Three Vice Stocks With Hard-To-Break Habits

Porter & Co.’s Best-Performing Best Buys

| This is Porter & Co.’s The Big Secret On Wall Street, our flagship publication that we publish every Thursday at 4 pm ET. Once a month, we provide to our paid-up subscribers a full report on a stock recommendation, and also a monthly extensive review of the current portfolio… At the end of this week’s issue, paid-up subscribers can find our Top 3 Best Buys, three current portfolio picks that are at an attractive buy price. You can go here to see the full portfolio of The Big Secret.

Every week in The Big Secret, we provide analysis for non-paid subscribers. If you’re not yet a paid subscriber, to access the full paid issue, the portfolio, and all of our Big Secret insights and recommendations, please click here. |

It was 1604, and King James I (yes, the one who commissioned his own version of the Bible) really, really did not want his subjects to smoke.

About 360 years before the first Surgeon General’s Warning graced a pack of cigarettes, we had King James’ A Counterblaste To Tobacco, a 32-page polemic that skewered pipe-smokers as “scorned,” “grossly mistaken,” and abusive to their poor wives, who were forced to lie next to them “in a perpetual stinking torment.”

James, a rather high-handed monarch who wrote a treatise in favor of the Divine Right of Kings, had a track record of going on odd moral crusades – he once executed over 200 women in a royal witch hunt after becoming convinced that England was full of “detestable slaves of the Devil.”

However, his outrage at tobacco probably had more to do with a prominent smoker he absolutely hated: Sir Walter Raleigh – poet, explorer, and court favorite to James’ predecessor, Queen Elizabeth I.

Raleigh kept screwing up James’ foreign policy by agitating for war with Spain, while James planned to marry his son off to a Spanish princess. Plus, Sir Walter was a popular ladies’ man, while the dour (and likely closeted) Scottish-born king just wasn’t.

And Walter Raleigh was a smoker. My, how he smoked.

Contrary to popular legend, Raleigh likely didn’t introduce tobacco to England after encountering Native pipe-smokers on a 1580s expedition to the colony of Virginia. The pungent leaf had already reached Europe a decade or two earlier thanks to Spanish and Portuguese sailors.

But Sir Walter certainly did plenty of high-profile puffing – and, when James finally executed him on trumped-up treason charges in 1618, Walter had left behind a tobacco box in his prison cell with the inscription: Comes meus fuit illo miserrimo tempo (It was my companion at that most miserable time).

Tobacco, by then, was the constant companion of nearly everyone in England – despite King James’ valiant efforts. Remarkably, the “filthy novelty” spread from coast to coast even as the rest of the English economy struggled for cash.

Three years after James assumed the throne in 1603, he’d drained England’s coffers from a surplus of 90,000 pounds to a deficit of 816,000 pounds – due to ill-considered policy around England’s wool trade, rising population and falling employment, rampant inflation, and James’ own wasteful spending on fancy lords of the court. (It was, as Sir Walter’s snuffbox said, a most miserable time.)

Since no one seemed to have taken the message of Counterblaste to heart, James followed up his tract with a prohibitive 4,000% tax on tobacco products. If the noxious weed was going to stink up the kingdom, he figured, the Crown might as well profit. The tax proved to be no deterrent: in London alone, some 7,000 stores stocked tobacco products as Englishmen continued to spend more than 300,000 pounds annually on the stuff.

Sensing a profit opportunity, King James dropped the witch hunt. In 1624 – several years after Walter Raleigh technically suffered an early death due to smoking – James reversed his stance on tobacco and made it a legal monopoly.

By virtue of his divine right as monarch, James seized England’s tobacco business and forced the growers in Virginian colonies to do business only with the English government – and on the government’s terms. The colonists chafed at this arrangement for the next century, until the tension finally boiled over in the American Revolution… resulting in a free country without the divine right of kings, and with Marlboro Man and Joe Camel hawking their smokes in every convenience store.

The moral of the story is probably that tobacco smoke is stronger than almost anything else in the world: economic recession, court intrigue, or punitive taxes. (Maybe that’s why it’s impossible to get it out of couches and carpets.)

Humans gonna human… and vice is incredibly tenacious.

The Wages Of Sin

Vice or “sin” stocks – booze, cigarettes, gambling – historically act as safe havens in times of economic turmoil, because addiction isn’t tethered to the S&P 500. Inflation won’t cure a craving for nicotine… or a yen for fine brandy (which is why one of Porter’s favorite “oddball” stocks in his personal portfolio remains Rémy Cointreau). And as a bonus for the discerning investor, vice stocks offer a kind of frisson that feels like you’re getting away with something.

Of course, those are just the commonly known vice stocks… sort of the “seven deadly sins,” if you will…

There’s also a batch of hidden vice stocks that offer vice on a much larger scale, if you’re into that sort of thing.

Regular vice stocks bank on people being addicted. Hidden vice stocks bank on society being addicted and continue to perform during recessions because the entire economy can’t break the habit… even if PC police or the TV talking heads disapprove.

“Dirty” energy is a prime example. No matter how expensive the cost of living gets, how much money the government prints, or how many tariffs and weird executive orders pour out of Washington, the world still needs light and heat at a reasonable cost.

