To kick off Year #2, we’ve set our sights on an industry that’s deeply underappreciated… enjoys a unique quirk of financing that allows the strongest players to be ludicrously profitable… and is essential to the operation of civilization as we know it.

Warren Buffett Calls This Industry “Cost-Free Money”

The Ultimate Defensive Sector

One year ago… on June 4, 2022… we published the first issue of The Big Secret on Wall Street.

And since the inaugural issue, the team here at Porter & Co. continues to stay several steps ahead of the financial press and Wall Street.

We’ve written about the leading global drug maker supplying a revolutionary new class of weight loss drugs that’s solving the global obesity epidemic (+51%), a discount retail franchisor profiting from the collapse in consumer purchasing power (+71%), and the next NVR – a land-lite homebuilder riding high on today’s record housing shortage (+46%).

We’ve explained what’s next for the U.S. oil and gas boom… why nuclear energy is set for a revival… and warned about the coming implosion of the corporate debt bubble.

And we’re just getting started…

There are a number of huge stories my team and I will be shining a light on soon… starting with today’s.

To kick off Year #2, we’ve set our sights on an industry that’s deeply underappreciated… enjoys a unique quirk of financing that allows the strongest players to be ludicrously profitable… and is essential to the operation of civilization as we know it. It’s a sector I’ve followed closely throughout my career.

And in today’s issue of The Big Secret, fully paid-up readers get not just one recommendation in this sector, but two.

After all, it’s a special occasion.

And I want to make sure YOU get these stories first. Always and forever. Let me quickly explain…

Warren Buffett has been with the love of his life for 56 years.

That’s longer than his – according to the finance gossip press – “unconventional” 52-year marriage to Susie, who passed away in 2004. And certainly longer than his widely-publicized affair with Katharine, or his 17-year (and counting) second marriage, to Astrid.

Warren’s true love is the insurance business. They’ll be together until death parts them.

Once Buffett’s company, Berkshire Hathaway, made its first major insurance purchases – National Indemnity and another, smaller company – for $8.6 million in 1967, he never looked back…

Today, the core of Berkshire remains insurance – Berkshire Hathaway Reinsurance, Geico, and General Re, plus a collection of smaller companies. This growing tribe of insurance companies provided Buffett with the fuel that powered the compounding machine of Berkshire Hathaway – a source of permanent “free capital”, which he has used to invest in a wide range of other businesses.

This “free capital” gives Berkshire the ultimate advantage over banks, hedge funds and other money managers, all of which must pay to borrow capital for making investments. And it’s the secret sauce that paved the way for Berkshire Hathaway to become the eighth-largest company in the S&P, with a $660 billion market cap. Buffett himself is the fifth-richest man in the world.

