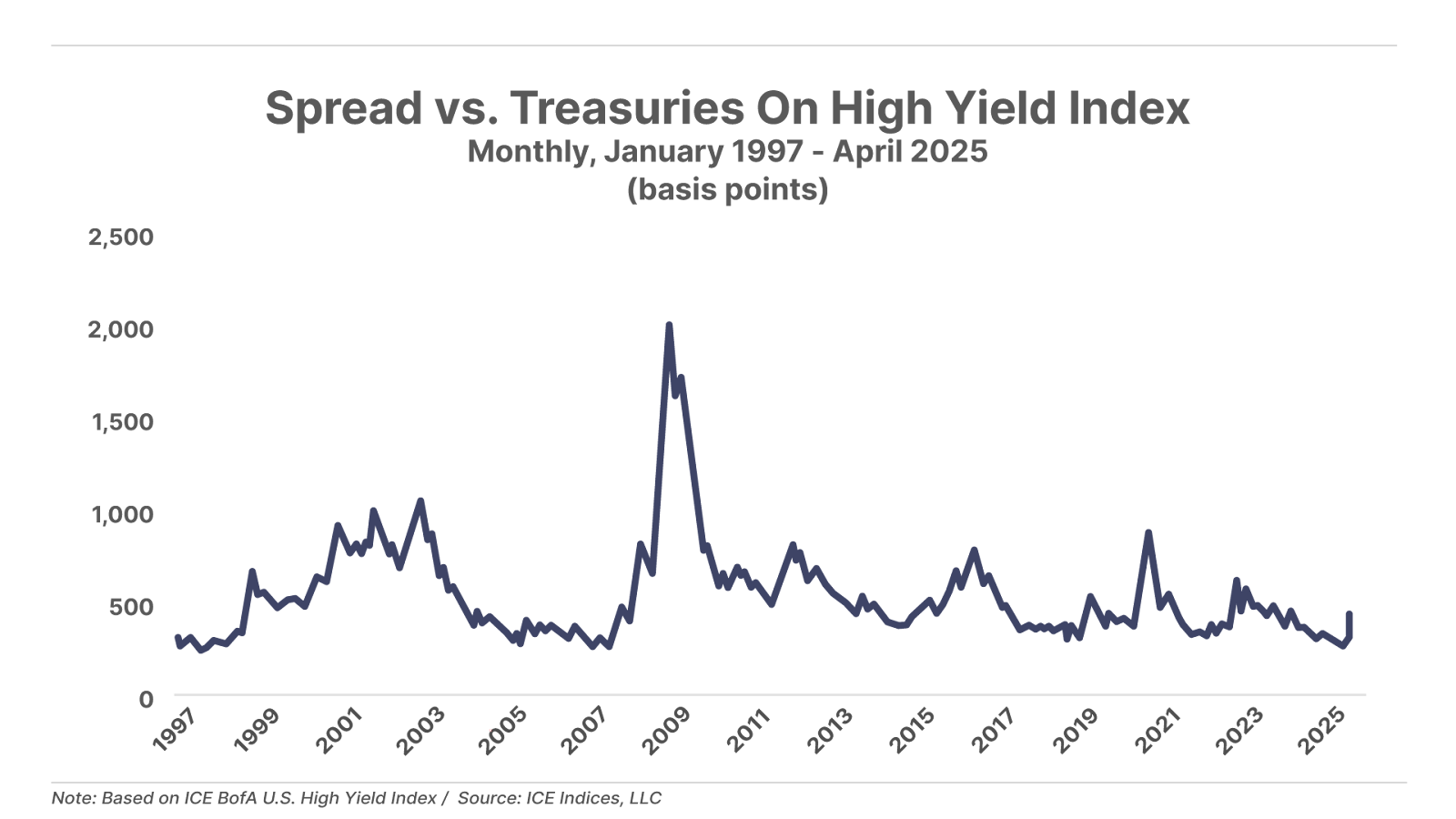

Based on that experience, investors can reasonably infer that a number of attractive opportunities are currently being created in the equities market. And some of them are taking shape in the debt market as well. Between Trump’s “Liberation Day,” when he announced his tariff strategy on April 2, and April 8, the yield on the ICE BofA U.S. High Yield Index jumped from 7.40% to 8.51%.