The best ways to get that light and heat – in spite of what Greta Thunberg tells us – remain coal, oil, and unfairly-maligned nuclear power. Together, these types of dirty energy produce about 85% of the world’s power – with that amount projected to increase significantly by 2030 thanks to the massive demands of artificial intelligence (“AI”). AI data centers consume just 4% of all U.S. energy today, but this is expected to reach as high as 12% by 2028. Dirty energy, much like sin, is never going away.

In this week’s issue of The Big Secret, we’re revealing three of our historically top-performing Best Buys – and all three, it turns out, are vice stocks… of one kind or another.

(By the way, two of the best-performing Big Secret stocks right now are vice stocks. If you’d like to learn more about receiving these hand-picked recommendations each month, click here.)

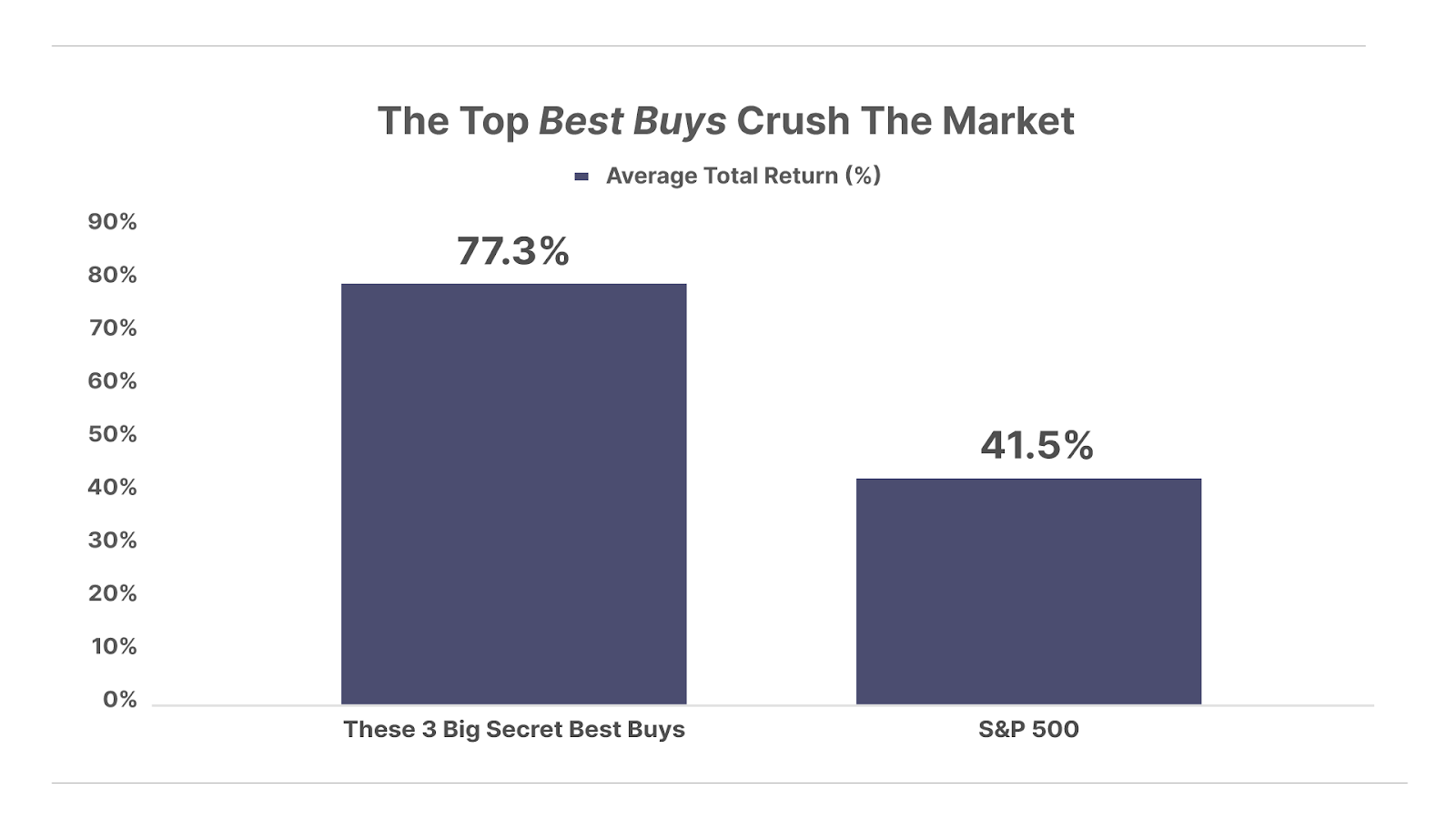

As you can see from the chart below, these three stocks have smoked the S&P 500 since we introduced Best Buys in February 2023.

The first is a classic indulgence that’s one of Porter’s all-time favorite businesses: a tobacco company that works more like a bank.

And the second two are “dirty” energy companies – one oil, one nuclear – that, despite plenty of moralizing from left-wing activists, America just can’t quit.

Below, we provide excerpts from these three recommendations – we published all three reports in 2022.

Those three companies are Philip Morris International, Viper Energy, and BWX Technologies. The excerpts for these three reports are below, along with their performance since we recommended them and during their times as a Best Buy.