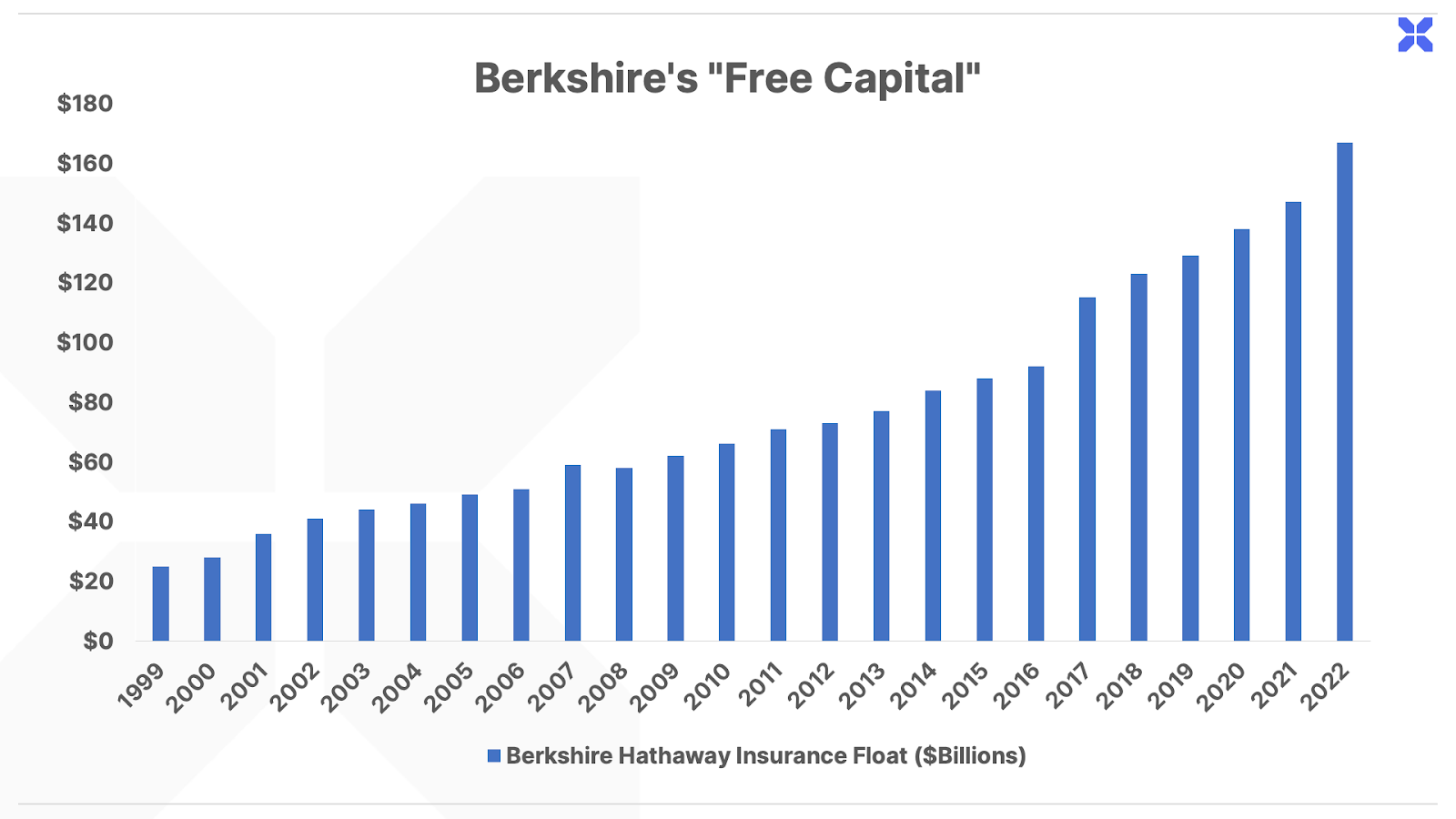

Starting in 1970, Berkshire’s insurance operations provided Buffett with $39 million in “free capital.” He invested this free capital into a collection of world-class companies, providing more profits to buy more insurance companies, which in turn, provided more “free capital” in a virtuous compounding cycle.

Over the last five decades, Berkshire has snowballed its way into an incredible $164 billion in “free capital.”

In Buffett’s own words, if he hadn’t made that first, fateful insurance buy back in the ‘60s, “Berkshire would be lucky to be worth half of what it is today.”

Warren flirted with insurance long before they got together, though.

In 1951, he made a small purchase of Geico, for around $10,000. He sold a year later, for around $15,000.

He didn’t buy back in until the 1970s. Waiting so long – and selling in the first place – was a mistake.

If he’d held his original stake during that 20-year period, he’d have walked away with $1.3 million. The episode “taught me a lesson about the inadvisability of selling a stake in an identifiably wonderful company,” he said later.

But starting again in the 1970s hasn’t turned out so badly.

Today, Geico – now fully owned by Berkshire Hathaway – is worth approximately $27 billion, and has made Buffett $25 billion, for a return of around 1,050%, since then. But far more importantly, the original $2.35 billion acquisition of GEICO now provides Berkshire with over $30 billion in “free capital” each year.

And Geico is just one of Buffett’s insurance businesses (though, he’s admitted it’s his favorite). Since he first bought into the industry, Berkshire’s “free capital” base has exploded from $39 million in 1970 to $164 billion as of year-end 2022:

It’s not hard to see why Warren’s in love with insurance. But why do these companies turn everything they touch to gold?

It’s a fascinating story – and one that may very well end up as a passionate (investment) love affair for you, too.

And, like many great stories, it starts with catastrophe.

We All Need Insurance – Whether We Want It Or Not

Insurance, at its core, is the sharing or pooling of risks. When the chances of a financial loss – some as catastrophic as a hurricane that wipes your house from the face of the beach, or as minor as a fender bender on the freeway – are spread among many members of a group, the loss to any one member is substantially less than had the risk not been pooled.

