Issue #62, Volume #2

And That’s Not Necessarily Good News

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| The ridiculous idea of Peak Oil… There is plenty of oil and there always will be… OPEC has lost control of the market… the huge disparity between oil prices and gold prices is a warning… There’s too much speculation in gold and Bitcoin… The tariff roller coaster continues… |

By 2008, American oil production had been falling since 1970.

That year, America barely produced 5 million barrels of oil per day – down by 50% since the early 1970s.

I’m sure you will remember, with falling production came the inevitable Malthusian nonsense: Peak Oil.

Like “killer bees,” global warming, the “population bomb,” and Y2K, Peak Oil was also a ridiculous idea that publishers used to scare the bah-jesus out of people to sell newsletters. Some of my less-credible peers even called themselves “Mr. Peak Oil.”

The funny thing about all these neo-Malthusian ideas is, while they might sound plausible, all of the actual evidence proves that they are completely wrong.

As early as 2006, I was predicting a renaissance in U.S. oil production because I knew that higher prices would drive new discoveries and innovation in production. The Peak Oil wingnuts shouted me down at conferences.

But, guess what? Economics won, again. Shocker.

By 2009, my best contact in the oil and gas industry, Cactus Schroeder, was telling me about a huge new field (the Eagle Ford) that was going to produce unprecedented amounts of crude oil. He also explained that these new kinds of oil fields – driven by revolutionary new production methods like horizontal drilling and fracking – meant an end to dry holes and vastly more capital efficient discovery.

Porter, you wouldn’t believe it… we took that six-inch horizontal pipe and we replaced it with a 12-inch pipe…”

Cactus, let me guess,” I interrupted. “Production increased by four-fold.”

How’d you know that?”

It was obvious to anyone who knew what was happening in the fields that U.S. oil and gas production was going to boom. I remember being at a conference in Las Vegas with commodities expert Rick Rule in 2010 or 2011. Rick was, of course, saying he thought natural gas was pretty cheap at $3. I said, “Anyone who is buying gas here should have their heads examined. There’s no question gas is going below $2 and oil is going below $40.” We made a bet about gas prices.

I won.

And Rick is a man of his word: I got a case of first-growth Bordeaux.

It took 44 years for U.S. oil and gas production to double after World War II. That was the primary economic engine that drove America’s incredible prosperity in the 1950s and 1960s. Well, guess what? This time production doubled in only eight years: from 2011 to 2018.

If you knew, like I did, that oil production was going to boom, it wasn’t hard to figure out how to make a lot of money.

I went on to make three of the best recommendations of my career: Targa Resources (TRGP, which was exporting propane before crude-oil exports were legalized), Cheniere Energy (LNG, which was exporting liquefied natural gas before crude-oil exports were legalized), and Texas Pacific Land (TPL, which was sitting on an ocean of oil).

Since the very beginning of the oil industry, the “problem” has always been (and will always be) that there’s an economically unlimited supply of crude oil available. Since the very beginning (Standard Oil), the industry has always organized cartels – like the Texas Railroad Commission – to limit production.

Today, however, the primary oil cartel has lost control of the market.

That’s because the world’s marginal suppliers are small, independent producers in the Permian Basin in west Texas and New Mexico. Unlike the major oil companies (which can handle lower prices because it increases their margins on refined products), these smaller producers can ramp up production quickly when prices go above about $80 per barrel, and, likewise, they will shut down production gradually as prices go below $60.

Today, in an attempt to regain market share, OPEC+ is ramping up production despite the lower prices. They’re trying to force the smaller, independent producers to cut production. And, as a result, U.S. production is likely to drop. Maybe by a lot.