Going From High Risk To Reduced Risk

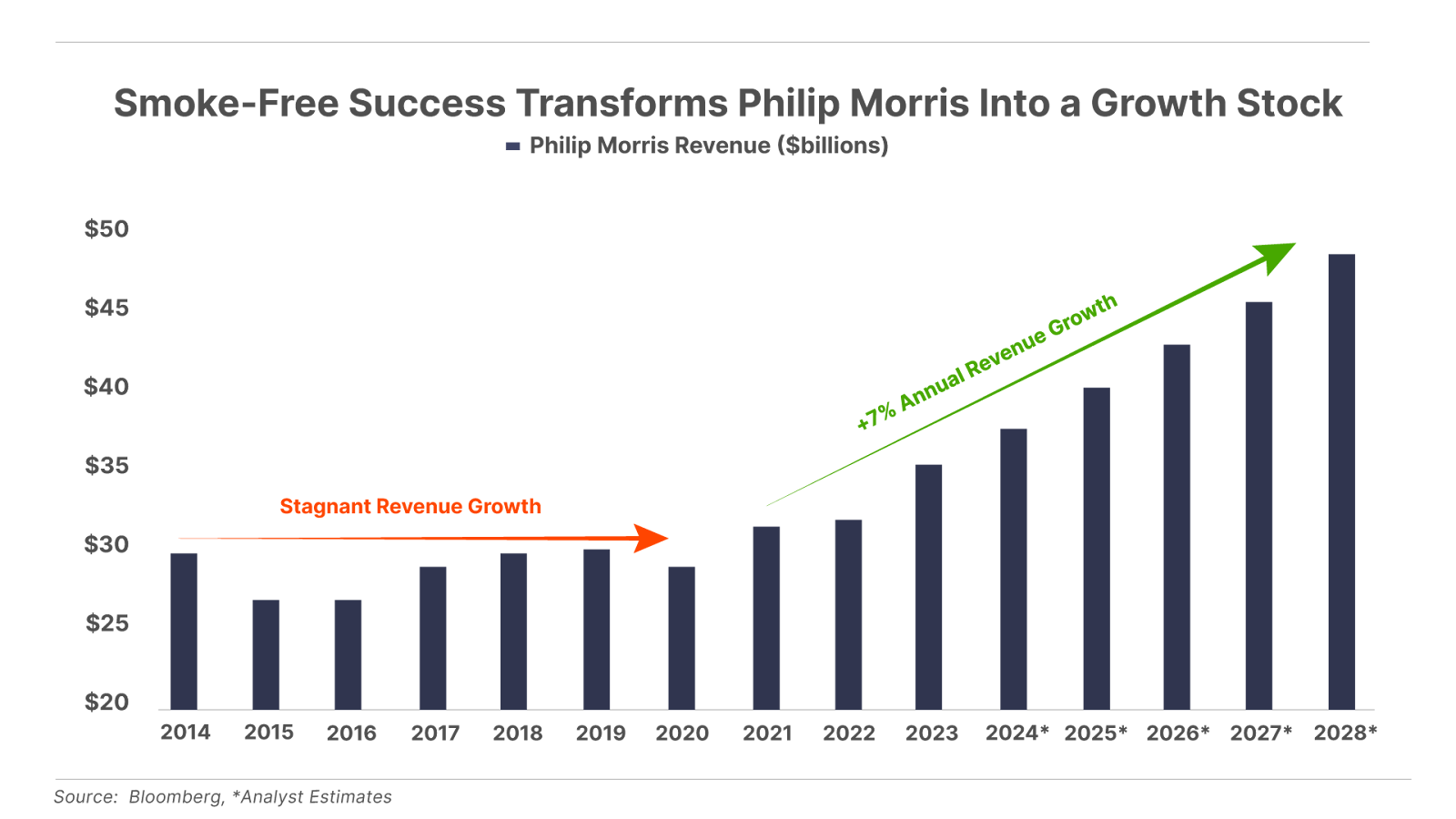

Up until March of 2008, Philip Morris was a subsidiary of parent company Altria (MO). The two companies split, based on the idea that Philip Morris could focus on growing the Marlboro brand internationally, while Altria concentrated its efforts on the domestic U.S. market.

As the two companies went their own ways, Philip Morris International (NYSE: PM) invested heavily in a suite of reduced-risk products (“RRP”) over the last decade.

The company plans to get half of its revenue from smoke-free products by 2025. And within 15 years, Philip Morris believes it will become the world’s largest smoke-free nicotine company.

Chief among them is the IQOS device, which heats up specially made tobacco “heat sticks” to a temperature that releases the nicotine of tobacco leaves – without combusting the thousands of additional harmful byproducts.

The company has invested $9.2 billion since 2014, and that bet is starting to pay off. IQOS is the number-two nicotine brand in the world, with nearly 18 million daily users, and which currently generates more than 30% of Philip Morris revenue.

In 2020, the Food And Drug Administration (“FDA”) granted Philip Morris the authorization to sell IQOS in the U.S. under the designation of a “modified-risk tobacco product.” IQOS is only the second product ever to earn this label, in addition to the General Snus product by Swedish Match – a company Philip Morris is now seeking to acquire.

In simple terms, this means that the FDA has ruled that IQOS qualifies as a device that can protect public health, and that can be marketed with the highly coveted “reduced exposure” label.

The IQOS product has so far avoided the regulatory snafus from a public health perspective that have plagued Juul and the broader vaping sector. Plus, IQOS has been a massive international success, and if smokable tobacco is going to be disrupted, all signs indicate that IQOS will be the disruptor.

