Issue #57, Volume #2

Answering Your Toughest Questions About Berkshire

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| For 50 years, buying shares of BRK was a risk-free way to beat the market… Questions about the portfolio: first about Berkshire’s cash… What about gold and Bitcoin?… Why didn’t you include entry prices?… The U.S. gets a rating reduction… |

I knew when I decided to critique Berkshire Hathaway publicly, there would be consequences.

For more than 50 years, investing in Berkshire Hathaway was a virtually risk-free way to beat the market. Long-term investors have been unbelievably enriched. And there’s no question that Warren Buffett was the greatest investor to ever live.

But, and it’s a big “but,” Berkshire’s primary edge – Buffett’s ability to invest its enormous insurance “float” in the public markets – has virtually disappeared over the past 25 years as the company has become one of the largest in the world. Berkshire is like the whale that ate the world. Berkshire now holds a third of its assets ($330 billion) in cash because making outstanding investments in the public markets at Berkshire’s scale is extremely difficult.

How difficult? Well, if Berkshire decided to allocate 100% of its cash into the stocks of the S&P 500 and it started with the smallest of these 500 businesses, it could buy every single outstanding share of 476 companies. Berkshire has evolved from a world-class property and casualty insurance company with a best-of-breed public equity portfolio into the world’s largest conglomerate.

And, like it or not, large conglomerates usually perform poorly. Look at GE at its peak in 2000, when it was the largest publicly traded business in the world.

Berkshire’s enormous size (around $1 trillion market cap) and its heavy commitments (roughly $200 billion) to capital intensive and highly regulated businesses (BNSF Railway and Berkshire Hathaway Energy) make it virtually certain that Berkshire will underperform the S&P 500 going forward. And then there’s this: Berkshire is at tremendous risk of suffering a major loss (potentially $40 billion+) in its power business.

Last September, Ajit Jain, who has run Berkshire’s insurance companies since 1986, sold half of his Berkshire shares in an unprecedented move. Historically, nobody sells Berkshire.

My job is to make sure that you recognize these risks. If you’ve used Berkshire as a de facto substitute for the S&P 500, it’s time to change your strategy. And on Friday, I published a fully allocated portfolio of stocks that’s Better Than Berkshire. While the asset allocation mimics Berkshire’s (absent the cash), each of these publicly traded companies is superior to its Berkshire analog.

Boy, did that kick the hornet’s nest…

It also confused a lot of you. So today, I’m taking all of your questions. I hope this helps you understand what I’ve done, why I’ve done it, and how you might put this information to work in your investing.

First, about Berkshire’s cash:

I understand your choice of companies to align with Buffett’s portfolio, but you stopped too short. You did not address a very significant component – Buffett’s $325 billion of cash.

– Paid-up subscriber Ed”

Porter’s comment: That’s quite correct, Ed. What I’ve done is create a Better Than Berkshire index that could be used to create an equity portfolio. If you want to create your own version of Berkshire, including the cash, then you’d simply reduce these allocations about 30% each to mimic Berkshire’s cash holdings.

Kind of schlocky:

I thought the idea to create a homemade alternative to BRK was interesting but I found the execution to be kind of schlocky. What I’m wondering is if this was done because of a “you get what you pay for” attitude, being that it was given away in the free Journal.

– Paid-up subscriber David”

Porter’s comment: No, that wasn’t the impact I was trying to achieve, certainly. I can tell you that the resources (the compute power) and the effort behind the Berkshire analysis was the most intensive work I’ve ever done as an equity analyst. I also think it’s wholly original: I haven’t seen anyone critique Berkshire this thoroughly, ever. I wouldn’t want to be your cat.

I don’t have years or decades to invest:

What is hard about coming into the investment arena at this moment is the reality that I cannot invest into the companies you have held for years or decades.

– Paid-up subscriber Roger”

Porter’s comment: I disagree. Every investor is faced with the same challenge, every year of their lives. You have a certain amount of “risk” capital – money that you’re willing to put at some risk in an equity investment. Your job is to earn the highest possible return on that capital each year. However, most investors are wholly unrealistic about what returns are likely and what risks are inevitable. Earning 12% to 16% on average is the very best you’re likely to achieve without taking extraordinary risks. Following our best advice (our highest-rated stocks) and our “Best Buys,” you will be able to earn 15% to 20% annually, which is an extraordinary return. Using this Better Than Berkshire approach (without any cash component) will likely perform around 15% annually, on average.

What about gold and Bitcoin?

