A True Federal Reserve “Pivot” Will Require More Pain for the Economy and Markets

If you’re new here:

Welcome! You’re reading “Something You Don’t Know,” Porter’s complimentary e-letter. It reveals a hidden market story, or dissects a largely misunderstood element of investing, every other Friday, at no charge. You can see our archive of earlier issues at this link.

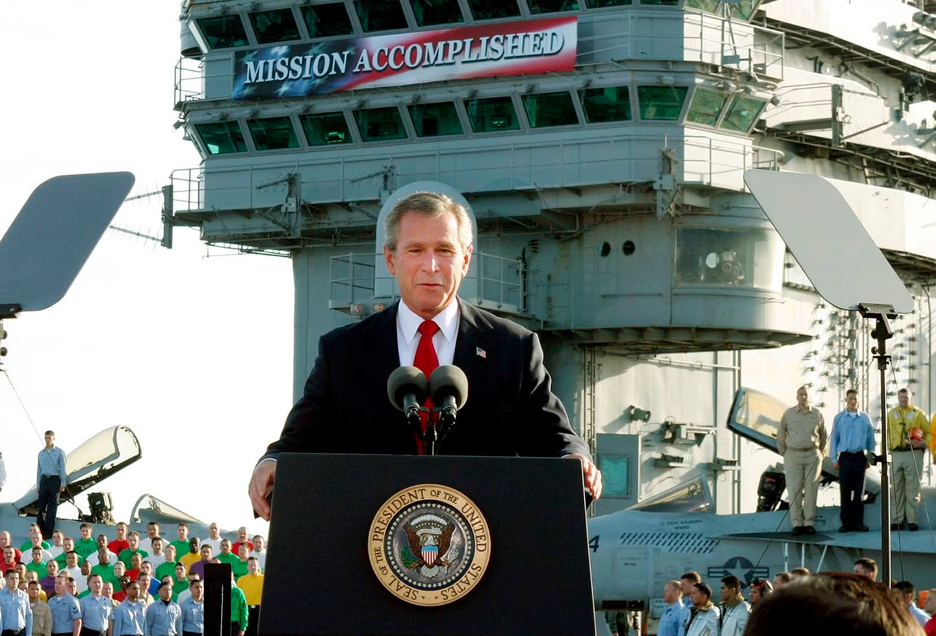

May 1, 2003 was supposed to be a day to remember.

Nearly 20 years later, it’s one former President George W. Bush probably wishes he could forget.

That morning, W.’s plane had touched down on the deck of the aircraft carrier USS Abraham Lincoln, which had recently returned to the San Diego coast, after several months of combat operations in the Persian Gulf.

The president flew that day in the co-pilot’s seat of a Lockheed S-3 Viking jet – dubbed Navy One – rather than his usual Marine One helicopter, becoming the first sitting president to arrive on a carrier in a fixed-wing aircraft. Adding to the middle-aged-man-trying-to-look-cool vibe, he had even donned an official flight suit.

It was all leading up to the White House’s big announcement that afternoon.

Standing at his presidential podium – below a celebratory “Mission Accomplished” banner on the Lincoln – Bush shared the good news: the U.S.-led war in Iraq was over… less than two months after it began.

My fellow Americans: Major combat operations in Iraq have ended.

In the battle of Iraq, the United States and our allies have prevailed. And now our coalition is engaged in securing and reconstructing that country…

It was a declaration that didn’t age well.

It turned out that the real war – rather than being over – had only just begun.

In short, while the U.S.’s “shock and awe” campaign easily bested Saddam Hussein’s forces, the ensuing power vacuum later led to civil war between various Iraqi factions and a prolonged insurgency against U.S. and coalition forces.

After about five more years of fighting, President Bush reluctantly agreed to a withdrawal of all U.S. troops in 2008.

By the time the withdrawal was finally completed in 2011 under President Barack Obama, nearly 4,000 American and coalition troops (and untold numbers of Iraqi civilians) were dead… tens of thousands were injured… and U.S. government coffers were $2 trillion lighter – a cost of nearly $7,000 for every man, woman, and child in America at that time.

W. had vastly underestimated the enormity of the risks facing American troops in Iraq. And this speech, and the now-infamous banner, have become a symbol of U.S. government hubris, and the folly of premature gloating.

Though it’s a very different arena – war and geopolitics versus investing – we think many investors are making a similar blunder today.