Plus, Philip Morris continues investing heavily in a wide range of additional smoke-free nicotine products. This includes vaping products, nicotine patches, and a series of other cigarette alternatives.

That’s why we believe Philip Morris offers the ultimate hedge against both Altria’s core cash cow smokable business, as well as a hedge against the broader vaping industry, including Juul.

The financials are robust at Philip Morris. The company enjoys 20% returns on equity, and 40% returns on invested capital, and 40% operating margins. The stock is attractively priced at less than 15x earnings and pays out a well-covered 5.5% dividend.

And its ownership in the iconic Marlboro brand as well as IQOS puts the company in the leading international position for both smokable tobacco products, plus a potential future of smokeless nicotine consumption.

Excerpted from “Grab A Bucket: It’s About To Rain Gold,” July 15, 2022

We first recommended shares of Philip Morris International (NYSE: PM) at $90, and today shares trade at $159, for a total return including dividends of 95%. Philip Morris was first recommended as a Best Buy from November 2023 to October 2024 for an average return of 65%.

All The Energy Without The Costs

The oil-and-gas-producing land assets of Viper Energy (Nasdaq: VNOM) were developed by Diamondback Energy (FANG) and are in the heart of Texas’ Permian Basin – one of the largest oil fields in the U.S. If an oil company – Diamondback or anyone else – wants to produce oil from land that Viper owns mineral rights on, it must pay Viper a cut of the profits.

The key to understanding businesses like Viper Energy is that they don’t have to pay any of the production costs or take any of the developmental risks: Viper just owns the mineral rights – all capital and operating expenses lie with the operator.

Viper transforms a capital-intensive industry into a capital efficient business that’s virtually guaranteed to produce increasing returns across time. Well-run mineral-rights businesses like Viper are truly one of Wall Street’s greatest secrets.

Consider: our standard rule of thumb when seeking out capital efficient companies is finding businesses capable of converting at least 10% of sales into free cash flow, or a 10% free cash flow margin. Over the five years from 2017-2022, Viper has averaged an incredible 77% free cash flow margin.

Viper was created as a spin-off from Diamondback Energy in 2014. Viper was one of the first pure-play energy royalty businesses in the Permian and leads the market in consolidating royalty acreage – investing over $2.5 billion acquiring mineral rights over the last several years.