Without this risk-mitigating tool, the economy would be a fraction of its size… global trade would collapse… businesses would be hamstrung… and innovation would be crippled. People would live shorter, sicker lives. It’s no exaggeration to say that without insurance, you wouldn’t own a home, drive a car, go on vacation, have healthcare, or enjoy any of the modern luxuries we take for granted.

In the words of the International Association of Insurance Supervisors (IAIS), “The absence of insurance would make progress and growth impossible.”

And property and casualty (P&C) insurance – the two stocks we’re recommending this week are in the sector – offers a way to compound money, year after year, with unyielding efficiency. And, when applied correctly, with very little risk.

Property and casualty insurance enjoys a unique financial benefit like no other business: it has a positive “cost” of capital.

That is, rather than having to pay for capital – like a bank that must offer interest payments on deposits – well-run P&C businesses receive zero-cost upfront capital in the form of insurance premiums. If the company charges more for the premiums versus what it ultimately pays out, it pockets the difference.

Most importantly, because P&C claims typically aren’t made for a number of years (or, in the best case scenario, are never paid at all if a claim fails to arise), insurance companies can invest that capital along the way – earning returns beyond the profits from their insurance underwriting.

Because insurance is often a cost of living, and of doing business – you have to have insurance in order to buy a car or home; businesses are required to have insurance in order to operate – overall growth of the industry is tied to the health of the economy.

But despite its close marriage with the economy, P&C is a business with a mind of its own.

And today, we’ll walk you through exactly what makes it unique… why it’s one of the safest defensive investments of all time… and how to find the top-performing companies in the sector.