The investing public has broadly interpreted the Federal Reserve’s response to last month’s SVB bank failure (which we’ll detail in a moment) as a resumption of quantitative easing (QE) and a return to the bullish, easy-money policies of the past more generally. And they’ve been rushing back into stocks like there’s no tomorrow.

In the roughly four weeks since the Fed stepped in, the broad market has rallied 6%, while technology stocks and more speculative areas of the market have surged as much as 9% or more.

But speculators will likely experience buyer’s remorse on these purchases soon.

The reality is that Fed’s actions could have the near-opposite effect of QE. Instead of easing financial conditions and boosting asset prices, they’ll likely lead to further tightening and hasten the arrival of the impending credit crunch.

To understand why, we need to review how these programs work.

Welcome to “Quantitative Teasing”

In simple terms, QE is just an asset swap between the Fed (or other central banks) and the banking system.

The Fed purchases a security – typically a U.S. Treasury note or bond or mortgage-backed-security (MBS) – owned by a bank or non-bank lender, and in return, that entity receives new reserves (cash) on its balance sheet.

This process injects new liquidity into the financial system. It’s intended to support private sector lending by providing banks with new, unencumbered reserves – thereby supporting economic growth – in addition to boosting asset prices.

QE has arguably provided only modest benefits for the real economy. But it certainly has been a boon for asset prices.

The Fed’s first three rounds of QE – which increased its balance sheet from around $900 billion in late 2008 to over $4 trillion by the end of 2014 – coincided with a 130%-plus rally in the S&P 500.

Following the COVID pandemic, the next round of QE nearly doubled the Fed’s balance sheet (from around $4.5 trillion to almost $9 trillion) in just two years. This more aggressive easing coincided with a similar gain in the S&P 500 of just over 100% in roughly one-third the time of the Fed’s previous scheme (though a couple trillion dollars in government fiscal stimulus likely played a role, too).

The Fed’s recent actions – including “discount window” lending and its new Bank Term Funding Program (BTFP), which we’ll explain below – are types of asset swaps as well. But they differ from QE in some critical ways.

Before the Great Financial Crisis – after which QE and similar market interventions became routine – the traditional role of the Fed and other central banks was to act as a “lender of last resort.” And one of the primary ways the Fed served this role was through its discount window.

The discount window is one of the Fed’s oldest direct-lending facilities. Like QE, it allows banks to swap securities for cash from the Fed. However, this swap comes with some additional “strings” attached.

First, unlike QE, it’s only a temporary swap. In this case, the securities the Fed receives are just collateral – and banks must repay this borrowed cash within 90 days.

Borrowing from the discount window is also relatively expensive. The Fed charges banks interest on these loans. This rate – known as the discount rate – is typically higher than the Fed’s other short-term rates.

As the name implies, the Fed also typically lends at a “discount,” i.e., it gives banks less cash than the securities (collateral) are worth. That adds an extra measure of safety for the Fed in case the bank can’t repay the loan.

Finally, it’s also worth mentioning that unlike QE, the discount window has long carried a stigma in the banking community. As the Richmond Fed noted in an April 2020 brief…

Currently, discount window borrowing remains undisclosed for two years, but there are reasons to believe that use of the discount window can sometimes be inferred circumstantially by other financial market participants.

To the extent that an institution’s discount window borrowing becomes known to other parties, it is possible in principle that those other parties will draw negative conclusions about the institution’s health; if the institution were in good financial condition, the argument goes, it would have borrowed privately at the market rate rather than paying the discount window’s higher penalty rate.

The fear of such a stigma would make institutions that need liquidity more reluctant to borrow from the discount window — a reluctance that could work against the program’s purposes.

For these reasons, banks generally avoid borrowing from the discount window unless absolutely necessary.

More importantly, because these short-term liquidity loans are collateralized and must be repaid (with interest), they generally don’t represent new reserves for the banking system – and thus do not support private sector lending and economic growth – like QE is meant to do.

The Bank Term Funding Program (BTFP) is a new facility introduced by the Federal Reserve following the SVB failure last month.

Like the discount window, it allows banks to borrow money from the Fed for a predetermined time at a predetermined interest rate. But its terms are less onerous.

First, it does not require banks to take a discount on their collateral. In fact, it allows banks to pledge Treasury bonds and MBS to the Fed at par value, even if they currently trade for less.

Second, it allows banks to borrow cash for up to one year, rather than just 90 days like the discount window.

This program enables banks to receive cash for these assets without having to immediately realize the significant losses on their bond portfolios (thanks to the Fed’s aggressive rate hike campaign over the past year).