To put that 1.11-percentage-point one-week move into perspective, it’s greater than the yearly change, up or down, in the index’s yield in 41% of years since 1996.

With U.S. Treasury yields declining during the one-week period last week, the rise of the high-yield index was the result of an increase in the risk premium. That’s defined as the excess of the index’s yield over the yield of default-risk-free Treasury bonds. In an extraordinarily short period, the yield-spread-versus-Treasuries went from a very skimpy level by historical standards to just .05 percentage points below the historical median of 4.66 percentage points.

The roster of potential distressed “buy” candidates grew as more high-yield bonds moved into distressed territory – defined by a yield 10 percentage points or more above Treasury rates – after Trump disclosed his tariff plan. Within the ICE BofA U.S. High Yield Index, the number of distressed issues swelled from 112 on April 2 to 168 on April 7. What’s more, the bonds that were already distressed in March got more distressed after April 2 – that is, they got cheaper. The average issue’s price fell 8.22% between March 31 and April 7. Seven bonds dropped by 20% or more.

Cheaper valuations don’t automatically make these bonds smart purchases. Some bonds that suffer price declines wind up deteriorating further and ultimately defaulting. To recommend a distressed credit in the current environment, we must be confident that the issuing company most likely has enough cash-generating capability to make it to the end of a recession. And in case it fails to do so, we want to be sure that bondholders’ claims are well covered by the value of the company’s assets.

The last few trading days saw extraordinary intraday swings. For example, on April 7, the S&P 500 fell by 4.3% and then, in just over half an hour, it swung to up 3.4% on the day, only to give back that entire gain. Share prices rose on an unsubstantiated report that Trump would soften his stance, and prices plunged when those hopes were dashed. This experience points to a continuing wide range of possible outcomes for the next few months. Bloomberg-surveyed economic forecasters currently see a 30% probability of recession within the next 12 months. That’s up from a 25% probability as recently as March 27. Investors could be in for rough sledding for quite some time.

But some highly profitable opportunities will arise for those who know what to look for and who can ride out the volatility they should expect along the way.

Three Things To Know Before We Go…

1. Credit crunch hits U.S. consumers. The latest Federal Reserve data on consumer lending revealed an $810 million decline in total borrowing in February, a significant miss versus economists’ expectations for a $15 billion increase. This follows Q4 data from the Fed indicating that total the share of consumer debt in delinquency rose to a five-year high at year end. Notably, this data reflects the weak state of the consumer before the recent chaos unleashed in the economy and financial markets from the escalating trade war in March and April. We expect more pressure on consumer lending and spending in the months ahead.

2. The bond market is not cooperating with President Trump. Long-term rates continue to climb, with the yield on the benchmark 10-year U.S. Treasury note rising to 4.51% this morning. While the Trump administration has publicly stated its goal is to reduce long-term borrowing costs, rates have reversed nearly all of their decline since inauguration day. The 10-year yield is now roughly 20 basis points higher than it was when tariffs were announced last Wednesday… and only around 20 basis points below where it was trading when Trump took office.

3. Trump pulls back on tariffs… except against China. Trump’s tariff war is heating up and cooling down. Responding to the U.S. president’s actions, China today announced an 84% tariff on U.S. goods, effective April 10. Trump had pushed total U.S. tariffs on China to a staggering 104%. Then Trump announced this afternoon on Truth Social that the U.S. is increasing its tariffs on Chinese goods – for the third time – to 125%, effective immediately. Meanwhile, Trump authorized a 90-day pause while substantially lowering reciprocal tariffs to 10% for the 75-plus countries that have begun to negotiate solutions. While the stock market likes the latest gambit, it’s not clear how much damage has been done.

And one more thing… Today’s Poll

As Marty Fridson detailed above, a two-year recession and bear market followed President Nixon’s changes in economic policy in the 1970s. So now we ask readers…

How Trump’s Mar-A-Lago Accord Will Send These Gold Stocks Up 10x

Among Trump’s biggest moves, none will be as important to the American economy or the gold market than the revaluation of American gold holdings.

Click here to read how a “Mar-A-Lago Accord” could reshape global monetary action for decades to come – and find out which gold securities are primed to benefit.