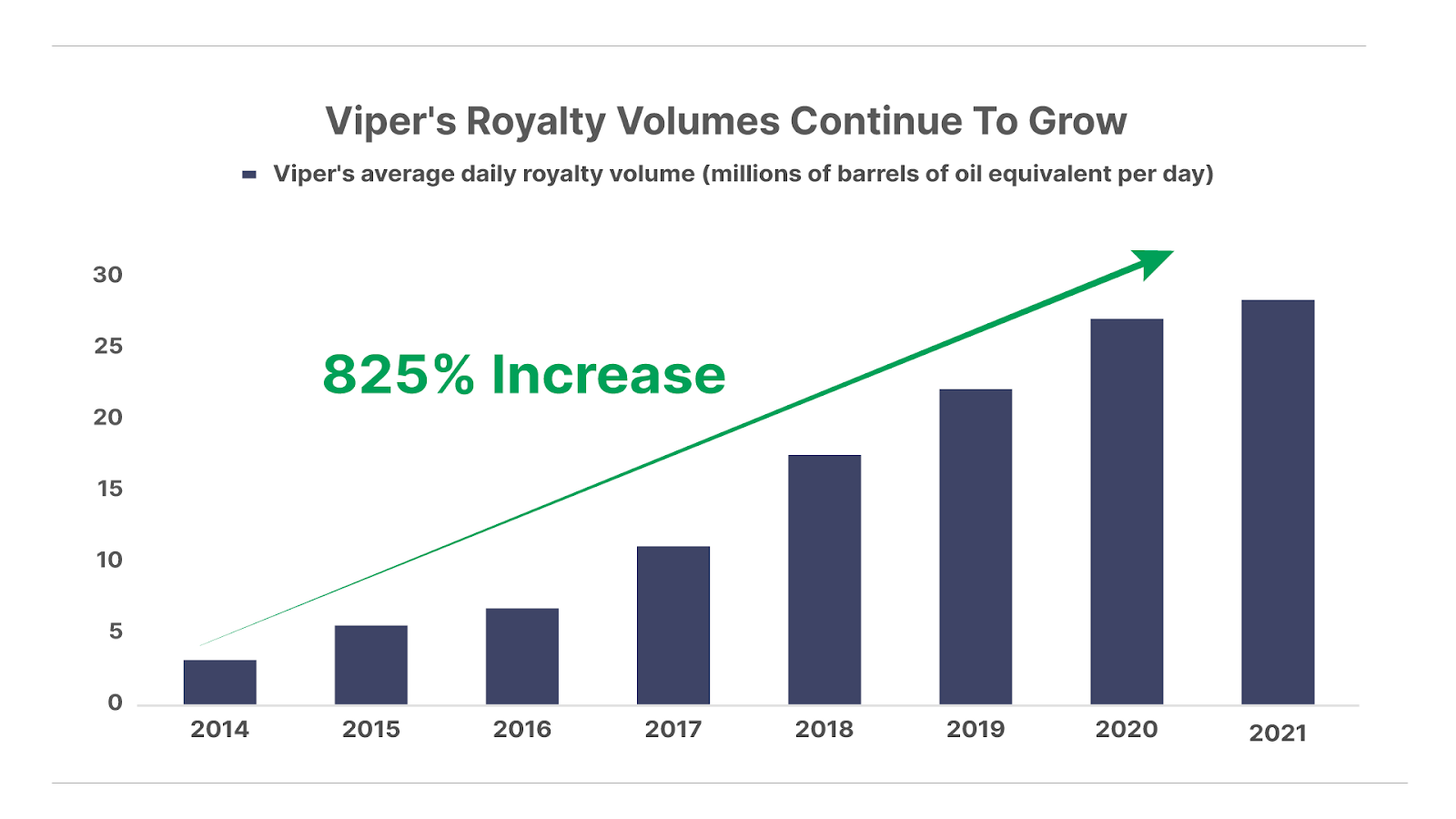

Since going public in 2014, Viper’s royalty volumes have grown nearly 10-fold, from average daily volumes of 3,000 barrels of oil equivalent (“BOE”) eight years ago to 28,000 in 2021:

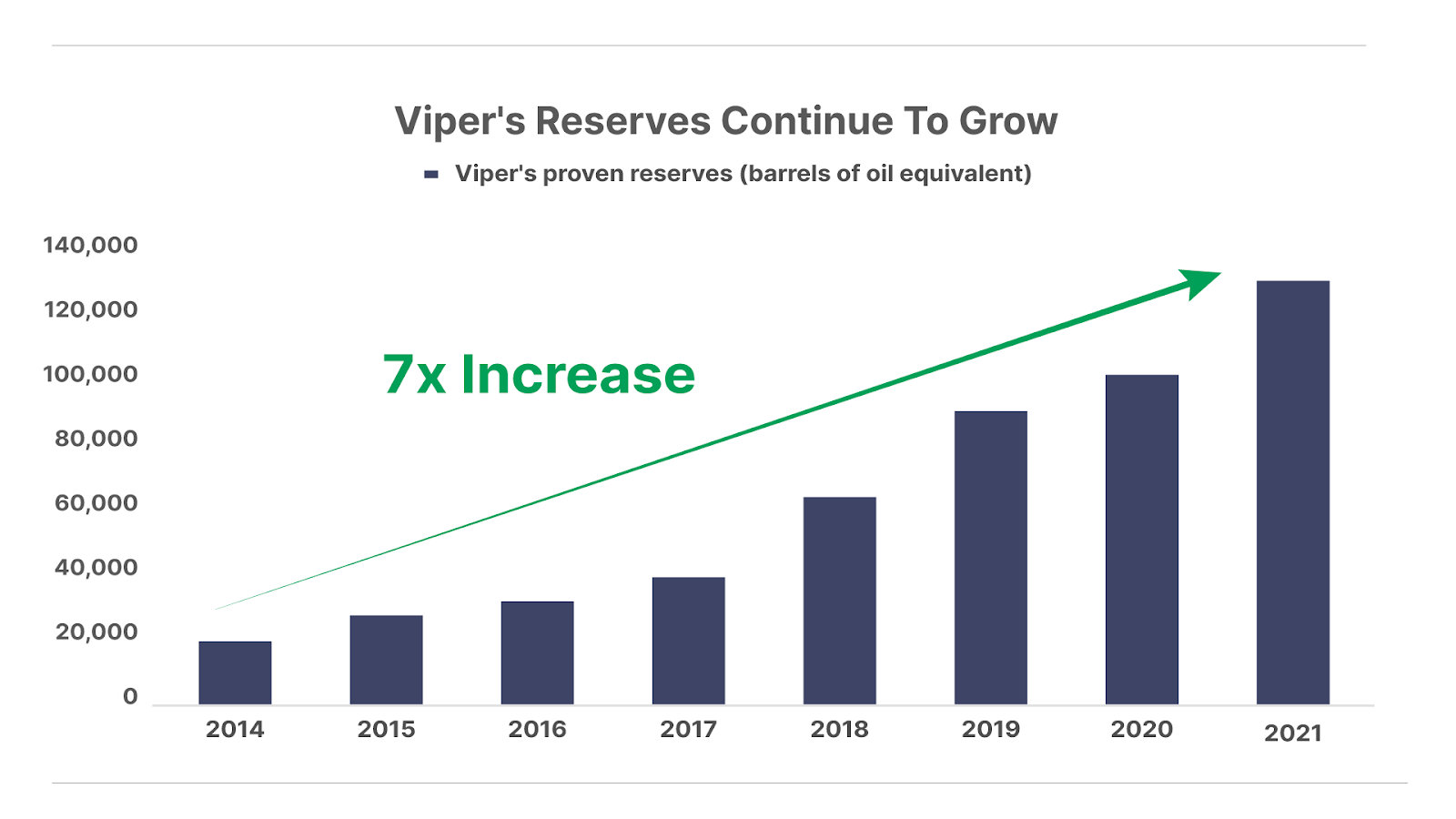

Viper owns mineral interests spanning across 930,871 gross acres and over 9,000 producing wells, with net production of 31,359 barrels of oil equivalent per day (“BOE/d”). The company’s total proven reserves stood at 128 million BOE as of year-end 2021, including 54% oil and 46% natural gas and natural gas liquids (“NGL”).