As a result, it should prove to be slightly more positive for liquidity than traditional discount window borrowing. But it is still a far cry from QE.

Most notably, banks are still required to pay relatively high interest rates on this cash – well in excess of what they’re currently earning from their loan books on average – and will ultimately have to repay these loans to the Fed.

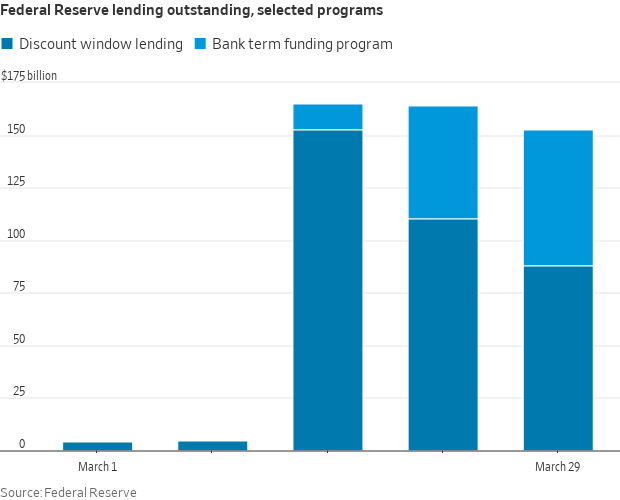

Banks have borrowed more than $150 billion through these two programs alone over the past several weeks.

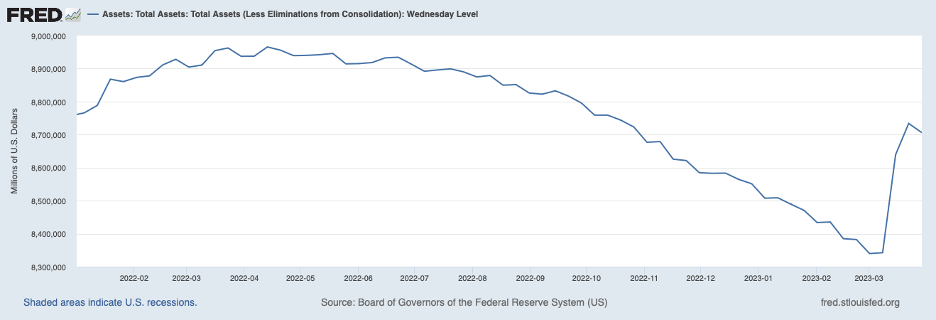

Along with a handful of additional lending programs, these measures have expanded the Fed’s balance sheet by over $300 billion to date.

This increase has effectively erased half of the decline in the Fed’s balance sheet over the past year (via quantitative tightening [QT]). It now sits above $8.7 trillion after falling to a multi-year low of less than $8.4 trillion in early March.

This reversal in the Fed’s balance sheet is stunning. But make no mistake… It does not represent QE in its traditional sense.

Again, the bulk of this increase is from temporary emergency lending programs. And because these loans are collateralized and must be paid back, banks are unlikely to use this liquidity to support loan growth in the real economy. That’s a sugar-and-salt difference from the “money for you and you and you” approach of QE, which has benefitted markets in the past.

In short, as financial journalist Greg Barker put it recently, compared to actual quantitative easing, these measures are better described as “quantitative teasing” – similar in appearance but without the overt stimulatory effects of the real thing.

Why BTFP is Not a Reason to BTFD (“Buy the F@%$^#& Dip”)

Judging by some recent headlines in the financial media, and the outsized rally in risk assets over the last several weeks, hopeful traders see BTFP as the new QE and are eager to hop back on the speculation train.

Yet wishful thinking aside, these programs are unlikely to provide much benefit to markets or the economy.

That’s because they don’t solve the banks’ problems – which we explained to The Big Secret on Wall Street subscribers last month – and, as we mentioned earlier, they don’t actually pump new liquidity into the economy like QE.

At best, these programs will merely buy the Fed time – so that it can continue to raise rates in an attempt to slow the economy and bring down inflation without creating another financial crisis.

We doubt the Fed will be successful. (And as we’ve explained, any reprieve from inflation is likely to be temporary at best). But even if these programs can stave off an immediate crisis, they won’t prevent banks from restricting credit… to each other, to businesses, and to consumers.

In fact, this process already appears to be underway.