Mailbag

In Monday’s Daily Journal, “Dumb And Dumber Leading Us To The Apocalypse,” Porter wrote that “President Donald Trump’s tariffs, if left in place, will destroy the global economy. And this wouldn’t be the first time… It’s painful to watch.”

We received a flurry of emails. Our first letter writer is Peter A., who said:

I loved reading your piece “Dumb And Dumber Leading Us To The Apocalypse.”

It reminded me of the series of your Chairman of General Motors letters that you wrote. You were bang on then and you’re bang on again.

Thank you for your candor and for your courage in speaking out.

Take care,”

Hello Porter,

In your “Dumb and Dumber” article, you state that the “Orange Man” is leading us to the apocalypse, whereas in your presentation with Brad Thomas (Trump’s Secret Stocks) you put forward the opinion that Trump is knowingly carrying out a creative destruction which will lead to a reborn economy, and of which you approve.

When one reads you and listens to you as much as I do, Porter, it is difficult to figure out what you really believe in.

I have bought quite a few of your offers nonetheless: The Parallel Processing Revolution, Distressed Investing, and now Trump’s Secret Stocks…

Regards,

JP G.”

Porter’s comment: JP – Wonderful question!

In my discussions with Brad Thomas and candidate Donald Trump last year, I believed that Trump was going to take our country in a new and much better direction. Specifically, I expected he would open vast new markets for American products, drive large amounts of foreign investment into America, cut the size of our government’s deficits, and thereby put our finances back in order.

I understood that threatening our trading partners with tariffs would be a major cudgel of his policymaking. And, as Trump had long explained, I expected him to threaten to impose reciprocal tariffs, to get our trading partners to “come to the table” and lower their tariffs, expanding our markets.

What Trump has done instead is simply madness.

Without any warning he’s decided not merely to fight back against foreign tariffs (a reasonable objective) but instead to end America’s trade deficit with every nation in the world, by placing tariffs as high as 90% on some countries and provoking trade wars with others.

Ending the trade deficit with every individual country in the world is an absurd goal that will not serve America.

Most countries in the world have a trade deficit with America because most countries are not wealthy enough to afford to buy many of our products.

With countries that can (and should) buy more American products – like China, Japan, Europe, Mexico, and Canada – we should be able to negotiate low, mutual tariffs, or even better, genuinely free trade.

But, what I keep hearing from the Trump administration – most notably its quack economist Peter Navarro – is that they’re going to insist that other countries’ internal tax regimes (like VAT taxes) count as tariffs. That kind of argument is ludicrous and will lead to a global catastrophe, as America’s government ought not be dictating to our allies how to run their economies. Likewise, I hear more and more about forcing other countries to pay “reparations” to us, as though we were in some way cheated or enslaved by them. That kind of rhetoric is anti-American and idiotic.

As I wrote in “Dumb And Dumber” on Monday, high tariffs and other absolute barriers to trade (like demanding reparations) don’t merely harm our trading partners, they will kill our economy too because of the incredible wealth building dynamic of comparative advantage, which is one of the oldest and best understood theories of economics.

High tariffs lead to economic stagnation and, eventually, collapse. It happens every single time. Our trading partners haven’t been “cheating” us. They’ve been cheating their own people, which is why Europe’s economy doesn’t compare to ours, why China’s economy is imploding, and why Japan’s economy hasn’t grown in 30 years!

Tariffs are horrible for economic growth because they’re an abridgment of individual rights. The government ought not dictate to anyone who they can or can’t buy from. That’s why tariffs are a bad idea. Seeing other countries adopt bad policies shouldn’t lead us to copy them!

In summary, I was in favor of President Trump threatening our trading partners with tariffs. But I have never been, nor will I ever be, in favor of tariffs. Tariffs, along with estate taxes and capital gains taxes, represent the most damaging ways of generating government revenue because they lead to grave misallocation of capital and they reduce labor productivity by disincentivizing capital investments and innovation.