I reviewed the portfolio you created to beat Buffett with great interest. I was surprised you had no allocation to gold, even Franco-Nevada (FNV) or to Bitcoin. Especially since Franco-Nevada is one of your “Best Buys.” I thought in the past, you’d said that 10 to 15 stocks was the most a person could manage… Following these recommendations amounts to buying over 30 stocks. Is that what you are suggesting?

– Paid-up subscriber Judy”

Porter’s comment: Buffett famously has never invested in gold or Bitcoin, ergo a portfolio mimicking Berkshire won’t include gold or Bitcoin. Likewise, Berkshire owns well over 100 companies. To mimic its volatility and performance, I must use a diversified approach. And, just to clarify, the purpose of this exercise was to build a portfolio that would be Better Than Berkshire. Porter’s Permanent Portfolio is outperforming Berkshire this year. And it is up almost 20% since September – with almost no volatility. For now, that’s the portfolio approach I endorse. But for the millions (!) of people who have simply been buying Berkshire over the past 50 years, they could very well prefer a 100% allocation to stocks that are alternatives to Berkshire. I created this portfolio for those folks.

Good work, but why no specific buy prices?

I think these last two Fridays were some of your best work! I am a long-time Stansberry Alliance member as well as a Porter & Co. Partner Pass member since shortly after you started it.

I would be surprised if you caught any flack from last week’s article! You just simply stated facts about Warren Buffet. You were very complimentary of him as he deserves but you simply highlighted some deficiencies in some of his decisions. I loved when you pointed out some alternatives he could have chosen. This was a good follow-up on individual stocks one should consider and why. My question for you is as follows:

I have my list of Permanent Portfolio names I am going to buy. Why don’t you publish the approximate entry price you would buy each of your Better Than Berkshire stocks at?

– Paid-up subscriber Tom”

Porter’s comment: Great question, Tom. The answer is, I built this as a thought experiment to be used as an index to compare to Berkshire. Indexes are “price agnostic.” With 30 positions, some will be bought at good prices, some at expensive prices. But the average is what matters, compared to Berkshire. If you’re looking for specific advice about what to buy now at a good price, see our current 3 “Best Buys.”

A Backdoor Way Into Elon’s Next Company

A rogue venture capitalist is revealing a backdoor ticker symbol into Elon’s next big company… giving you early, pre-IPO exposure.

He’s giving the ticker away to PORTER’S READERS – just for watching today.

Three Things To Know Before We Go…

1. The U.S. loses its last triple-A credit rating. Porter first predicted that America would lose its AAA-credit rating in 2010, in his legendary documentary The End Of America, which detailed the inevitable consequences of the U.S. Treasury bailing out the world’s financial system. Less than a year later, on August 2, 2011, Standard & Poor’s downgraded America’s credit.

Why didn’t the other leading rating agencies follow suit?

Two weeks after the S&P downgrade, the Securities and Exchange Commission (“SEC”) announced an investigation into S&P’s role in rating mortgage-backed securities. On August 23, 2011, S&P’s board of directors fired the company’s CEO in an attempt to placate the government. That didn’t work: the investigation led to a $5 billion lawsuit, which was settled for $1.3 billion. And S&P was forced to publicly retract its claim that the lawsuit was in retaliation for the credit downgrade. And yet people still believe that America is a free country and that firms, like S&P, have First Amendment protections. Thus it’s no surprise that rating agency Fitch waited more than a decade to follow S&P, downgrading America’s credit rating in August 2023. With deficits now approaching $2 trillion annually (6.4% of GDP) and interest expenses soaring, it’s no surprise that Moody’s has now downgraded America’s creditworthiness too. What’s sad is that none of these firms is willing to actually deliver the kind of warning that America desperately needs. Ray Dalio, the founder of Bridgewater Associates (the world’s largest hedge fund), is one of the few financial leaders who is willing to speak honestly about the U.S.’s inevitable financial collapse. Regarding Moody’s downgrade, Dalio said:

“You should know that credit ratings understate credit risks because they only rate the risk of the government not paying its debt. They don’t include the greater risk that the countries in debt will print money to pay their debts thus causing holders of the bonds to suffer losses from the decreased value of the money they’re getting (rather than from the decreased quantity of money they’re getting). Said differently, for those who care about the value of their money, the risks for U.S. government debt are greater than the rating agencies are conveying.”

Dalio also predicts that the U.S. government will reach $50 trillion in total debt by 2035.