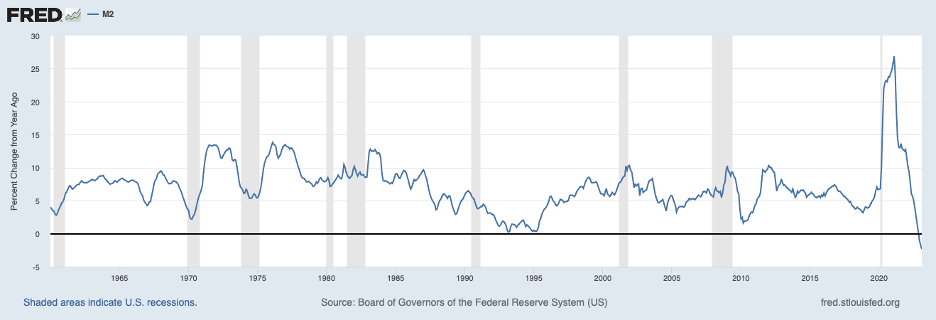

The latest data show that the U.S. money supply is contracting on a year-over-year basis for the first time since at least the 1960s.

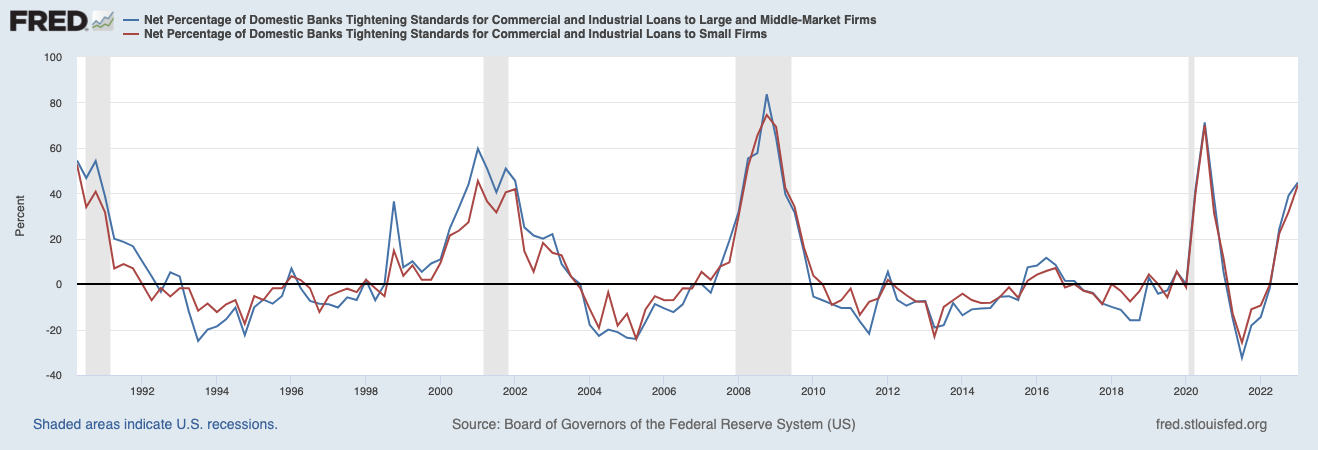

Meanwhile, the Fed’s latest senior loan officer survey showed the net percentage of banks tightening lending standards on commercial and industrial loans has already risen to recessionary levels.