I’m surprised how badly you whiffed on this softball pitch. Come on, man! You obviously missed the key descriptor of the tariffs as “reciprocal.” You went on a rant about free trade. Free trade only can operate on a level playing field. You know that. So what is your plan to level the playing field if you find these tariffs so objectionable? We have suffered tariffs tacked on to our products. We’ve been paying for global security since WWII. Have you ever been to Wiesbaden, Germany? Any military base in Guam, Japan, South Korea, or the Philippines? Any idea what this has cost us? Since you’re clueless about all things military, you’re not in a position to pass judgment on the tariffs.

Free trade has been non-existent, and any global trade has only been enabled by our vigilance on the seven seas and the skies. Your only accurate statement was that our debt is a real problem. Don’t worry, that solution is in the works. I’m surprised you are discounting Treasury Secretary Scott Bessent when he speaks of monetizing U.S. assets. We have endless wealth in real estate and natural resources. Buckle up, dude, and watch in wonder.

Bruce C.”

Porter’s comment: Bruce –

With all respect, I’ve been studying free trade, tariffs, economics, and the history of financial markets for more than 30 years. Trade policy has nothing to do with our military adventures or the huge waste of capital we’ve spent on endless wars.

“Free trade” refers to the minimal barriers our citizens face from accessing products and services from any market in the world.

The benefit of free trade to Americans is:

1. It enables individuals, industry, and government at all levels, access to the best goods and services at the very best price. This is an enormous advantage for our markets, for our dollar, for our industrial production, and for the lives of every individual. This opens the miracle of comparative advantage in the most complete way, creating massive wealth for Americans.

2. Free trade enables and creates a dynamic economy. Why do you think America’s competitive position in software, entertainment, media, technology, AI, etc. is so dominant? Why did Japan’s Sony lose so badly to Apple? Why did Netflix, Google, etc. all start in America – not in China? The answer is free trade: our companies have access to the entire global supply chain. And, they face competition from the entire global supply chain. That dynamic is what has created America’s unique economy.

And, like I pointed out, this same dynamic is what created the British Empire, too.

As I said in my response to the previous email, my understanding was that as the president, Trump would insist on matching reciprocal tariffs in an effort to craft more free trade agreements, opening more markets for American products while maintaining low tariffs here. What he’s done is nothing like that. And what he’s saying about using tariffs to create large revenue for the government is, in my mind, about the worst possible option for raising tax revenue.

Whether he’s bluffing or negotiating, I can’t tell. But immediately placing huge tariffs on our trading partners (who are also our largest creditors) is a recipe for a global economic collapse.

Finally, whether it makes sense to you or not, the world is never going to be a “level playing field.” Most countries’ politicians get bought by their domestic industry and place protections around those industries. Ironically, this leads to much less growth in labor productivity, and, eventually, an industry that’s completely uncompetitive. History shows this happens every time.

Just because our trading partners do stupid things with their economies, doesn’t mean we should copy them.

One last point:

Most Americans would agree that they don’t want Europe’s sclerotic economy, with heavy taxes and heavy government regulation. That’s exactly what’s happening though – tariffs represent a huge encouragement of the government into an area of the economy that was previously free of regulation and they are the biggest tax increase since at least 1968, and maybe ever.

Great analysis, Porter.

The Western world has changed. Instead of economics ruling politics – the liberal state’s great achievement, before being poisoned by its grandiosity – now politics is going back to ruling economics.

Tariffs are perfect timing for bringing down China – an enormous achievement, given that they still intend to take over the world. Primarily using 19-century debt-diplomacy, but not averse to other means.

The only thing we can hope for is that the tariffs get negotiated way down. Meantime, it looks like madness unleashed, especially with China.

As Bill Bonner said, trade wars tend to turn into currency wars and then shooting wars. If China President Xi Jinping slips up too much – and he absolutely depends upon exports – he will invade Taiwan in order to stay in power, and bye-bye TSMC.

Paid-up subscriber Barry H.”

Porter’s comment: I sure hope you’re wrong.

But, this much I know, destroying the global economy, ending the dollar’s world reserve currency status, and defrauding all of our creditors isn’t going to be good for any American.

It’s hard to understand why so many people are clamoring for a new Great Depression and the collapse of our economy.

Porter,

Couldn’t agree more. The size of government is the problem. However, you should knock off the name calling, i.e. “Orange Man.” Makes you sound like a Democrat.

Regards, Larry H.”

