Issue #131, Volume #2

When Junk Is Winning, Run Far, Far Away

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Buffett’s words of wisdom… Cutting Michael Jordan… Quality versus junk… What happens in market manias!… Looking at data back to 1956… Peak oil still a myth… Venture Global gets more deals… A 50-year mortgage?… |

In his 1996 shareholder letter, Warren Buffett gave away many of his greatest secrets.

He wrote about the importance of time (inactivity):

We continue to make more money when snoring than when active.”

While humans have emotional and biological urges for action, the very best investment policy is almost always to do nothing.

He explained the supremacy of quality businesses:

The art of investing in public companies successfully is little different from the art of successfully acquiring subsidiaries. In each case you simply want to acquire, at a sensible price, a business with excellent economics and able, honest management.”

He explained the extreme power law (Pareto’s Law) in the markets by comparing great businesses to basketball great Michael Jordan.

When carried out capably, a [high-quality] investment strategy will result in its practitioner owning a few securities that will come to represent a very large portion of his portfolio… To suggest that this investor should sell off portions of his most successful investments simply because they have come to dominate his portfolio is akin to suggesting that the Bulls trade Michael Jordan because he has become so important to the team.”

And he explained one of the attributes of long-lived, high returning investments: a moat unlikely to be threatened by technological change.

You will see that we favor businesses and industries unlikely to experience major change. The reason for that is simple: Making either type of purchase, we are searching for operations that we believe are virtually certain to possess enormous competitive strength ten or twenty years from now. A fast-changing industry environment may offer the chance for huge wins, but it precludes the certainty we seek.”

He labeled these kinds of investments “inevitables,” and savvy subscribers will notice how I’ve slavishly adopted these ideas as my own with many of my best, all-time recommendations: The Hershey Company (2007), Microsoft (2012), W.R. Berkley (2012), American Express (2016). And I’m sure you’ve noticed that trend has continued at Porter & Co., with what will become the greatest recommendations of my career: Philip Morris International (2022), Domino’s Pizza (2023), Deere & Co. (2023), Diageo (2023), and Kinsale Capital (2024), among others.

But… Buffett’s greatest secret of all was published 10 years earlier.

In his 1986 letter, Buffett wrote:

Be fearful when others are greedy, be greedy when others are fearful.”

This advice is critical because, as I’m sure you’ve noticed over time as an investor, the value of a public company’s earnings vary depending on the mood of the market. Sometimes investors will pay 25x earnings. And sometimes, not much over 10x earnings – even for great businesses.

As Buffett reminded us in 1996:

You can, of course, pay too much for even the best of businesses… Investors making purchases in an overheated market need to recognize that it may often take an extended period for the value of even an outstanding company to catch up with the price they paid.”

Buffett’s greatest secret – to be fearful when others are greedy and to be greedy when others are fearful – is largely ignored because, first of all, a frothy market that’s going higher virtually every day looks like the best time to make a lot of money in stocks.

Plus, it can be very difficult to know if stocks are trading at high valuations because their prospects are legitimately improving. Ironically, that was the case in 1996, when Buffett gave this warning. It was the beginning of the internet era, an incredible period where computer and communication technologies vastly increased productivity – permanently. The market was rationally discounting the long-term impact of improved margins and returns on investment. Buffett was wrong.

Sure, sometimes – like virtually anytime CNBC is running a “market crisis” special, or when the CBOE Volatility Index (VIX) is soaring over 30 – it’s obvious when people are fearful. It was a lay up on March 24, 2020 – after the market had fallen farther and faster than any other time in history – that now was the time to make major investments in great companies. (At Stansberry Research, I hosted a webinar on that day, urging subscribers to make their largest-ever commitments to the market.) Likewise, at the bottom of the market in late 2008 / early 2009, it was very easy to find once-in-a-lifetime values.

So knowing when to buy isn’t nearly as hard as knowing when to lighten up. And selling too early can be far more dangerous than doing nothing (Buffett’s First Law). If you’d sold out of stocks in 1996, you would have missed out some of the very best gains in the history of the market.