How the P&C Business Works

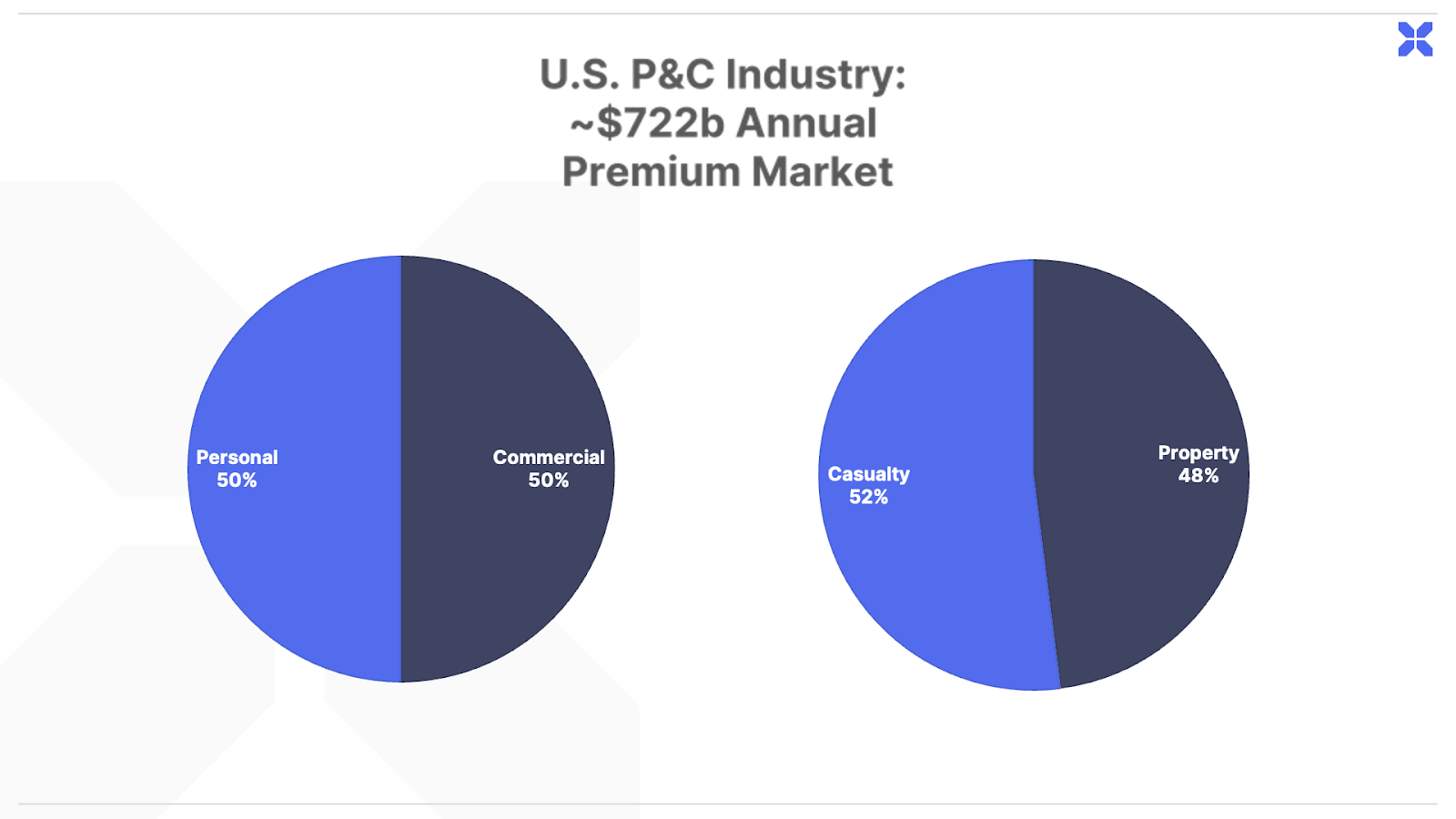

The P&C business (not to be confused with Porter & Co.!) writes about $700 billion total of annual premium. There are two main ways to split up this premium: property vs. casualty (each about 50% of the total premium) and personal vs. commercial (also, each about 50% of premium).

Property lines of insurance are “first party” lines: that is, they pay for actual physical damage to the insurance buyer’s (first party’s) owned property. Examples would be damage to your personal car from a hailstorm, or damage to the insurance buyer’s warehouse from a heavy windstorm.

Casualty lines are “third party” lines that pay for damage that the insurance buyer caused to a third party’s – that is, someone else’s – property. Liability is the determining factor of the insurance claim here: the insurance buyer is at fault for the damage, and the insurance premium pays for the loss as well as for legal defense, if necessary.

Property lines are typically settled and paid quickly, since there is no liability in dispute and doctors and attorneys are not involved. Casualty lines, in contrast, can take years to settle because of complicated medical bills, liability disputes, and attorney involvement. It’s not unheard of for casualty claims to take more than a decade to reach full resolution, making the pricing for such insurance products incredibly complex.

Both property and casualty insurance can also include personal (insurance purchased by an individual) or commercial (insurance purchased by an institution) lines.

Insurance for large corporations is far more complex than personal home or auto insurance, so companies that excel over the long run in commercial lines stand out with an unyielding focus on quality underwriting at the account level.

Underwriting is the process where an insurance company evaluates risks and decides which to take. Losses that are incurred and paid by an insurance company are known as claims.