Porter’s comment: Larry –

You might not remember, but I famously called Obama “OBAMA!”

I’ll keep calling him Orange Man until he fires Peter Navarro, who is a complete quack.

Then I’ll call him Golden Man.

Good investing,

Porter Stansberry

Stevenson, MD

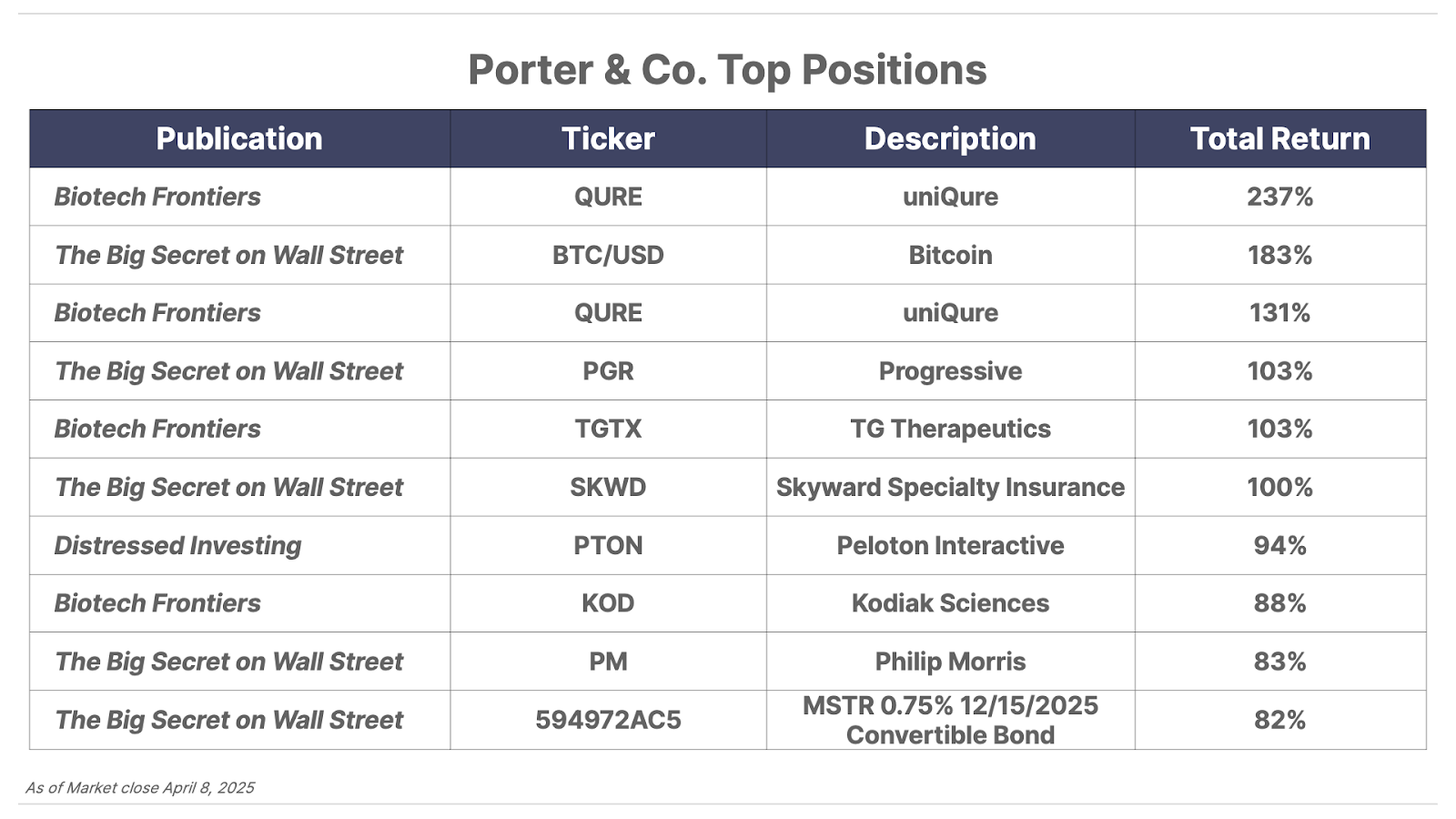

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.