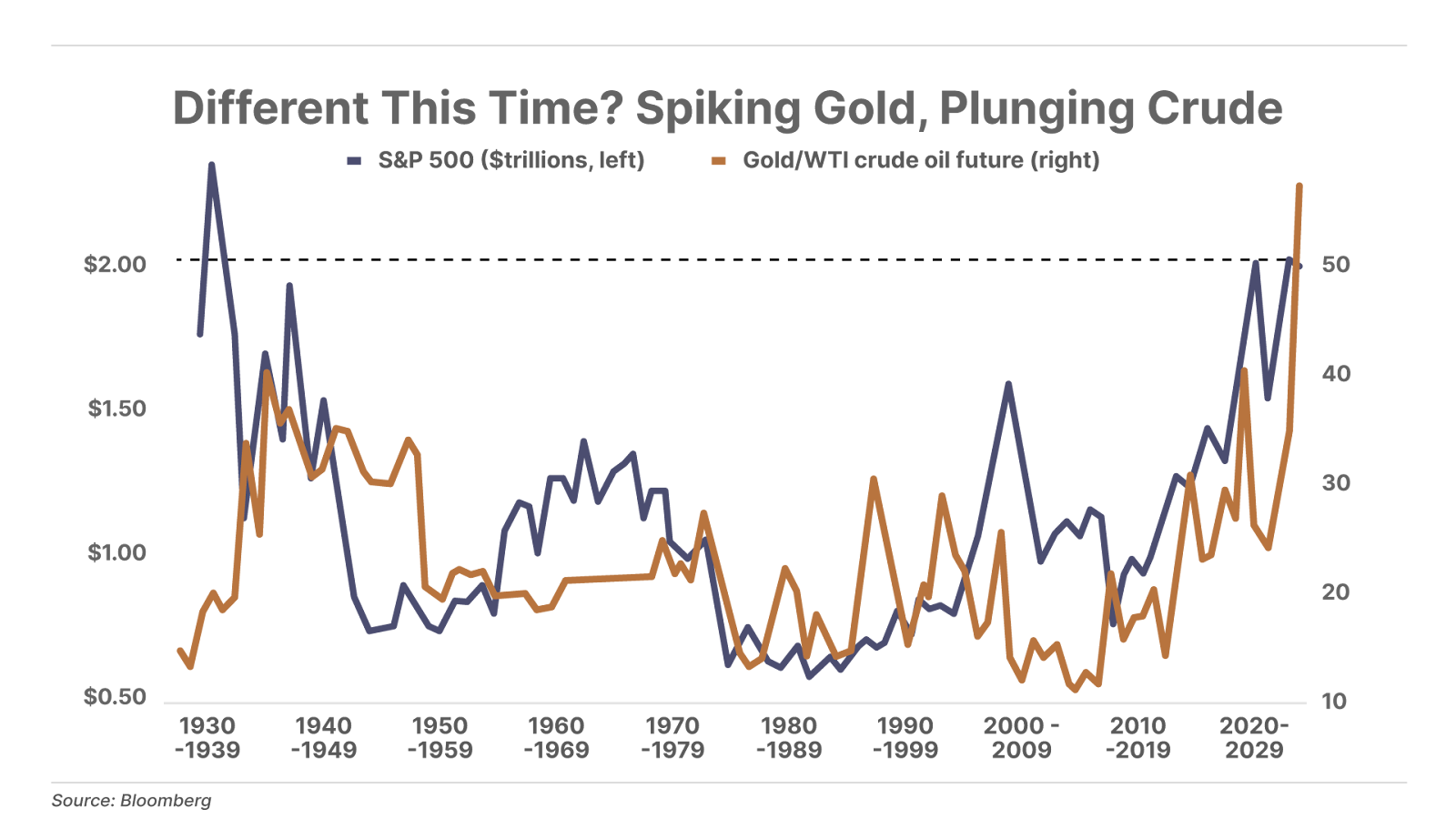

To really understand how cheap oil has become, consider this pretty remarkable chart: measured against gold, oil has never been cheaper than it is today.

The last time the gold-to-oil ratio was this out of balance was in mid-2008, just before the financial crisis. It happened because there had been a huge amount of credit inflation (the mortgage bubble) and oil production had been in decline for a long time. The result was a huge speculative bubble in oil prices, which shot above $140 per barrel.