If only there was a way to know if, even at higher multiples, the market was still behaving rationally…

And, there is.

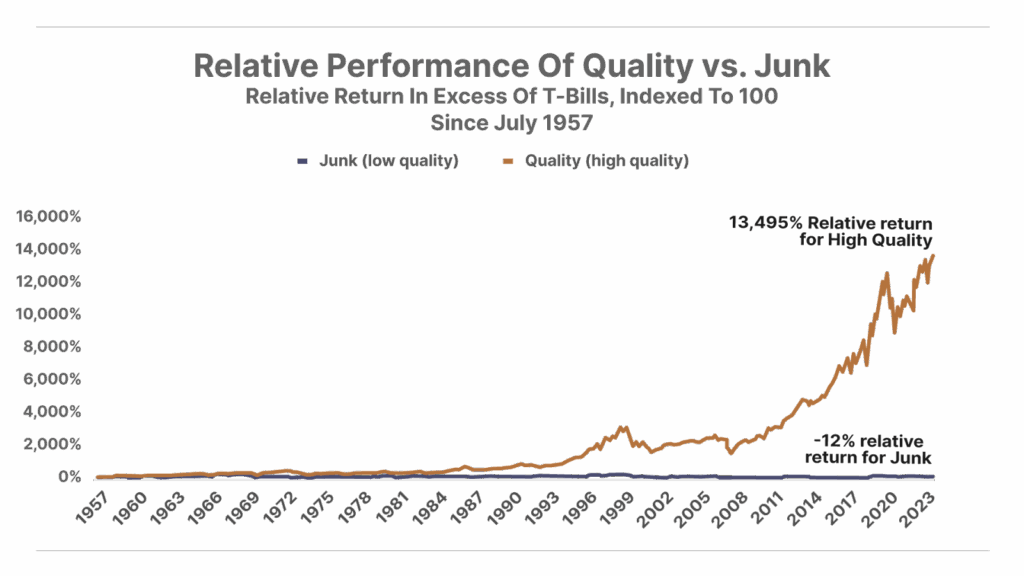

In 2013, Cliff Asness, Andrea Frazzini, and Lasse H. Pedersen wrote a seminar paper, Quality Minus Junk, that was later (2015) published in the Review of Accounting Studies.

I’ll assume you missed that issue.

What their paper showed was that investing in high-quality businesses produces real, sustained alpha. That is, buying high-quality “inevitable” businesses, like the ones Buffett prefers, will deliver high returns over long periods of time, even after controlling for many other variables, such as volatility. And not only that, but the effect was consistent across the quality scale: the higher the quality of the business, the higher the value of the business in the market.

This [quality] coefficient implied that a one standard deviation change in a stock’s quality score is associated with a 22% increase in its price-to-book.”

This, of course, makes perfect sense. A company that’s capable of earning higher returns on its equity (over sustained, long periods of time) is worth more than another company with the same amount of net assets that’s producing only average returns.

Thus, over time, the highest-quality businesses should outperform the lowest-quality businesses. And they do. By about 4% a year, which is an enormous edge over time.

To measure this accurately, Cliff Asness and his team at AQR Capital Management divided up all of the stocks in the market into 10 separate quality-sorted portfolios. Thus, across the entire stock market, all stocks were sorted into 10 quality-ranked deciles.

This research begins with the U.S. stock market in 1956 and continues (updated on AQR’s website) every month. These portfolios are value-weighted and rebalanced every calendar month to maintain their accuracy. Quality is defined as the top two portfolios of the quality deciles. And “junk” is defined as the bottom two portfolios of the quality deciles.

The difference in the performance of these portfolios – Quality Minus Junk – is known as the QMJ factor. It simulates the performance of buying the quality stocks and shorting the junk stocks. And the result is extraordinary: annualized returns of almost 4% a year.

The point isn’t that you would simply mimic this strategy. No, the point is that the market should be more efficient than these numbers imply. Simply buying quality shouldn’t consistently produce higher returns than buying “junk.” The market should be able to handicap future relative returns more accurately. Quality should cost more, and junk should cost less.