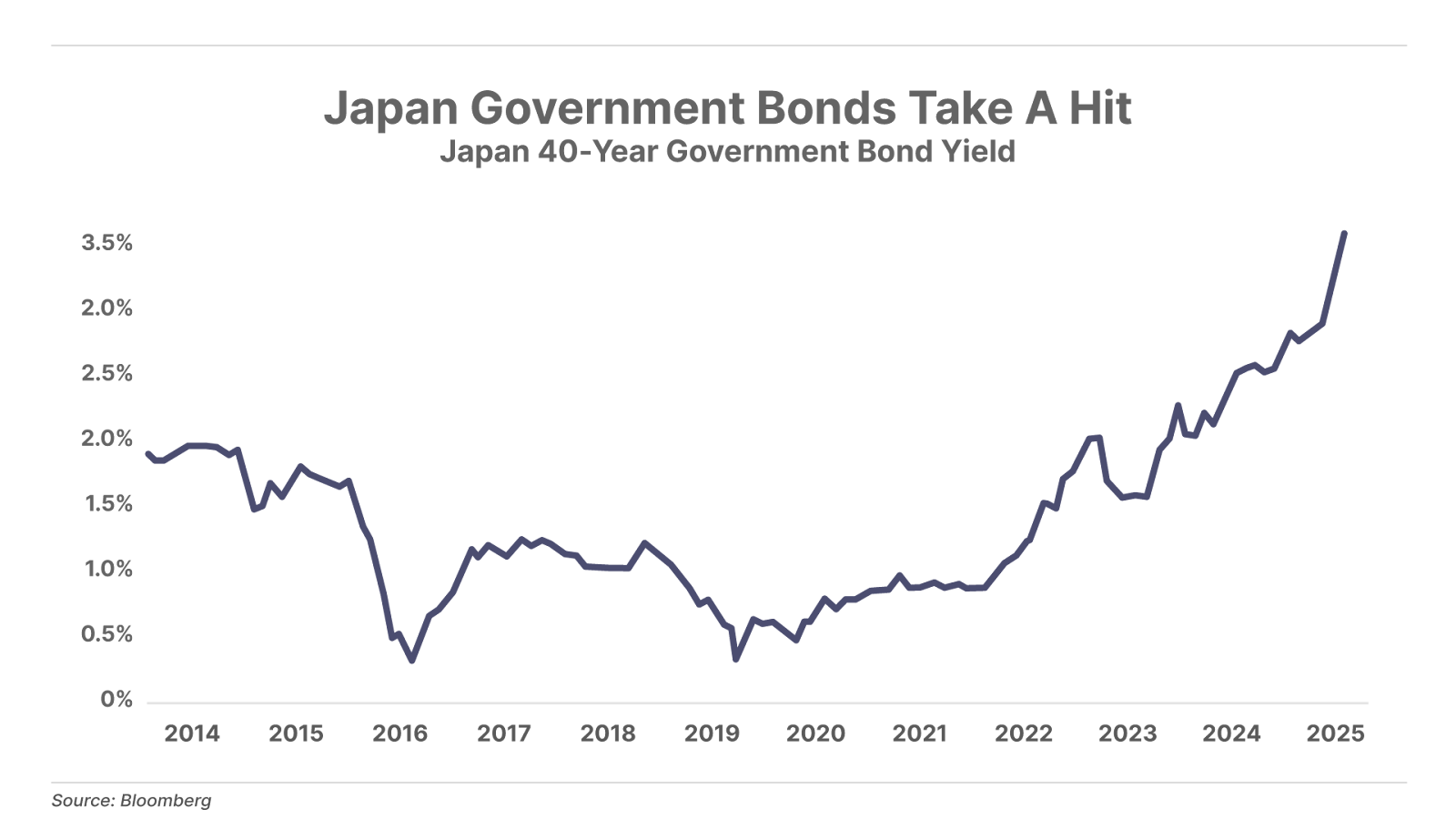

2. The U.S. is not alone. As dire as the U.S. government’s credit outlook is, Japan’s is arguably worse. In remarks this morning, Japanese Prime Minister Shigeru Ishiba admitted his country’s debt burden – currently equal to 240% of GDP, or roughly double that of the U.S. – is becoming a serious risk as global interest rates rise. “It is important to recognize the dangers of a society and a world with interest rates… Our country’s fiscal situation is undoubtedly extremely poor, worse than Greece’s.” Ishiba’s comments come as the yield on 40-year Japanese government bonds is hitting a multi-decade high near 3.50%.