This reserve mix provides us with hedged exposure to a general bull market in fossil fuels – including oil and natural gas.

Viper’s asset base is concentrated in the heart of the Permian – America’s most prolific oil and gas deposit. The Permian spans across 75,000 square miles in West Texas and New Mexico, and it’s one of the oldest producing formations in America.

Going beyond oil, the Permian also hosts one of America’s largest deposits of low-cost natural gas. Over the last decade, explosive growth in gas production has pushed the Permian into America’s second-largest gas basin, trailing only the Marcellus formation in the Appalachian shale.

But owning mineral rights on great acreage is only half the battle. After all, mineral owners only get paid when oil and gas gets produced. That’s why it’s critical to partner with the right operators to maximize the value of that acreage.

And that’s where Viper’s biggest edge comes from its strategic partnership with Diamondback Energy, one of the best operators in the Permian.

Diamondback management maintains a disciplined approach to capital allocation and a conservative balance sheet. That’s how the company posted consistently impressive growth through the ups and downs in energy prices over the last decade.

We can see clear evidence of the success of this model through Viper’s track record of growing oil and gas reserves since inception, which has increased by an incredible 7-fold from 18 million BOE in 2014 to 128 million at the end of 2021:

Viper is simply the publicly listed portion of Diamondback’s huge royalty book. It allows investors to buy hydrocarbons directly, without the risks and capital requirements of production. In that way, Viper is more like a financing company than an energy company.

For such a compelling business model, you would expect Viper to command an exorbitant valuation premium. And yet, with a market capitalization of roughly $5 billion, the company trades at less than 10x free cash flow today.

The best part? Without needing to recycle earnings back into expensive equipment and other operating costs, that cash flows right back to investors. That’s how the company pays out a current distribution of $3.24 annualized, or a yield of nearly 11% on the current unit price of around $30.50

So, if you believe that Viper and Diamondback will continue thriving in America’s best oil and gas basin – as they have for the last decade – then it’s all upside from here.

Excerpted from “The Big Secret Behind T. Boone’s Fortune,” September 2, 2022

We recommended shares of Viper Energy (Nasdaq: VNOM) in September 2022 when they were $30. Today, shares trade for $39, up 48% when dividends are included. It was a Best Buy from February 2023 to January 2024 for an average return of 51%.

The Military’s Mr. Monopoly

BWX Technologies (NYSE: BWXT) has been at the forefront of nuclear technology since the birth of the industry. Today, it operates four main nuclear business units in the U.S. (BWXT mPower, BWXT Nuclear Energy, BWXT Nuclear Operations Group, and BWXT Technical Services Group), as well as the only two commercial plants in the U.S. that process uranium.

Most importantly, BWX Technologies is the sole manufacturer of nuclear reactors and fuel for U.S. military aircrafts and submarines. It’s also one of only two providers licensed to store and process highly-enriched uranium (“HEU”) for these reactors.

The government sector accounts for 80% of BWXT’s revenue. And nearly all of its deals with Uncle Sam are carried out via long-term contracts, resulting in a very stable and predictable business and revenue flow.