Today, we have a similar situation – but in reverse.

Now, the bubble is in gold and Bitcoin – not in oil.

There’s been a huge – an enormous – credit bubble in sovereign bonds. And the production of Bitcoin (and gold) has been falling for a long time. Of the 21 million Bitcoin that will eventually be mined, over 19 million have already been produced. Gold production continues to grow – 2024 saw a new global production record: 3,661 metric tons. But, even so, that’s less than 2% of the existing gold in the world. So when a lot of capital moves into gold, there isn’t nearly enough new production to meet demand. That means the price is going to go up.

What’s driving all of this gold and Bitcoin buying is, of course, America’s outrageous spending and the debt (and money printing) that’s financing all of it.

Nobody sees this coming yet, but, eventually (and I can’t know when) the sovereign bond bubble is going to burst. America is going to default on its bonds. Nobody wants to even think about that… but it’s going to happen. It happened in the 1930s. And it happened in 1971. And it’s going to happen again.

I think the huge disparity between oil prices and gold prices is a warning.

There’s far, far too much speculation in gold and Bitcoin. And it’s not going to last forever. At some point in the future, all those Bitcoin bros are going to wish they owned an oil well, not a Bitcoin server.

While these kinds of changes take decades to play out, it’s very clear to me that this is a good time to be a buyer of high-quality oil reserves.