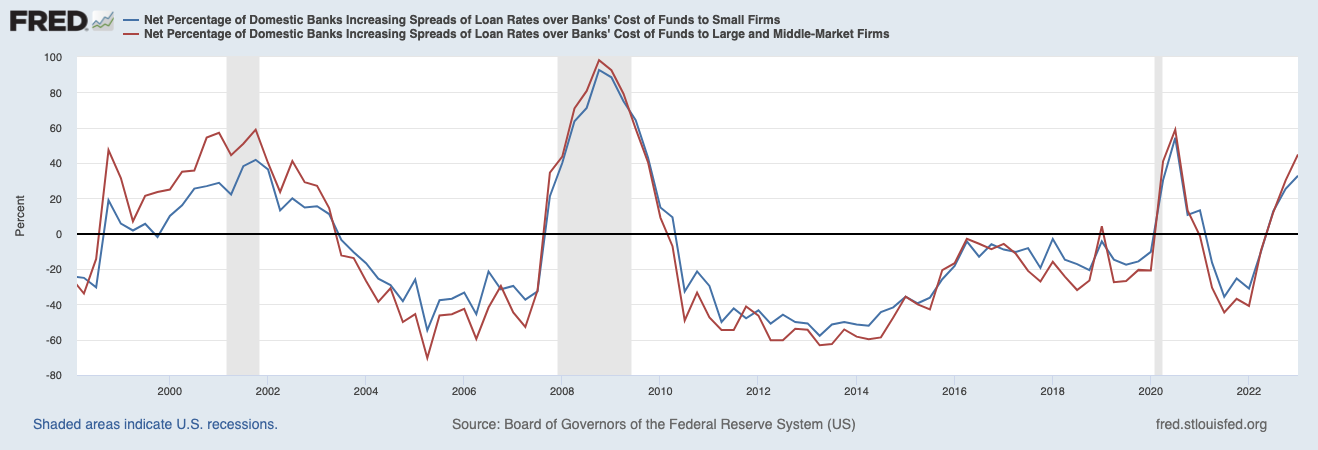

The percentage of banks increasing spreads over their funding costs – essentially building up a capital cushion in the event of future write-downs – has also risen to near-recessionary levels.

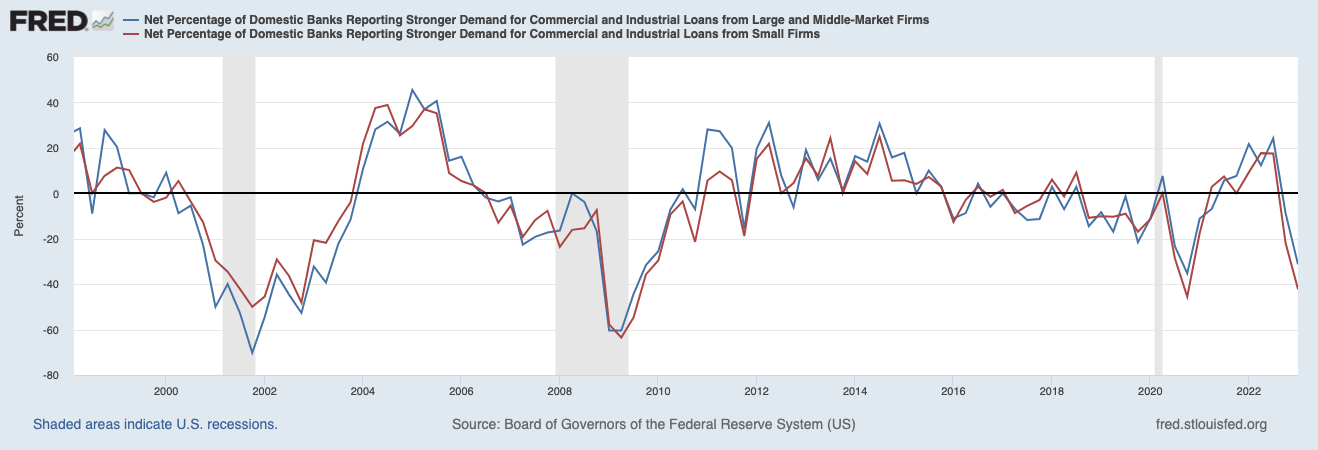

Finally, the percentage of banks reporting stronger loan demand has also plummeted to levels last seen during the depths of the COVID crisis.

These signals suggest the Fed is already sowing the seeds of a significant credit contraction in the banking system. It’s now simply a matter of time until this slowdown works its way through the rest of the economy and, ultimately, the markets, via falling corporate profits.

The Destination is Clear, But the Path is Not

Of course, as we’ve explained, all roads ultimately lead back to the only remaining solution for the Fed and the U.S. Treasury (along with most other Western governments): more money printing.

So, we do expect the Fed will eventually resume (and expand) QE in some form or another.

But it’s critical to understand that the Fed – like all central banks and governments in general – is reactive by nature. Historically, it has only taken significant action in response to significant problems… not in anticipation of them.

That means we’re likely to see a return to easy-money policies only after the U.S. economy slows dramatically enough to bring down inflation temporarily… or we experience a severe market crisis that forces the Fed to respond. And history suggests either of these scenarios will likely be bearish for most risk assets.

In other words, piling back into speculative, overpriced stocks probably isn’t the wisest choice right now. Yet, that’s exactly what many investors have been doing.