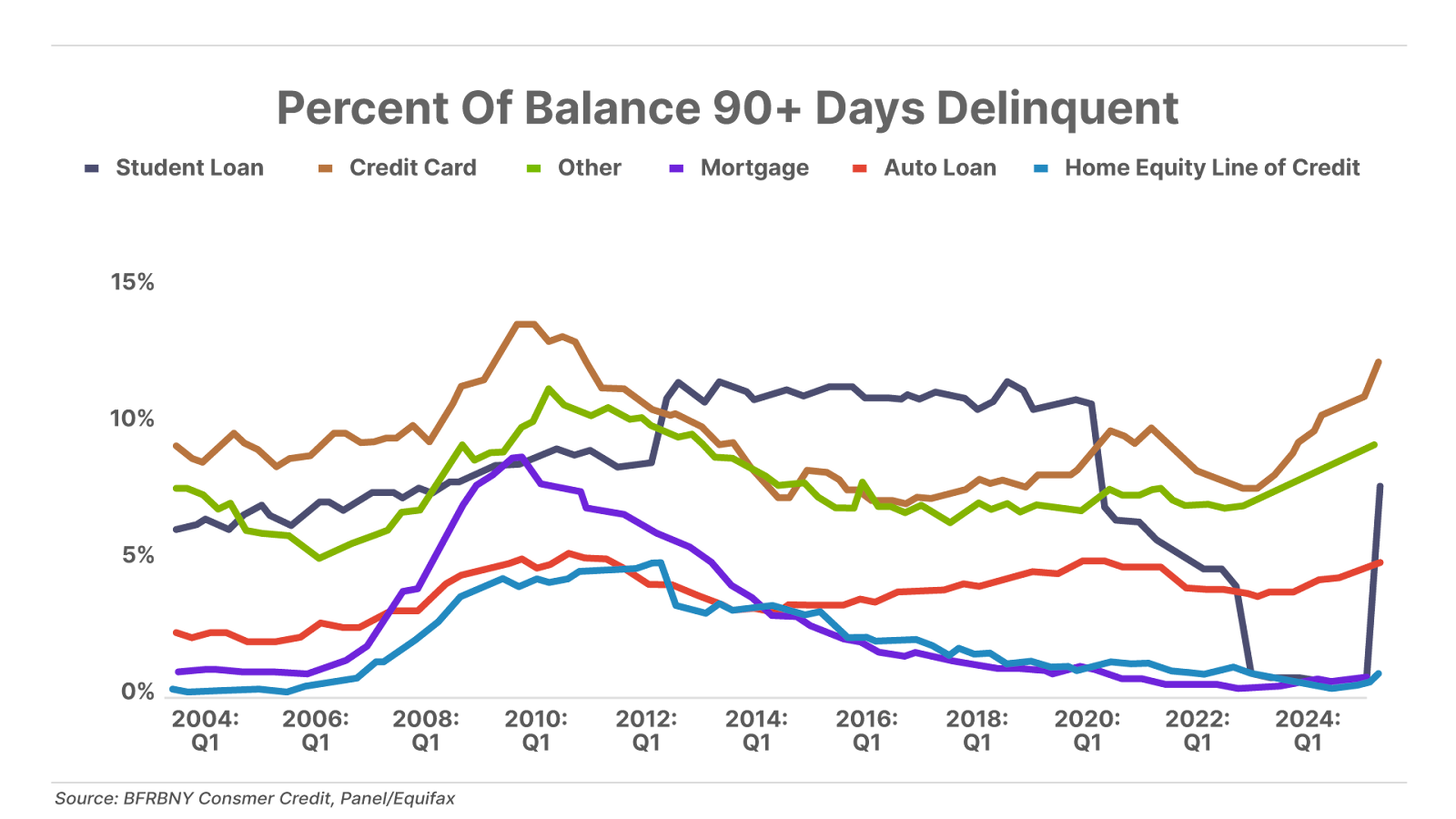

3. U.S. student loan collections resume, delinquencies rise. The Department of Education restarted collections on student loans earlier this year, following nearly five years of deferments. This has caused a surge in the delinquency rate on $1.6 trillion in student loans, from 0.5% to 7.7% in Q1. Analysts from JPMorgan estimate that 25% of all student loans could eventually fall into delinquency status, a level that would be a significant hit to the discretionary spending that fuels America’s economy.

And One More Thing… Better Than Berkshire

On Friday, Porter constructed a portfolio called Better Than Berkshire, using publicly traded stocks that are analogous to Berkshire’s holdings. And today, he answered reader questions about that portfolio and its makeup. So we ask:

Tell me what you think: [email protected]

Mailbag

I am a 64-year-old female who has worked since I was 15. I live in Central Missouri. I am a certified nursing assistant who works in hospice. I work paycheck to paycheck and have no savings. Most investments take thousands of dollars if a person wants to see any kind of return. How is it possible for anyone in my position to ever possibly invest and to make any substantial return that would even be worth the time and effort of investing. And how do I choose the investment that will not just take my money and leave me that much further behind in paying my bills?