Three Things To Know Before We Go…

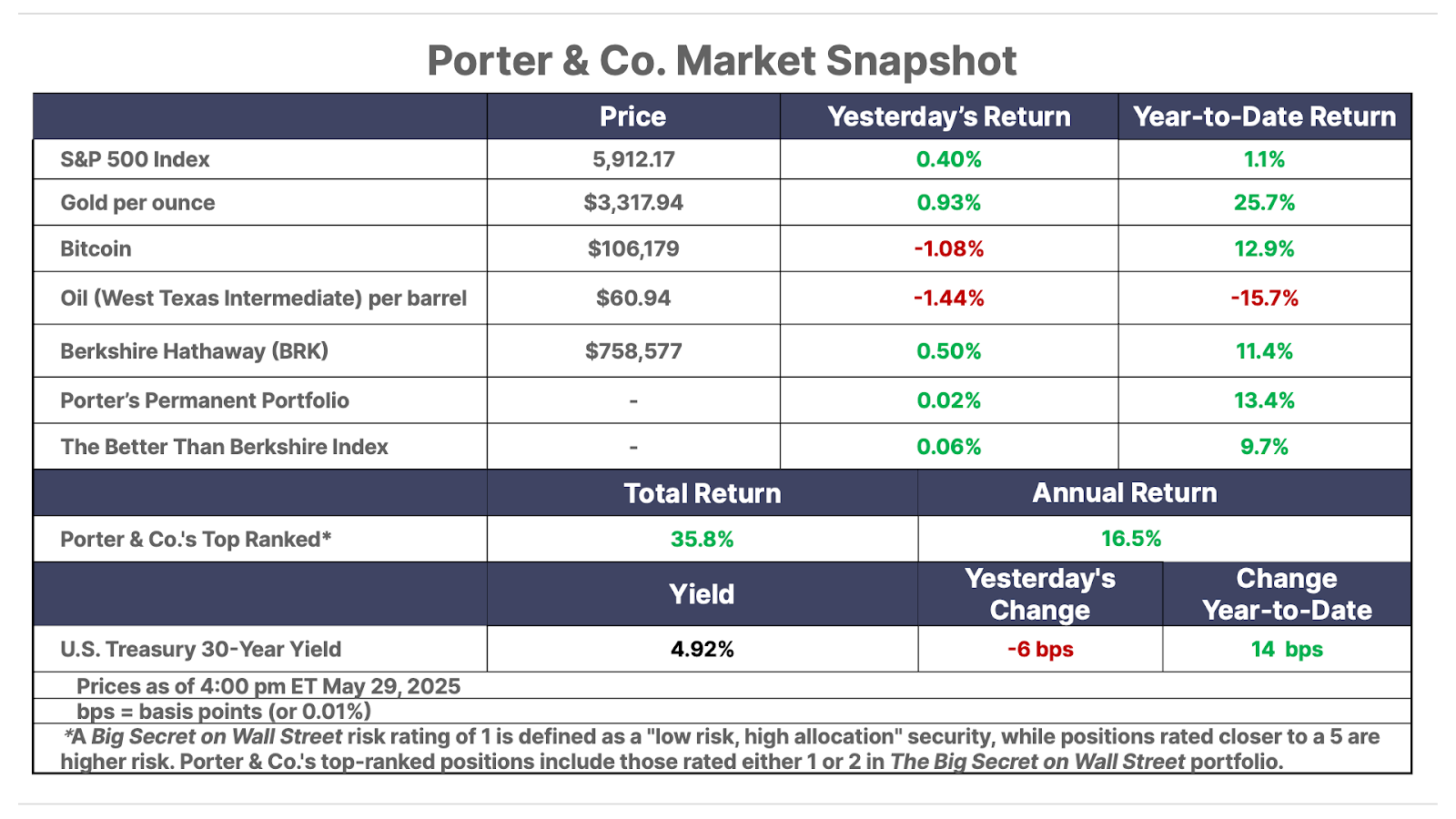

1. OPEC+ unleashes the production floodgates. Oil prices dropped on a Reuters report that the OPEC+ cartel may agree at its Saturday meeting to boost production by 411,000 barrels per day in July. Two sources noted that the group may also discuss a larger increase. This flood of production into an already-oversupplied market indicates the growing risks of an oil price war. We previously warned about this in the May 22 Big Secret On Wall Street, along with several ideas for how investors can capitalize on lower oil prices.

2. The tariff roller coaster rolls on. On Wednesday evening, the U.S. Court of International Trade ruled that President Donald Trump’s “Liberation Day” tariffs are illegal. On Thursday morning, the U.S. District Court for the District of Columbia followed this up by blocking the president’s authority to unilaterally impose tariffs – at all – seemingly putting the Trump administration’s broad trade policy in question. However, shortly after that ruling, the U.S. Court of Appeals for the Federal District granted the president’s request to put a temporary hold on Wednesday’s judgment as the White House appealed these rulings. Finally, this was all followed by President Trump’s Truth Social post this morning, accusing China of violating its recent temporary trade deal with the U.S., suggesting the trade war could soon be ramping up again.

3. CEO confidence suffered its steepest drop on record. The Conference Board’s Measure of CEO Confidence fell by 26 points in the first quarter – the largest quarterly decline in the survey’s 49-year history. The index now stands at 34, its lowest level since Q2 2022, reflecting mounting concern over President Trump’s volatile trade policies and resulting political instability. Trump’s trade policies change on a daily – sometimes even hourly – basis, eroding the CEO’s visibility into the future and heightening fears of economic disruption. To make matters worse, 83% of CEOs surveyed expect a recession within the next 12 to 18 months. If tariff uncertainty continues and businesses pull back on hiring and investment, the slowdown could arrive sooner – and hit harder – than many anticipate.

And One More Thing… The Trading Club Launches

Porter & Co. just kicked off The Trading Club with our inaugural tranche of trades in a funded $100,000 live account. This afternoon, we collected $4,140.80 in premiums from selling options on a list of world-class businesses. We reinvested a portion of those proceeds into a call-option trade that we believe could have 10x to 15x upside over the next 18 months. It’s not too late to join us – all of these trades are still actionable now – but you only have until midnight tonight to become a member.

Click here to get started now.

Today’s Poll… Where Will Bitcoin Go?