This study gives a lot of statistical evidence to support my personal preference for only owning truly great businesses. Even when you buy them at average market prices, they are very likely to outperform the market.

But there’s one other very important thing the study revealed.

While most of the time the market rewards investment in high-quality stocks, from time-to-time, investors lose their minds. During these periods, the market behaves irrationally and the opposite occurs: junk consistently outperforms quality.

Can you guess when this occurs? During market manias.

From 1998 through 2000, junk outperformed quality, with quality losing -0.3% a year. During the crypto-fueled meme-stock mania in 2020-2021, quality lost again, by -1.1% annually.

If you want an objective measure of whether or not the market is behaving rationally, just look at the relative performance of AQR’s quality-versus-junk portfolios, commonly known as the QMJ factor.

So far this year, quality is beating junk by 4.2%.

Stocks are expensive. But the market isn’t irrational.

The Corner Of The Market No One’s Watching

Presented by Jared Dillian Money

While the herd chases AI and crypto, former Lehman trader Jared Dillian— ranked among Porter Stansberry’s top three favorite newsletter writers — is focused on an unassuming, cash-rich corner of the U.S. market…

The same corner that outperformed by thousands of basis points after the dot-com bubble burst.

This area is still off CNBC’s radar (for now). But last time investors ignored it, the S&P, and their portfolios, were cut in half.

The next rotation has already started. This time, the opportunity could be even bigger.

Click here for full details on this developing story.

Three Things To Know Before We Go…

1. The “clean energy” hype is fading. The International Energy Agency (“IEA”) – the Paris-based “energy security watchdog” that ironically has been one of the biggest pushers of anti-energy security propaganda in the name of the climate crisis – is walking back its forecast for slowing oil and gas demand. In a report published this morning, the IEA said it now believes the world will continue to use more oil and gas through at least 2050, after previously forecasting that “peak oil demand” would arrive no later than 2030, while also calling for an end to all new investment in oil, gas, and coal projects, as recently as 2023. Porter called foul on “peak oil” more than a decade ago… good that IEA is slowly catching up.

2. Leading Japanese trading firm signs a 20-year agreement with Venture Global. Yesterday, liquefied natural gas (“LNG”) exporter Venture Global (NYSE: VG) announced a 20-year deal with Mitsui & Co. (OTC: MITSY) for the purchase of 1 million tonnes per annum (“MTPA”) of LNG starting in 2029. The Mitsui deal follows recent long-term LNG agreements Venture Global has signed with fellow Japanese energy majors JERA and Osaka Gas, as well as Monday’s announcement of a 20-year, 1 MTPA supply contract with Spain’s Naturgy beginning in 2030. Securing these strategic contracts demonstrates strong buyer confidence in Venture Global’s reliability, cost leadership, and growing influence in global LNG markets. The company’s core business fundamentals remain exceptionally strong, and the Mitsui agreement serves as a clear endorsement of its long-term growth trajectory.

3. The Trump administration mulls new offshore oil and gas leasing. Yesterday, reports surfaced that the U.S. Interior Department will auction new offshore oil and gas drilling leases along the U.S. coastlines. The move could provide a lifeline to Sable Offshore (SOC), which has faced a series of legal roadblocks in restarting oil production at its Santa Ynez Unit production facility, off the California coastline. Sable remains a high-risk, but potentially high-upside opportunity. While we no longer formally recommend the shares in our Complete Investor portfolio, we’re keeping it on our radar in case it gains regulatory approval to produce and transport its oil to market.

And One More Thing… Housing Affordability And Today’s Poll

Policymakers are floating ideas like 50-year mortgages and looser credit and debt-to-income rules to boost homeownership. The goal is to open the market to first-time buyers, many still burdened by student loans. Longer terms may lower monthly payments, but they also mean decades more interest and slower equity accumulation. These plans are financial novocaine: they numb the pain temporarily, while the real problem – lack of housing supply – remains untouched. To make housing (or college) more affordable, require homebuilders (or the colleges) to provide the loans. Keep the government out of the deal. That would make sure that only qualified borrowers (and talented kids) got access to loans.

Tell us what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.