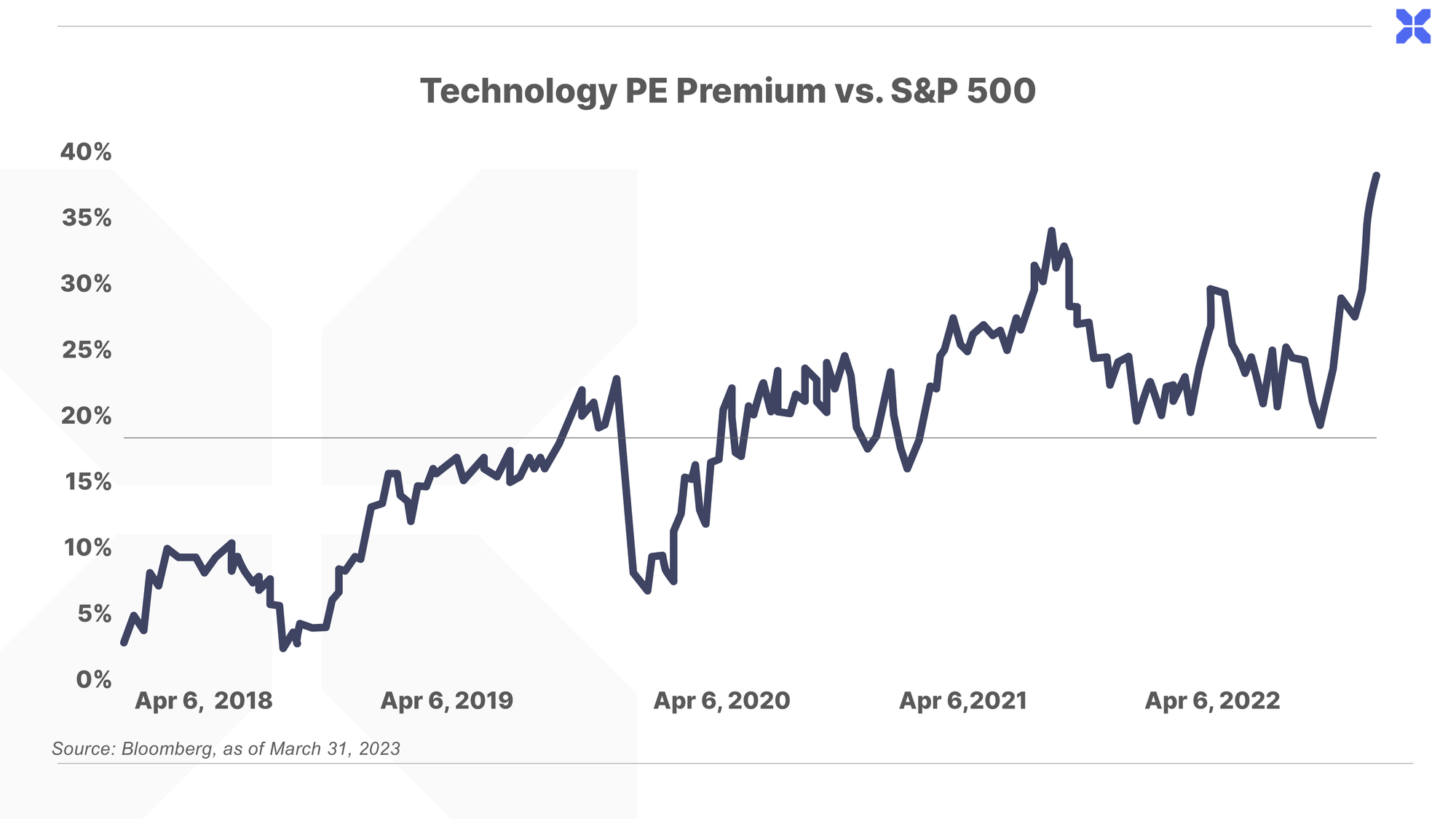

There may be no better example than the technology sector, where unbridled buying has pushed relative valuations to absurd extremes. Tech stocks are now trading at a nearly 40% premium to the overall market, which is even higher than at the peak of the post-COVID bull market in 2021.

These stocks are priced for perfection, which means that anything less – let alone a severe recession or outright financial crisis – could create devastating losses for anyone holding them.

Instead, we believe investors would be wise to position their portfolios to weather a near-term deflationary crisis while also preparing for the inflation that’s likely to emerge when the Fed inevitably resumes easing.

Last week, paid subscribers of The Big Secret on Wall Street learned about a unique two-part investment strategy designed to do just that. It combines a little-known investment vehicle managed by one of the best distressed-debt investors on Wall Street with a powerful long-term hedge against inflation. Click here for access.

Porter & Co.

Stevenson, MD

P.S. If you’d like to learn more about the Porter & Co. team – all of whom are real humans, and many of whom have Twitter accounts – you can get acquainted with us here.