Tell me what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

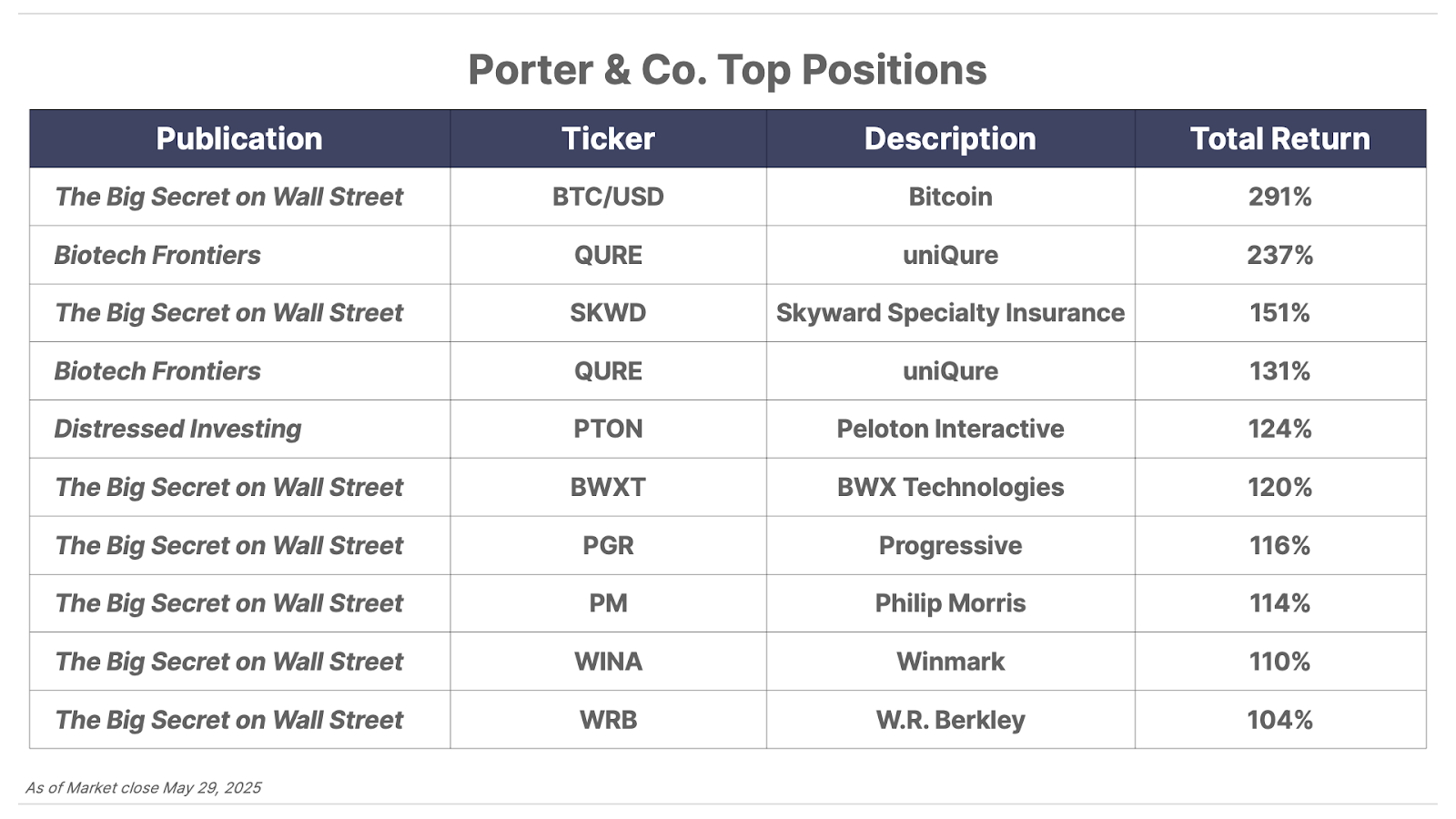

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.