I understand that you personally have enough money that you could put $100,000 in an investment and it wouldn’t hurt you if you lost that. Unfortunately, normal people in the world can barely afford to invest $100 and if they lost that, to most of us that is a lot of money. It is very frustrating to me that apparently investing is a rich person’s game and not a normal person’s game.

Frankie H.”

Porter’s comment: Hi Frankie —

Thanks for your note.

The first step toward wealth is learning to save money. I know you’ll reply that there’s no way for you to save, so you’ll have to think carefully about how you can change those circumstances. I’ve consistently saved half of my after-tax income, every year, for my entire life, starting when I was mowing lawns as a teenager.

After that, I’d focus on making long-term investments in good businesses that you personally understand.

Good investing,

Porter Stansberry

Stevenson, Maryland

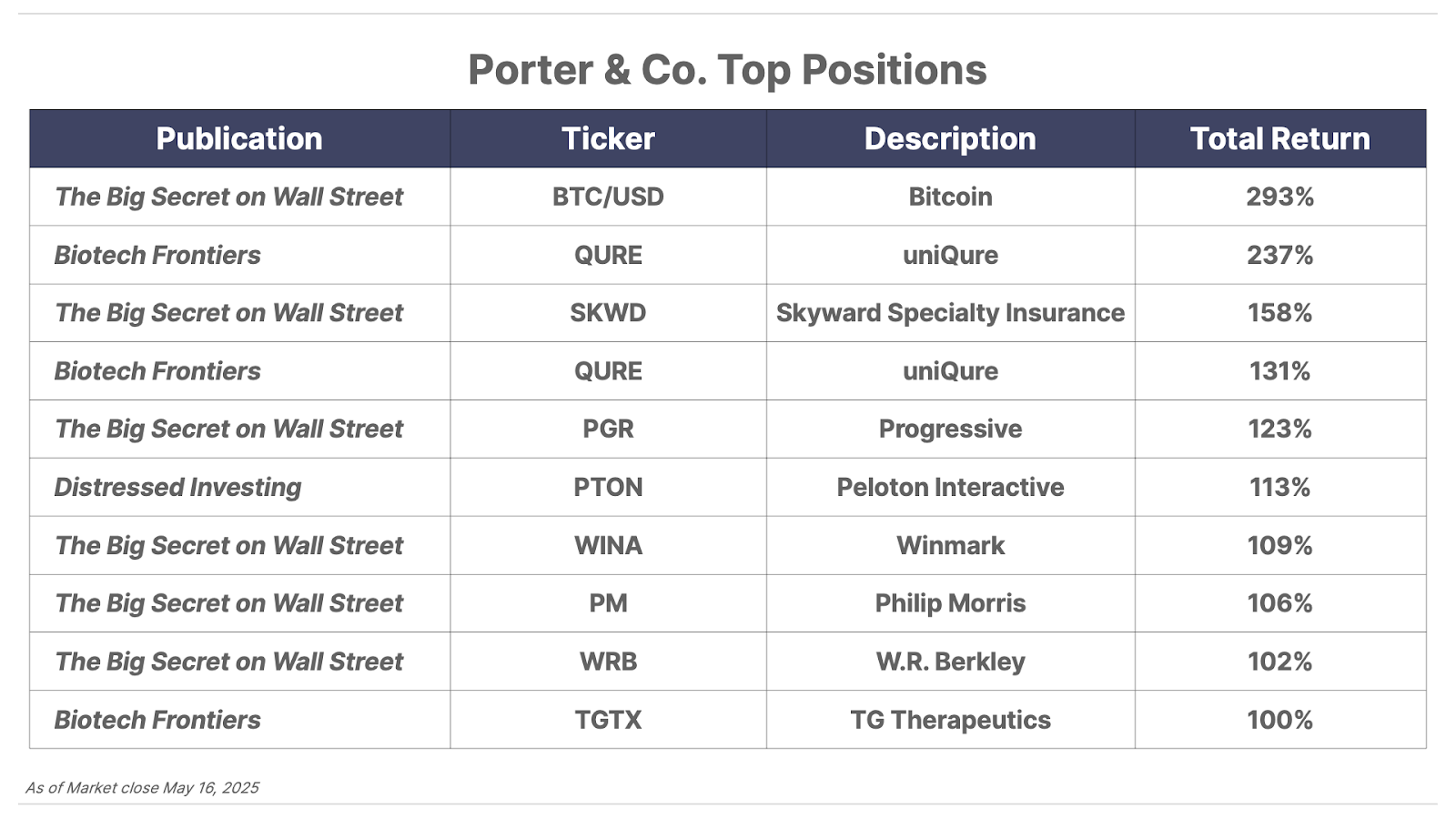

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.