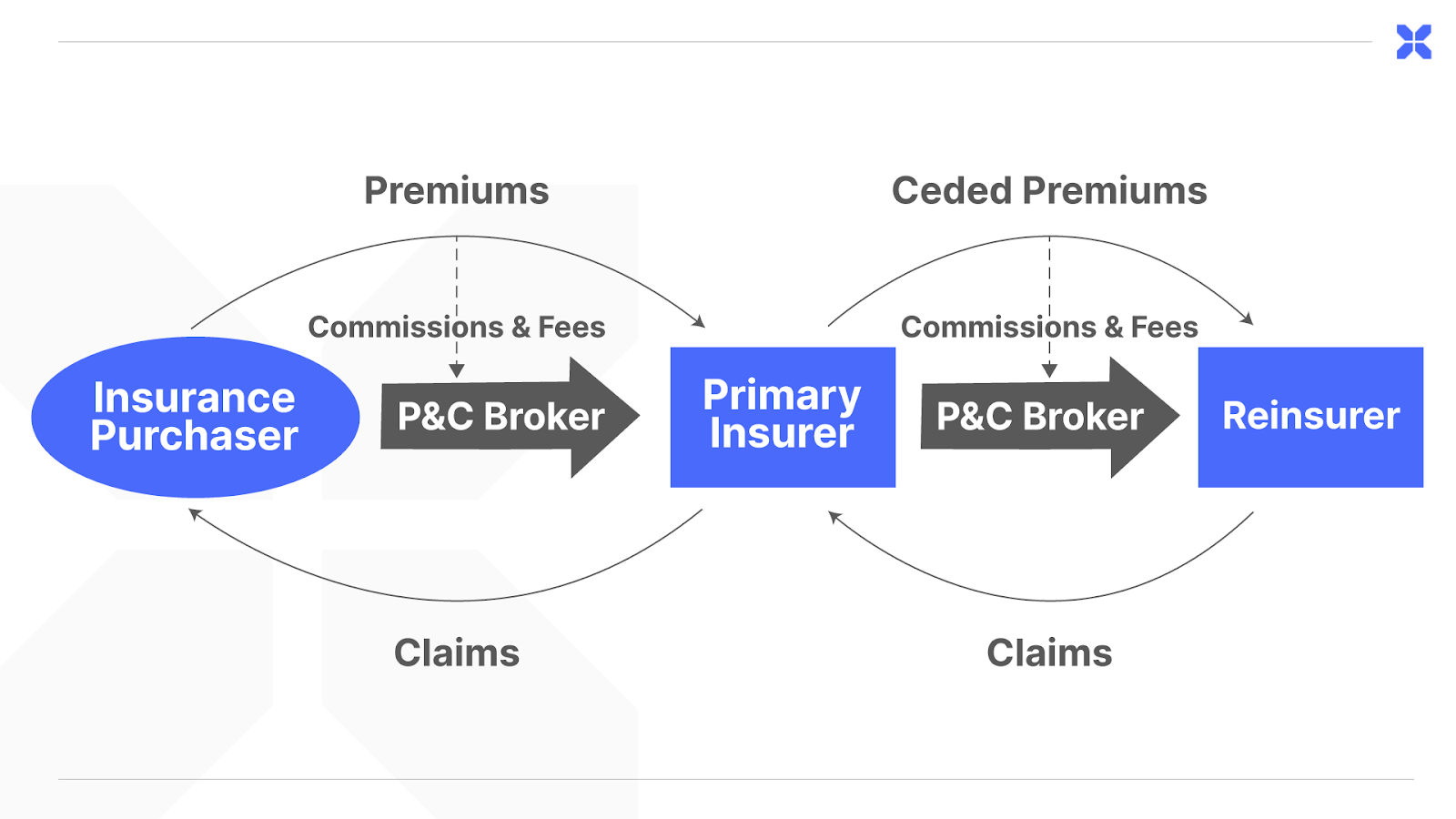

The chart below diagrams the industry supply chain, showing the flow of payment (premiums – what you pay for insurance) from the insurance buyer to the primary insurance company:

In return for premiums, the insurance company agrees to pay claims if a qualifying future loss event (like the car accident that damaged your vehicle, or the hurricane in Florida that hit your beachfront home) occurs. Most insurance business is placed via a broker (agent), who collects a commission or fee – but assumes none of the underlying risk. Insurance companies also buy insurance from “reinsurers” in order to further spread the risk of large losses to more insurers.

Insurers earn money on their underwriting expertise (underwriting income) and on earnings from investments that they make with premiums (more on this later).

Underwriting profitability is measured by the “combined ratio”, which is the sum of losses paid for insured claims and expenses associated with these losses, divided by the premium collected. For example, on one individual risk, if the insurance company collected $1,500 from you for your auto policy, and you had one claim to repair a bumper that cost $1,000 … the combined ratio on this one risk would be $1,000 / $1,500 or 67%.

Of course, such ratios only make sense when evaluated on an insurer’s entire book of business (not just one individual auto policy). Note that from this definition, a combined ratio below 100% equates to an underwriting profit, while one above 100% is an underwriting loss. A combined ratio of exactly 100% is breakeven. While the industry is in the business of underwriting and pricing insurance risk, most years it has an underwriting loss.

But that loss is usually more than made up for by gains from investments it has made from investing the insurance float (stay tuned, more on this topic below).

P&C Insurance Protects Investors, Too

While there are certainly growth periods for the property/casualty insurance industry, investing in property/casualty stocks is generally more of a defensive investment strategy.