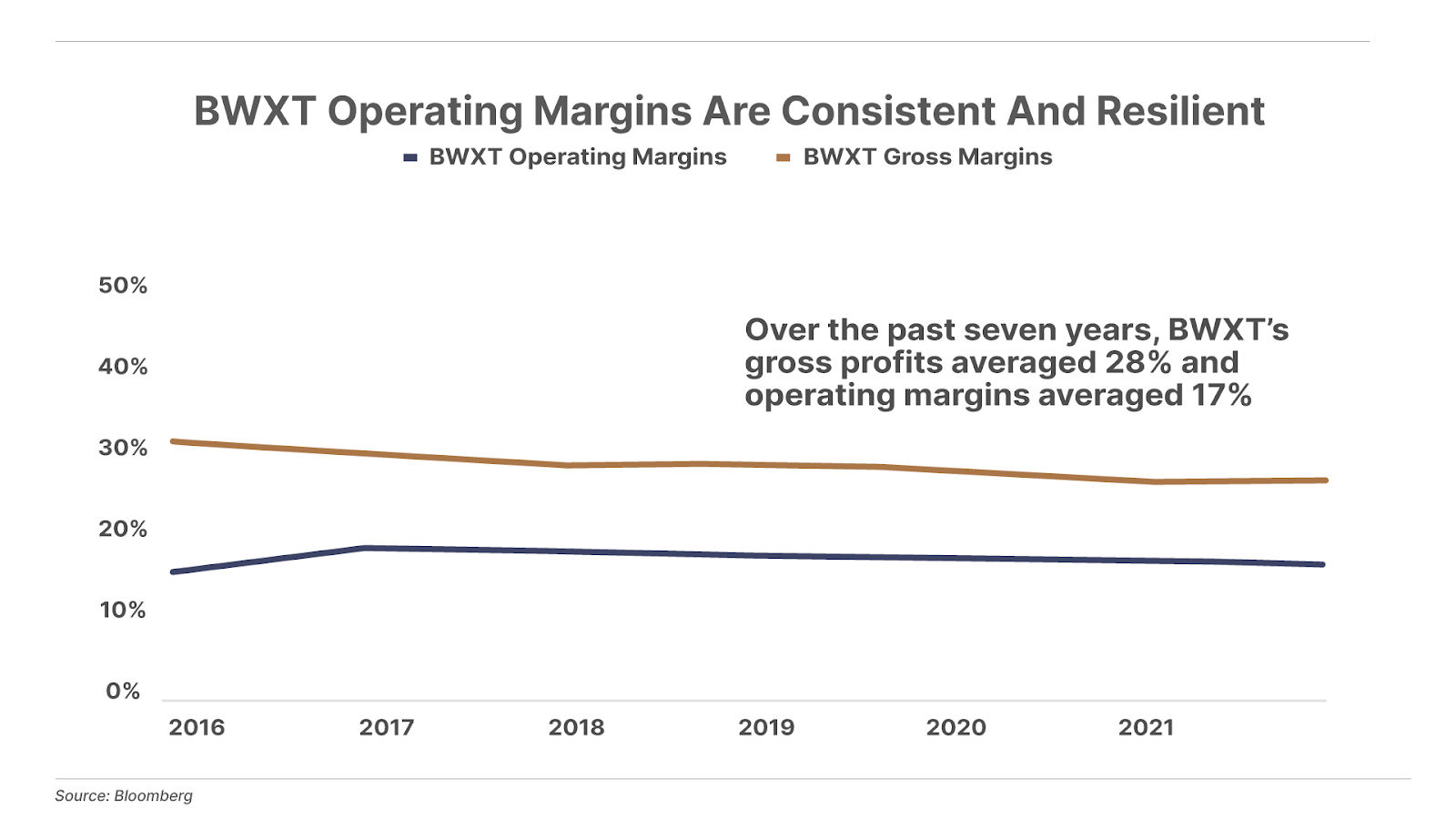

As a monopoly manufacturer, BWXT can set prices (within reason), and lock in steady profit margins. If a project incurs unexpected cost overruns, BWXT can charge the Navy backfees to make sure it hits its target profit margins. That’s how BWXT posts stable profit margins, with very little exposure to swings in the economy from recessions, inflation, or other external factors.

Over the last five years, the economy suffered through a devastating pandemic and economic shutdown, followed by the hottest inflation in the last 40 years. During one of the most turbulent macroeconomic periods in U.S. history, BWXT’s business has chugged along with remarkable stability with profit margins:

The business also provides a clear line of sight into the future, based on the full slate of projects BWXT has lined up…

With around 290 active, deployed ships, the U.S. Navy is not the largest in the world by ship count, though it’s by far the most powerful naval force thanks to its unmatched fleet of nuclear-powered vessels, including 50 attack submarines, 18 strategic submarines equipped with nuclear warheads, and 11 aircraft carriers.

The predictability and stability of BWXT’s business is unmatched. It has a near-lock on supplying the Navy with critical nuclear inputs. And demand for new carriers and submarines is based largely on the retirement of the existing fleet, so it’s easy to map out what the business will do next. And it’s growing apace…