A defensive strategy aims to reduce risk exposures and provide a more conservative approach to weathering market volatility while preserving capital. The primary focus of defensive investing is capital preservation rather than maximizing returns. The goal is to protect the value of investments and limit potential losses. One of the more overlooked aspects of investing is to preserve capital (minimize losses) when markets are in turmoil.

It’s important to note that while the P&C insurance sector is generally considered defensive, it can still be influenced by factors such as catastrophic events, regulatory changes, and shifts in underwriting conditions. Additionally, individual companies within the sector may have different risk profiles and financial performance.

Here are some of the reasons why the P&C sector is considered “defensive”:

- Steady Demand: The need for insurance coverage persists regardless of the economic climate. People and businesses require protection against property damage, liability claims, and other non-life risks, regardless of economic downturns. This consistent demand for insurance products provides a level of stability for P&C insurers.

- Non-Cyclical Nature: The P&C insurance has a more micro-oriented cyclicality because it’s less influenced by broader economic cycles compared to other sectors. While economic downturns can affect premium growth and investment income, insurance claims tend to correlate less with overall economic conditions. This non-cyclical nature provides a defensive characteristic, as the sector is less susceptible to significant volatility caused by economic fluctuations.

- Long-Term Orientation: P&C insurers operate with a long-term perspective, focusing on risk management, underwriting discipline, and maintaining sufficient reserves to meet policyholder obligations. This conservative approach helps P&C insurers weather short-term market volatility and uncertainties.

- Predictable Cash Flows: P&C insurance companies often have a reliable and predictable stream of cash flows. Premium payments are typically collected upfront, providing insurers with a consistent inflow of funds. Additionally, claims payments are spread over time, allowing insurers to manage their cash flow and liquidity.

- Risk Diversification: P&C insurers diversify their risk exposure across various policies, geographic regions, and lines of business. This diversification helps mitigate the impact of localized events or specific risks on the overall financial performance of the insurer.

- Conservative Investment Practices: P&C insurers generally adopt conservative investment strategies, focusing on low-risk assets such as high-quality bonds and cash equivalents. This approach aims to protect the insurer’s capital and ensure liquidity, minimizing the impact of market volatility on investment returns.

- Regulatory Oversight: P&C insurers operate within a regulated framework, subject to capital requirements, reserve obligations, and strict oversight by regulatory authorities. This oversight helps maintain stability and financial strength within the sector.

For these reasons, the P&C sector tends to be considered a “safer” investment asset class than many others such as technology, communications, or consumer cyclicals. This is because unlike many other industries, the demand for insurance remains relatively stable during all phases of the economic cycle and the industry has a recurring revenue model that provides more predictable cash flows over time.

At the same time, the regulatory oversight of the industry helps ensure that P&C companies maintain strong capital levels.

Perhaps counterintuitively, the P&C sector tends to outperform competing sectors in the stock market.

P&C Stocks Beat the Market

The P&C sector (including reinsurance) represents about 8% of the financial sector, which itself is 12% of the S&P 500. This means P&C stocks make up roughly 1% of the S&P.

But even though they’re a tiny slice of the S&P, property and casualty stocks have proven to be a longer-term outperformer relative to the market. Some investors might view P&C as a “boring” sector (“hey, let me tell you about the great insurance stock I just bought” is not a popular cocktail party line of conversation) – but there’s nothing boring about market-beating share price performance with lower risk.