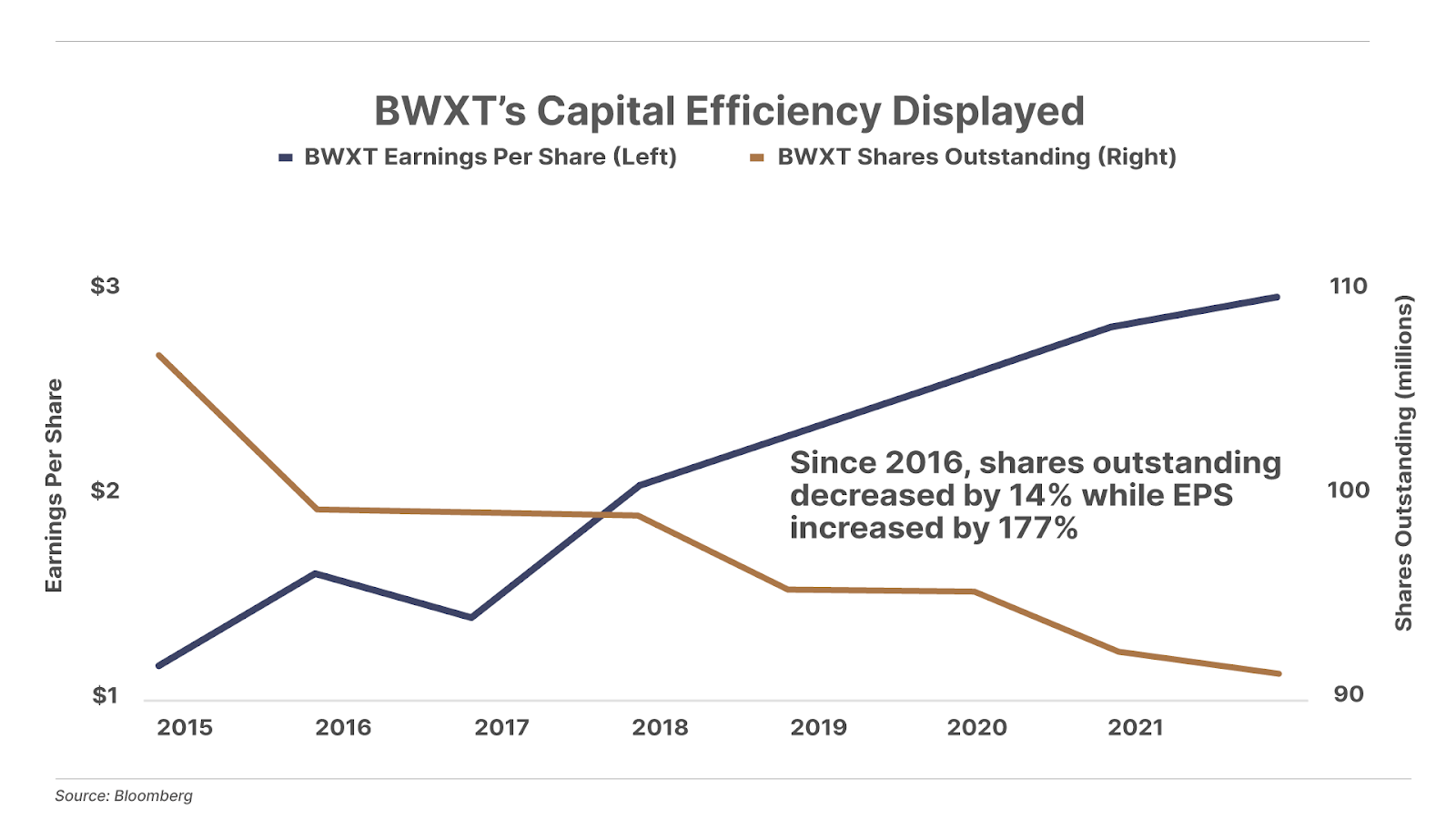

Revenue grew from $1.6 billion in 2016 to $2.2 billion by the end of 2022, while earnings rose from $184 million to $313 million. The company generates roughly $90 million in free cash flow and spends between $100 million to $200 million in capex each year. This free cash flow goes toward a steady buyback program, which has reduced the outstanding share count by 14%, from 105 million in 2016 to 91 million by 2022. (Share buybacks are a tax-efficient way of returning value to shareholders.)

The combination of growing net income and a falling share count has boosted earnings per share from $1.79 in 2016 to a record high of $3.41 through 2022.

The company’s balance sheet is conservatively managed, with $1.3 billion in long-term debt, supported by roughly $400 million in annual operating income. So BWXT offers investors a very stable, recession-proof business that’s well-positioned to thrive in an uncertain economy.

But by far, the most exciting part of this story will come from BWX Technologies’ work on the Project Pele reactor, and its huge upside potential. In June of 2022, BWXT won the design competition for the Project Pele reactor prototype, and received a $300 million contract to build a full-scale version.

The project’s aim: develop a nuclear microreactor for deployment “by road, rail, aircraft, or sea” that was also capable of “quickly being brought on land” and was “inherently safe.” Success would be “a strategic game-changer for the United States, both for the DoD and for the commercial sector,” according to Project Pele manager Jeff Waksman.

BWXT’s vertically integrated approach gives it a leg up over companies that depend on other countries – like TerraPower, Bill Gates’ pet nuclear project, which also features more compact nuclear reactors but unfortunately relies on Russian-produced HALEU fuel.

The Project Pele microreactor received an initial contract of $300 million to deliver up to 5 megawatts of electrical power. But the DoD uses 30 terawatts – that is, 30 million megawatts – of electricity per year, opening the door to enormous revenue growth.

The DoD Strategic Capabilities Office (SCO) partnered with BWXT to build the first advanced nuclear reactor of its kind and further engrains BWXT’s role as a critical military supplier, while bolstering BWXT’s position as a nuclear power pioneer.

Since the beginning of Europe’s energy crisis, it’s been obvious that the world will eventually vastly increase its use of nuclear power. Technology and humanity consistently evolves toward more dense forms of energy. And with each evolution of power technology, human wealth grows exponentially. The next 50 years will almost certainly be the age of nuclear power. There are virtually unlimited applications for the small, safe, and portable reactors that BWXT builds.

For now though, BWXT offers a stable business model that’s recession-resistant, a durable competitive advantage, and the upside kicker of advancing small modular nuclear reactors, first to the military, and potentially to the world.

Excerpted from “A Matter Of National Security,” December 23, 2022

We recommended buying shares of BWX Technologies (NYSE: BWXT) at $58 in December 2022, and they now trade for $150. We had BWX Technologies as a Best Buy from March 2023 to August 2023 for an average return of 116%.

Want to get access to monthly Big Secret recommendations like these? If you pay for just one year of The Big Secret On Wall Street… to celebrate our third anniversary, Porter is offering to cover the cost of your membership every single year after that…

But you need to qualify. Click here to find out if you do.

New to The Big Secret Portfolio? Start With Our Top 3 Best Buys Today

Our goal at Porter & Co. is to bring you world-class investment research, focused on “inevitable” businesses that you can buy and hold forever. This is the surest and safest path to building permanent wealth.

While we don’t believe in timing the market, we do keep a constant eye out for bargains. In each edition of The Big Secret, we highlight three current portfolio picks that are at an attractive buy point. We suggest you focus on these.

Since we began compiling and tracking the performance of the Best Buys in February 2023, the companies on the list have generated a 32.2% return, while the overall market, measured with the S&P 500, has produced a 30.0% return.

To see our latest Best Buys, click here to learn how to subscribe.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.