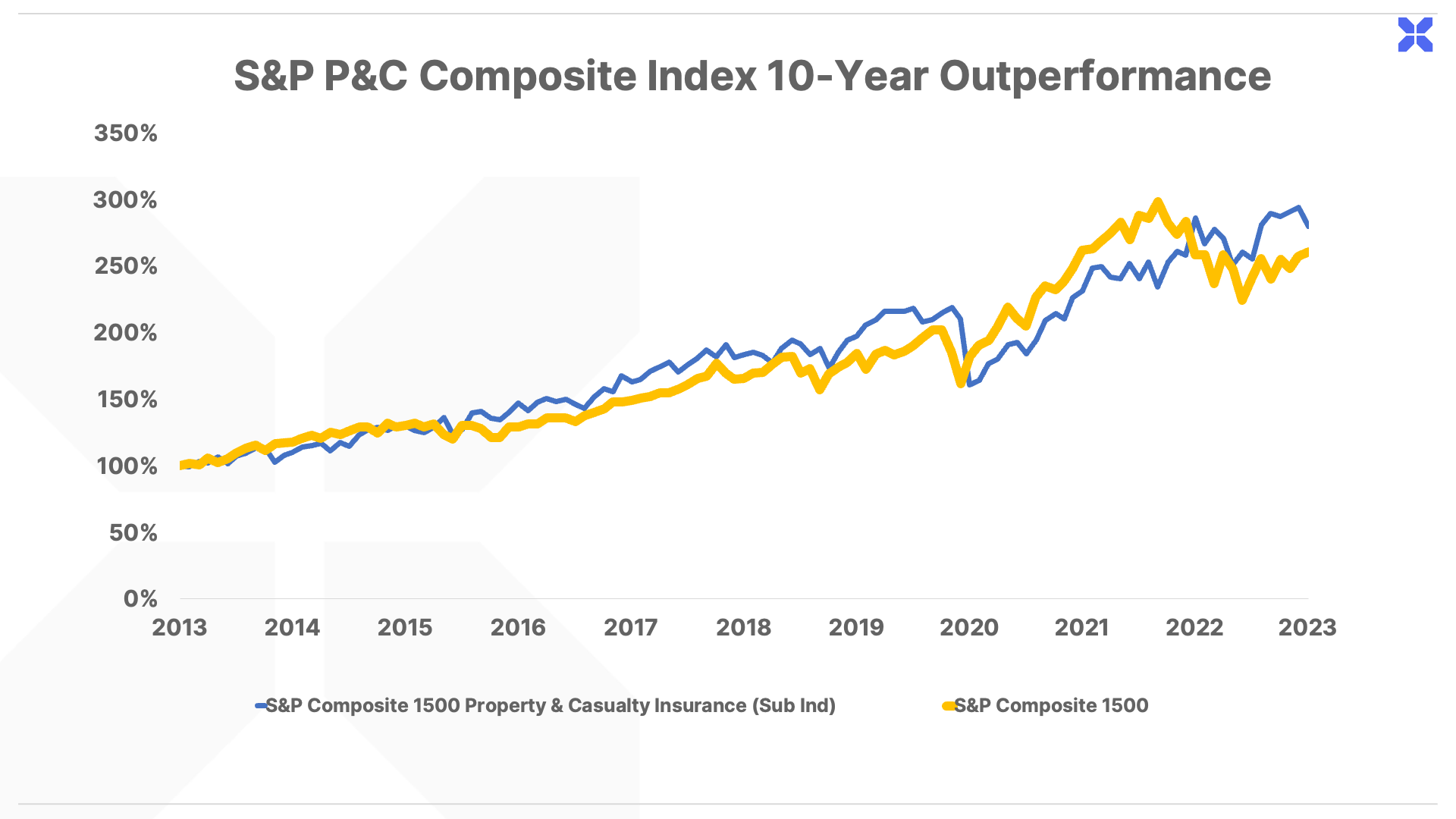

In fact, for the 10-year period from 2012 to 2022, the P&C sector’s stock performance was over 100 basis points (12.75% vs. 11.50%) better than the broader market performance. Moreover, the P&C sector maintains a very steady dividend yield in the range of 2.6% versus about 1.6% for the S&P 500. Hence, the total returns are even more impressive for P&C stocks relative to the S&P 500.

The 10-year outperformance of the sector has been relatively steady and consistent, at least up until the pandemic. The sector fell at about the same pace as the overall market, but the broader market had a slight outperformance on the rebound during the uncertainty of the Covid timeframe. However, in 2022, the P&C sector resumed its historical outperformance as investors embraced “value” strategies and rewarded insurers’ pricing power.

Defensive stocks tend to get a lot of attention and money flow when there is a great deal of uncertainty in the market or in the overall economy. They tend to be a safe haven in times of greater market volatility as a result of exogenous events, such as the potential of recession or other global economic turmoil created by pandemics and/or war… etc. In fact, P&C stocks have outperformed in 4 of the last 6 recessions, exceeding the market by 7 points on average.

It’s not surprising that these safe outperformers are a centerpiece of Warren Buffett’s legendary portfolio. And in fact, they offer one more very special characteristic that he describes as “cost-free” money.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care Concierge, Lance James, at 888-610-8895.